Bitcoin set for a rebound that could stretch toward $100000, BTIG says

Introduction & Market Context

Indorama Ventures PCL (IVL) reported its first quarter 2025 financial results on May 9, revealing significant pressure on profitability despite robust cash flow generation. The company’s stock rose 5.15% to $20.40 following the release, suggesting investors may be focusing on operational improvements rather than headline earnings figures.

The chemical manufacturer faced multiple headwinds during the quarter, including planned maintenance turnarounds, compressed benchmark spreads, elevated energy costs, and declining ocean freight rates. These challenges occurred against a backdrop of continuing uncertainty in global markets due to tariff impacts and trade tensions.

Quarterly Performance Highlights

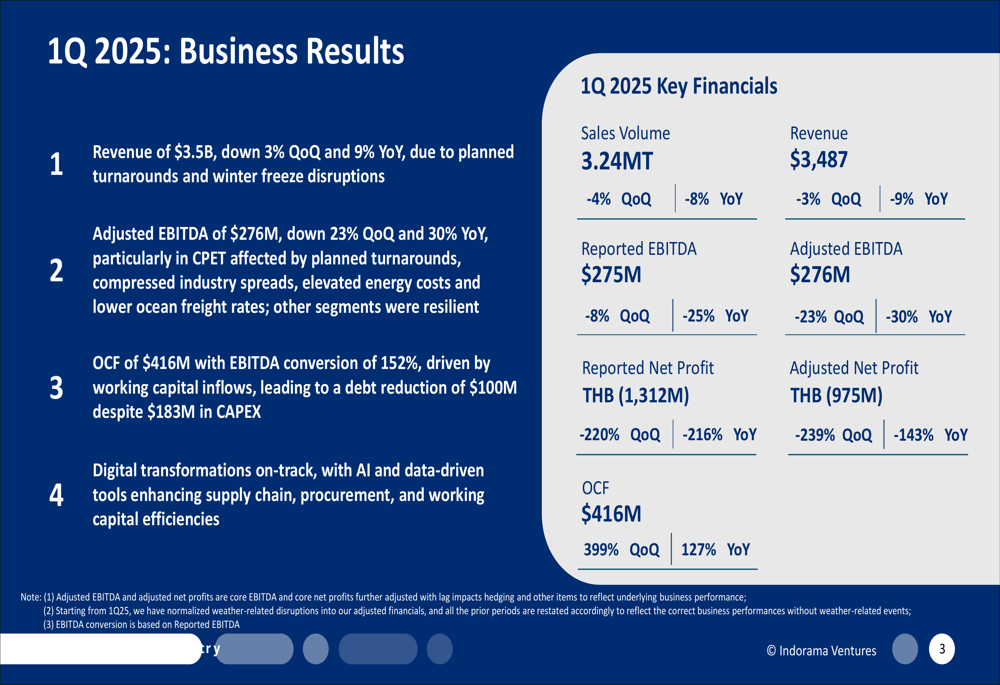

Indorama Ventures reported revenue of $3.5 billion for Q1 2025, representing a 3% decline quarter-over-quarter and a 9% drop year-over-year. More concerning was the 30% year-over-year plunge in Adjusted EBITDA to $276 million, which also fell 23% from the previous quarter.

As shown in the following chart of key financial metrics, the company experienced declines across most performance indicators:

Sales volume decreased to 3.24 million tons, down 4% quarter-over-quarter and 8% year-over-year. The company reported a net loss of THB 1,312 million, a stark reversal from previous periods, representing a 220% decline quarter-over-quarter and 216% year-over-year. Adjusted net profit similarly fell to a loss of THB 975 million.

