ION expands ETF trading capabilities with Tradeweb integration

Introduction & Market Context

Indorama Ventures PCL (IVL) presented its second quarter 2025 results on August 20, showing sequential improvement amid ongoing industry challenges and global trade tensions. The chemical and petrochemical manufacturer reported a 20% quarter-on-quarter increase in adjusted EBITDA, driven by improved volumes following first-quarter disruptions and better performance in its Combined PET segment.

The company's stock was trading at 20.3, up 2.96% on the day of the presentation, showing positive market reaction to the results. This comes after a challenging period for the company, which had seen its stock fall significantly from its 52-week high of 27.5.

Quarterly Performance Highlights

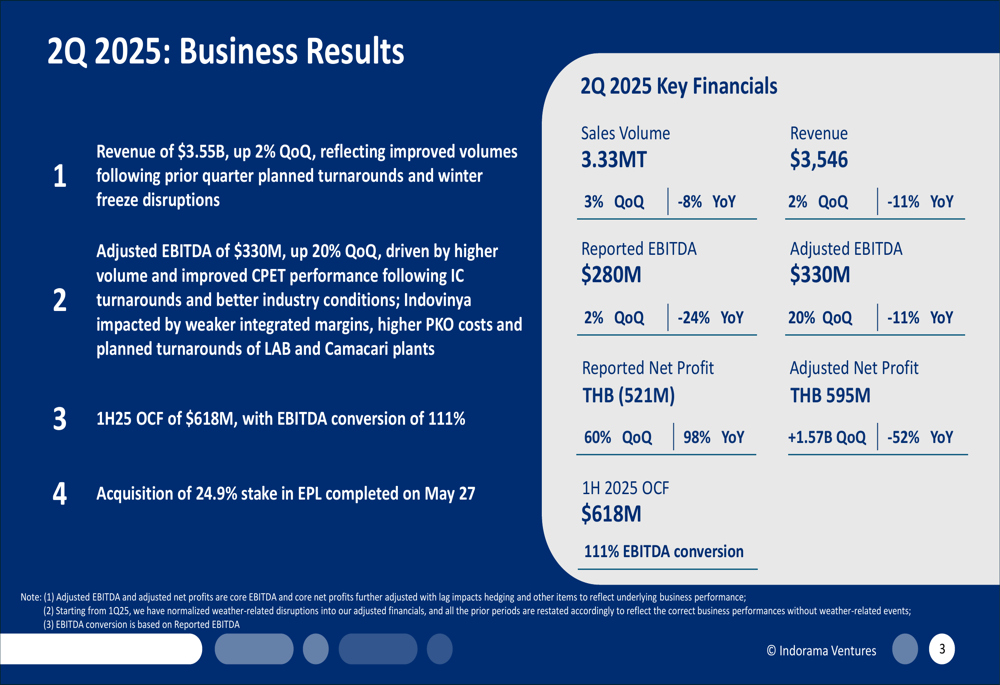

Indorama Ventures reported Q2 2025 revenue of $3.55 billion, up 2% quarter-on-quarter, primarily driven by improved volumes following turnarounds and winter freeze disruptions in the previous quarter. Adjusted EBITDA reached $330 million, a significant 20% increase from Q1, though still down 11% year-on-year.

As shown in the following comprehensive financial overview from the presentation:

Sales volume for the quarter stood at 3.33 million tons, representing a 3% increase quarter-on-quarter but an 8% decrease year-on-year. The company reported a net loss of THB 521 million on a reported basis, though this represented a 60% improvement from the previous quarter. On an adjusted basis, net profit was THB 595 million, a substantial improvement of THB 1.57 billion from Q1 2025.

Operating cash flow for the first half of 2025 reached $618 million with an impressive EBITDA conversion rate of 111%, highlighting the company's focus on cash generation and working capital efficiency.

