Oracle stock falls after report reveals thin margins in AI cloud business

Introduction & Market Context

ING Groep NV ( AMS (VIE:AMS2):AS:INGA) presented its first quarter 2025 results on May 2, 2025, highlighting record deposit growth and strong fee income performance. The Dutch banking group demonstrated resilience in its commercial operations while announcing a new €2 billion share buyback program, underscoring its solid capital position and commitment to shareholder returns.

Quarterly Performance Highlights

ING reported strong growth across key performance indicators in Q1 2025, with particularly impressive results in deposit growth and fee income. The bank added 174,000 mobile primary customers during the quarter, slightly below the 182,000 added in Q1 2024, but maintained that over 36% of its 40 million customers are now mobile primary.

As shown in the following key performance indicators chart, ING achieved substantial growth in several core metrics compared to the same period last year:

Net core lending grew by €6.8 billion (4% annualized), up from €4.2 billion in Q1 2024, primarily driven by mortgage lending. Even more impressive was the bank’s net core deposit growth of €22.6 billion (13% annualized), which ING described as "the highest ever" and significantly higher than the €13.5 billion recorded in Q1 2024.

Fee income reached €1,094 million, representing 10% growth compared to Q1 2024’s €998 million, with Retail Banking being the main driver. The bank also reported a 23% increase in sustainable finance mobilized, reaching €30 billion versus €25 billion in the prior-year period.

Detailed Financial Analysis

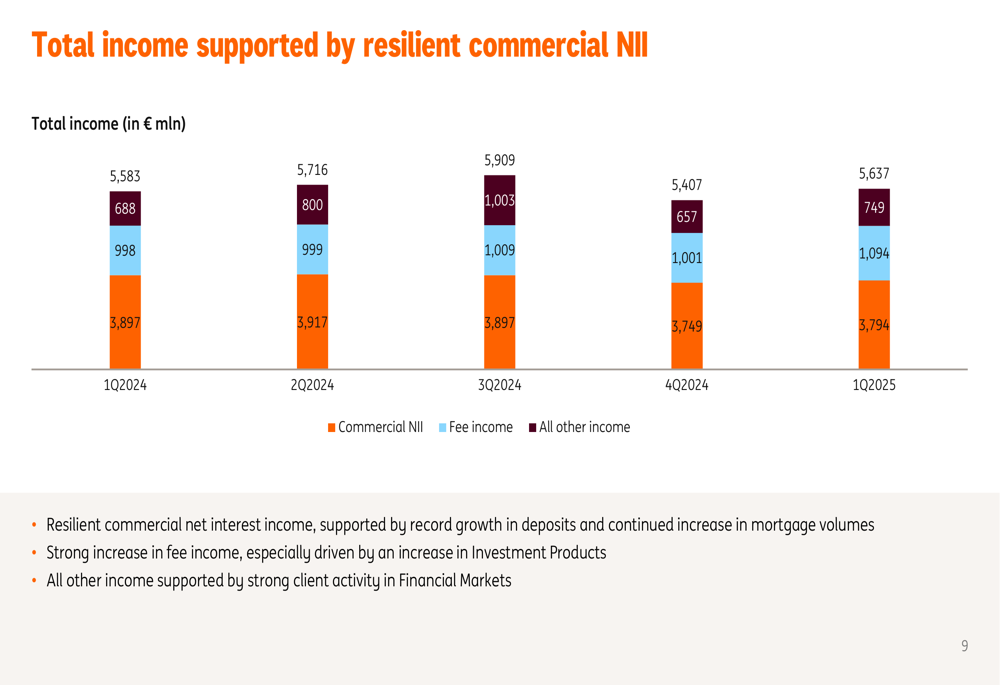

ING’s total income for Q1 2025 reached €5,637 million, showing resilience despite interest rate pressures. The breakdown reveals that commercial net interest income remained stable, while fee income and other income sources contributed to overall performance.

The following chart illustrates ING’s total income by category over the past five quarters:

Commercial net interest income (NII) remained relatively stable at €3,794 million in Q1 2025 compared to €3,897 million in Q1 2024. This resilience was supported by record growth in deposits, which helped offset some pressure on margins. Fee income showed strong growth at €1,094 million, while other income contributed €749 million, benefiting from increased client activity.

