Intel stock spikes after report of possible US government stake

Introduction & Market Context

Ibotta Inc (NYSE:IBTA) delivered its second quarter 2024 earnings presentation on August 13, 2024, highlighting strong revenue growth and a significant new partnership with Instacart (NASDAQ:CART). The digital promotions technology company, which connects consumer packaged goods (CPG) brands with consumers through its Ibotta Performance Network (IPN), reported continued expansion of its third-party publisher business while facing challenges in its direct-to-consumer segment.

The company’s stock has experienced significant volatility over the past year, trading at $32.80 as of August 8, 2025, well below its 52-week high of $79.80 but slightly above its 52-week low of $31.40. In premarket trading on August 11, 2025, the stock was up 0.98% to $33.12.

Quarterly Performance Highlights

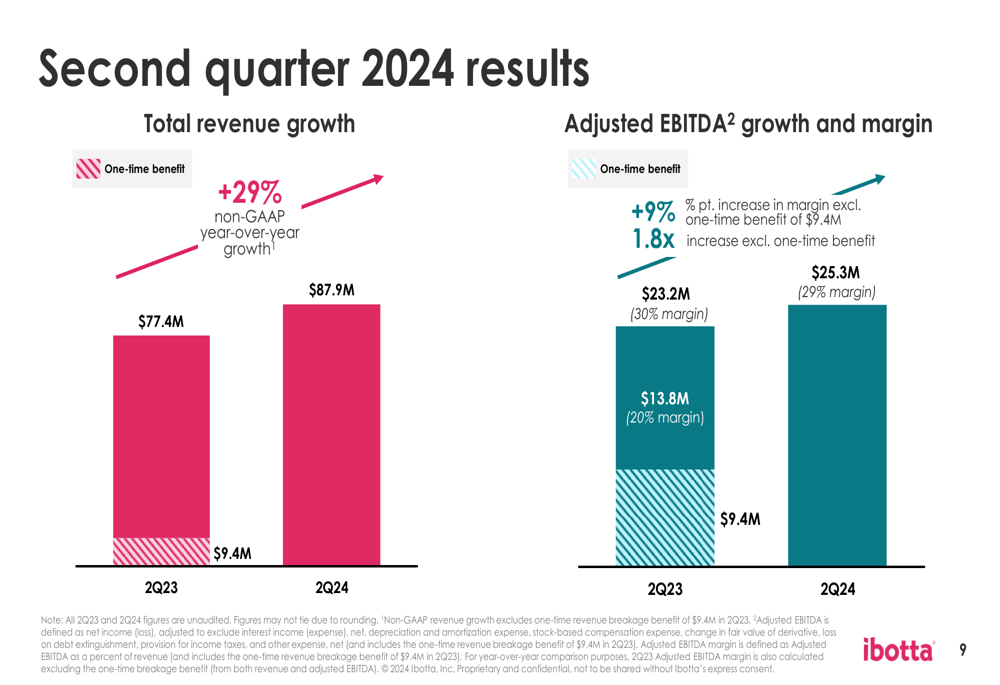

Ibotta reported total revenue of $87.9 million for Q2 2024, representing 29% year-over-year non-GAAP growth compared to $77.4 million in Q2 2023. Adjusted EBITDA reached $25.3 million with a 29% margin, up from $13.8 million (20% margin) in the same period last year.

As shown in the following chart of quarterly financial results:

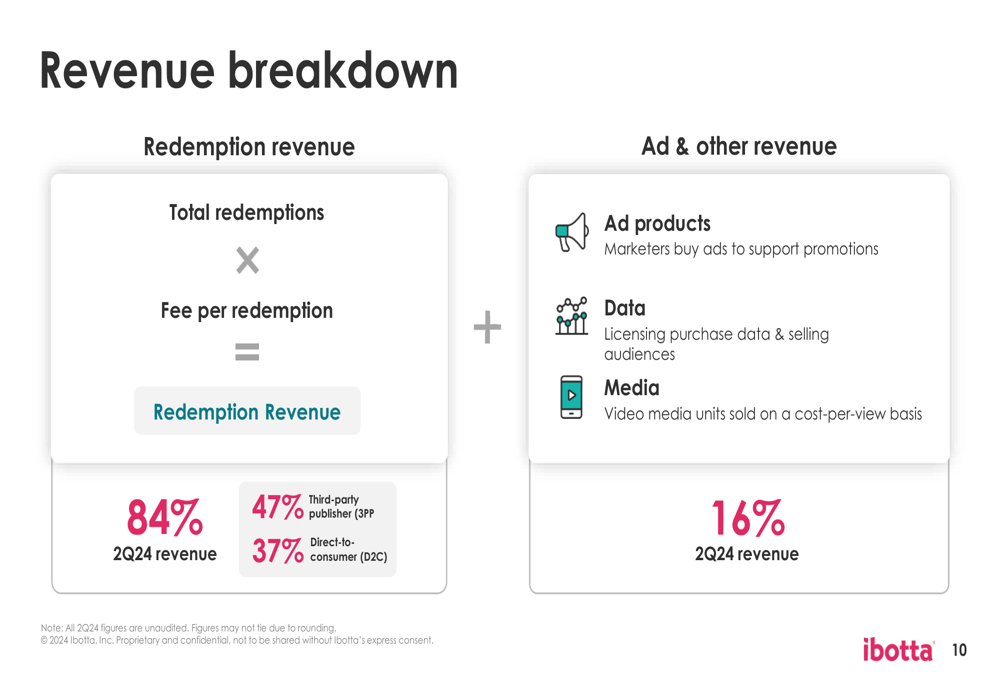

The company’s revenue breakdown reveals that 84% comes from redemption revenue, with the remaining 16% from advertising and other sources. Within the redemption revenue category, 47% is generated by third-party publishers while 37% comes from direct-to-consumer channels.

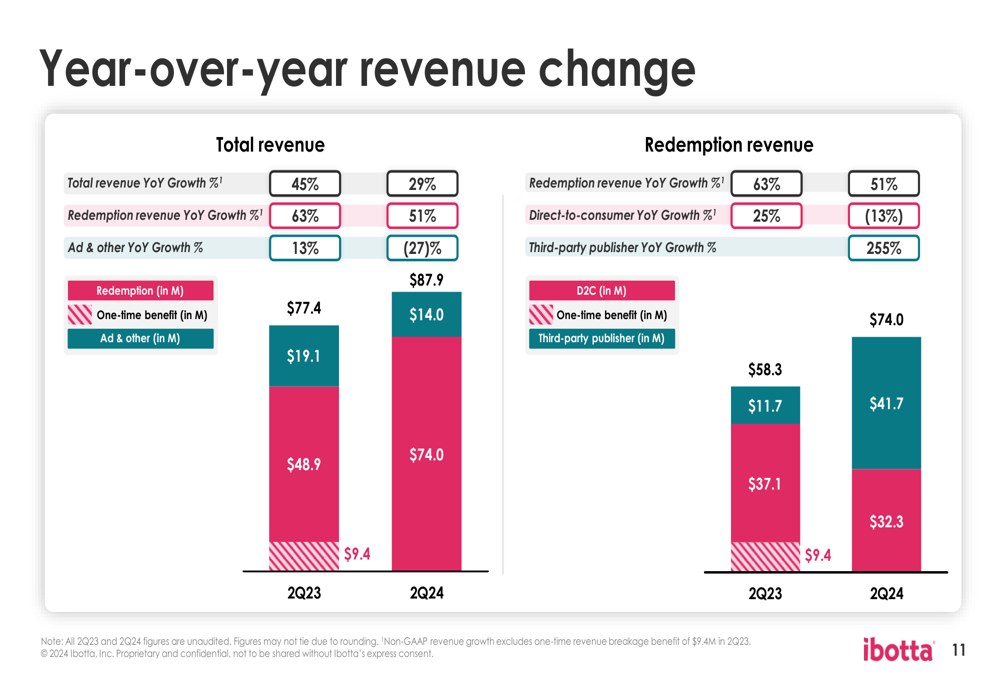

A closer look at year-over-year revenue changes shows divergent performance across business segments. While total revenue grew 29% on a non-GAAP basis and redemption revenue increased 51%, direct-to-consumer revenue declined 13% and advertising revenue fell 27%.