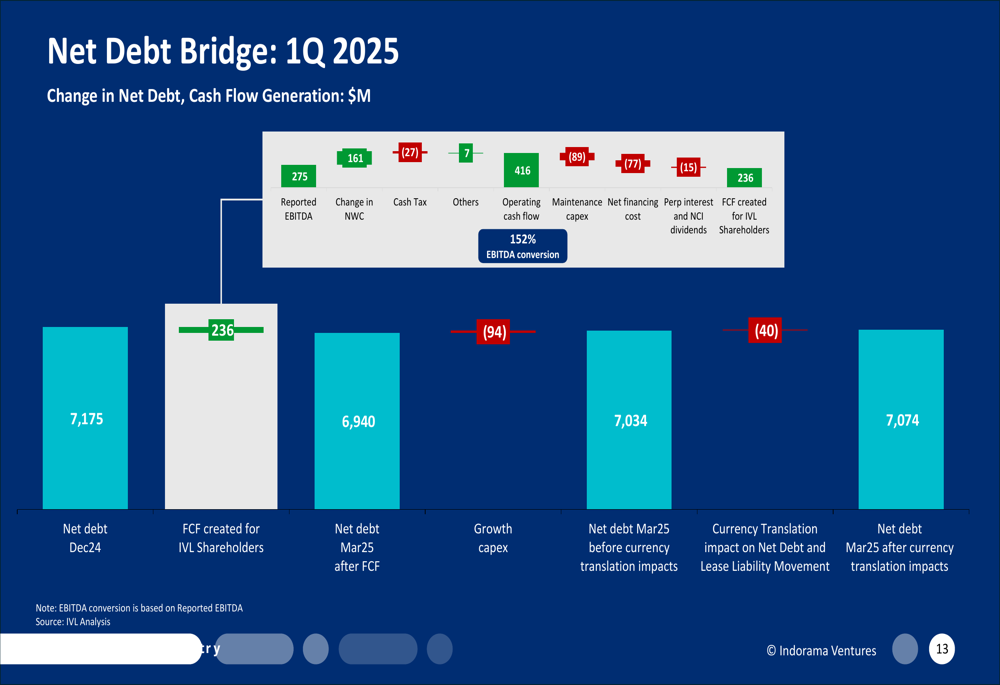

A bright spot in the results was operational cash flow, which surged to $416 million, representing a remarkable 399% increase quarter-over-quarter and 127% year-over-year. This strong cash generation led to an impressive EBITDA conversion rate of 152%, enabling the company to reduce debt by $100 million despite allocating $183 million to capital expenditures.

Segment Performance Analysis

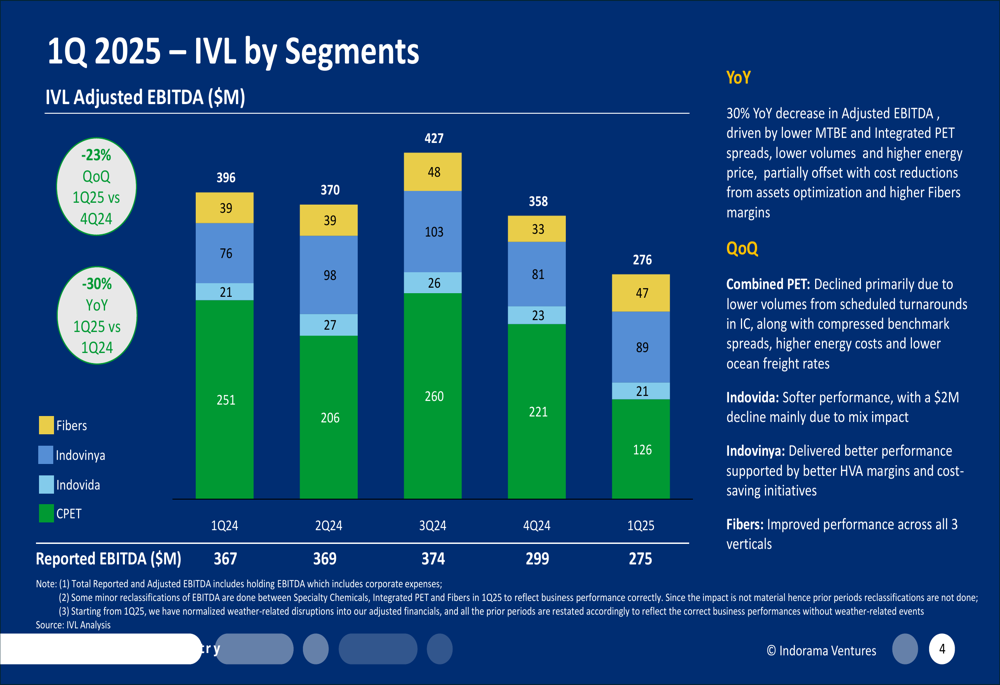

Indorama’s performance varied significantly across business segments, as illustrated in this breakdown:

The Combined PET segment faced the most severe challenges, with Adjusted EBITDA plummeting 50% year-over-year to $116 million. This decline was attributed to lower MTBE and integrated PET spreads, planned turnarounds in Intermediate Chemicals assets, and higher energy prices. The segment was partially supported by fixed cost savings from asset optimization.

In contrast, the Fibers segment emerged as a standout performer, with Adjusted EBITDA increasing 43% quarter-over-quarter and 22% year-over-year to $61 million. This growth was driven by margin recovery in the Lifestyle vertical and ongoing cost-saving initiatives, which helped offset higher energy prices and lower volumes in Europe.

