S&P 500 falls as ongoing government shutdown, trade jitters weigh

Introduction & Market Context

Independent Bank Corp. (NASDAQ:INDB), parent company of Rockland Trust, released its Q2 2025 earnings presentation on July 18, 2025, revealing strong financial performance that exceeded analyst expectations. The bank reported an operating earnings per share (EPS) of $1.25, surpassing the forecast of $1.21 by 3.31%. This positive performance contributed to a 5.77% increase in the stock price, which closed at $69.48 following the announcement.

The bank’s presentation highlighted its positioning as a "Strong, Resilient Franchise; Well Positioned for Growth" in the competitive New England banking landscape. Independent Bank emphasized its strong balance sheet, prudent risk management, and diversified deposit base as key competitive advantages.

Quarterly Performance Highlights

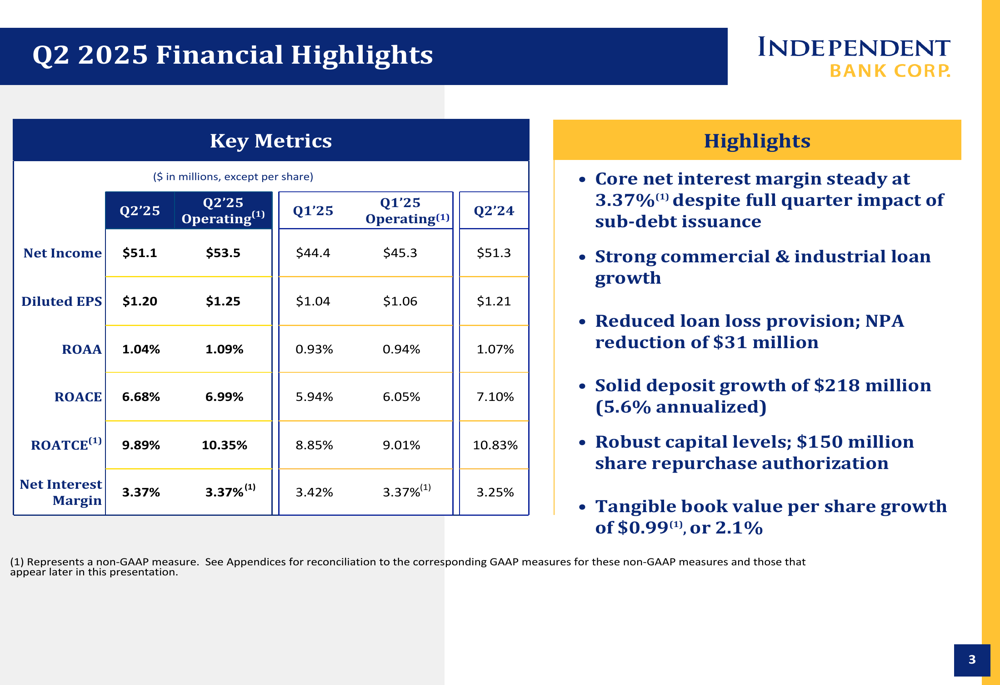

Independent Bank reported Q2 2025 net income of $51.1 million, or $1.20 per diluted share. On an operating basis, which excludes merger and acquisition expenses, the bank achieved $53.5 million in net income, or $1.25 per diluted share. Return on average assets (ROAA) reached 1.04%, while return on average tangible common equity (ROATCE) was 9.89%.

The bank maintained a stable core net interest margin of 3.37% despite absorbing the full quarter impact of a $300 million subordinated debt issuance completed in March 2025. Other notable achievements included solid deposit growth of $218 million (5.6% annualized) and tangible book value per share growth of $0.99, or 2.1%.

As shown in the following financial highlights table, the bank’s performance improved significantly compared to the first quarter of 2025:

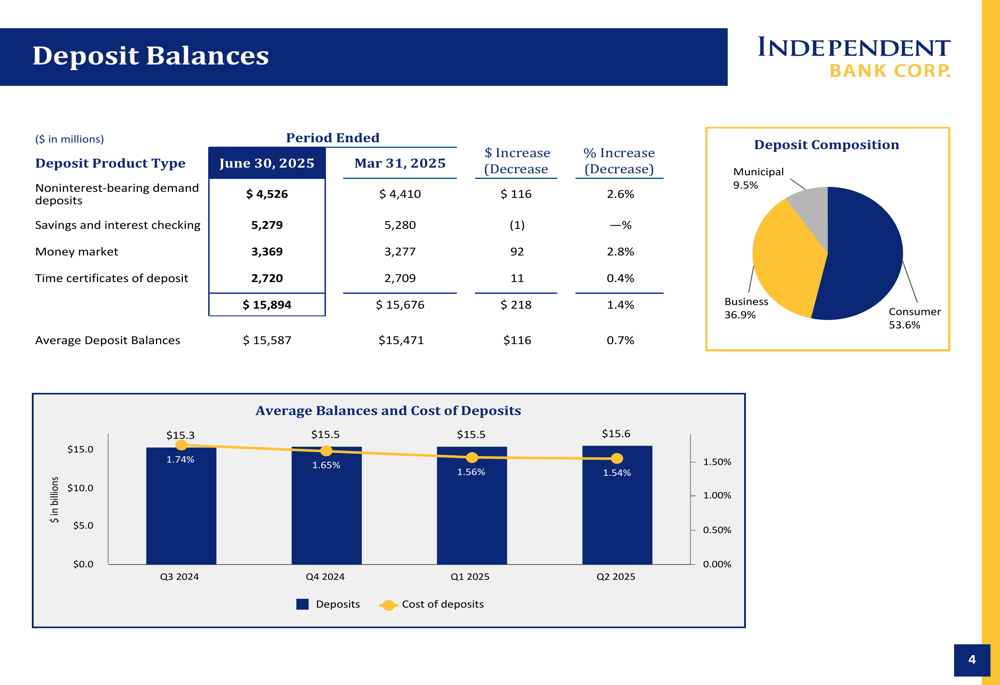

Deposit growth remained strong with total deposits increasing by $218 million or 1.4% from the previous quarter to reach $15.89 billion. The deposit composition showed a healthy mix with consumer deposits accounting for 53.6%, business deposits at 36.9%, and municipal deposits at 9.5%. Importantly, the average cost of deposits decreased slightly to 1.54% from 1.56% in the previous quarter, indicating stabilization in funding costs.

The following chart illustrates the bank’s deposit trends and costs over recent quarters:

Asset Quality Improvement

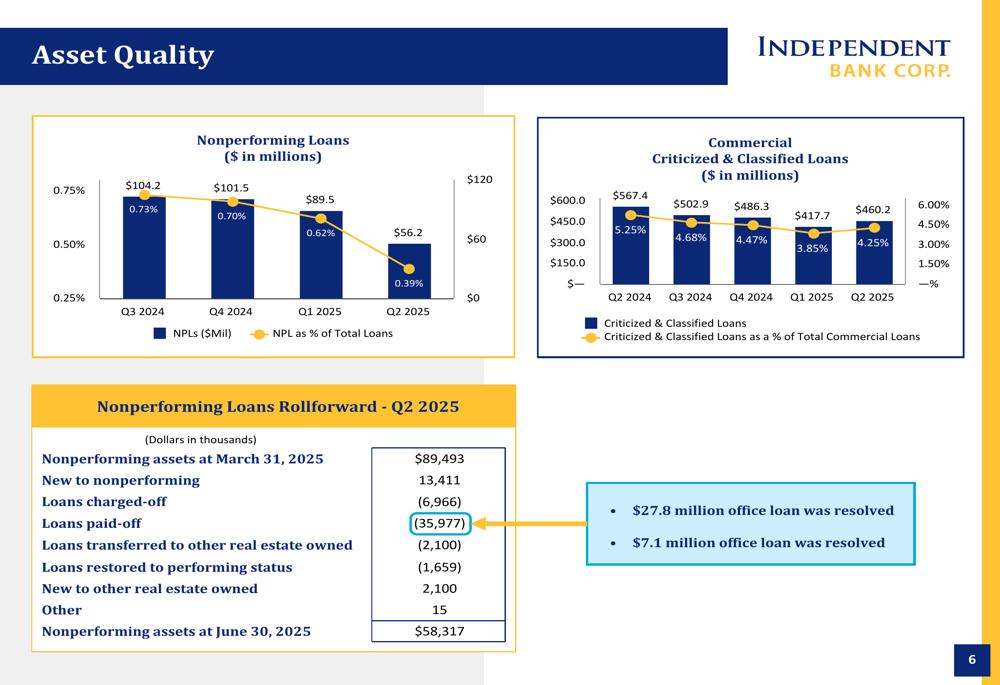

One of the most significant developments in the quarter was the substantial improvement in asset quality. Nonperforming loans (NPLs) decreased dramatically from $89.5 million in Q1 2025 to $56.2 million in Q2 2025, representing a reduction from 0.62% to 0.39% of total loans. This improvement was largely driven by the resolution of two significant office loans worth $27.8 million and $7.1 million.

