Intel stock spikes after report of possible US government stake

Introduction & Market Context

Informatica Inc (NYSE:INFA) released its first quarter 2025 earnings presentation on May 7, 2025, showcasing strong cloud growth as the company continues its strategic shift toward a cloud-only business model. The data management solutions provider reported results that exceeded guidance across key metrics while maintaining robust profitability.

The company’s shares closed at $18.73 before the earnings release, rising 1.71% during the trading session. In after-hours trading, the stock held steady at $19.03, suggesting investors were largely satisfied with the results.

Quarterly Performance Highlights

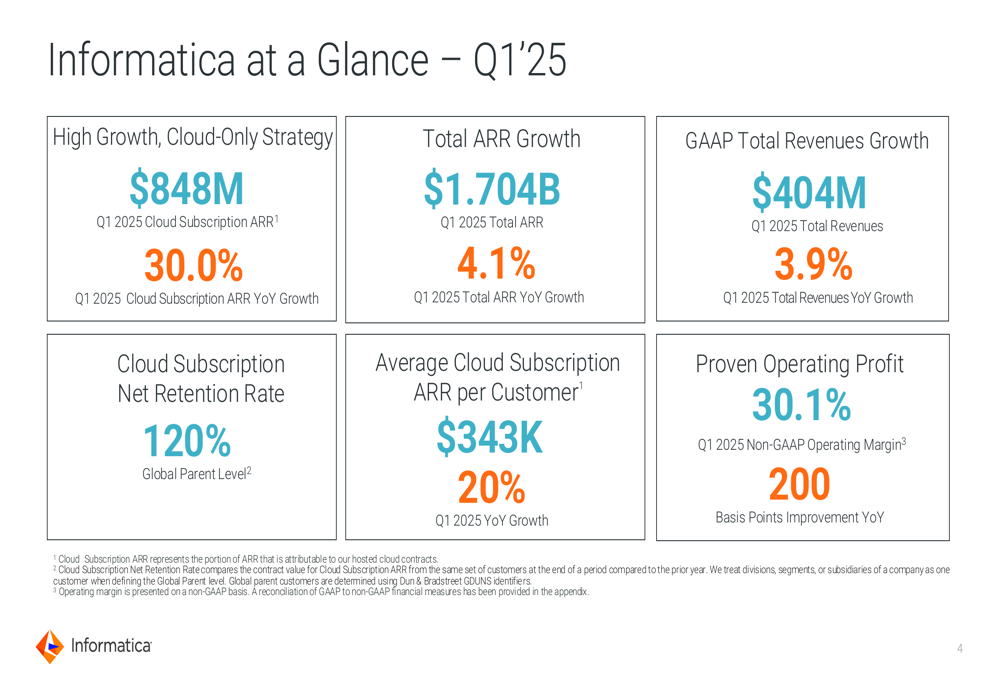

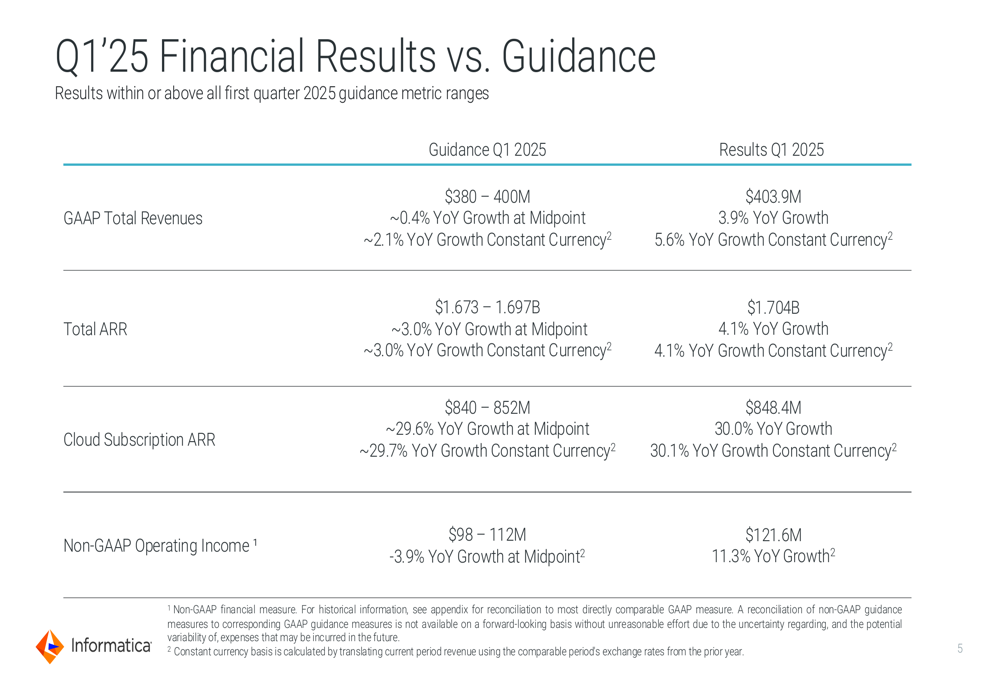

Informatica reported total revenues of $403.9 million for Q1 2025, representing a 3.9% year-over-year increase, or 5.6% growth in constant currency. This performance exceeded the high end of the company’s guidance range of $380-400 million. The company’s total Annual Recurring Revenue (ARR) reached $1.704 billion, growing 4.1% year-over-year and also surpassing the guidance range of $1.673-1.697 billion.

As shown in the following comprehensive overview of Q1 2025 performance:

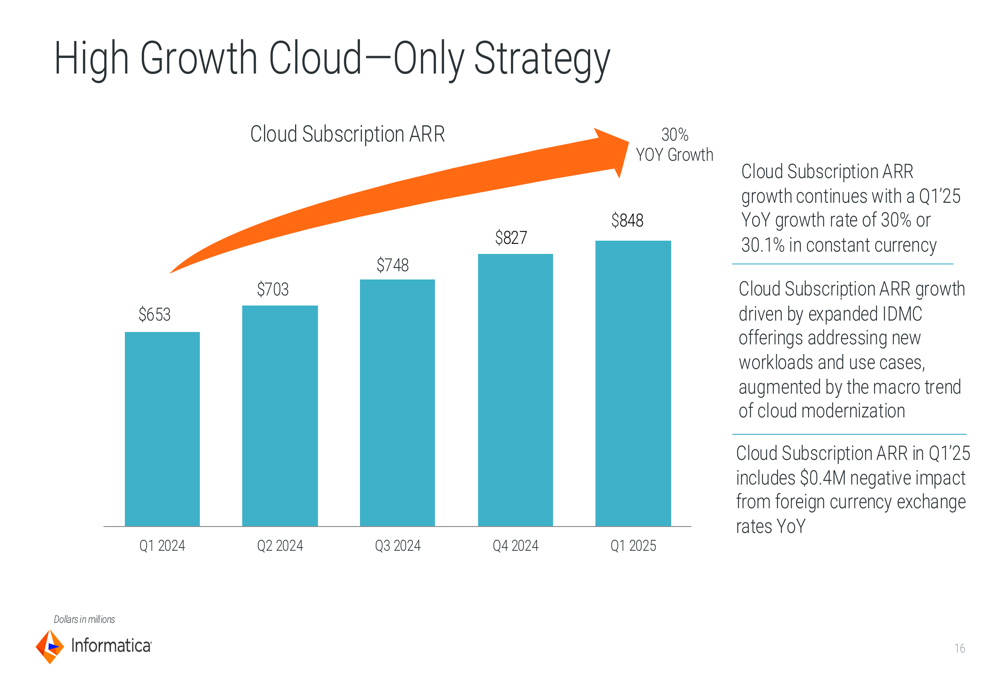

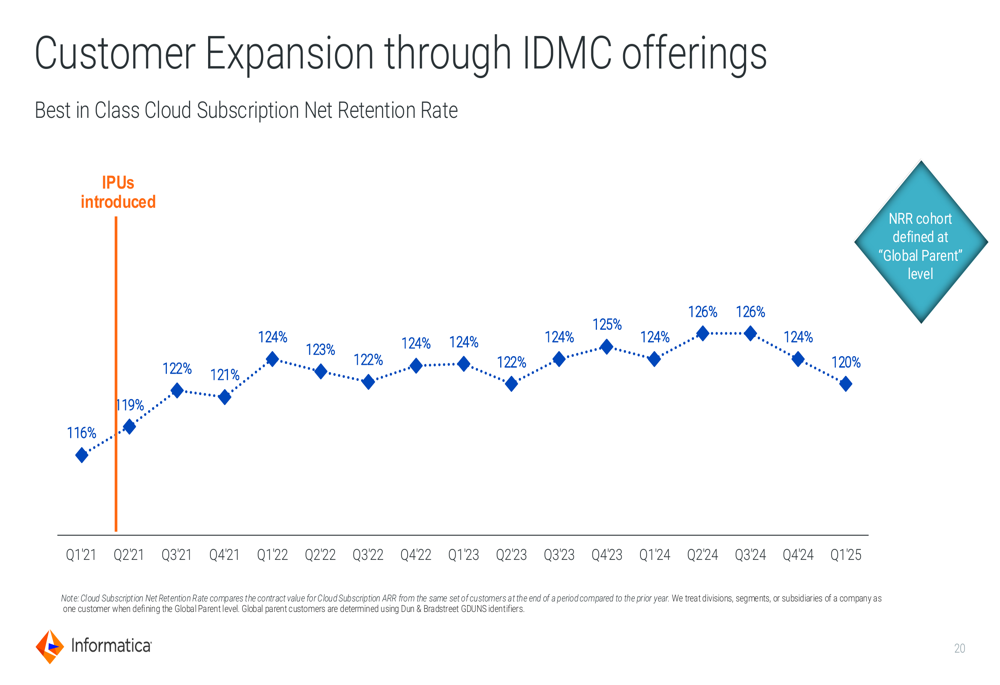

Cloud Subscription ARR, a critical metric for Informatica’s transformation, reached $848.4 million with impressive 30.0% year-over-year growth. The company also maintained a strong Cloud Subscription Net Retention Rate of 120% at the Global Parent level, indicating high customer satisfaction and expansion.

Informatica’s performance against guidance was particularly strong, with all metrics either meeting or exceeding expectations:

