US stock futures flounder amid tech weakness, Fed caution

Introduction & Market Context

Independent Bank (NASDAQ:INDB) Corporation (NASDAQ:IBCP) presented its second quarter 2025 earnings results on July 24, revealing a mixed financial performance that prompted a market reaction. The Michigan-based community bank reported earnings per share that exceeded analyst expectations, but fell short on revenue targets, leading to a 3.69% stock decline following the announcement.

The bank’s shares closed at $32.84 on July 25, down 1.16% for the day, and currently trade well within their 52-week range of $26.75 to $40.32. Year-to-date, IBCP stock has shown resilience with only a modest decline of 0.29%, despite facing industry-wide challenges in deposit costs and net interest margin pressure.

Quarterly Performance Highlights

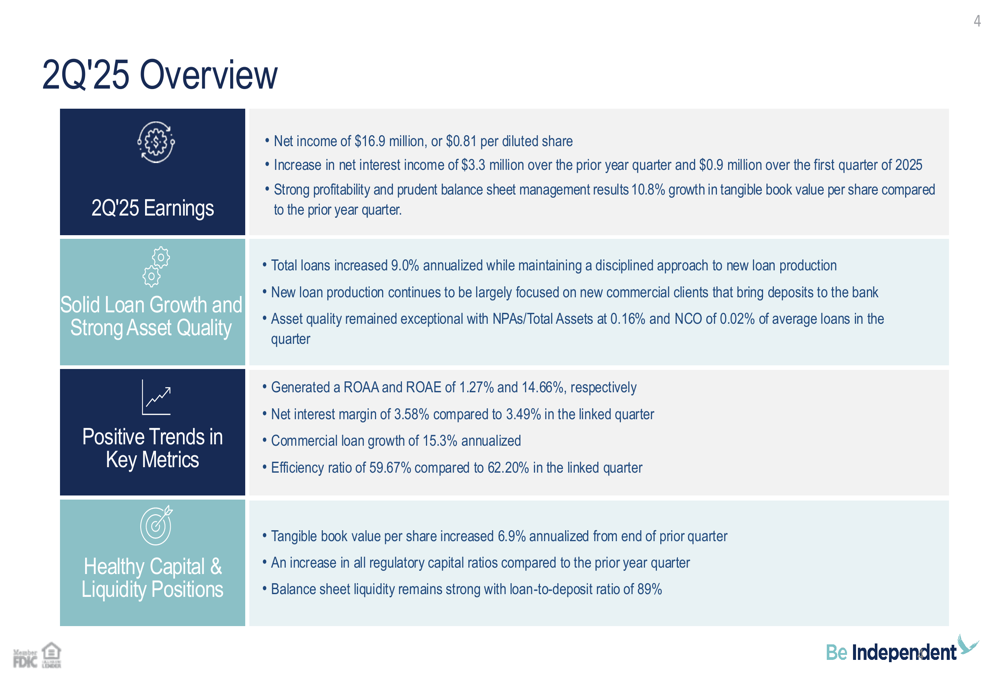

Independent Bank reported net income of $16.9 million for Q2 2025, translating to $0.81 per diluted share, which surpassed analyst forecasts of $0.79. However, this represented a decline from $18.5 million, or $0.88 per share, in the same quarter last year. Total (EPA:TTEF) revenue came in at $54.44 million, below the forecasted $57.11 million.

