Cigna earnings beat by $0.04, revenue topped estimates

Ibotta Inc (NASDAQ:IBTA) released its first quarter 2025 financial results on May 14, exceeding revenue and adjusted EBITDA guidance despite ongoing business model transformation. The company’s stock, which had previously suffered a significant drop following Q4 2024 results, showed signs of recovery with shares rising 13.31% in after-hours trading to $56.80.

Quarterly Performance Highlights

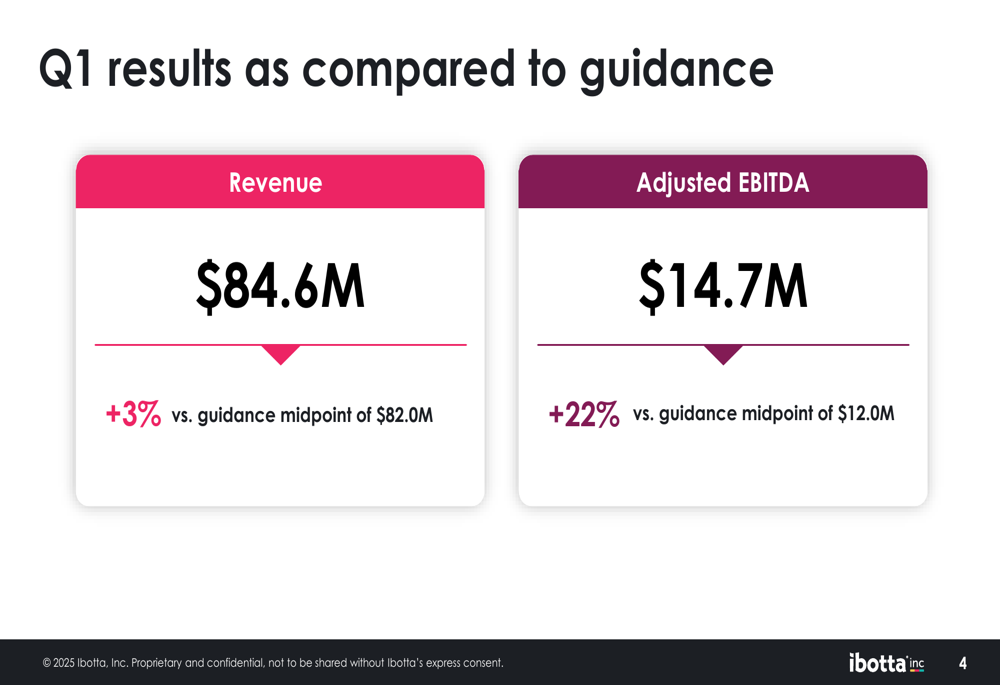

Ibotta reported Q1 2025 revenue of $84.6 million, representing a 3% increase year-over-year and exceeding the company’s guidance midpoint of $82.0 million by 3%. Adjusted EBITDA came in at $14.7 million, surpassing guidance by 22%, though the adjusted EBITDA margin contracted to 17% from 28% in the prior-year period.

As shown in the following chart comparing actual results to guidance:

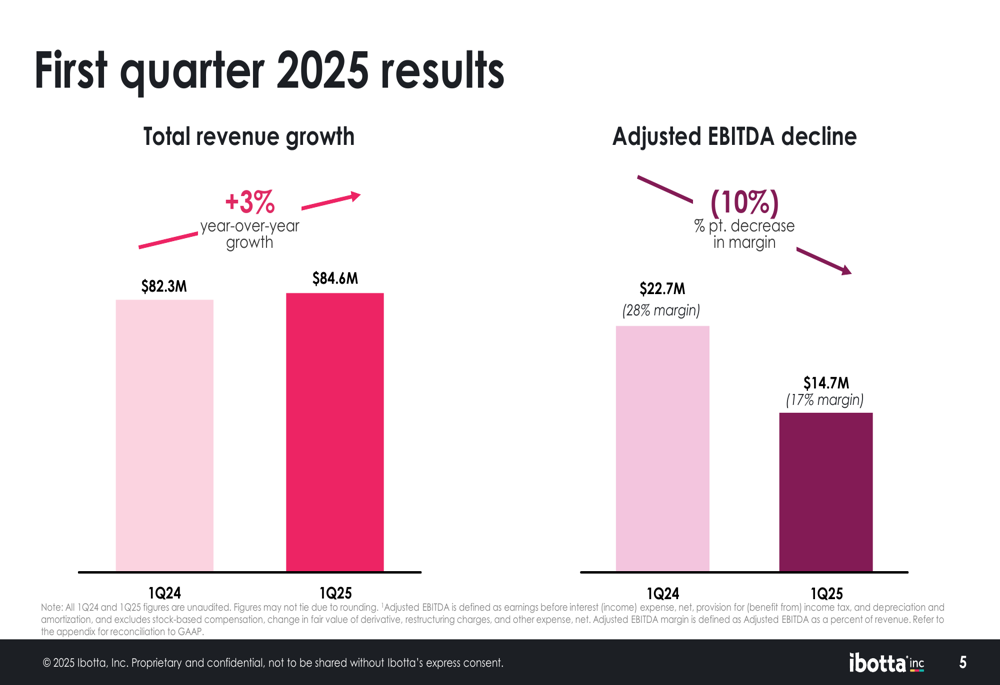

The company’s total revenue grew modestly from $82.3 million in Q1 2024 to $84.6 million in Q1 2025, while adjusted EBITDA declined from $22.7 million to $14.7 million, reflecting significant margin compression:

Detailed Financial Analysis

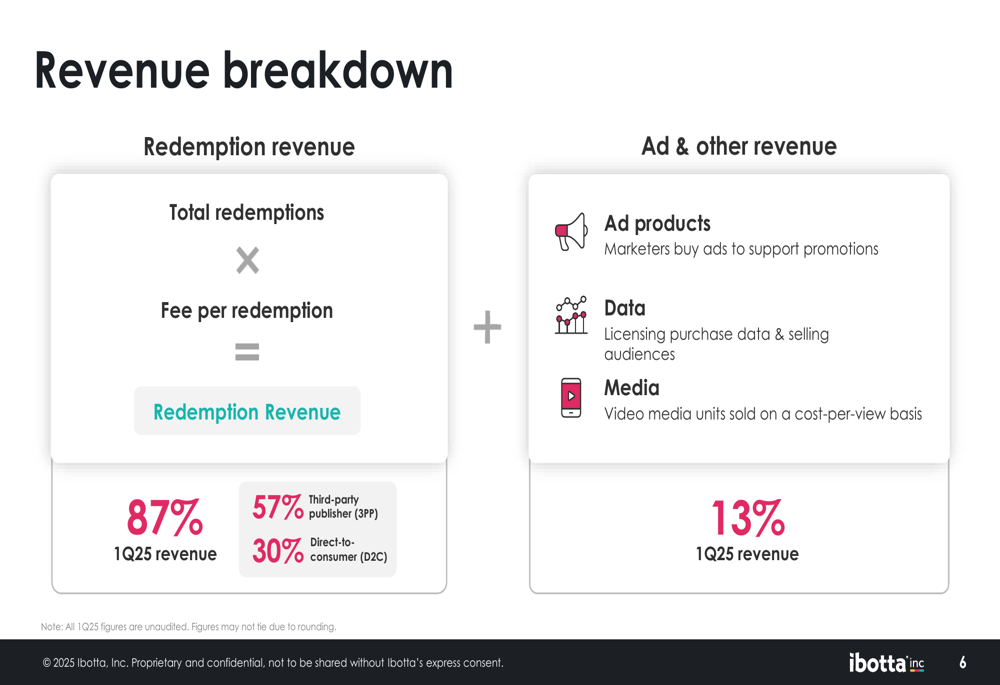

Ibotta’s revenue composition reveals a business in transition, with redemption revenue accounting for 87% of total revenue and advertising and other revenue making up the remaining 13%. Within redemption revenue, third-party publishers now represent 57% of total revenue, while direct-to-consumer (D2C) accounts for 30%.