Non-GAAP Operating Income of $121.6 million grew 11.3% year-over-year, significantly above the guidance range of $98-112 million. This demonstrates the company’s ability to drive profitability while investing in cloud growth.

Cloud Strategy and Customer Metrics

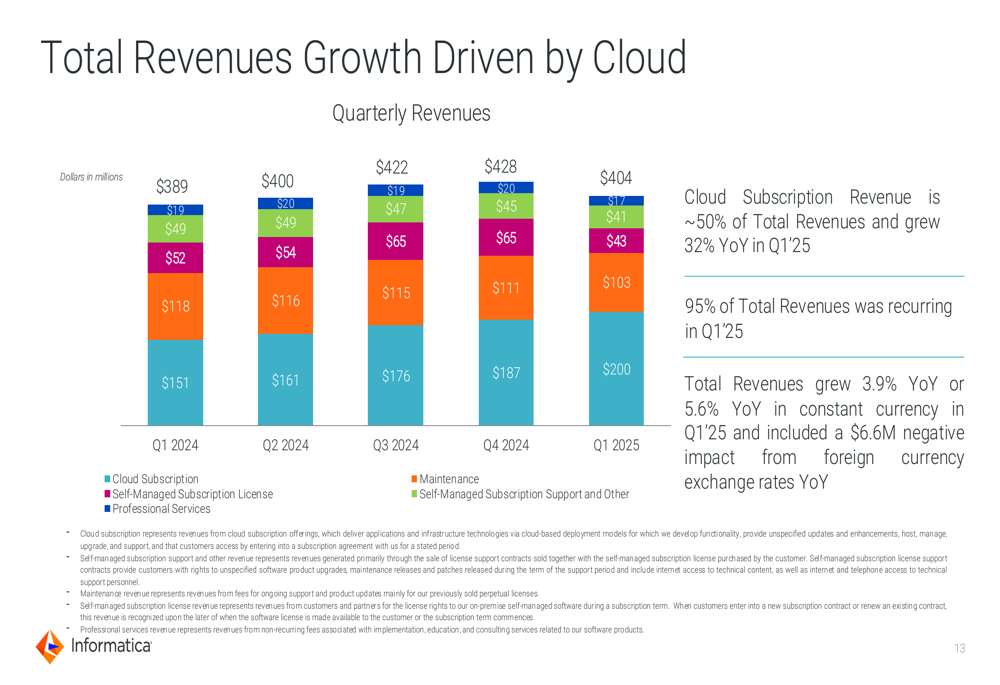

Informatica’s cloud-only strategy continues to gain momentum, with Cloud Subscription Revenue now representing approximately 50% of total revenues. This marks a significant milestone in the company’s transformation journey, as cloud revenues grew 32% year-over-year in Q1 2025.