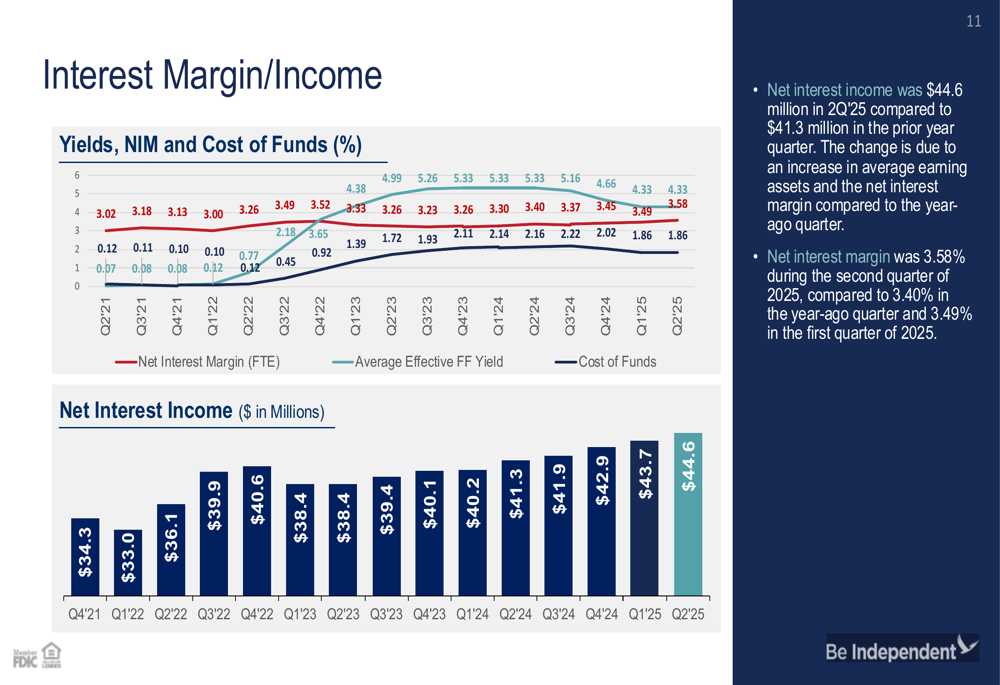

The bank achieved a return on average assets (ROAA) of 1.27% and return on average equity (ROAE) of 14.66%, demonstrating solid profitability metrics despite revenue challenges. Net interest margin improved to 3.58% from 3.49% in the previous quarter, reflecting the bank’s ability to manage its interest-earning assets effectively in the current rate environment.

As shown in the following overview of key performance metrics:

Net interest income increased by $3.3 million compared to the prior year quarter and $0.9 million over the first quarter of 2025, highlighting the bank’s ability to grow its core earnings despite industry headwinds. The efficiency ratio improved to 59.67% from 62.20% in the linked quarter, indicating better operational performance and cost management.