Strategic Initiatives

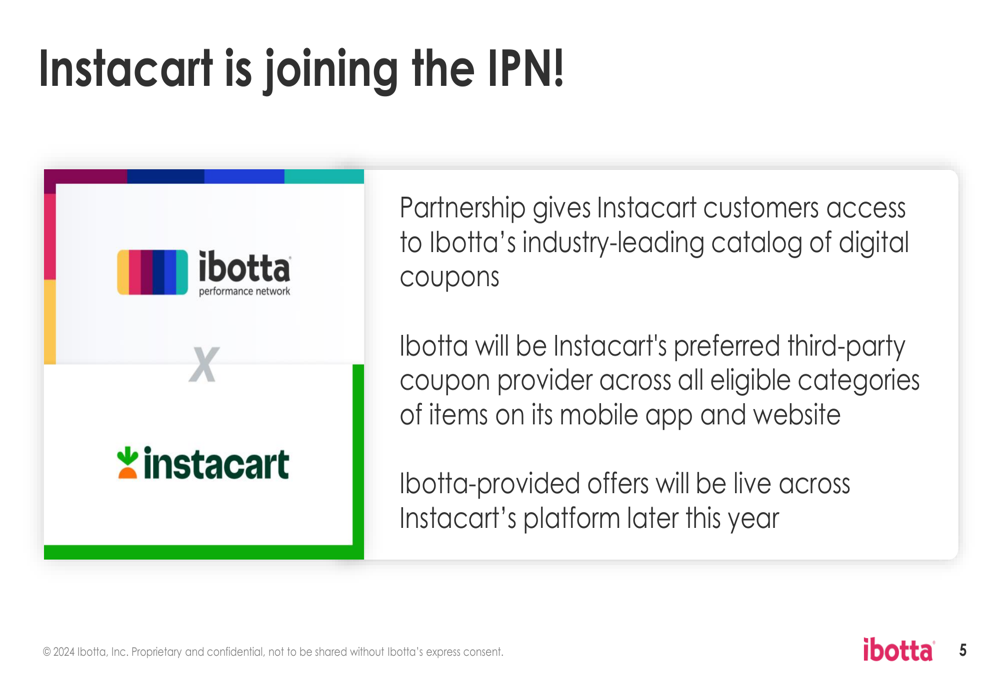

The highlight of Ibotta’s strategic announcements was a major partnership with Instacart, which will join the Ibotta Performance Network. This partnership will make Ibotta’s digital coupons available to Instacart customers, with Ibotta becoming Instacart’s preferred third-party coupon provider. The integration is expected to go live across Instacart’s platform later this year.