The following chart illustrates the ongoing shift in revenue composition toward cloud offerings:

The company’s Cloud Subscription ARR growth remains robust, driven by expanded offerings addressing new workloads and use cases, augmented by the broader trend of cloud modernization:

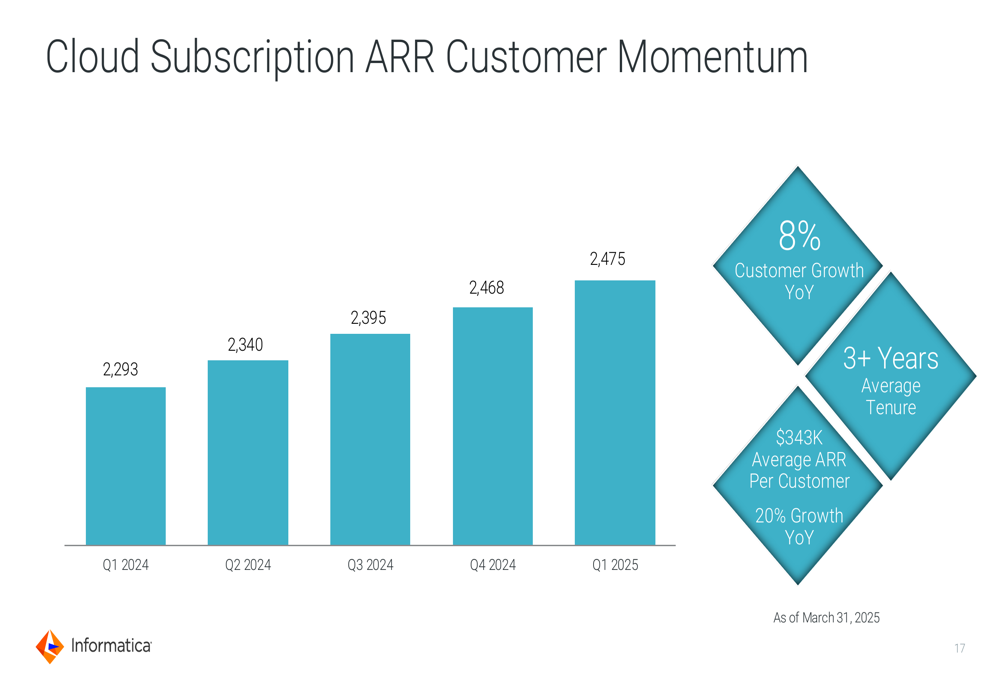

Informatica’s customer metrics also show healthy growth, with the average Cloud Subscription ARR per customer reaching $343,000, up 20% year-over-year. The company now serves 2,475 cloud customers, representing 8% growth from the previous year:

The company’s ability to expand within its customer base is evident in its strong net retention rate, which has consistently remained above 120% since 2021:

Competitive Position and Strategic Initiatives

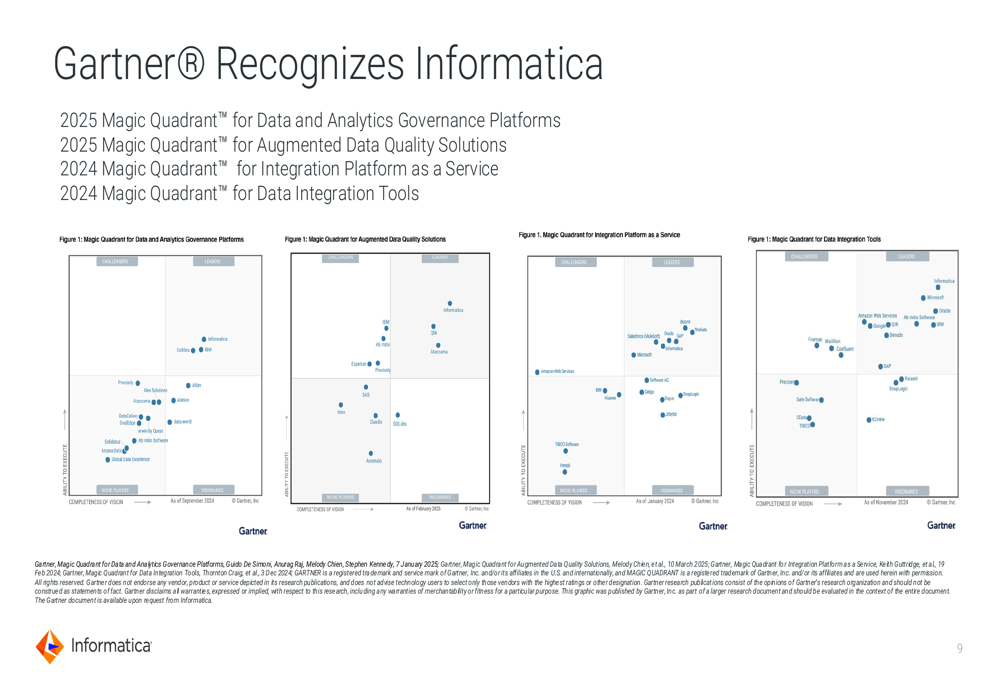

Informatica continues to strengthen its competitive position, being recognized as a Leader in multiple Gartner (NYSE:IT) Magic Quadrant reports, including Data and Analytics Governance Platforms, Augmented Data Quality Solutions, Integration Platform as a Service, and Data Integration Tools:

The company maintains a cloud-neutral strategy, partnering with major cloud providers including Oracle (NYSE:ORCL) Cloud, AWS, Microsoft (NASDAQ:MSFT) Azure, Google (NASDAQ:GOOGL) Cloud, Databricks, and Snowflake (NYSE:SNOW). This approach allows Informatica to serve customers regardless of their cloud infrastructure choices. The scale of the company’s cloud operations is impressive, processing over 119 trillion cloud transactions per month, up from just 0.2 trillion in 2015.

Informatica’s global customer base spans various industries, with 80+ of the Fortune 100 companies using its solutions:

During Q1 2025, the company introduced several innovations, including CLAIRE Copilot for Data Integration and iPaaS, and CLAIRE GPT integration for Master Data Management. Informatica also expanded partnerships with Databricks and Google, and appointed Krish Vitaldevara as chief product officer.

Financial Analysis and Profitability

Despite the ongoing transition to a cloud-based model, Informatica has maintained strong profitability metrics. The company reported a Non-GAAP Gross Profit Margin of 82% for Q1 2025, consistent with previous quarters. Non-GAAP Operating Margin improved to 30.1%, representing a 200 basis point increase year-over-year.

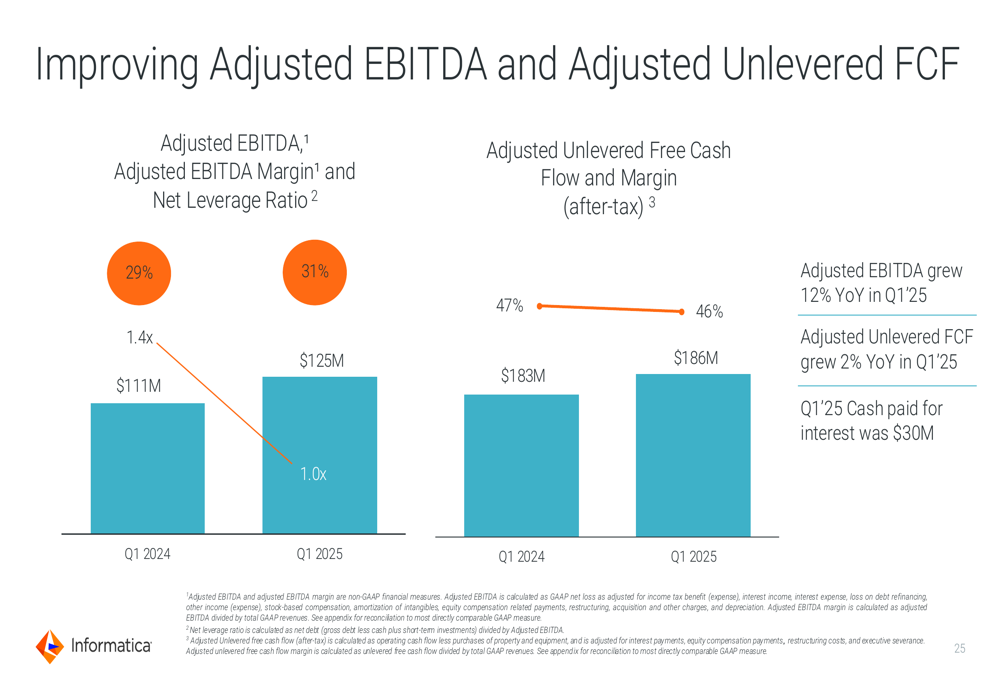

Adjusted EBITDA and Adjusted Unlevered Free Cash Flow both showed improvement, with Adjusted EBITDA growing 12% year-over-year to $125 million (31% of revenue) and Adjusted Unlevered FCF increasing 2% to $186 million (46% of revenue):

The company continues to return capital to shareholders, spending $100 million to repurchase 4.9 million shares during the first quarter, reducing the total outstanding share count by 2.8%.