Deposit and Loan Portfolio Analysis

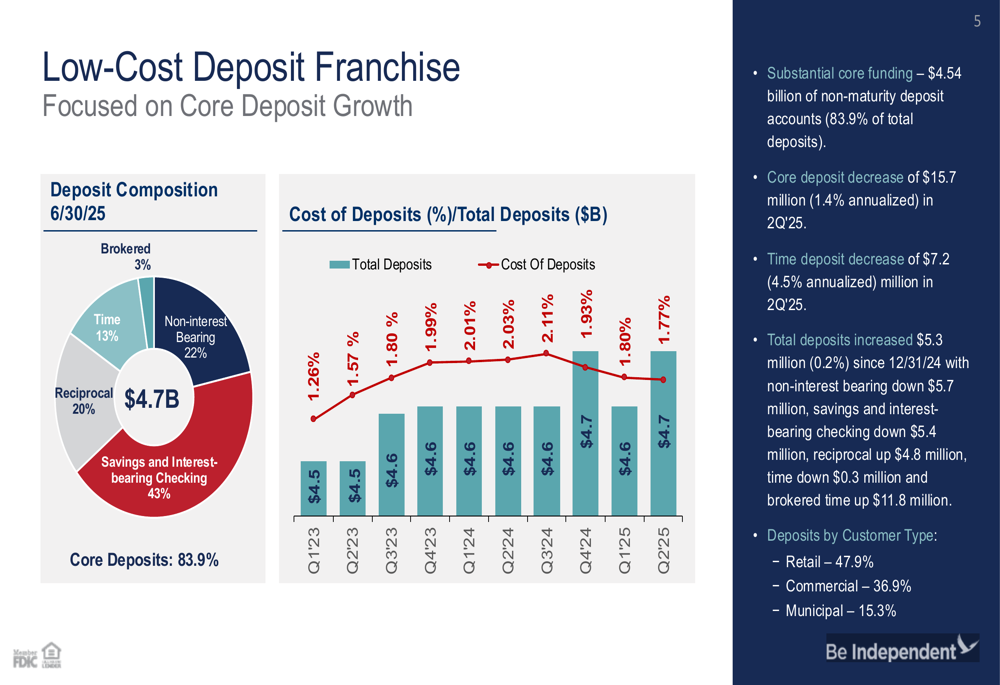

Independent Bank’s deposit franchise remains a key strength, with core deposits representing 83.9% of the total $4.7 billion deposit base. The deposit composition shows a well-diversified mix, with savings and interest-bearing checking accounts comprising the largest segment at 43%, followed by non-interest bearing deposits at 22%.

The following chart illustrates the bank’s deposit composition and cost trends:

While core deposits decreased slightly by $15.7 million (1.4% annualized) in Q2 2025, the bank’s overall deposit costs have risen more slowly than the Federal Funds rate, demonstrating effective liability management. The deposit beta (the percentage of rate changes passed through to depositors) remains favorable compared to industry peers.

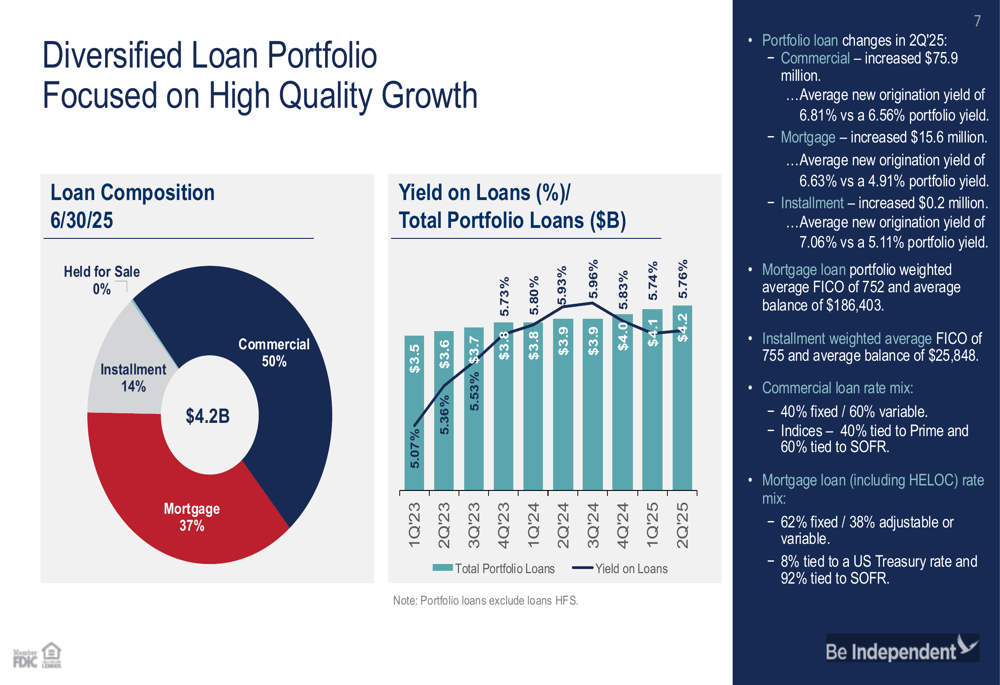

On the lending side, Independent Bank reported strong loan growth, with total loans increasing at a 9.0% annualized rate while maintaining disciplined underwriting standards. Commercial loans, which now represent 50% of the $4.2 billion loan portfolio, grew at an impressive 15.3% annualized rate during the quarter.

The diversification of the loan portfolio is illustrated in this breakdown:

The yield on loans increased to 5.76% in Q2 2025, contributing to the improvement in net interest margin. Management emphasized that new loan production continues to focus on commercial clients who bring deposits to the bank, supporting a relationship-based banking approach rather than transactional lending.