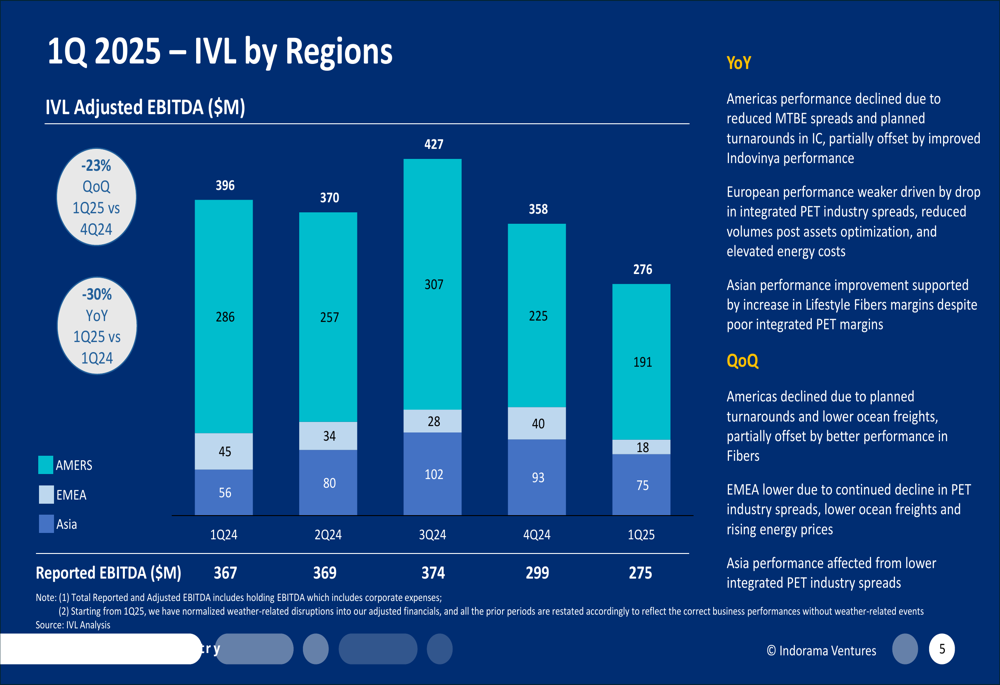

The company’s regional performance also showed divergent trends:

Americas and EMEA regions experienced significant declines, while Asia showed relative resilience. The Americas performance suffered from reduced MTBE spreads and planned turnarounds, partially offset by improved performance in the Indovinya segment. European operations were hampered by dropping integrated PET industry spreads, reduced volumes following asset optimization, and elevated energy costs. Asian performance improved slightly, supported by increased Lifestyle Fibers margins despite poor integrated PET margins.

Strategic Initiatives

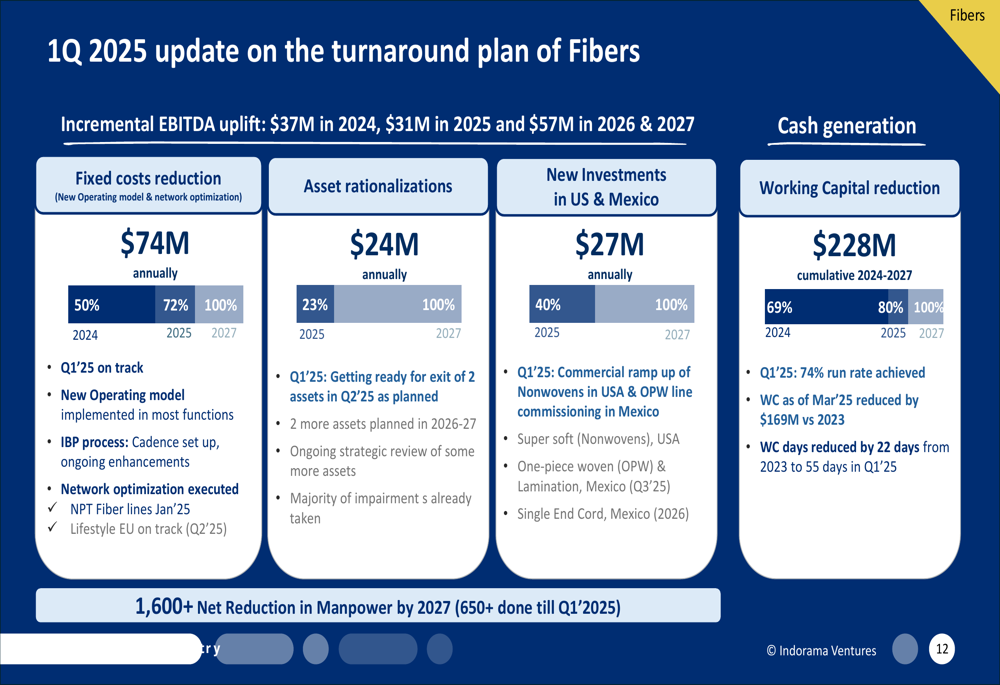

Despite challenging market conditions, Indorama Ventures continues to execute its strategic turnaround plan for the Fibers segment, which is showing promising results:

The company reported that its Fibers turnaround plan is on track, with implementation of a new operating model across most functions. The plan targets $74 million in annual fixed cost reductions, with 72% achieved in 2025 and full implementation expected by 2027. Asset rationalizations are expected to yield $24 million annually, while new investments in the US and Mexico are projected to contribute $27 million annually by 2027.