Forward-Looking Statements

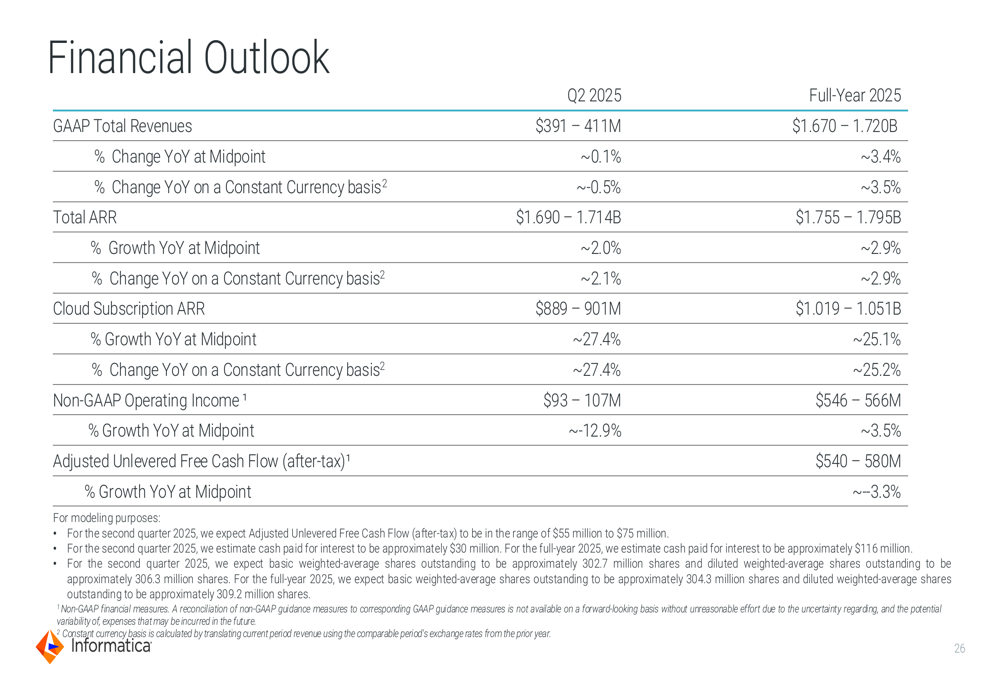

For the second quarter of 2025, Informatica provided the following guidance:

- GAAP Total (EPA:TTEF) Revenues of $391-411 million (~0.1% YoY at midpoint)

- Total ARR of $1.690-1.714 billion (~2.0% YoY at midpoint)

- Cloud Subscription ARR of $889-901 million (~27.4% YoY at midpoint)

- Non-GAAP Operating Income of $93-107 million

For the full year 2025, the company expects:

- GAAP Total Revenues of $1.670-1.720 billion (~3.4% YoY)

- Total ARR of $1.755-1.795 billion (~2.9% YoY)

- Cloud Subscription ARR of $1.019-1.051 billion (~25.1% YoY)

- Non-GAAP Operating Income of $546-566 million (~3.5% YoY)

- Adjusted Unlevered Free Cash Flow of $540-580 million

The guidance reflects Informatica’s continued focus on cloud growth while maintaining profitability. The company’s cloud modernization opportunity remains significant, with only 10.7% of its maintenance and self-managed ARR base having migrated to cloud subscription ARR so far. These migrations have historically generated an average uplift ratio of 1.9x, though the company expects this to moderate to a range of 1.5x to 1.7x for FY25.

Conclusion

Informatica’s Q1 2025 results demonstrate the company’s successful execution of its cloud-first strategy, with strong cloud growth, improving profitability, and consistent customer expansion. The milestone of cloud subscription revenue reaching approximately 50% of total revenues marks a significant point in the company’s transformation journey.

While the growth in traditional segments continues to decline as expected, the robust performance in cloud offerings more than compensates for this planned transition. With a strong competitive position, expanding partnerships, and significant remaining modernization opportunity, Informatica appears well-positioned to continue its growth trajectory in the evolving data management market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.