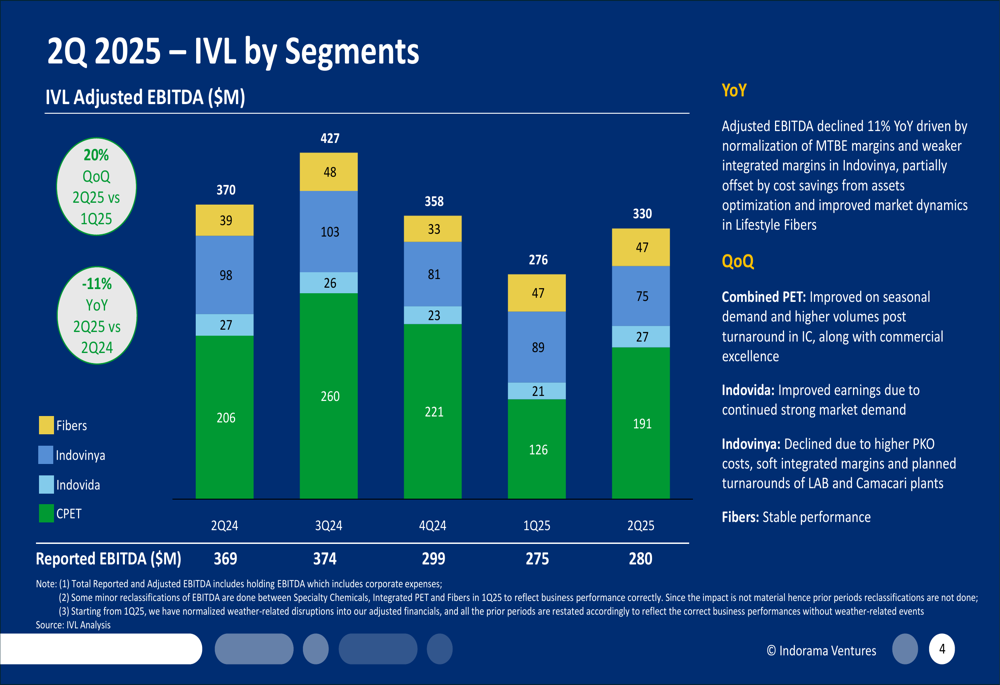

Segment Performance Analysis

Indorama Ventures' performance varied across its business segments, with Combined PET showing improvement while Indovinya faced challenges. The following chart breaks down the company's adjusted EBITDA by segment:

The Combined PET segment delivered an adjusted EBITDA of $191 million in Q2 2025, up significantly from $126 million in Q1. This improvement was driven by increased volumes, better business conditions, commercial excellence initiatives, and lower energy prices. However, year-on-year performance was down 7% due to normalization of MTBE margins and higher energy prices.

The Indovinya segment faced headwinds with adjusted EBITDA declining to $75 million, down 16% quarter-on-quarter and 24% year-on-year. This decline was attributed to planned turnarounds in LAB and Camacari plants, trough cycle Essentials business, and reduced integrated margins due to trade volatility.

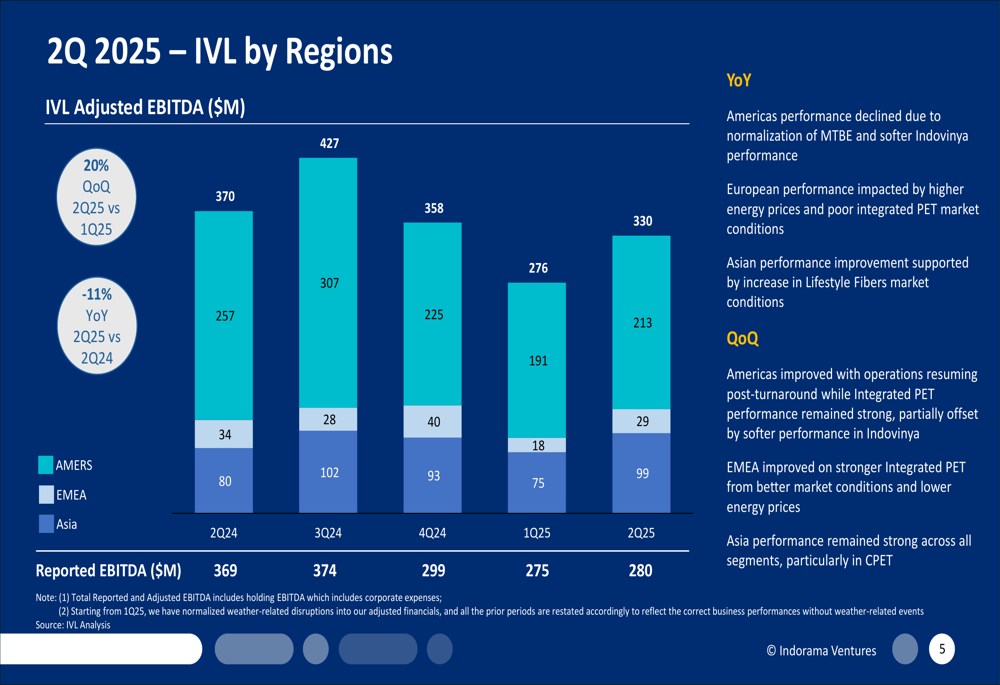

Regional performance showed improvements in Americas and EMEA, while Asia remained strong, as illustrated in this regional breakdown:

The Americas region, which accounts for approximately 50% of IVL's EBITDA, improved with operations resuming post-turnaround while Integrated PET performance remained strong. EMEA improved on stronger Integrated PET performance from better market conditions and lower energy prices, while Asia performance remained strong across all segments, particularly in CPET.