The bank’s presentation provided a detailed breakdown of the nonperforming loans reduction:

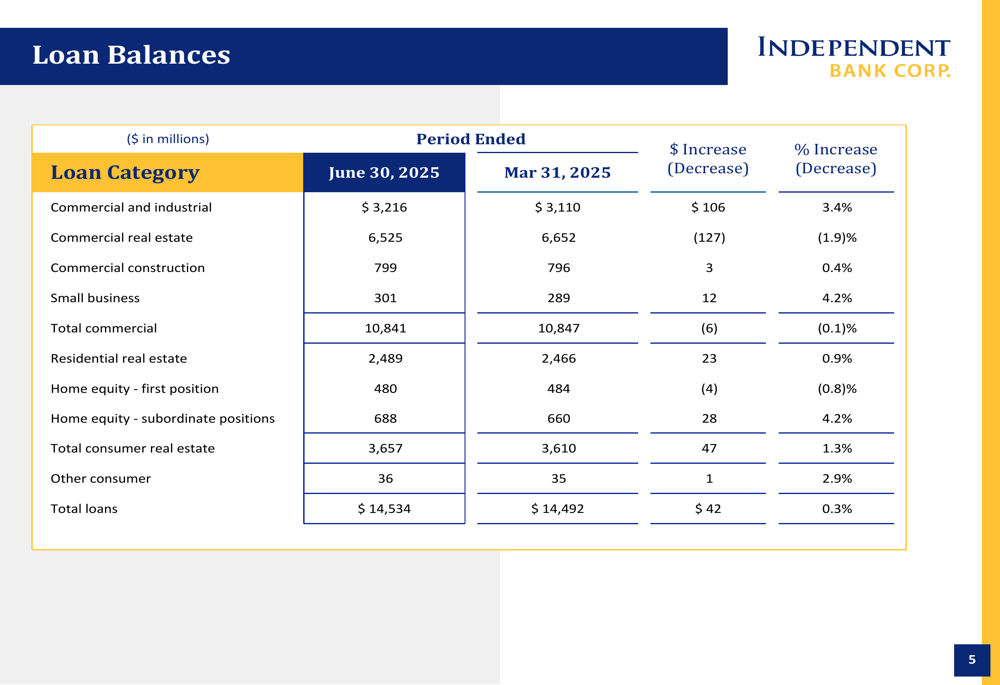

The loan portfolio showed modest overall growth of $42 million or 0.3% from the previous quarter, reaching $14.53 billion. This growth was primarily driven by strong performance in commercial and industrial (C&I) loans, which increased by $106 million or 3.4%. This strength was partially offset by a decrease in commercial real estate loans, which declined by $127 million or 1.9%.

The following table provides a comprehensive view of the loan portfolio composition:

Given market concerns about commercial real estate, particularly office properties, Independent Bank dedicated specific attention to this segment in its presentation. Office loans account for 13.1% ($960.9 million) of the bank’s $7.3 billion CRE and construction portfolio. The bank emphasized that the majority of these loans are conservatively underwritten and primarily Massachusetts-based.

The presentation also highlighted the strength of the bank’s $2.04 billion multifamily portfolio, which showed minimal delinquencies with only 0.1% classified as criticized and 0.1% as non-performing. Approximately 85% of this portfolio is Massachusetts-based, with 99% located in New England.

Strategic Initiatives

Independent Bank’s presentation referenced its acquisition of Enterprise Bancorp, which will significantly expand the bank’s footprint in New England. The combined entity will have approximately $25.0 billion in assets, $20.3 billion in deposits, $18.6 billion in loans, and $8.8 billion in wealth assets under administration, with 151 branches across the region.

According to the earnings call transcript, CEO Jeff Tingle expressed confidence in the bank’s strategic direction, stating, "We have all the ingredients to return INDB to its historical premium valuation." The bank plans to realize full cost synergies from the Enterprise acquisition by Q1 2026.

