Robinhood shares gain on Q2 beat, as user and crypto growth accelerate

Independent Bank (NASDAQ:INDB) Corporation (NASDAQ:IBCP) presented its first quarter 2025 financial results on April 24, revealing solid performance driven by strong commercial loan growth and an improved net interest margin. The Michigan-based community bank reported earnings per share of $0.74, exceeding analyst expectations of $0.70, despite a slight revenue miss.

Quarterly Performance Highlights

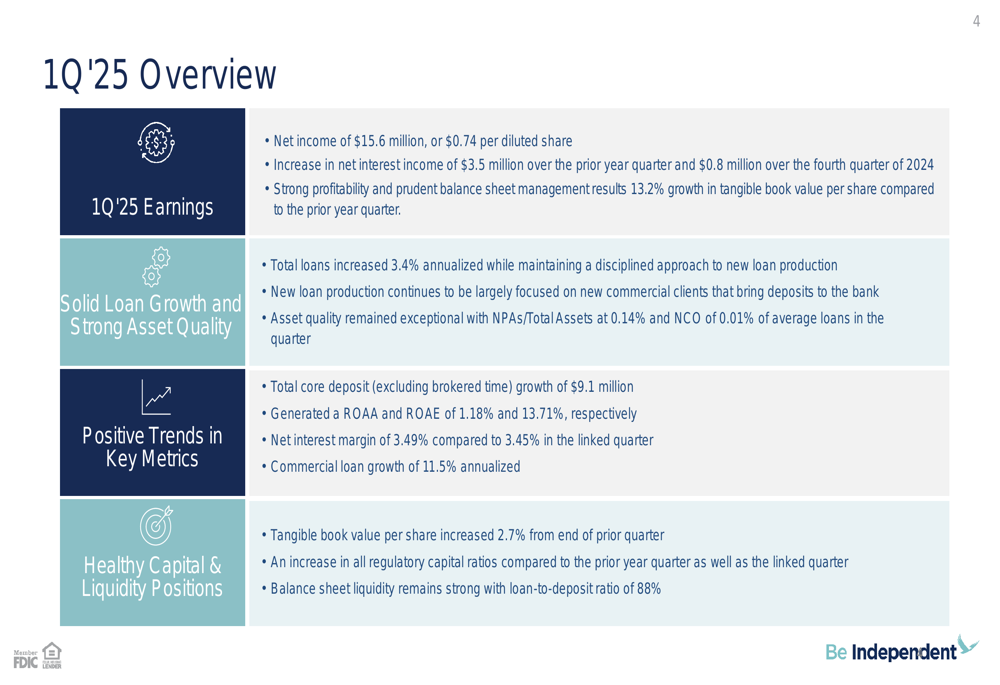

Independent Bank reported net income of $15.6 million ($0.74 per diluted share) for the first quarter of 2025, representing a slight decrease from $16 million in the same period last year. However, the bank demonstrated strong fundamentals with net interest income increasing by $3.5 million over the prior year quarter and $0.8 million over the fourth quarter of 2024.

As shown in the following overview of Q1 2025 performance, the bank achieved solid profitability metrics while maintaining strong asset quality:

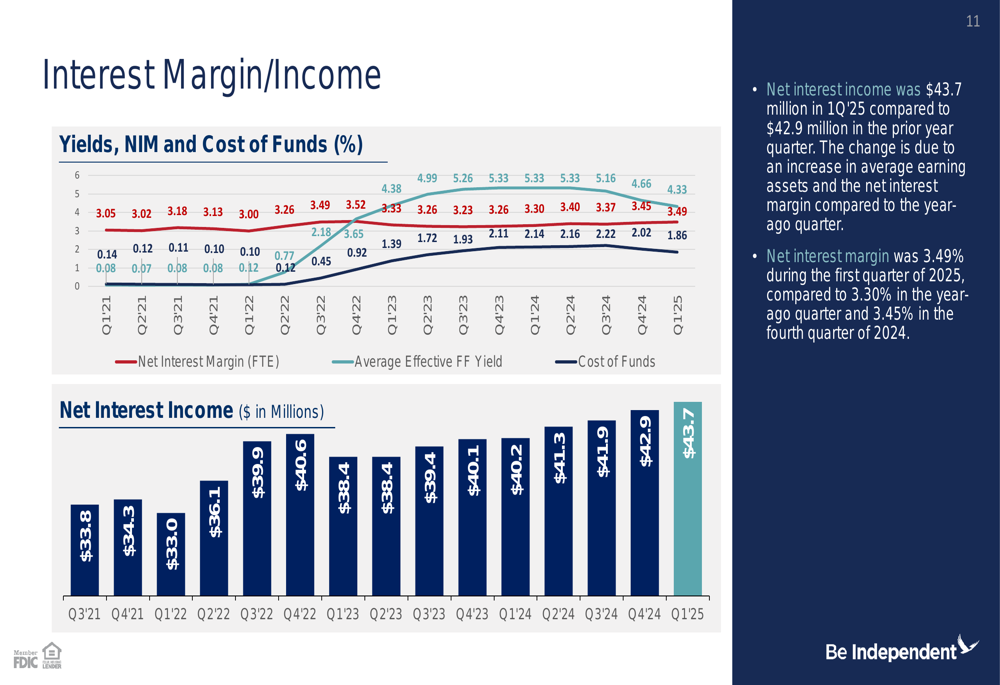

The bank’s net interest margin improved to 3.49% in Q1 2025, compared to 3.30% in the year-ago quarter and 3.45% in the fourth quarter of 2024. This expansion contributed to the earnings beat despite the revenue shortfall of $0.88 million compared to forecasts.

The following chart illustrates the positive trend in net interest margin and income:

"We’ve built a strong community bank franchise, which positions us well to effectively manage through a variety of economic environments," said CEO Brad Kessel during the earnings call. The market reaction to these results was slightly negative, with shares dropping 2% following the announcement, despite the EPS beat.

Deposit and Loan Portfolio Analysis

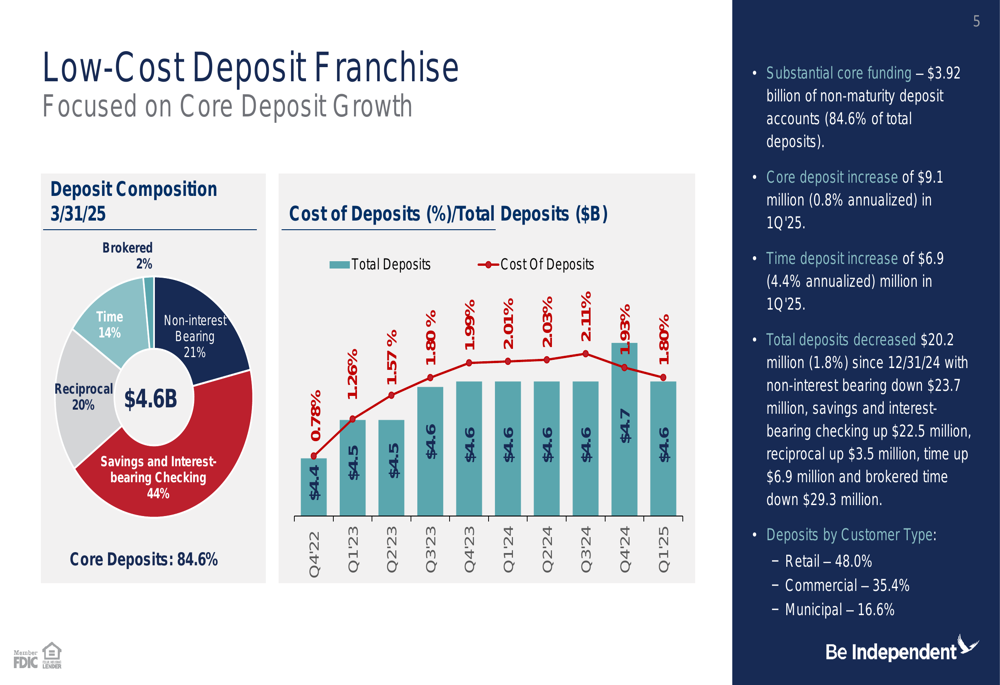

Independent Bank maintained a strong focus on its low-cost deposit franchise, with $3.92 billion in non-maturity deposit accounts representing 84.6% of total deposits. Core deposits increased by $9.1 million (0.8% annualized) in Q1 2025, while total deposits decreased by $20.2 million (1.8%) since December 31, 2024, primarily due to a reduction in non-interest bearing deposits and brokered time deposits.