Strategic Initiatives and Turnaround Plan

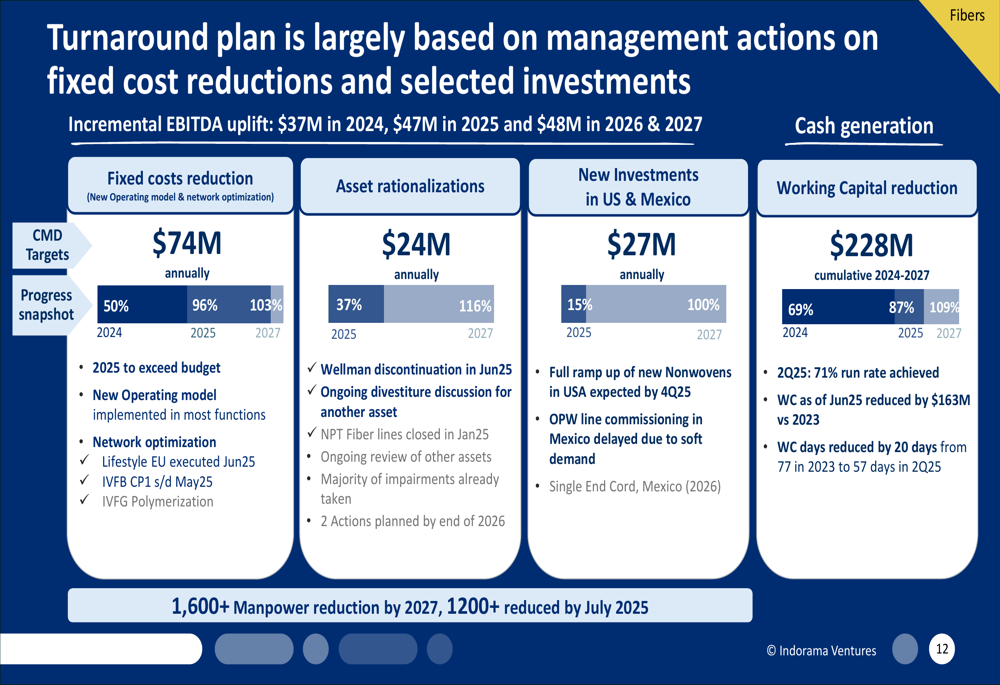

A key focus of Indorama Ventures' presentation was its ongoing turnaround plan, which is showing significant progress across multiple fronts. The company outlined its cost reduction initiatives and their implementation status:

The turnaround plan targets fixed cost reductions of $74 million annually, with 96% of the 2025 target already achieved. Asset rationalizations are expected to deliver $24 million annually, with 37% of the 2025 target achieved. New investments in the US and Mexico are projected to contribute $27 million annually.

Working capital reduction has reached a 71% run rate, with working capital days reduced from 77 in 2023 to 57 days in Q2 2025. The company has also reduced its workforce by over 1,200 employees by July 2025, progressing toward its target of 1,600+ reductions by 2027.

