Nvidia among investors in xAI’s $20 bln capital raise- Bloomberg

Introduction & Market Context

IDEX Corporation (NYSE:IEX) shares plunged 9.21% to $168.12 on Wednesday after the company’s second-quarter 2025 earnings presentation revealed a cautious outlook for the remainder of the year, despite reporting results that exceeded expectations. The stock had already dropped 5.63% in pre-market trading, signaling investor concerns about the company’s forward guidance.

The industrial manufacturer reported modest organic growth of 1% for the quarter, with total sales reaching $865 million, up 7% year-over-year when including acquisitions and currency effects. However, management’s commentary about "inconsistent day rate patterns" and "slower customer decision-making" impacting the second half forecast appears to have overshadowed the positive quarterly performance.

Quarterly Performance Highlights

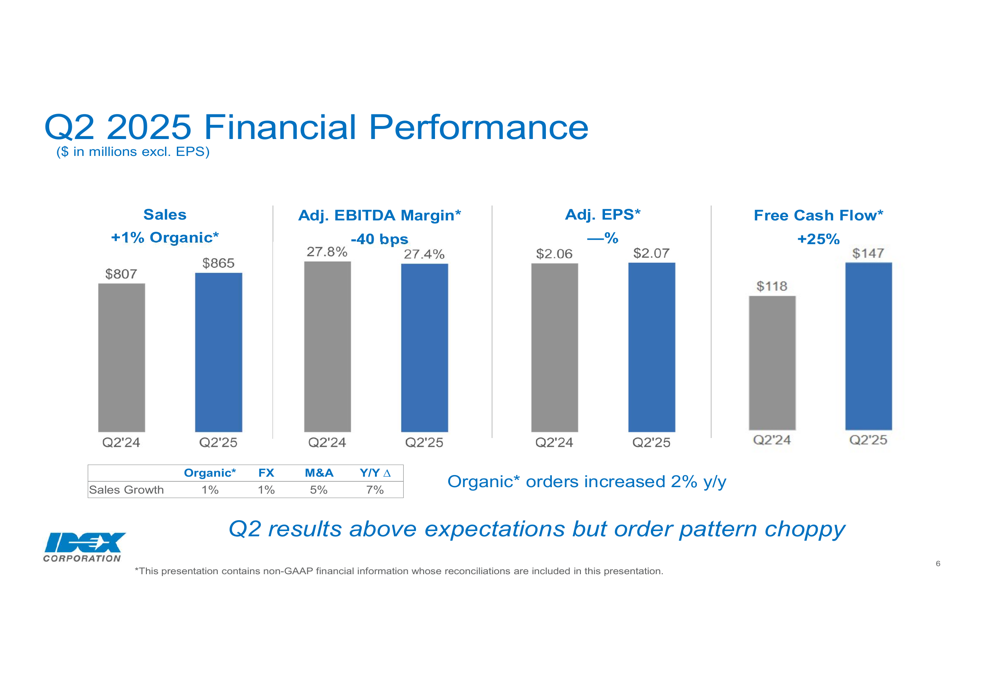

IDEX delivered mixed financial results for the second quarter of 2025. The company reported sales of $865 million, representing a 7% increase from $807 million in Q2 2024. This growth was primarily driven by acquisitions (5%) and favorable currency effects (1%), with organic growth contributing just 1%.

Adjusted EBITDA margin decreased slightly to 27.4%, down 40 basis points from 27.8% in the same period last year. Adjusted earnings per share remained nearly flat at $2.07 compared to $2.06 in Q2 2024. A bright spot was free cash flow, which increased 25% to $147 million from $118 million in the prior year period.

As shown in the following financial performance summary:

Orders showed some improvement with organic growth of 2% year-over-year, but the company characterized the order pattern as "choppy," suggesting inconsistent demand across its markets.

Segment Analysis

IDEX’s three business segments delivered varying results, reflecting the uneven market conditions facing the company.