Credit Quality and Capital Position

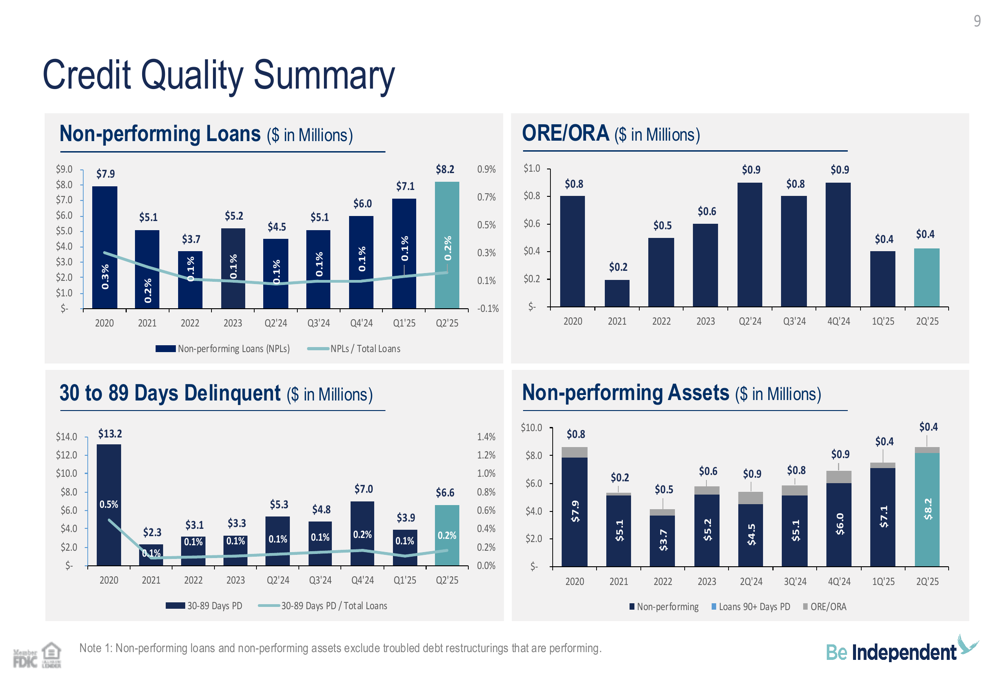

Independent Bank maintained excellent credit quality metrics, with non-performing assets to total assets at just 0.16% and net charge-offs of only 0.02% of average loans in the quarter. The following chart demonstrates the bank’s consistent credit quality performance:

The bank’s capital position remains strong, with all regulatory capital ratios increasing compared to the prior year quarter. Tangible book value per share grew 10.8% compared to the prior year quarter and increased at a 6.9% annualized rate from the end of Q1 2025, reflecting the bank’s continued profitability and prudent balance sheet management.

Net interest income and margin trends show steady improvement despite the challenging interest rate environment:

The net interest income reached $44.6 million in Q2 2025, continuing its upward trajectory from previous quarters. This growth has been supported by both expanding loan balances and improving yields.