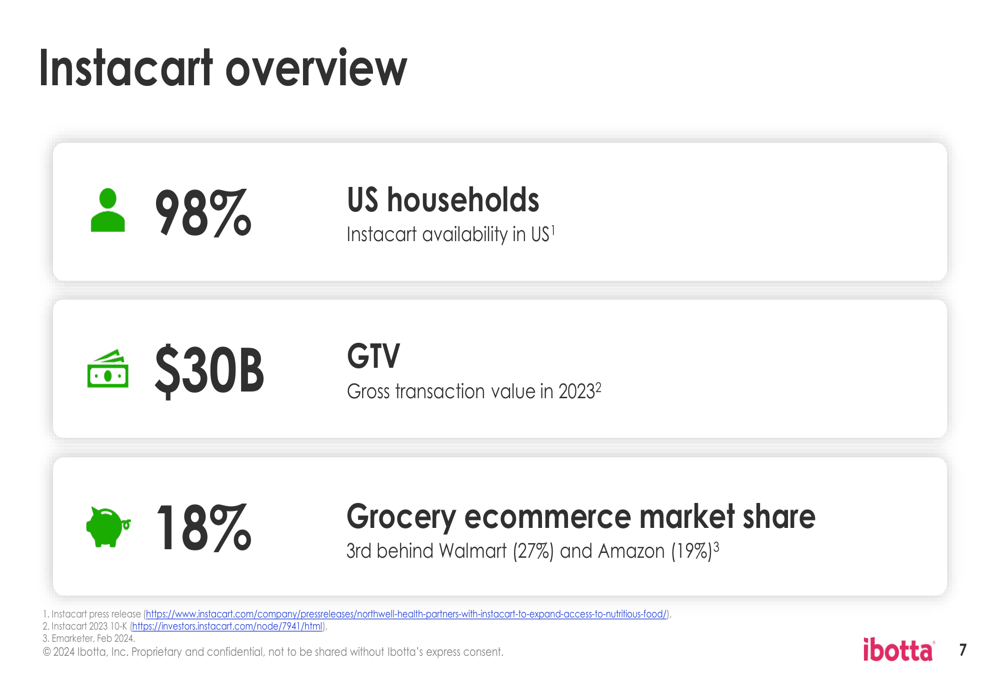

The strategic significance of this partnership is illustrated by Instacart’s market position:

Instacart represents a substantial addition to Ibotta’s network, with availability to 98% of US households, $30 billion in Gross Transaction (JO:NTUJ) Value, and an 18% share of the grocery ecommerce market, ranking third behind Walmart (NYSE:WMT) (27%) and Amazon (NASDAQ:AMZN) (19%).

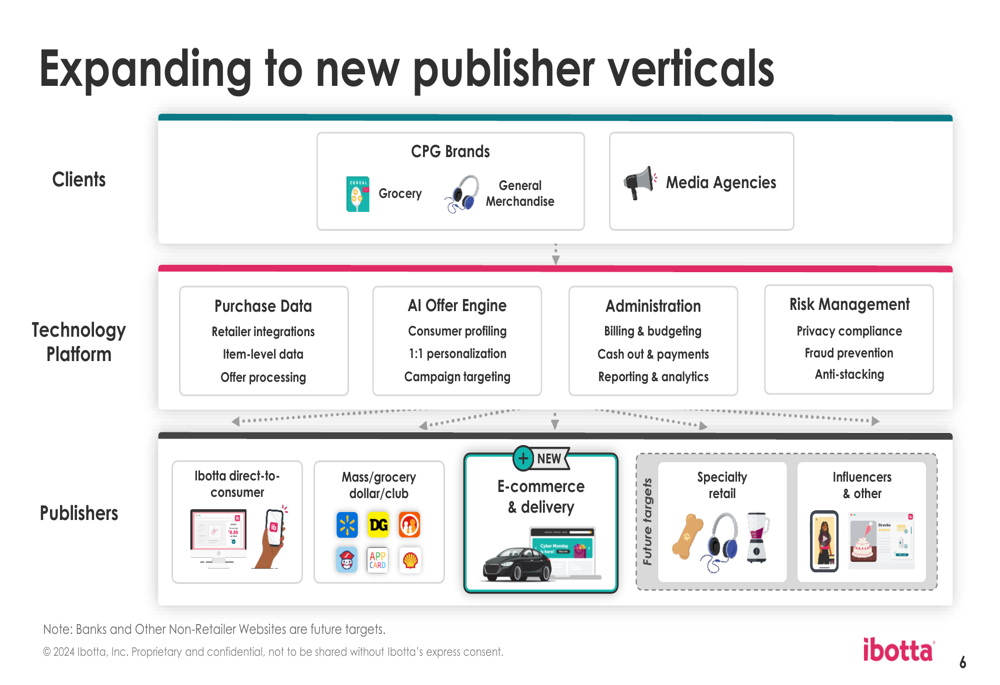

Beyond the Instacart partnership, Ibotta is expanding its publisher network across multiple verticals, creating more connections between CPG brands and consumers through various channels.