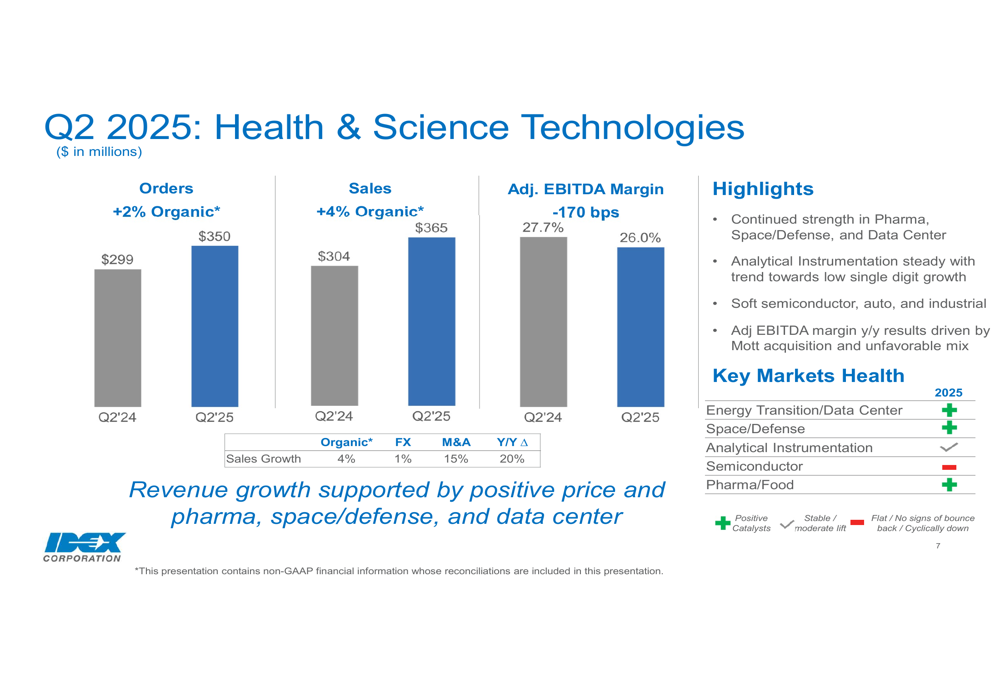

The Health & Science Technologies (HST) segment was the strongest performer, with organic sales growth of 4% to $365 million. This segment benefited from continued strength in pharmaceutical, space/defense, and data center markets. However, adjusted EBITDA margin declined 170 basis points to 26.0%, primarily due to the Mott acquisition and unfavorable product mix.

The segment’s performance is detailed in the following chart:

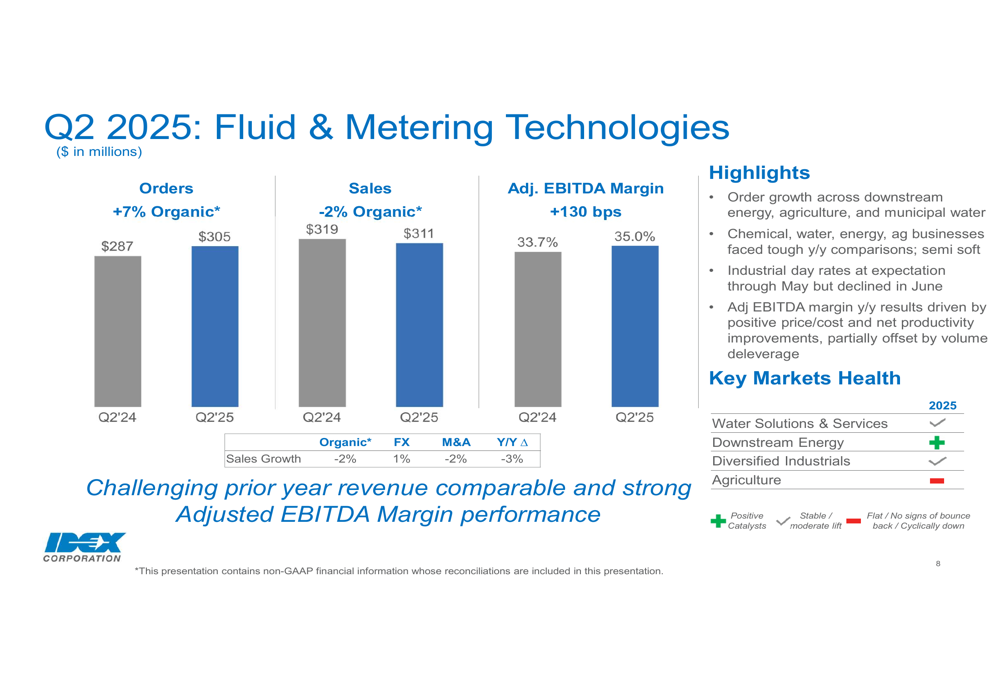

In contrast, the Fluid & Metering Technologies (FMT) segment experienced a 2% organic sales decline to $311 million, facing tough year-over-year comparisons. Despite the sales decrease, this segment achieved the highest adjusted EBITDA margin at 35.0%, an improvement of 130 basis points from Q2 2024, driven by positive price/cost dynamics and productivity improvements.

The FMT segment’s results are illustrated here:

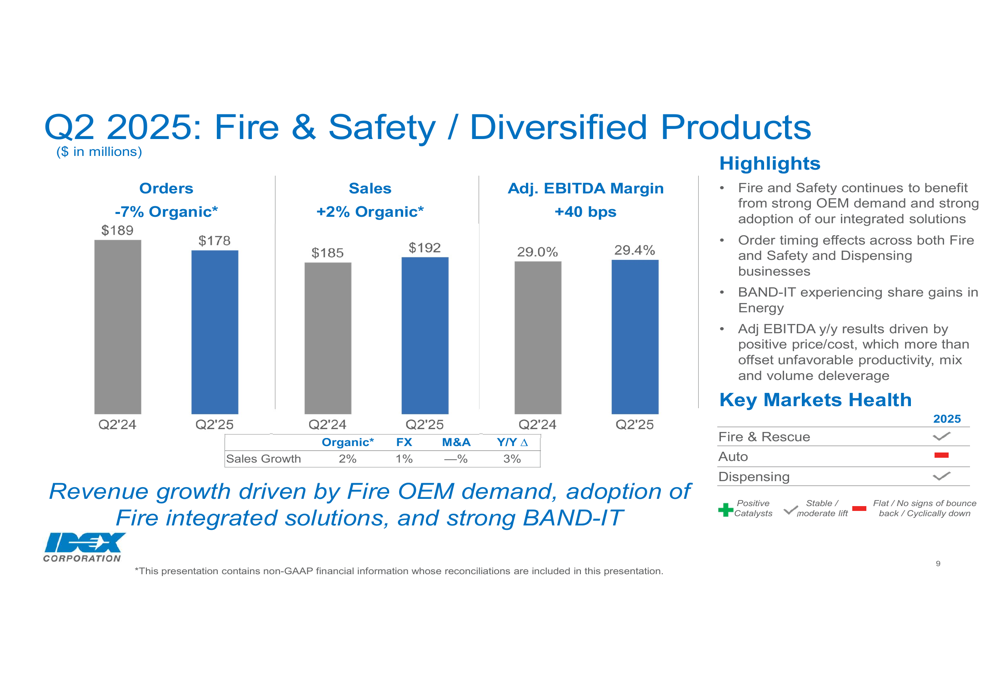

The Fire & Safety / Diversified Products (FSDP) segment delivered 2% organic sales growth to $192 million, with adjusted EBITDA margin improving 40 basis points to 29.4%. This segment benefited from strong OEM demand in the fire and safety business and share gains in the energy sector for BAND-IT products.

The FSDP segment’s performance is summarized in this chart:

Strategic Initiatives

Despite the challenging market environment, IDEX continues to execute on its strategic growth initiatives. The company highlighted its platform optimization and delayering plans, which remain on track. Management emphasized three key value drivers: organic growth, inorganic growth through acquisitions, and margin expansion.