The plan also includes a significant workforce reduction of over 1,600 positions by 2027, with more than 650 already completed by Q1 2025. These initiatives are expected to deliver incremental EBITDA uplift of $31 million in 2025 and $57 million in 2026-2027.

Indorama is also making progress on working capital management and debt reduction:

The company’s strong operational cash flow of $416 million, combined with a $161 million reduction in net working capital, contributed to a $100 million reduction in net debt during the quarter. This financial discipline is part of Indorama’s broader strategy to strengthen its balance sheet while navigating challenging market conditions.

Forward-Looking Statements

Management provided a cautiously optimistic outlook for the remainder of 2025, noting that uncertainty remains due to macroeconomic factors caused by tariffs. However, they expect Q2 results for the Combined PET segment to improve with normalization of turnaround volumes, improvement in industry spreads, and increased demand.

The company highlighted that its "local-for-local" model provides resilience amid rising trade uncertainty, minimizing cross-border exposure and enhancing supply chain agility across key regions. Management also emphasized their focus on growth beyond the current "IVL 2.0" strategy through strategic partnerships, targeted regional growth, and strict financial discipline.

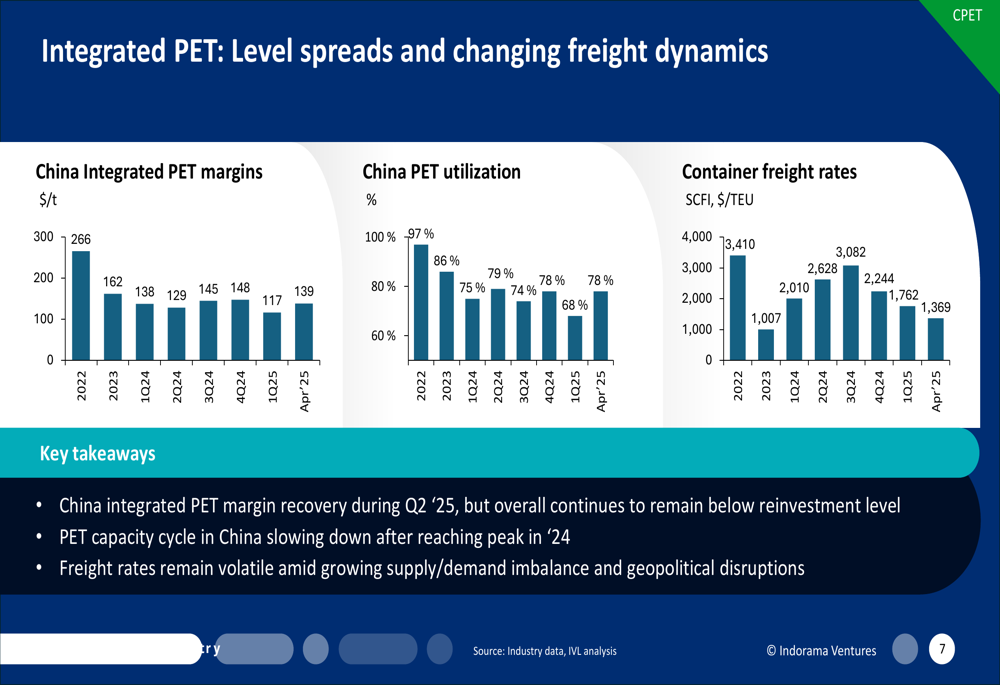

The Integrated PET market remains challenging, with China integrated PET margins continuing below reinvestment levels despite some recovery expected in Q2 2025:

Freight rates also remain volatile amid growing supply/demand imbalance and geopolitical disruptions, adding another layer of complexity to Indorama’s operating environment. However, the company noted that the PET capacity cycle in China appears to be slowing down after reaching its peak in 2024, which could eventually lead to more balanced market conditions.

As Indorama Ventures navigates these challenges, its diversified business model and ongoing strategic initiatives may provide a foundation for recovery in the coming quarters, despite the significant headwinds faced in Q1 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.