The following breakdown illustrates this revenue composition:

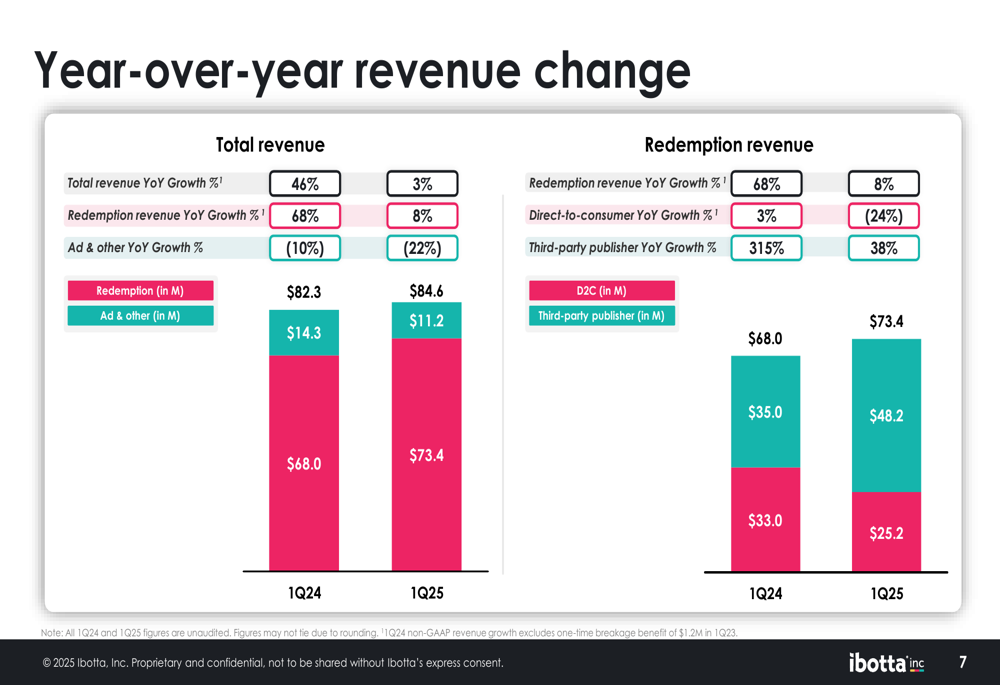

The most notable trend in Ibotta’s business is the significant shift from direct-to-consumer to third-party publisher revenue. While overall redemption revenue grew 8% year-over-year, this masked divergent performance between segments. Third-party publisher revenue surged 38% (from $33.0 million to $48.2 million), while direct-to-consumer revenue declined 24% (from $35.0 million to $25.2 million). Additionally, advertising and other revenue fell 22%.

This revenue transformation is clearly illustrated in the following chart:

The driver behind Ibotta’s redemption revenue growth was a 37% increase in redeemers, which grew from 12.5 million in Q1 2024 to 17.1 million in Q1 2025. However, this was partially offset by decreases in both redemptions per redeemer (from 5.7 to 4.8) and redemption revenue per redemption (from $0.95 to $0.89).

Ibotta’s profitability metrics showed pressure during the quarter, with non-GAAP gross profit margin declining from 87% to 81% year-over-year, while non-GAAP operating expenses increased from 61% to 65% of revenue. This margin compression reflects the company’s transition costs as it shifts its business model.