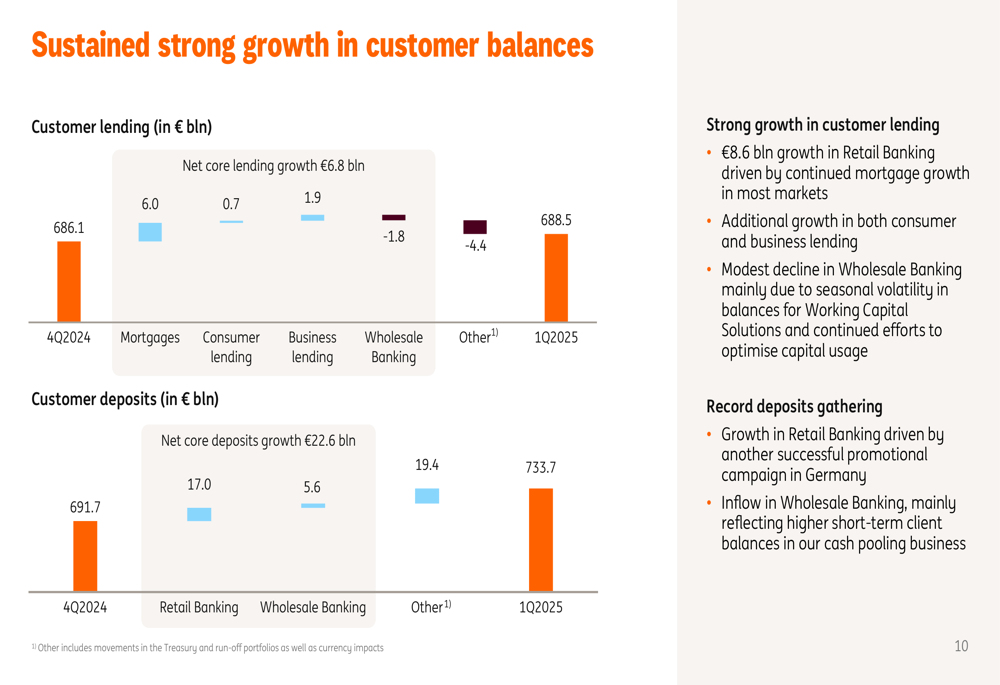

Customer balance growth was particularly strong on the deposit side, as shown in the following chart:

Customer deposits increased from €691.7 billion in Q4 2024 to €733.7 billion in Q1 2025, with net core deposit growth of €22.6 billion. This growth was primarily driven by Retail Banking (€17.0 billion) and Wholesale Banking (€5.6 billion). On the lending side, customer lending grew modestly from €686.1 billion to €688.5 billion, with mortgages contributing €6.0 billion to net core lending growth, while Wholesale Banking saw a modest decline of €1.8 billion.