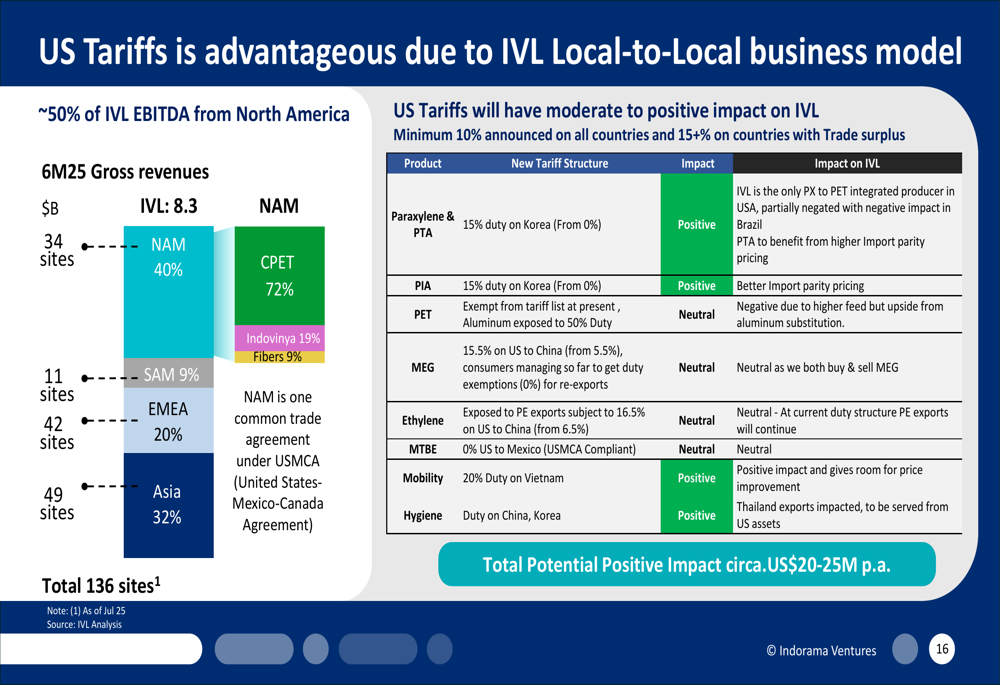

Indorama Ventures also highlighted its strategic positioning amid global trade tensions, particularly US tariffs. The company's "local-for-local" business model is expected to provide resilience and potentially benefit from these tariffs:

The company estimates a potential positive impact of approximately $20-25 million per annum from US tariffs, particularly in products like Paraxylene, PTA, PIA, Mobility, and Hygiene segments.

Financial Position and Outlook

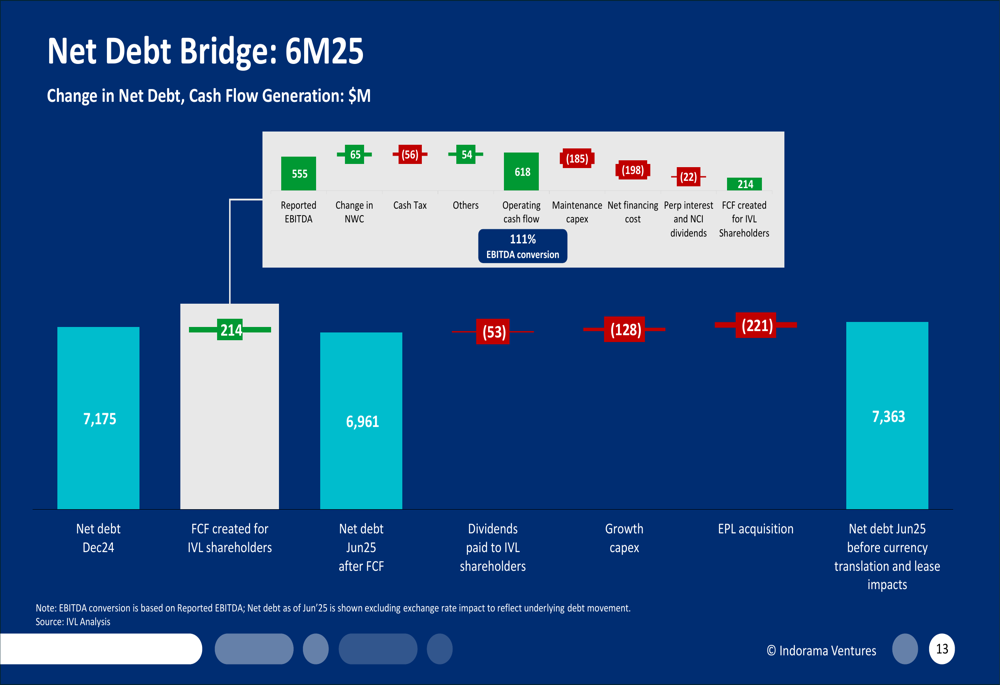

Indorama Ventures provided a detailed breakdown of its debt position and cash flow generation. The following chart illustrates the company's net debt bridge for the first half of 2025:

The company generated free cash flow of $214 million for IVL shareholders in the first six months of 2025. Net debt as of June 2025 stood at $7,363 million, impacted by dividends paid to shareholders ($53 million), growth capex ($128 million), and the EPL acquisition ($221 million).

The company maintains a liquidity position of $1.8 billion and has reduced its interest rate to 4.7%, down 22 basis points from 2024. The adjusted net debt-to-equity ratio stands at 1.39.

Looking ahead, Indorama Ventures expects improvement in Q3 with normalized PKO prices, seasonal demand from the crop season, and normalization of turnarounds in the Indovinya segment. However, the Fibers segment is expected to remain traditionally weaker in Q3 due to European holidays.

The company completed a 24.9% acquisition of EPL in May 2025 and continues to focus on its turnaround plan execution. Management acknowledged ongoing macro volatility from tariffs and trade measures but emphasized that IVL's local-for-local model has proven to provide resilience in this environment.

In summary, Indorama Ventures' Q2 2025 results show sequential improvement and progress on strategic initiatives, though year-on-year comparisons remain challenging. The company's focus on cost reduction, working capital efficiency, and strategic positioning amid global trade tensions appears to be yielding positive results.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.