What happens to stocks if AI loses momentum?

Introduction & Market Context

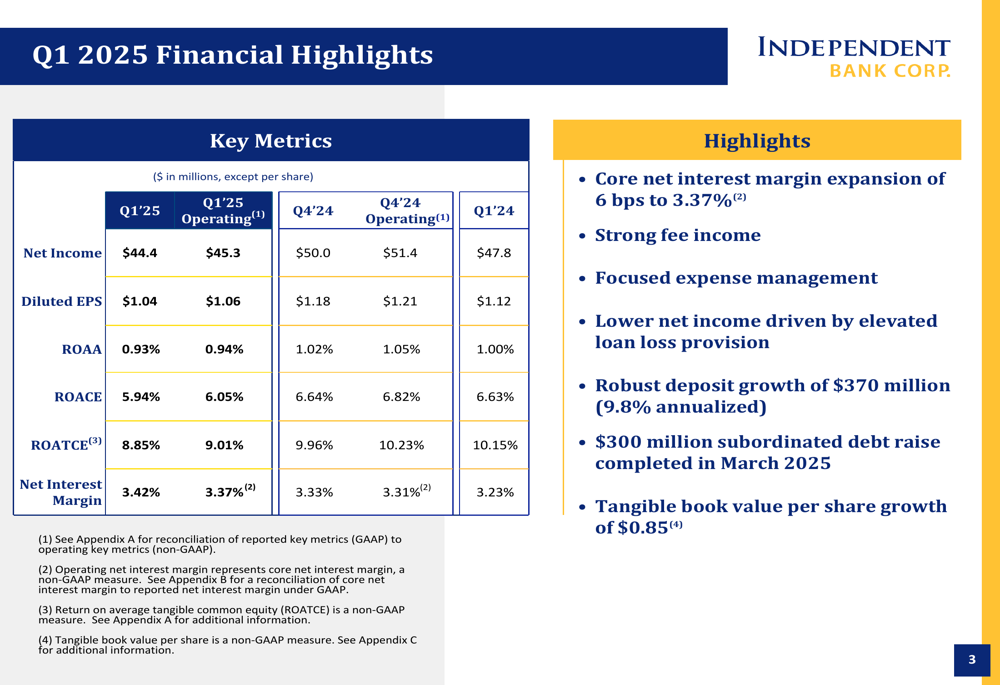

Independent Bank Corp. (NASDAQ:INDB), parent company of Rockland Trust, presented its first quarter 2025 earnings results on April 17, 2025, revealing a mixed financial performance characterized by expanding net interest margin but lower net income due to elevated loan loss provisions.

The bank, which recently announced its acquisition of Enterprise Bancorp, reported operating net income of $45.3 million for Q1 2025, down from $50.0 million in the previous quarter and $47.8 million in the same quarter last year. Despite the earnings decline, the bank highlighted several positive developments, including robust deposit growth and net interest margin expansion.

The Q1 results come after Independent Bank exceeded analysts’ expectations in Q4 2024, with an EPS of $1.21 versus the forecast of $1.17, according to previous earnings reports.

Quarterly Performance Highlights

Independent Bank reported diluted earnings per share of $1.04 for Q1 2025, or $1.06 on an operating basis, compared to $1.18 in Q4 2024 and $1.12 in Q1 2024. The bank’s net interest margin expanded to 3.42% (3.37% on a core basis), up from 3.33% in the previous quarter and 3.23% in the year-ago quarter, reflecting improved earning asset yields.

As shown in the following financial highlights summary:

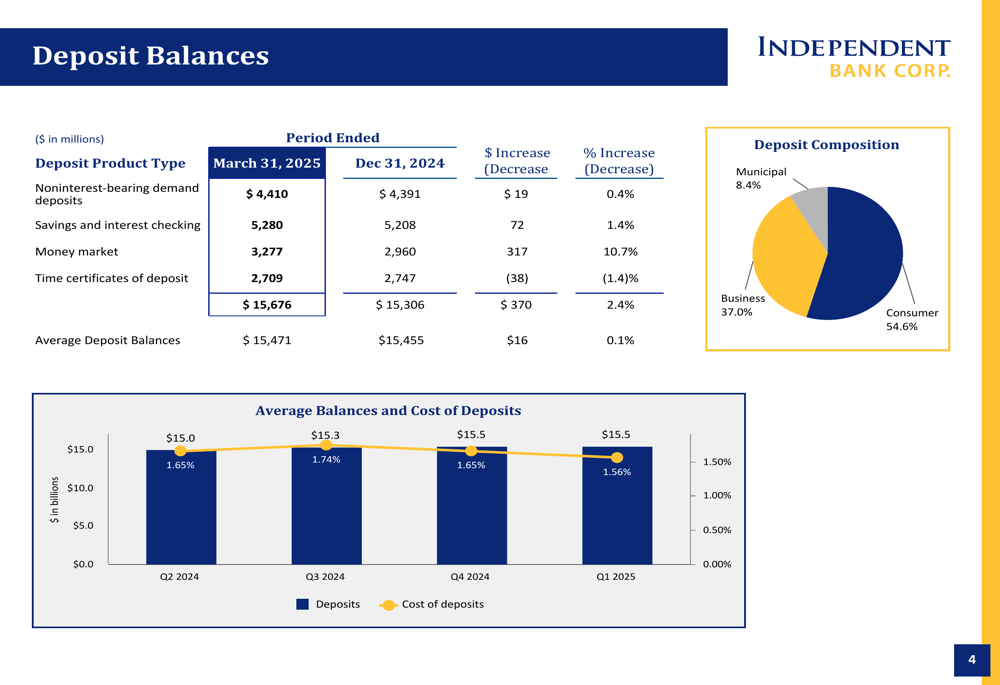

Deposit growth was particularly strong, with total deposits increasing by $370 million or 9.8% on an annualized basis. The bank’s deposit composition remains well-diversified with 54.6% consumer deposits, 37.0% business deposits, and 8.4% municipal deposits. The cost of deposits declined to 1.56% in Q1 2025 from 1.65% in Q4 2024, demonstrating the bank’s ability to manage funding costs in a changing rate environment.

The deposit growth and composition are illustrated in this breakdown:

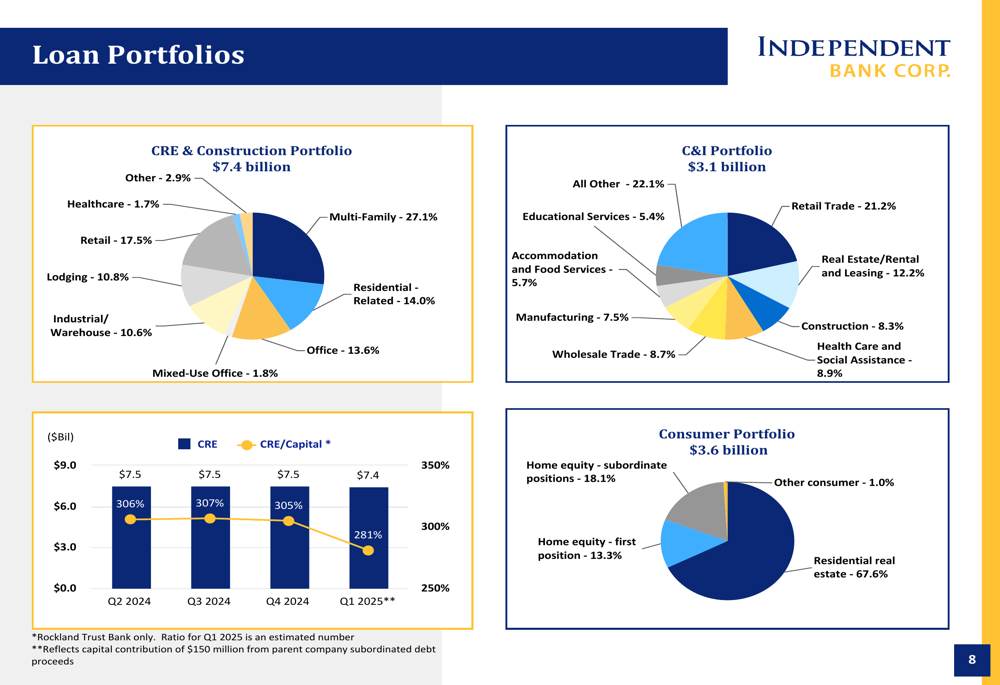

Total (EPA:TTEF) loan balances remained relatively stable at $14.49 billion as of March 31, 2025, a slight 0.1% decrease from December 31, 2024. Commercial and industrial loans grew by 2.0%, while commercial real estate loans decreased by 1.5%, reflecting the bank’s stated strategy of diversifying its loan portfolio away from commercial real estate concentration.