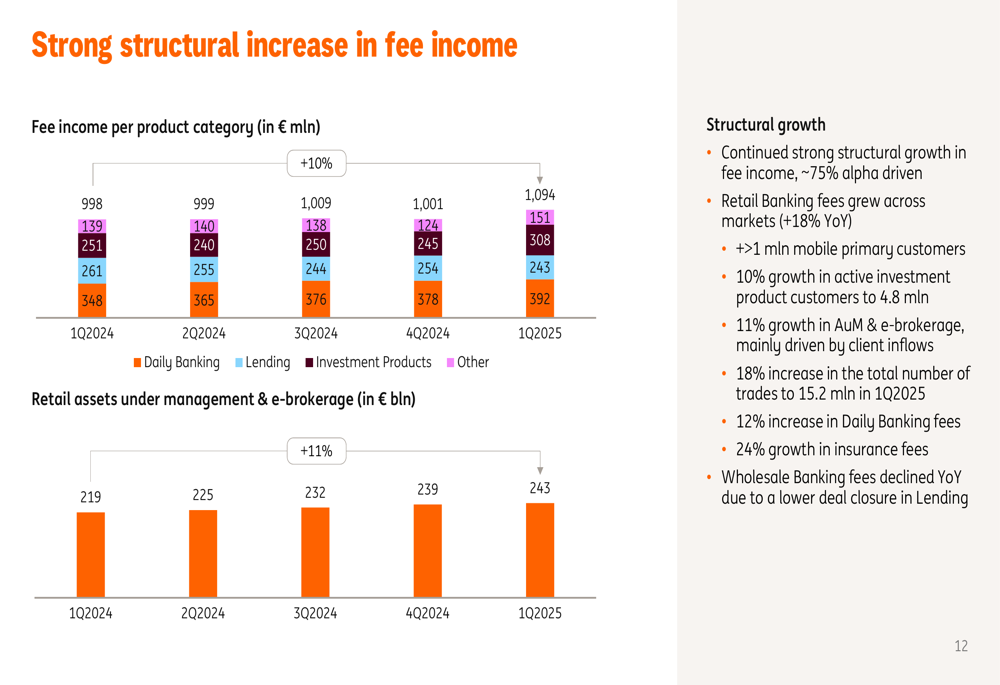

Fee income growth was a particular bright spot in ING’s Q1 results, as illustrated in the following breakdown:

The bank reported continued strong structural growth in fee income, supported by over 1 million new mobile primary customers, 10% growth in investment product customers, and 11% growth in assets under management (AUM). Daily banking, lending, and investment products all contributed to the overall 10% year-on-year growth in fee income.

Operating expenses increased to €2,835 million in Q1 2025 from €2,670 million in Q1 2024, reflecting continued inflationary pressures and additional investments in the business, partially offset by operational efficiencies. Regulatory costs remained stable at €361 million compared to €358 million in Q1 2024.

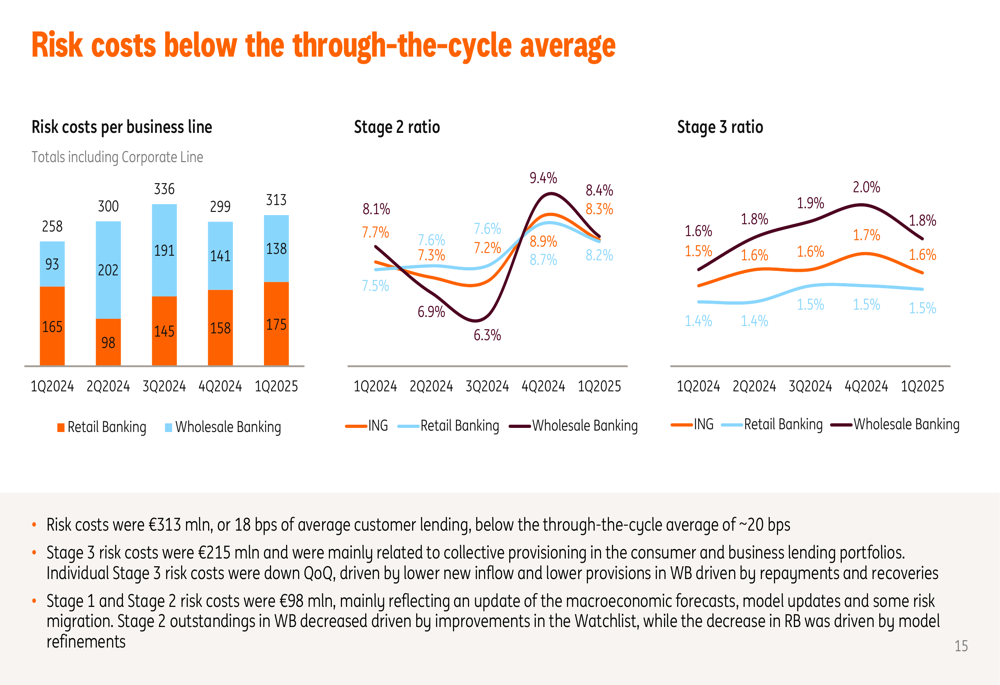

Risk costs for the quarter were €313 million, with the following breakdown by business line:

The risk cost breakdown shows €138 million for Retail Banking and €175 million for Wholesale Banking in Q1 2025, compared to €258 million and €165 million respectively in Q1 2024. This reflects an improvement in the retail segment while wholesale saw a slight increase in risk costs.