Detailed Financial Analysis

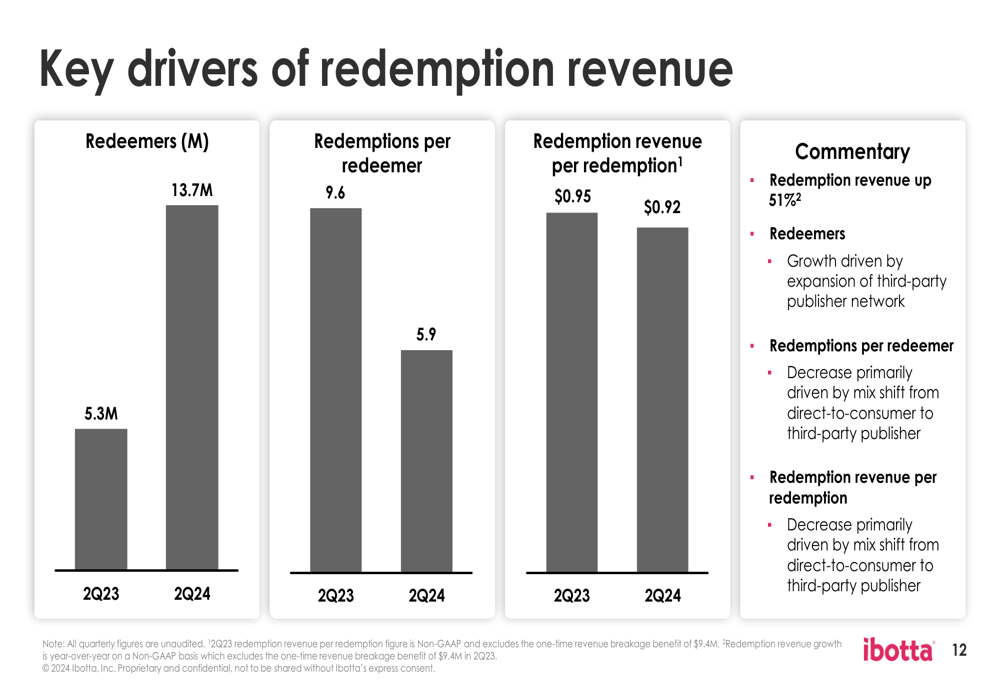

The key driver of Ibotta’s redemption revenue growth has been a significant increase in the number of redeemers, which grew from 5.3 million to 13.7 million. However, this was partially offset by decreases in both redemptions per redeemer (from 9.6 to 5.9) and redemption revenue per redemption (from $0.95 to $0.92).

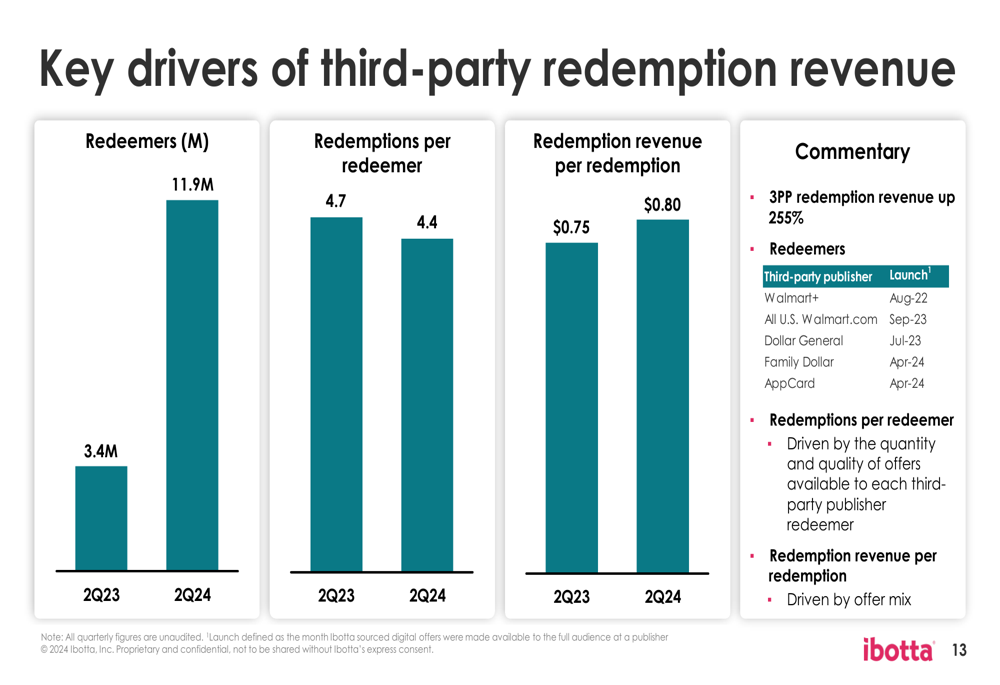

The contrasting performance between third-party publisher and direct-to-consumer segments is particularly noteworthy. Third-party publisher redemption revenue surged 255%, driven by an increase in redeemers from 3.4 million to 11.9 million.