Asset Quality and Credit Trends

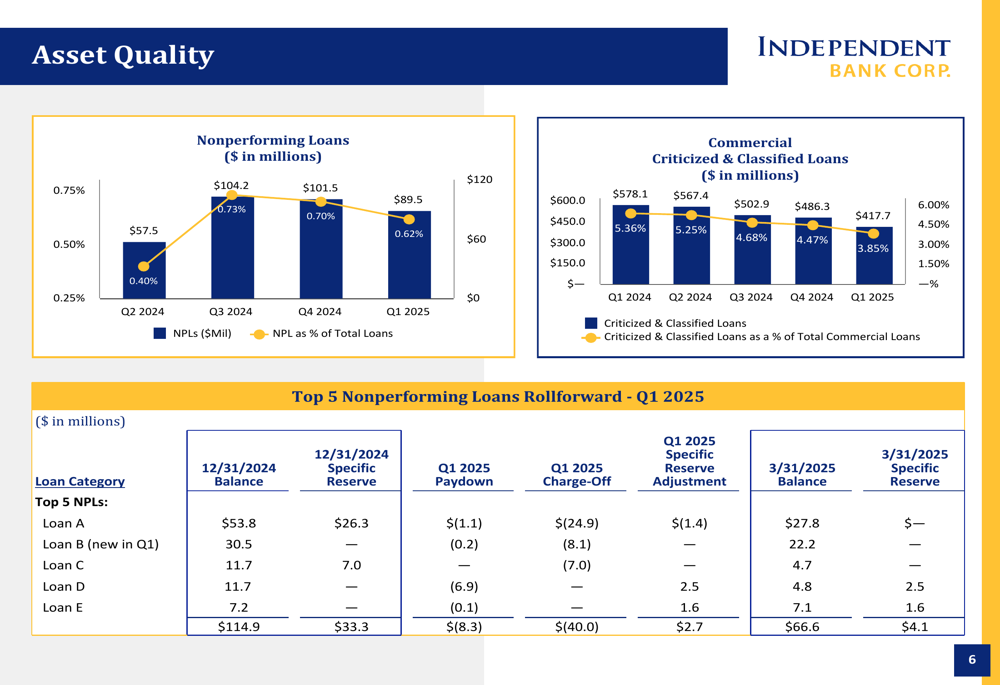

Asset quality metrics showed improvement in several areas, with nonperforming loans decreasing to $89.5 million (0.62% of total loans) in Q1 2025 from $101.5 million (0.70%) in Q4 2024. Commercial criticized and classified loans also declined to $417.7 million (3.85% of commercial loans) from $486.3 million (4.47%) in the previous quarter.

The following chart illustrates these improving asset quality trends:

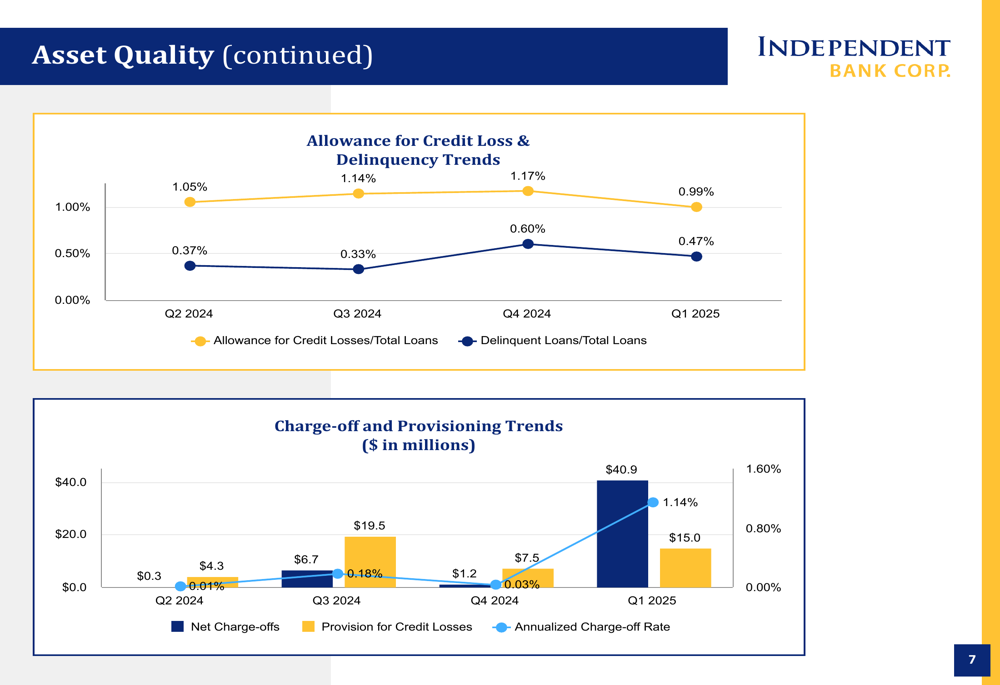

However, net charge-offs increased significantly to $40.9 million (1.14% annualized rate) in Q1 2025, compared to just $1.2 million (0.03%) in Q4 2024. This increase, along with a provision for credit losses of $15.0 million (up from $7.5 million in Q4 2024), contributed to the lower net income for the quarter.

The charge-off and provisioning trends are shown in this chart:

The bank provided detailed insights into its commercial real estate portfolio, particularly its office exposure, which has been an area of concern for many banks. Office loans represent 13.6% of the bank’s $7.4 billion CRE and construction portfolio. The bank’s CRE to capital ratio improved to 281% in Q1 2025 from 305% in Q4 2024, reflecting management’s efforts to reduce concentration risk.

Net Interest Income and Margin Analysis

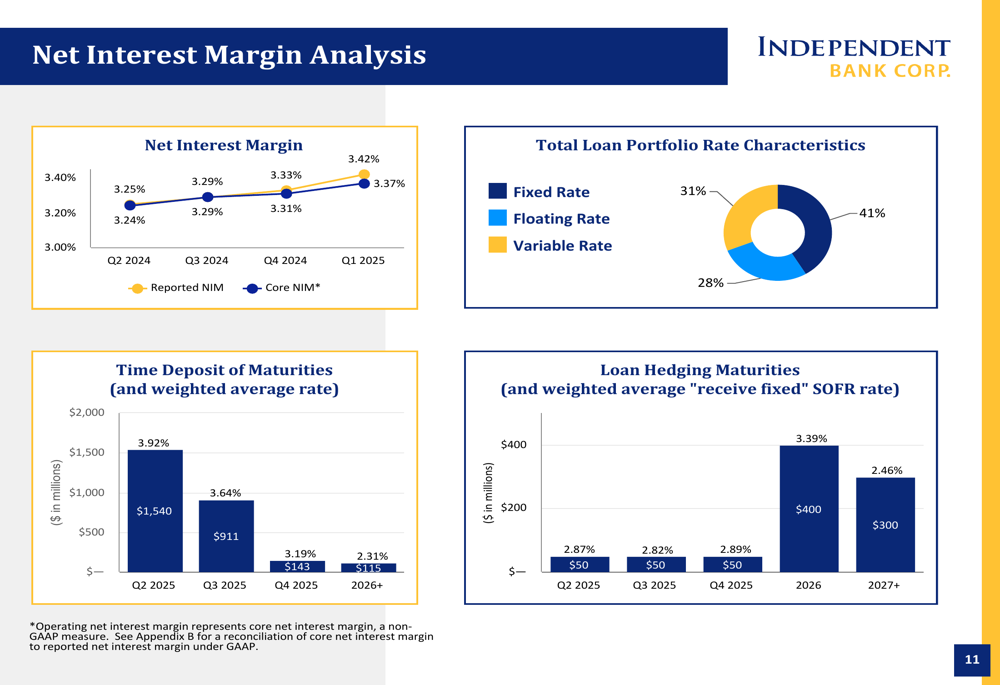

Independent Bank’s net interest margin expansion was a bright spot in the quarterly results. The reported NIM increased to 3.42% (3.37% on a core basis) in Q1 2025, continuing an upward trend from previous quarters. This expansion occurred despite the issuance of $300 million in subordinated debt in March 2025, which had a negative impact on the margin.

The bank’s loan portfolio rate characteristics show a balanced mix with 31% fixed rate, 41% floating rate, and 28% variable rate loans, positioning the bank to benefit from both the current rate environment and potential future rate changes.

