September looms as a risk month for stocks, Yardeni says

Introduction & Market Context

IMCD NV ( AMS (VIE:AMS2):AS:IMCD), a leading global distributor of specialty chemicals and ingredients, presented its half-year 2025 results on July 30, 2025. The presentation, delivered by CEO Marcus Jordan and CFO Hans Kooijmans, revealed a company navigating challenging market conditions while continuing its strategic expansion through acquisitions.

The specialty chemicals distributor, currently trading at €111.60, has seen its stock decline by 1.67% following the presentation. This represents a significant drop from the €120.10 closing price following its Q1 2025 results, suggesting investors may have concerns about the company’s performance trajectory.

As shown in the company’s executive team slide, IMCD’s leadership remains focused on its long-term strategy despite near-term headwinds:

Executive Summary

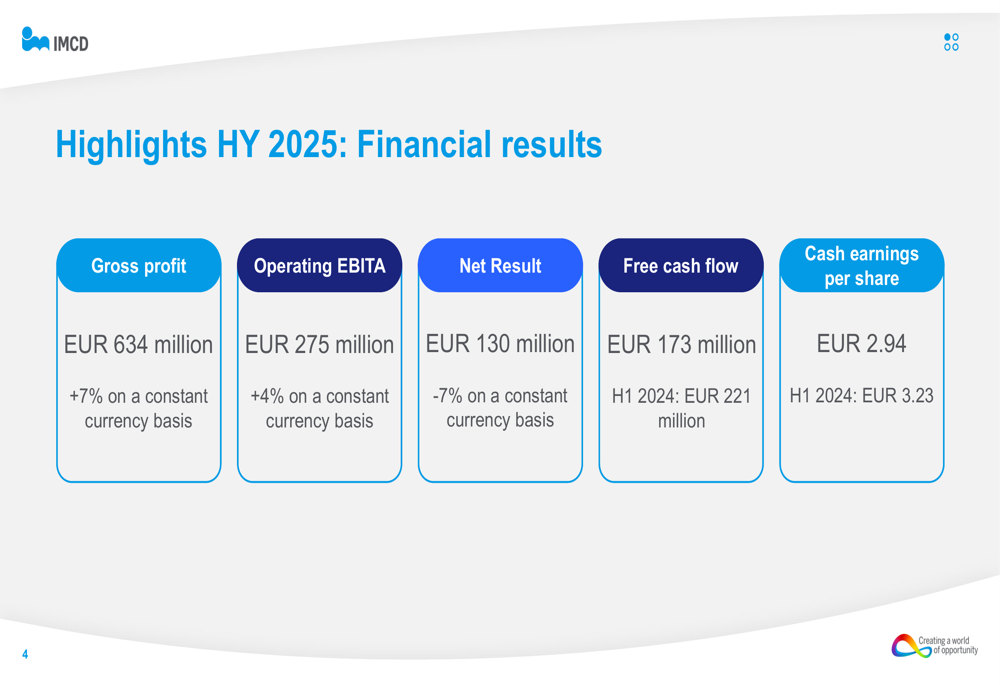

IMCD reported half-year 2025 revenue of €2,474 million, representing a 4% increase (6% FX-adjusted) compared to the same period in 2024. While gross profit grew by 7% on a constant currency basis to €634 million, the company’s net result declined by 7% to €130 million, highlighting pressure on profitability despite top-line growth.