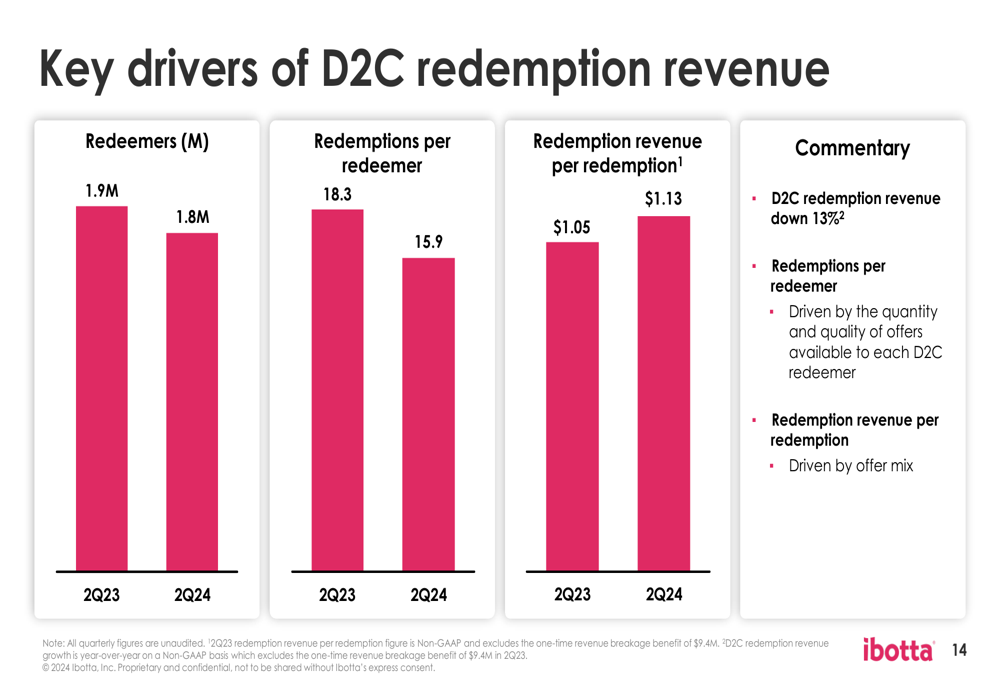

Meanwhile, direct-to-consumer redemption revenue declined 13%, with redeemers decreasing from 1.9 million to 1.8 million and redemptions per redeemer falling from 18.3 to 15.9. This was partially offset by an increase in redemption revenue per redemption from $1.05 to $1.13.