The following chart shows the bank’s deposit composition and cost trends:

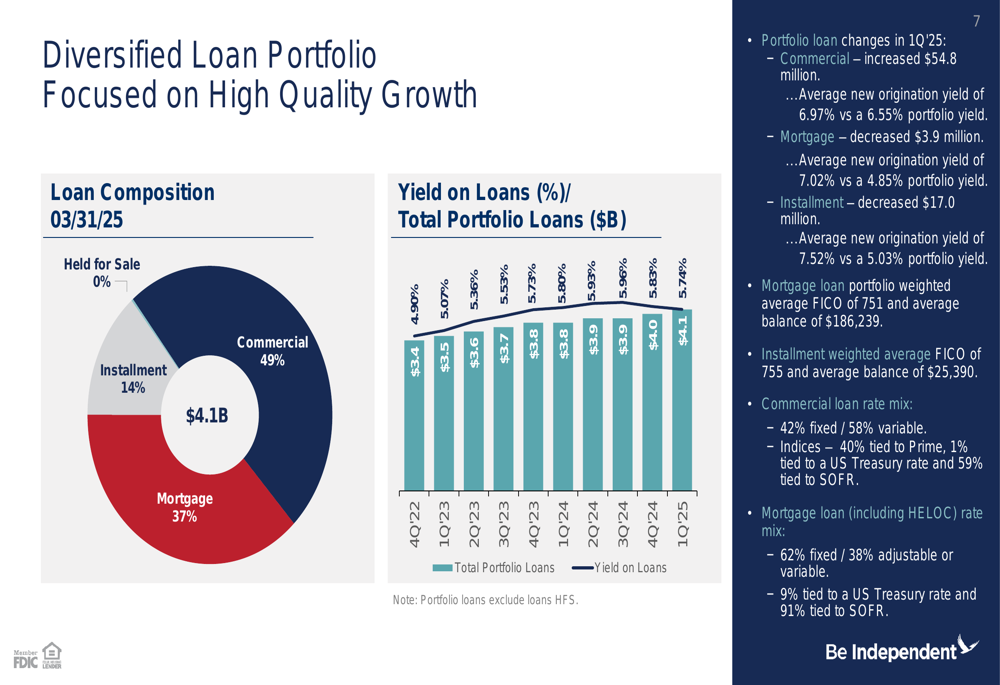

On the lending side, Independent Bank reported total loan growth of 3.4% annualized, with commercial loans leading the way at 11.5% annualized growth. The bank’s loan portfolio remains well-diversified, with commercial loans accounting for 49% of the total, followed by mortgage loans at 37% and installment loans at 14%.

The following breakdown illustrates the bank’s loan portfolio composition and yield trends:

CFO Gavin Moore expressed confidence in the bank’s adaptability to interest rate changes, noting, "We’re really indifferent to the Fed flat or today or no rate changes or the Fed cuts 100." This flexibility is reflected in the bank’s interest rate risk management, which shows positive net interest income impacts under various rate scenarios.