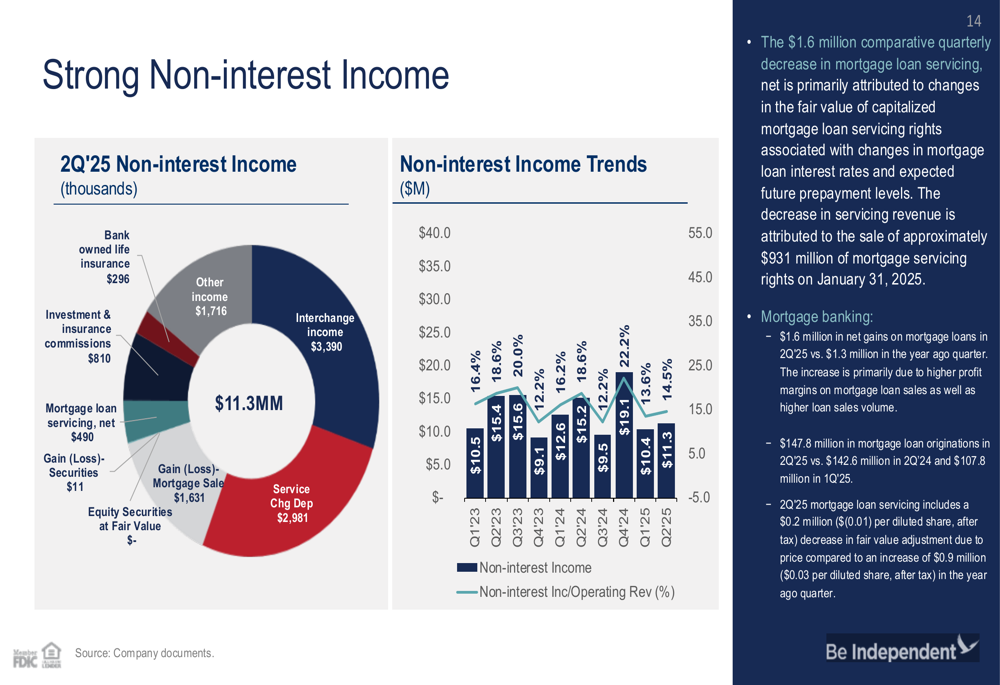

Non-Interest Income and Efficiency

Non-interest income totaled $11.3 million in Q2 2025, with a diverse revenue stream across multiple business lines. However, the bank noted a $1.6 million decrease in mortgage loan servicing income attributed to changes in fair value.

The breakdown of non-interest income sources is shown in the following chart:

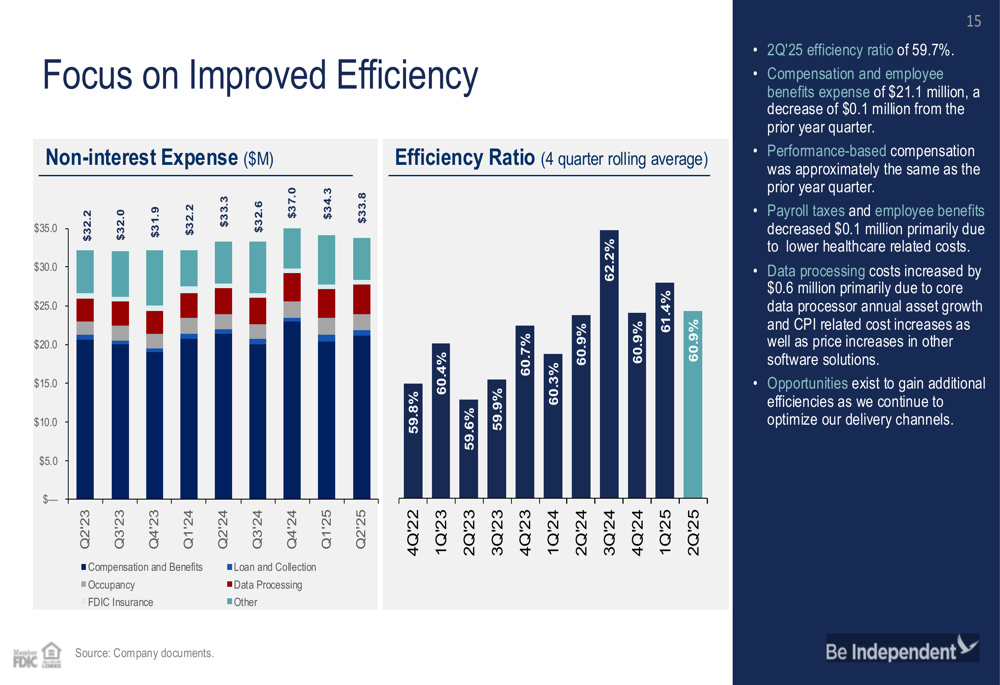

Independent Bank has maintained its focus on operational efficiency, with non-interest expenses well controlled. The efficiency ratio of 59.67% for Q2 2025 represents an improvement from 62.20% in the linked quarter, reflecting the bank’s ongoing efforts to optimize operations while investing in strategic growth initiatives.