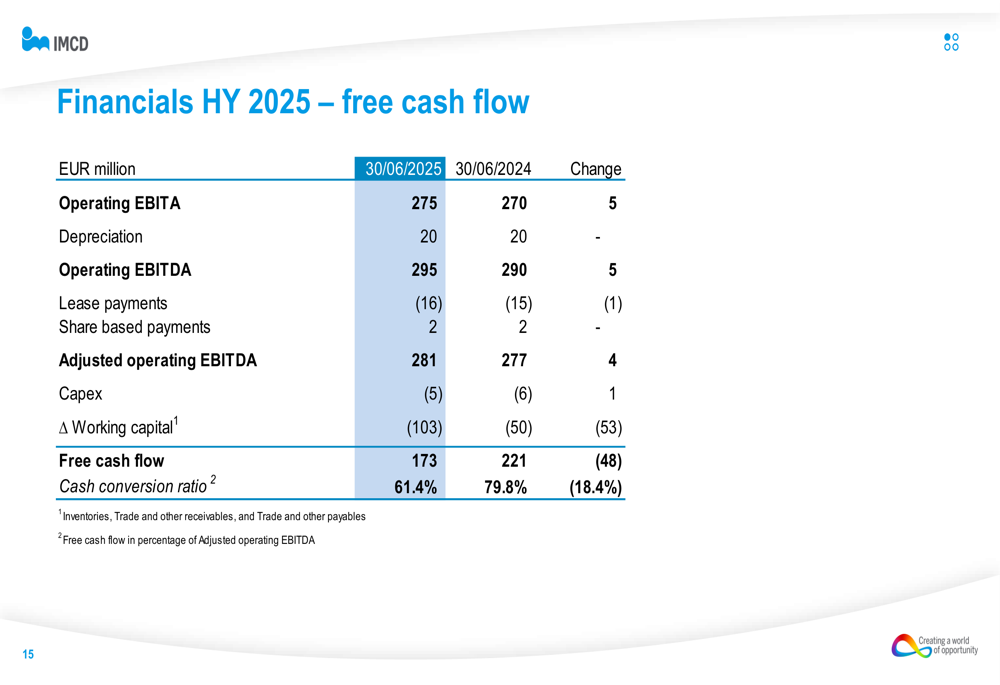

The company’s financial highlights reveal this mixed performance pattern, with operating EBITA growing at a more modest 4% rate to €275 million:

Free cash flow declined significantly to €173 million, down from €221 million in H1 2024, representing a 22% decrease. Cash earnings per share also fell to €2.94 from €3.23 in the comparable period. These metrics suggest IMCD is facing challenges in converting its revenue growth to bottom-line results and cash generation.

Detailed Financial Analysis

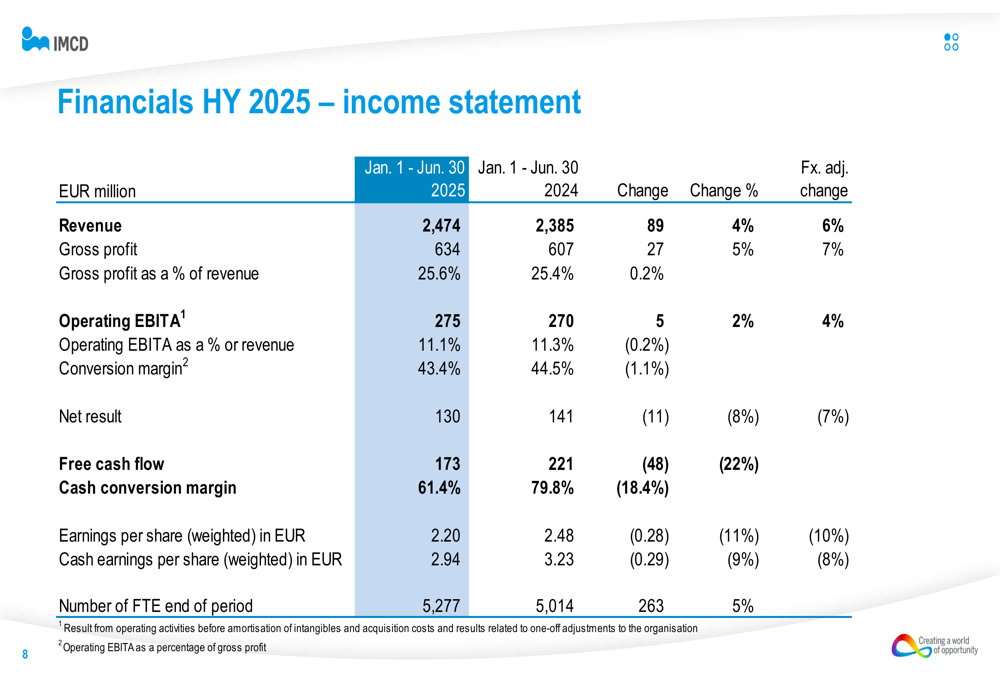

IMCD’s income statement reveals the full picture of the company’s financial performance for the first half of 2025. While revenue and gross profit showed positive growth, the conversion to operating profit and net income faced headwinds:

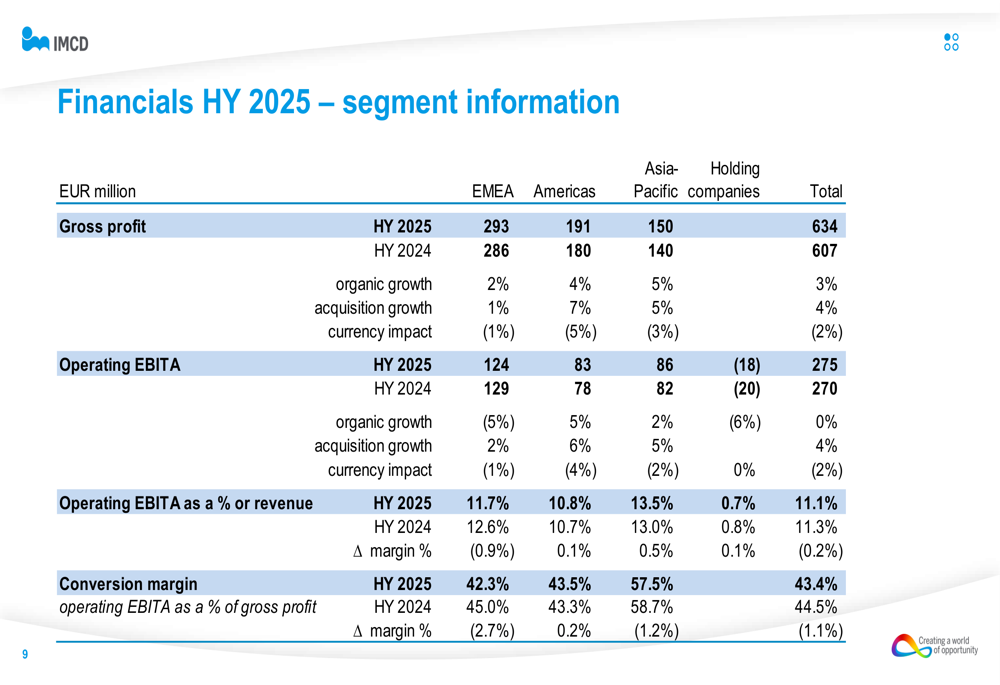

The segment breakdown provides further insight into regional performance variations. Unlike the strong 21% organic growth in the Americas reported in Q1, the half-year results show more modest performance across regions:

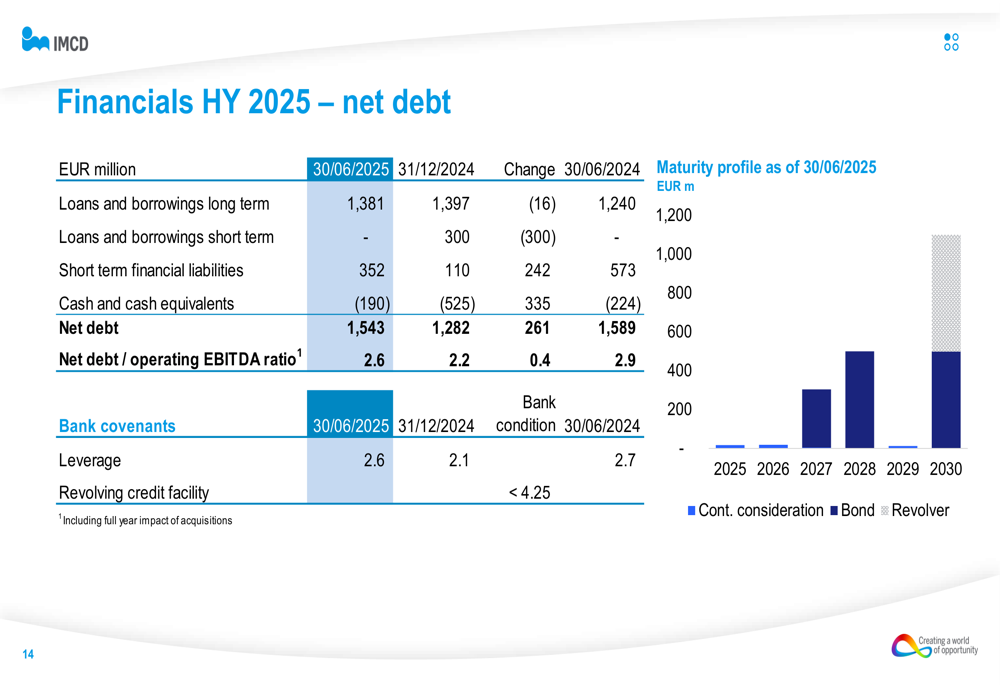

One area of potential concern is IMCD’s increasing debt levels. The company’s net debt reached €1,543 million, with a net debt ratio of 2.6, up from 2.2 at the end of 2024. While still below the company’s covenant limit of 4.25, this trend bears watching:

Working capital management appears to be a focus area, with the company providing detailed breakdowns of inventory, receivables, and payables. The free cash flow calculation highlights how working capital changes have impacted overall cash generation:

Strategic Initiatives & M&A Activity

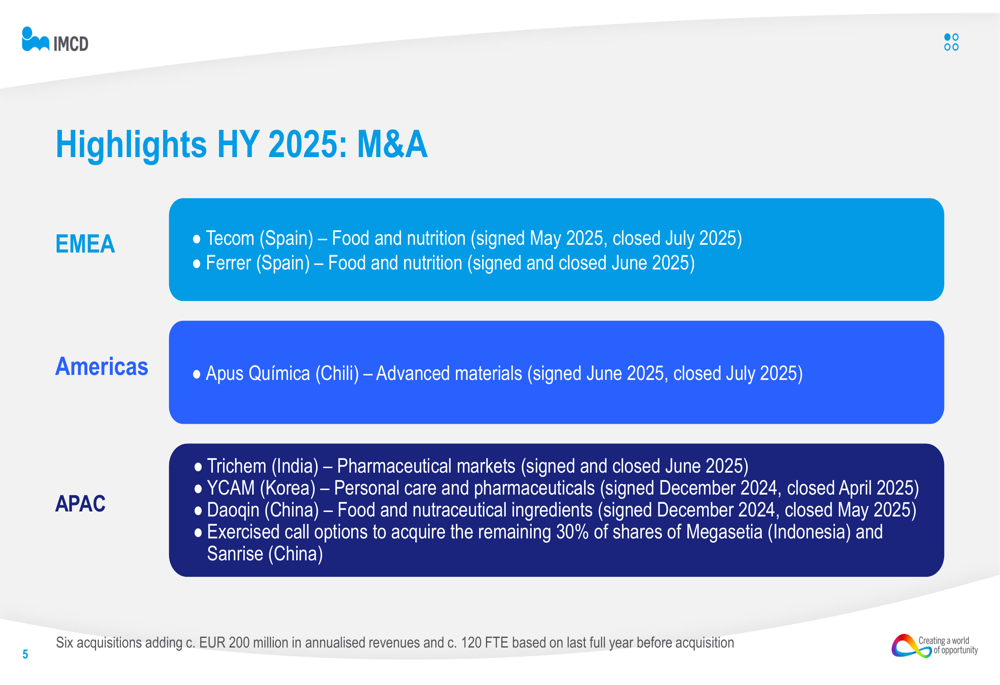

Despite financial pressures, IMCD has maintained its strategic focus on growth through acquisitions. The company completed six acquisitions across its global footprint during the first half of 2025, adding approximately €200 million in annualized revenues and 120 employees.