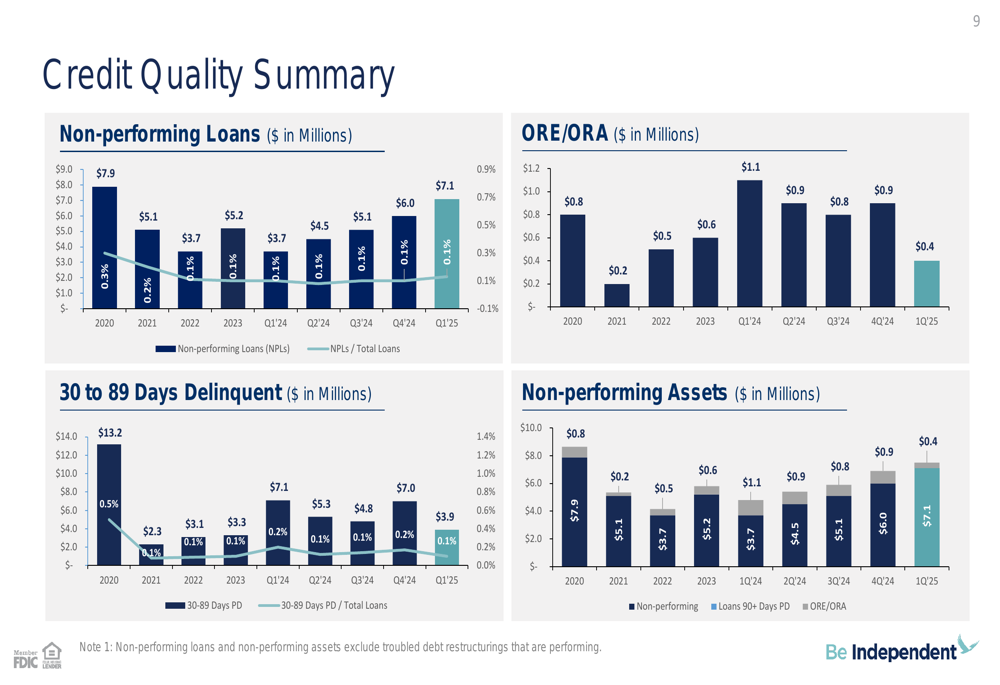

Capital and Credit Quality

Independent Bank maintained exceptional asset quality in Q1 2025, with non-performing assets to total assets at just 0.14% and net charge-offs of only 0.01% of average loans during the quarter. The following chart demonstrates the bank’s consistent credit quality metrics:

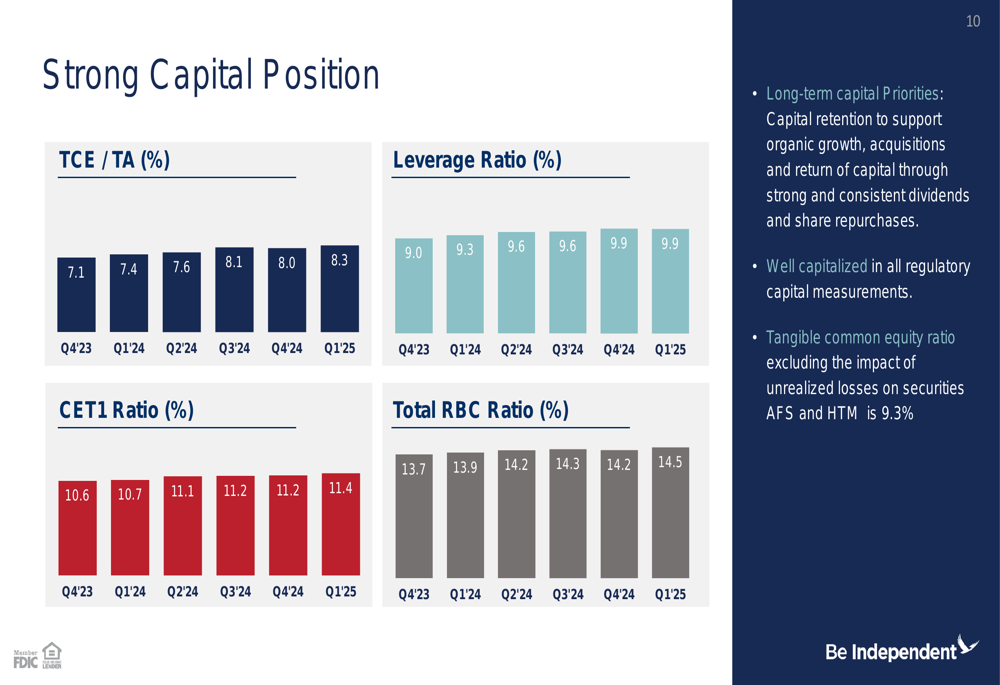

The bank’s capital position also strengthened during the quarter, with tangible book value per share growing by 13.2% compared to the prior year quarter and 2.7% from the end of the previous quarter. All regulatory capital ratios improved, with the TCE/TA ratio reaching 8.3% in Q1 2025, up from 7.1% in Q4 2023.

As shown in the following capital position summary, Independent Bank remains well-capitalized by all regulatory standards:

The bank’s balance sheet liquidity remains strong, with a loan-to-deposit ratio of 88% and substantial available liquidity sources equivalent to 44% of total deposits.