The expense trends and efficiency ratio improvements are illustrated here:

Management noted that data processing costs increased by $0.6 million due to annual growth as well as price increases in other software solutions, highlighting the bank’s continued investment in technology infrastructure.

Strategic Initiatives and Outlook

Looking ahead, Independent Bank provided guidance for the remainder of 2025, projecting mid-single digit overall loan growth driven primarily by increases in commercial and mortgage loans. The bank expects high-single digit growth in net interest income, supported by higher average earning assets.

Management anticipates steady asset quality metrics to continue, with provisions for credit losses aligned with loan growth. Non-interest income is forecasted to range between $11.0 million and $12.0 million quarterly for the remainder of 2025.

During the earnings call, CEO Brad Kessel emphasized the importance of organic growth, stating, "Organic growth will continue to be the primary driver of our overall growth." He also highlighted the company’s commitment to AI technology, noting, "We’re using probably several dozen AI use cases around the company."

The bank faces several challenges, including potential Federal Reserve rate cuts that could impact margin outlook, competitive pressures in mortgage loan sale margins, and the need to manage rising deposit costs. However, management expressed confidence in the bank’s ability to navigate these challenges through disciplined growth strategies and operational efficiency improvements.

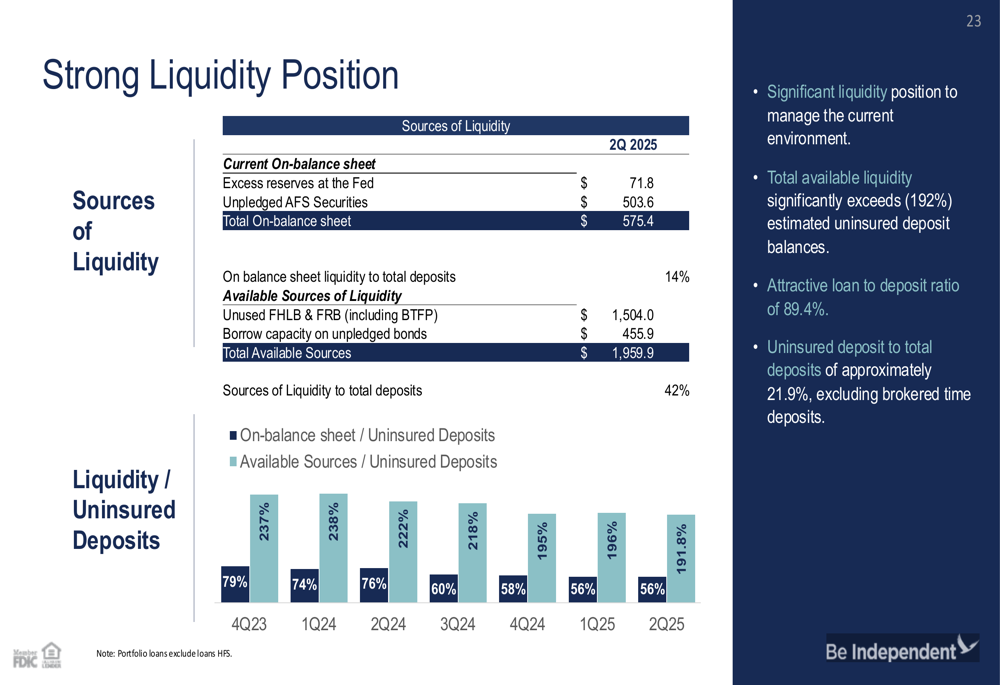

Independent Bank’s strong liquidity position provides a buffer against potential market volatility, with available liquidity significantly exceeding uninsured deposit balances:

This liquidity strength, combined with the bank’s diversified loan portfolio and granular deposit base, positions Independent Bank well for continued stable performance despite economic uncertainties in its key markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.