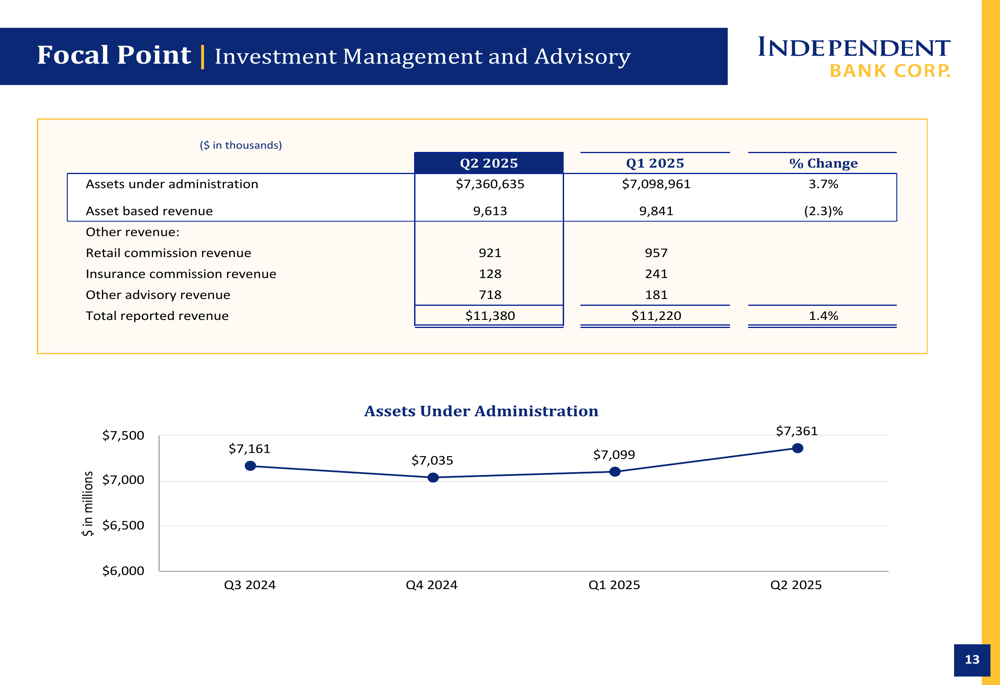

The wealth management business continues to be a strong contributor to fee income, with assets under administration increasing by 3.7% to $7.36 billion in Q2 2025. This segment generated $11.38 million in revenue during the quarter, up 1.4% from Q1 2025.

Forward-Looking Statements

Looking ahead, Independent Bank anticipates low single-digit loan growth and expects flat to slightly down deposit balances. The bank projects a Q3 net interest margin in the mid-3.60% range and plans to maintain its tax rate around 23%.

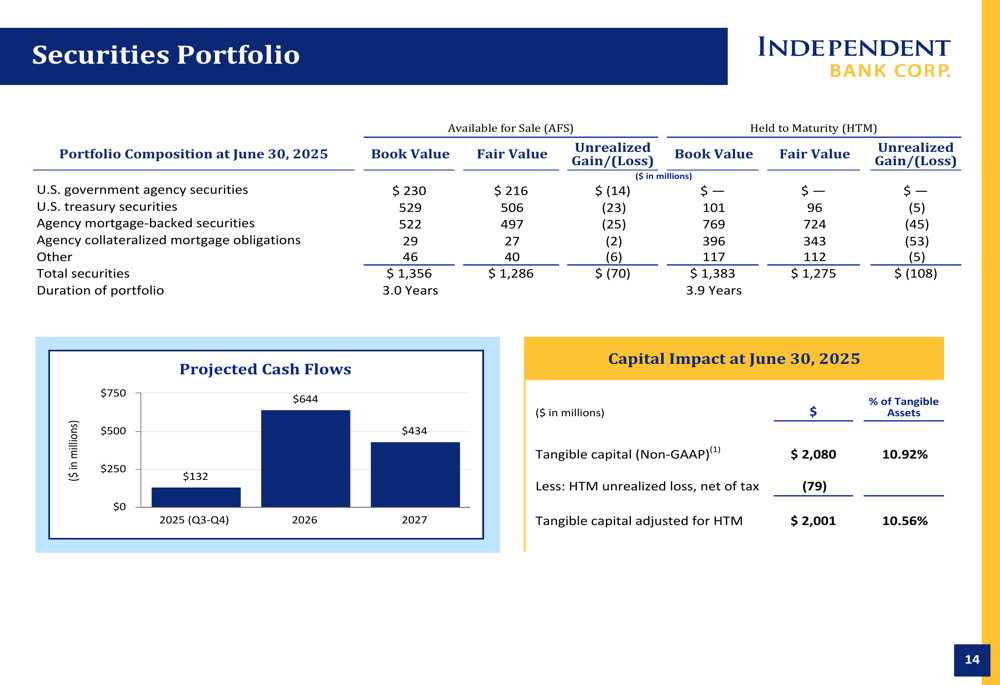

The bank’s securities portfolio, with a combined book value of $2.74 billion split between available-for-sale and held-to-maturity classifications, has projected cash flows of $132 million in 2025, $644 million in 2026, and $434 million in 2027. These cash flows will provide liquidity for future loan growth or other strategic initiatives.

Management noted during the earnings call that there is no immediate appetite for further acquisitions beyond Enterprise Bank, with the focus remaining on integrating this acquisition and addressing commercial real estate exposures.

CFO Mark Bregiro highlighted the bank’s strong positioning, noting, "We’re positioned pretty well on the short end of the curve." This statement reflects confidence in the bank’s ability to navigate the current interest rate environment, which has seen three Federal Reserve rate cuts since September 2024.

Independent Bank’s Q2 2025 presentation demonstrates a bank that is successfully managing asset quality challenges while maintaining profitability and pursuing strategic growth. With its strong capital position, improving asset quality, and strategic acquisition, the bank appears well-positioned to continue its positive trajectory in the New England banking market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.