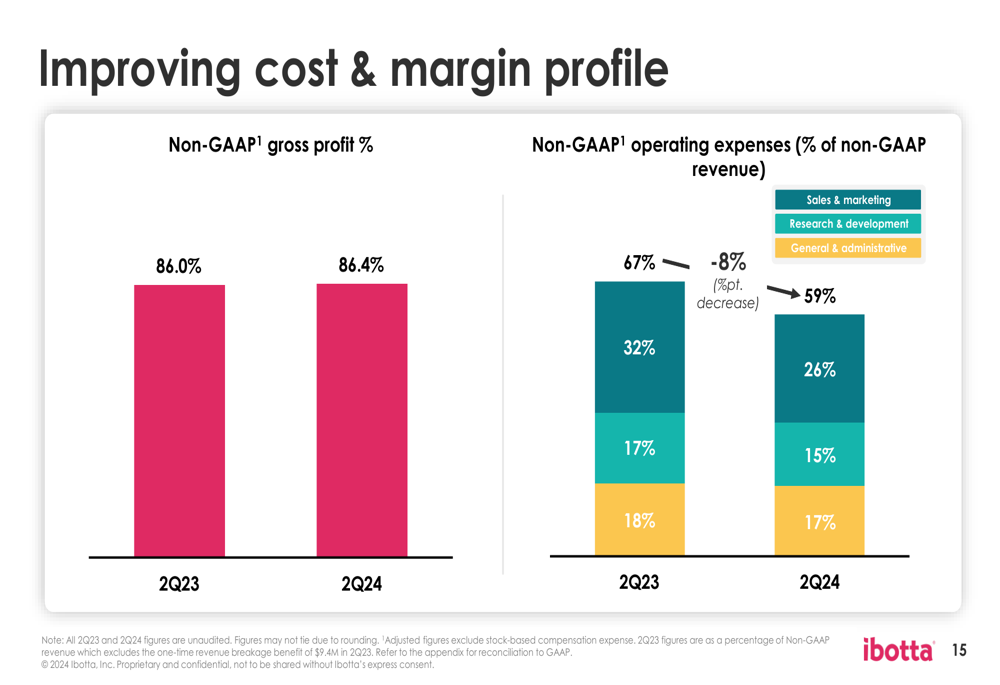

Ibotta has also made progress in improving its cost structure and margin profile. Non-GAAP gross profit percentage increased slightly from 86.0% to 86.4%, while non-GAAP operating expenses as a percentage of revenue decreased from 67% to 59%. Sales and marketing expenses saw the most significant reduction, falling from 32% to 26% of revenue.

Forward-Looking Statements

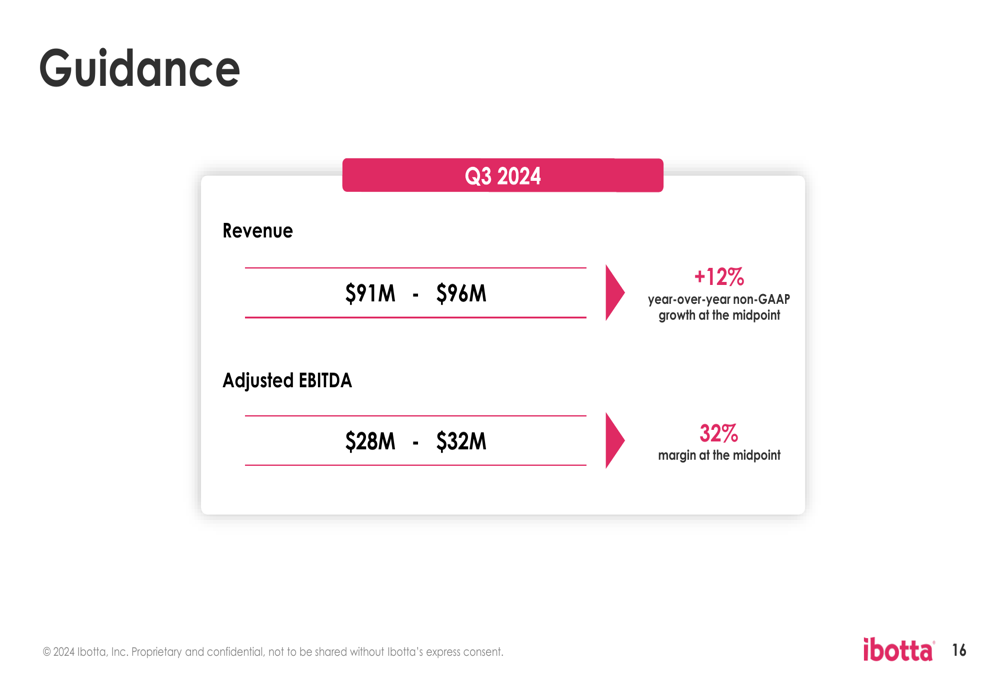

For the third quarter of 2024, Ibotta projects revenue between $91 million and $96 million, representing approximately 12% year-over-year non-GAAP growth. Adjusted EBITDA is expected to be between $28 million and $32 million, with a 32% margin.

The company highlighted several investment strengths, including its large addressable market, AI-enabled platform with valuable data assets, expansive partner network, solid double-digit revenue growth, and increasing profitability.

Looking ahead, Ibotta’s growth strategy appears focused on expanding its third-party publisher network while managing the decline in its direct-to-consumer business. The Instacart partnership represents a significant opportunity to accelerate this transition and potentially reverse recent stock price declines. However, investors will be watching closely to see if the company can maintain its projected growth trajectory and continue improving profitability metrics in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.