The following chart details the net interest margin trends and portfolio composition:

The bank’s investment management and advisory business continues to be a strong contributor to fee income, with assets under administration reaching $7.1 billion as of March 31, 2025, a 0.9% increase from the previous quarter. Revenue from this segment grew by 4.1% quarter-over-quarter to $11.2 million.

Strategic Growth Initiatives

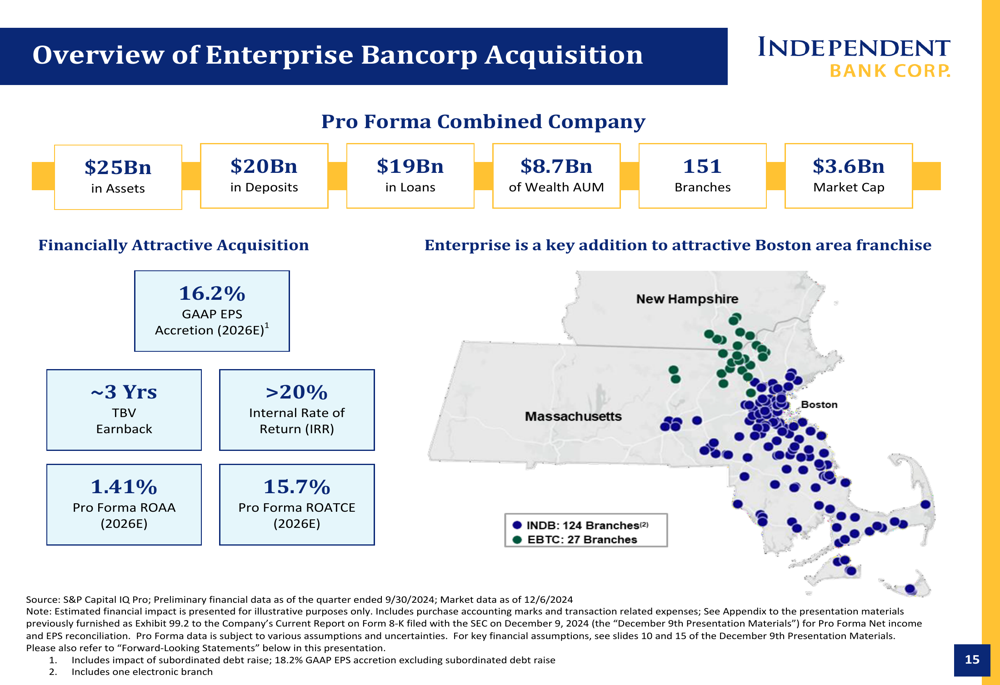

A significant focus of the presentation was the bank’s pending acquisition of Enterprise Bancorp, which is expected to create a combined entity with approximately $25 billion in assets, $20 billion in deposits, $19 billion in loans, and 151 branches across Massachusetts and New Hampshire.

The acquisition is projected to be financially attractive with 16.2% GAAP EPS accretion expected by 2026, a tangible book value earnback period of approximately three years, and an internal rate of return exceeding 20%. The transaction will enhance Independent Bank’s market presence and scale.

The following slide provides an overview of the acquisition:

Forward-Looking Statements

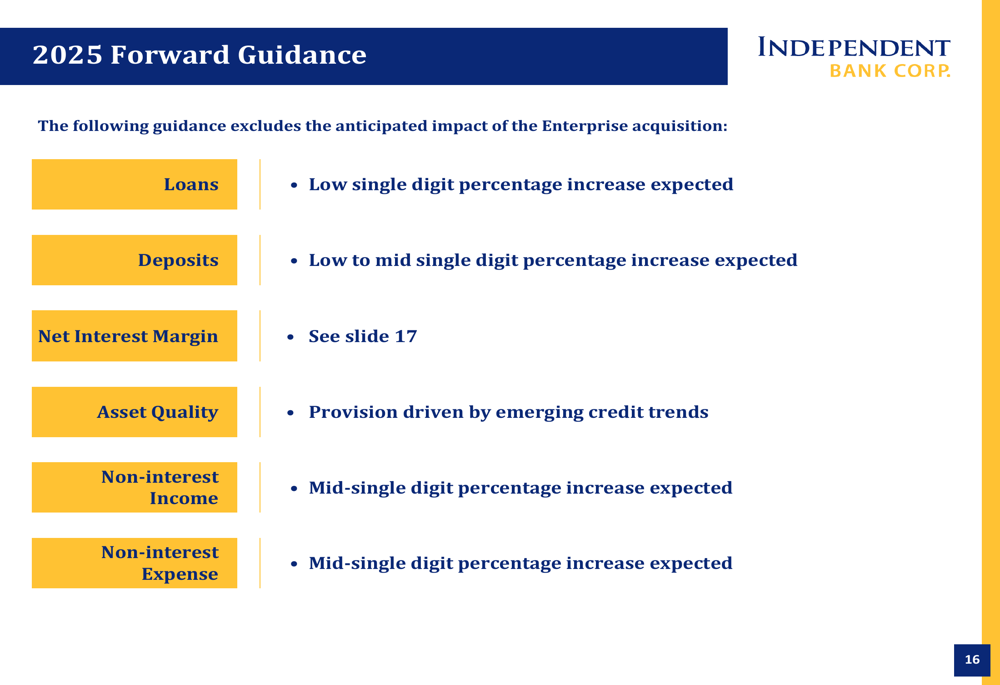

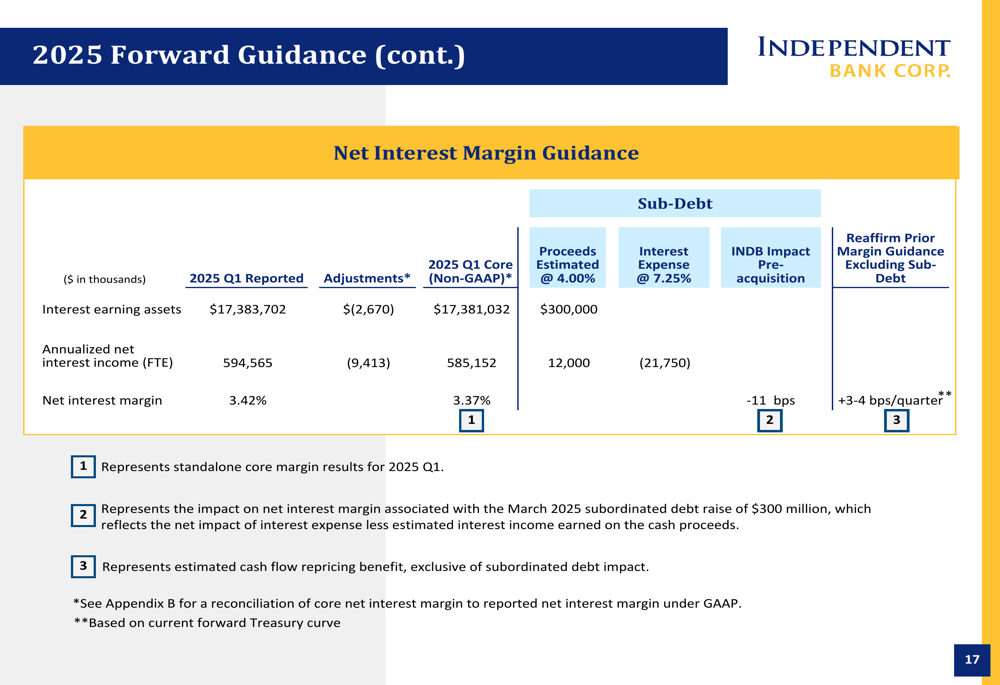

Looking ahead to the remainder of 2025, Independent Bank provided guidance excluding the anticipated impact of the Enterprise acquisition. The bank expects low single-digit percentage growth in loans and low to mid-single-digit percentage growth in deposits. Net interest margin is expected to benefit from the current positioning, with potential for 3-4 basis points of expansion per quarter, excluding the impact of the recent subordinated debt issuance.

The bank also provided specific guidance on its net interest margin, clarifying the impact of the recent subordinated debt issuance and reaffirming its previous margin guidance:

In conclusion, Independent Bank’s Q1 2025 results present a mixed picture with expanding net interest margin and strong deposit growth offset by elevated loan loss provisions and lower net income. The bank appears to be managing its credit risks proactively while positioning itself for future growth through the Enterprise Bancorp acquisition and continued focus on diversifying its loan portfolio away from commercial real estate concentration.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.