The company recently acquired Micro-LAM, a manufacturer of high-precision custom optical components and laser-assisted machining devices. This acquisition is expected to generate approximately $25 million in revenue for 2025 and be accretive to non-GAAP EPS in the first year. The acquisition complements IDEX’s Materials Science Solutions platform and aligns with its footprint in the space and defense segments.

IDEX also highlighted its capital deployment strategy, focusing on both growth investments and returning capital to shareholders. The company expects to generate over 100% free cash flow conversion in 2025, providing financial flexibility for organic growth initiatives, tuck-in acquisitions, and shareholder returns through dividends and share repurchases.

Forward-Looking Statements

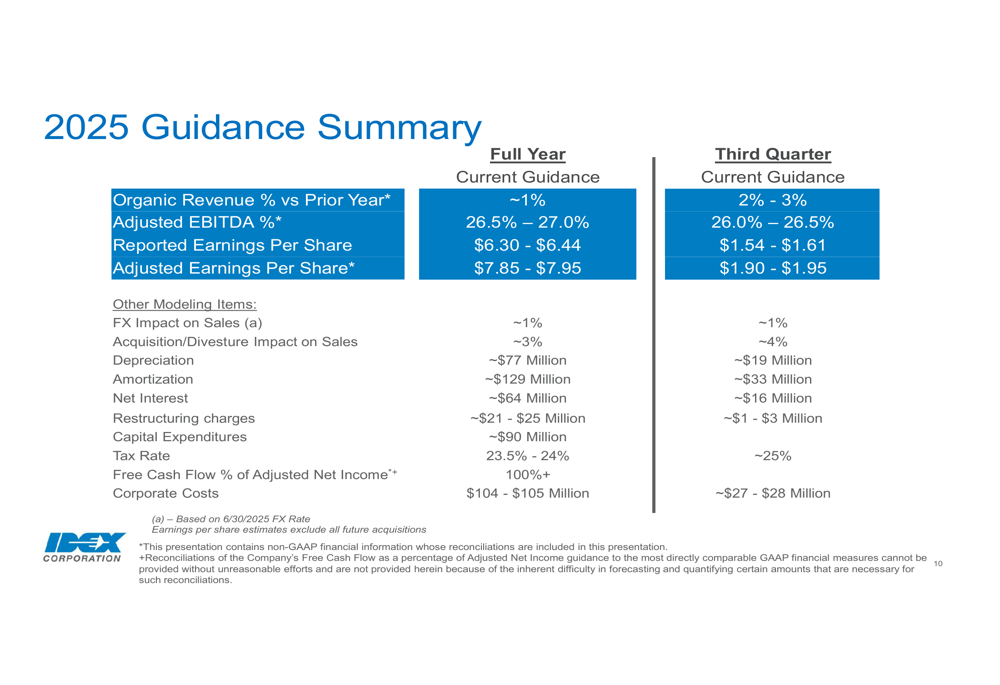

IDEX’s guidance for the remainder of 2025 appears to be the primary driver of the negative market reaction. The company now expects full-year organic revenue growth of approximately 1%, which represents a reduction from the previous guidance of 1-3% mentioned during the Q1 earnings call.

For the third quarter of 2025, IDEX projects organic revenue growth of 2-3%, adjusted EBITDA margin of 26.0-26.5%, and adjusted earnings per share of $1.90-$1.95. The full-year adjusted EPS guidance range is $7.85-$7.95.

The detailed guidance is presented in the following summary:

Management attributed the cautious outlook to inconsistent day rate patterns and slower customer decision-making, particularly in industrial markets. The company noted that industrial day rates were at expectation through May but declined in June, suggesting potential softening in demand.

While certain markets like pharmaceutical, space/defense, and data centers remain strong, the company faces challenges in semiconductor, automotive, and industrial sectors. The agricultural market was also identified as an area of weakness in the outlook.

The reduced guidance and cautious commentary about market conditions appear to have overshadowed the better-than-expected Q2 results, leading to the significant stock decline. Investors seem concerned about the company’s growth prospects for the remainder of 2025, despite IDEX’s strong cash flow generation and ongoing strategic initiatives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.