The acquisition strategy spans multiple regions and business segments, reinforcing IMCD’s global expansion ambitions:

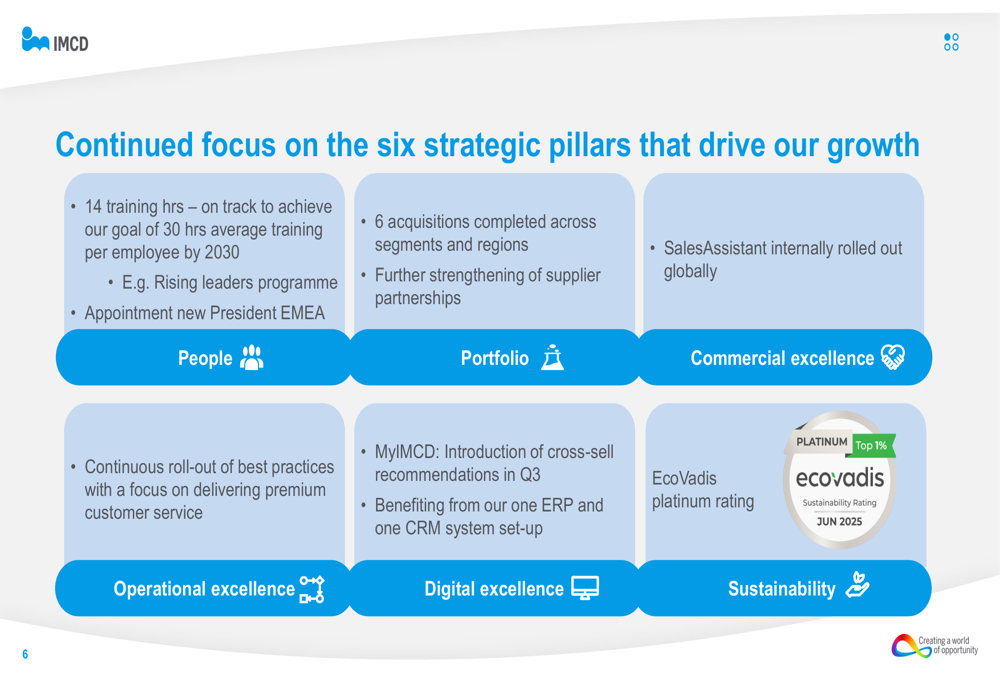

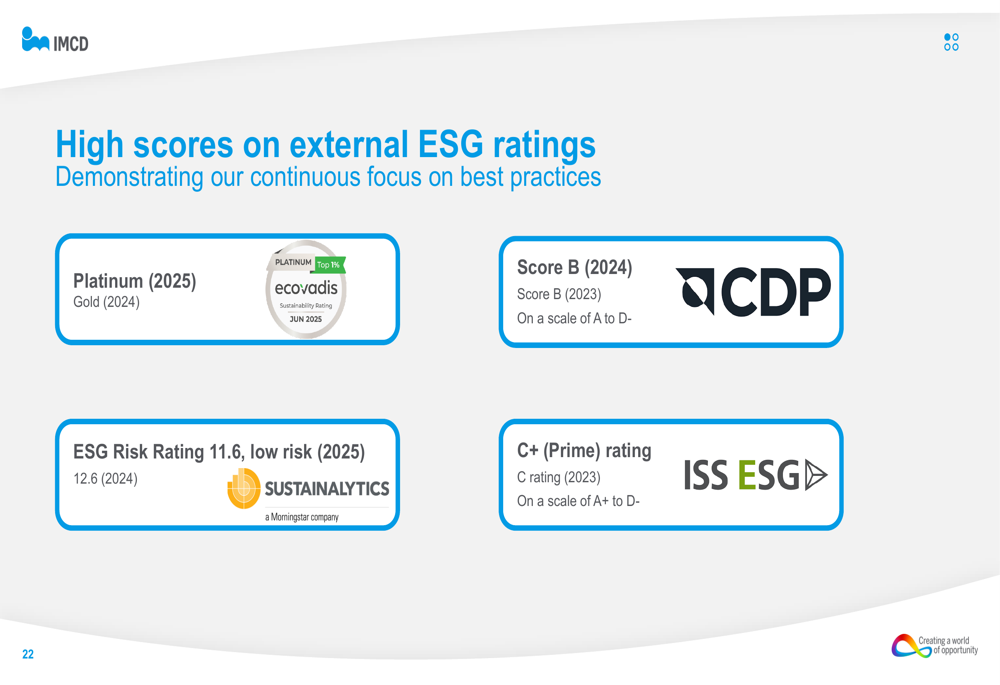

IMCD continues to execute against its six strategic pillars, with particular emphasis on digital transformation and sustainability. The company achieved an EcoVadis platinum rating, positioning it as a leader in environmental, social, and governance (ESG) performance:

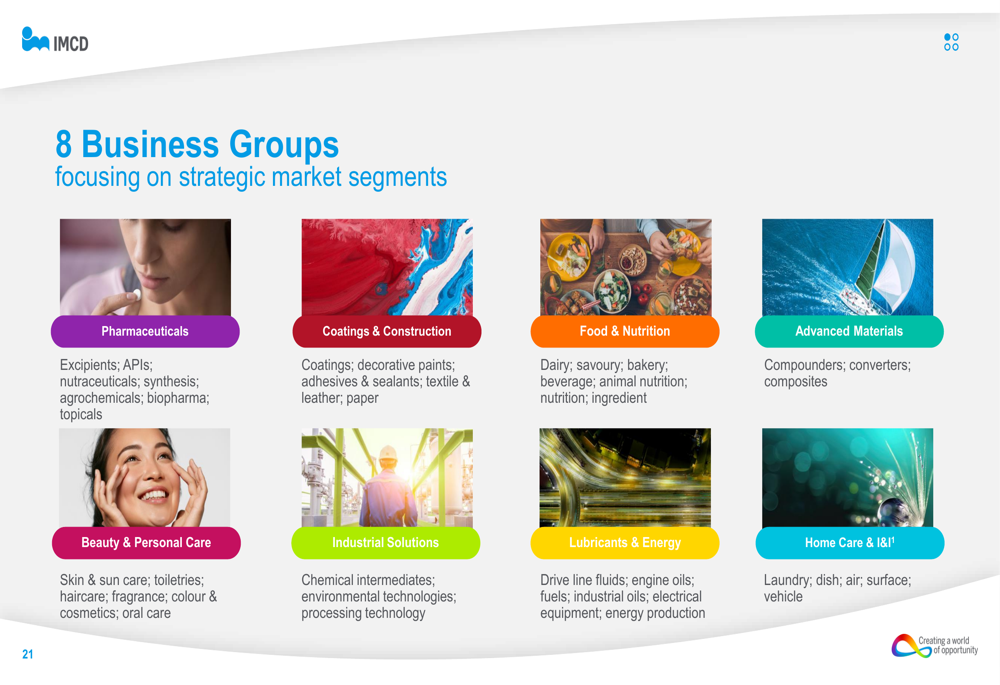

The company’s diverse business portfolio across eight specialty segments provides resilience against market fluctuations, though performance appears to vary significantly across these divisions:

Outlook & Forward-Looking Statements

IMCD’s outlook statement acknowledges the challenging macroeconomic environment while expressing confidence in the company’s business model. Management emphasized that success depends on maintaining commercial relationships, introducing new products, and effectively integrating acquisitions.

The company’s forward-looking statements strike a cautious tone, noting that "macroeconomic and political uncertainty make predictions difficult." This represents a somewhat more conservative stance compared to the more optimistic outlook following Q1 results, when CEO Marcus Jordan expressed strong confidence in the company’s diversified business model.

IMCD’s ESG credentials remain a bright spot, with the company highlighting its strong performance across multiple sustainability ratings:

While IMCD faces near-term challenges in converting revenue growth to bottom-line results, its continued focus on strategic acquisitions and digital transformation suggests management is positioning the company for long-term growth. Investors will likely watch closely to see if the company can reverse the trend of declining net profits and free cash flow in the second half of 2025.

The increased debt levels and working capital requirements will also be key metrics to monitor, particularly if macroeconomic conditions deteriorate further. With the stock trading well below its 52-week high of €159, market sentiment appears cautious about IMCD’s near-term prospects despite its strategic positioning in specialty chemical distribution.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.