The following chart illustrates these margin trends:

Strategic Initiatives

Ibotta’s presentation highlights the company’s strategic pivot toward third-party publishers. The number of third-party redeemers increased from 10.6 million in Q1 2024 to 15.4 million in Q1 2025, a 45% increase. This growth has been driven by partnerships with major retailers including Walmart+ (launched August 2022), Dollar General (NYSE:DG) (launched July 2023), and Instacart (NASDAQ:CART) (launched November 2024).

Meanwhile, the company’s direct-to-consumer business continues to decline, with D2C redeemers decreasing from 1.9 million to 1.7 million year-over-year, and redemptions per redeemer falling from 14.4 to 13.1.

This strategic shift aligns with comments from the previous quarter’s earnings call, where CEO Brian Leach emphasized the company’s long-term focus and efforts to "retool" the business. The Q1 results suggest this transformation is progressing, though not without challenges to profitability in the near term.

Forward-Looking Statements

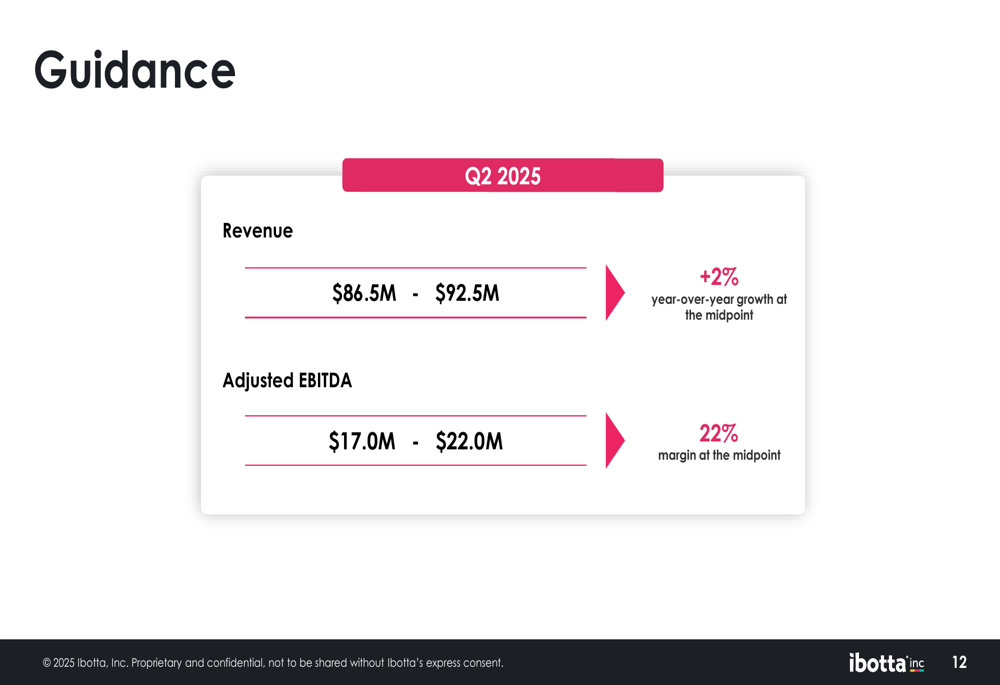

For the second quarter of 2025, Ibotta provided guidance for revenue between $86.5 million and $92.5 million, representing approximately 2% year-over-year growth at the midpoint. Adjusted EBITDA is projected to be between $17.0 million and $22.0 million, with a 22% margin at the midpoint.

The following chart details the Q2 2025 guidance:

This guidance suggests a sequential improvement in both revenue and adjusted EBITDA margin compared to Q1 2025, potentially indicating that the company’s strategic initiatives are beginning to yield positive results. The projected margin improvement from Q1’s 17% to Q2’s expected 22% would be particularly significant if achieved.

The Q1 results and Q2 guidance represent a potential turning point for Ibotta following its challenging Q4 2024, when the company missed earnings expectations and saw its stock drop sharply. The market’s positive after-hours reaction to these results suggests investors may be gaining confidence in the company’s strategic direction, though margin pressure remains a concern to monitor in coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.