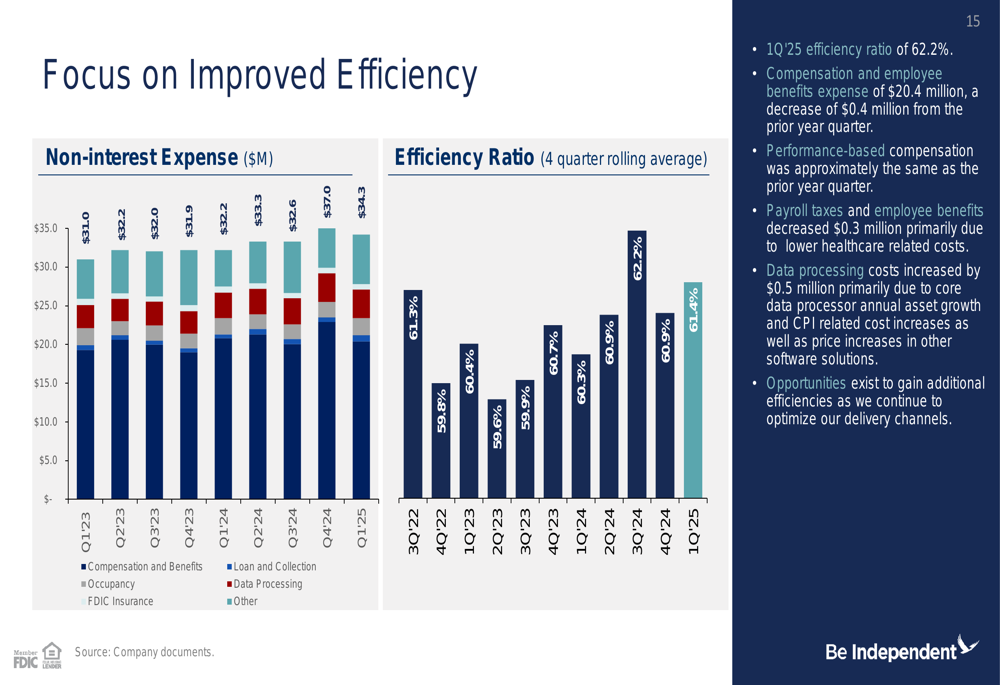

Efficiency and Non-Interest Income

Independent Bank reported an efficiency ratio of 62.2% for Q1 2025, reflecting its ongoing focus on cost control and operational efficiency. Non-interest expenses were well-managed, with compensation and employee benefits decreasing by $0.4 million from the prior year quarter.

The following chart shows the bank’s efficiency ratio trend and non-interest expense:

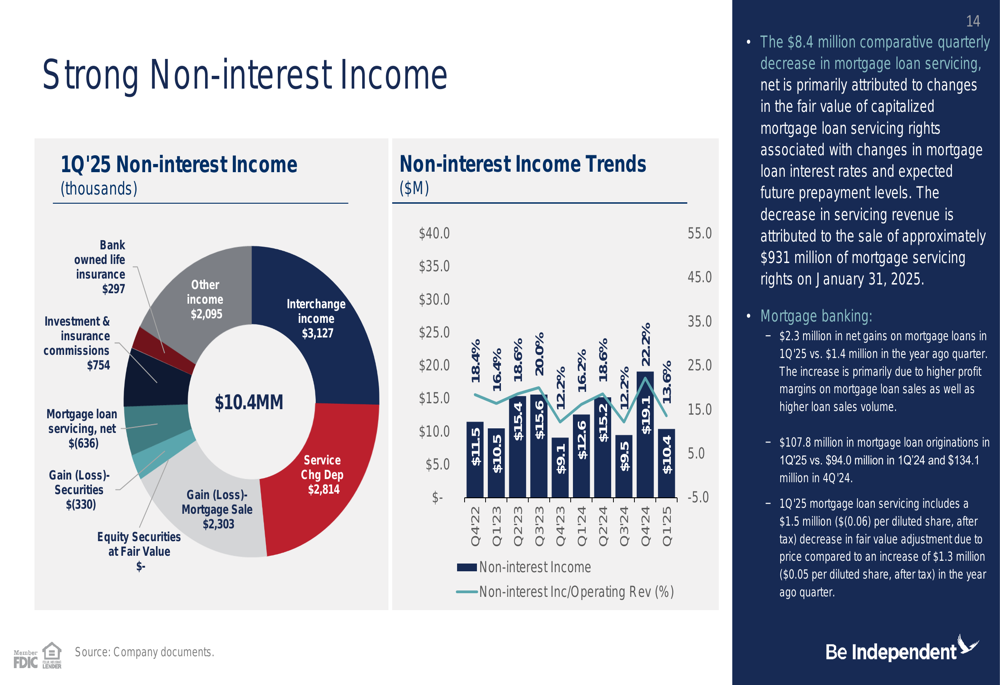

Non-interest income totaled $10.4 million in Q1 2025, representing 13.6% of operating revenue. The bank’s non-interest income sources are diversified, with interchange income, service charges on deposits, and mortgage loan sales being the largest contributors.

The composition of non-interest income is illustrated in the following chart:

Strategic Initiatives and 2025 Outlook

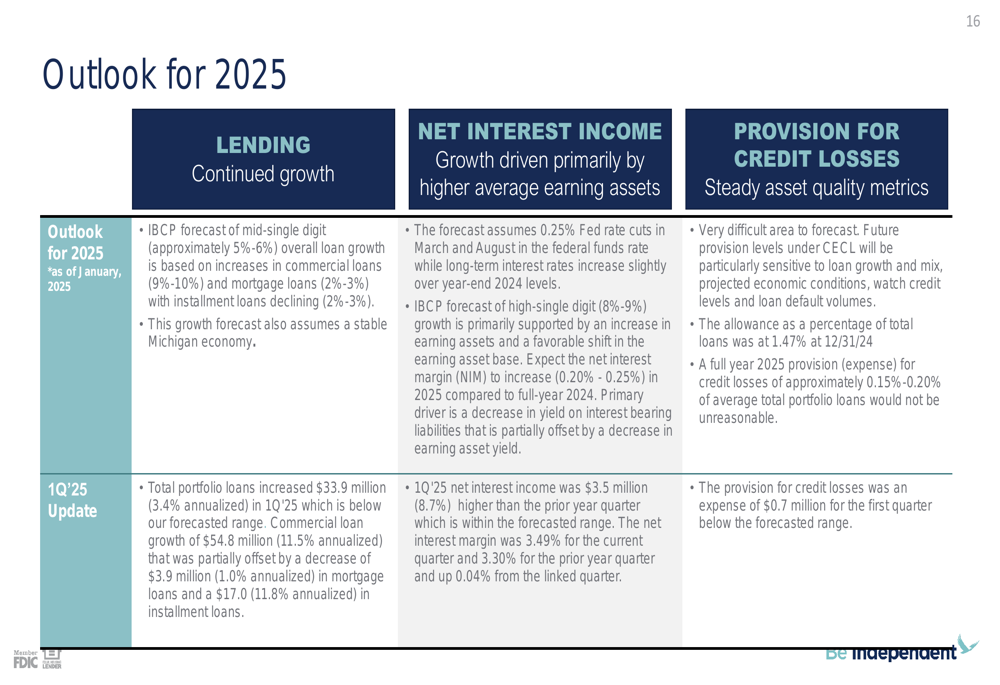

Looking ahead, Independent Bank provided an optimistic outlook for 2025, projecting mid-single digit (5%-6%) overall loan growth, driven primarily by commercial loans (9%-10%) and mortgage loans (2%-3%). The bank expects high-single digit (8%-9%) growth in net interest income, supported by an increase in earning assets and a favorable shift in the earning asset base.

The bank’s detailed outlook for 2025 is presented below:

Independent Bank’s strategic initiatives focus on four key areas: growth, process improvement and cost controls, talent management, and risk management. The bank plans to leverage outside sales, digital marketing, and new products for growth, while implementing process automation and branch optimization to improve efficiency.

The bank also announced a 2025 share repurchase authorization for approximately 5% (1.1 million) of outstanding shares, demonstrating its commitment to returning capital to shareholders. This aligns with the bank’s long-term capital priorities, which include supporting organic growth, pursuing acquisitions, and maintaining strong and consistent dividends.

Currently trading at $31.04, Independent Bank’s stock sits between its 52-week range of $22.53 to $40.32, with a P/E ratio of 9.5x. The bank continues its 11-year streak of dividend increases, further enhancing shareholder returns despite the competitive banking environment and economic uncertainties.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.