Strategic Initiatives & Capital Allocation

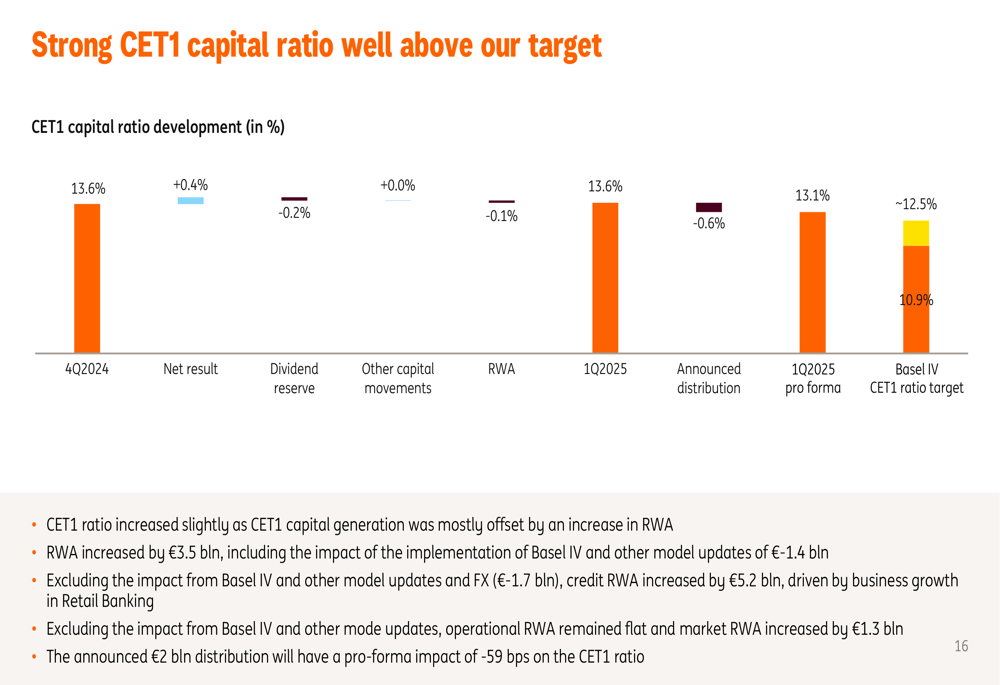

ING maintained a strong capital position with a CET1 ratio of 13.6% at the end of Q1 2025, as illustrated in the following chart:

The bank announced a €2 billion share buyback program, continuing its track record of returning capital to shareholders, with over €28 billion returned since 2021. After accounting for the announced distribution, the pro forma CET1 ratio would be 13.1%, still well above the target of approximately 12.5%. Under Basel IV rules, the pro forma CET1 ratio would be 10.9%.

ING highlighted its strong positioning to capture growth opportunities in Europe, particularly in mortgage markets which are expected to continue growing. The bank noted its strengthened market shares in most countries and pointed to low unemployment rates in its largest mortgage markets as supportive factors.

The bank’s balance sheet remains strong with a loan-to-deposit ratio of 0.92x and 68% of funding coming from deposits, as shown in the following chart:

Forward-Looking Statements

ING reconfirmed its financial targets for both 2025 and 2027. For 2025, the bank expects roughly stable total income, 5-10% growth in fee income, total expenses of €12.5-12.7 billion, a CET1 ratio of 12.8-13.0%, and a return on equity above 12%.

Looking further ahead to 2027, ING targets 4-5% compound annual growth rate in total income from 2024-2027, fee income of €5 billion, a cost/income ratio of 52-54%, a CET1 ratio target of approximately 12.5%, and a return on equity of 14%.

The bank summarized its key performance indicators for Q1 2025 as follows:

In conclusion, ING delivered a strong start to 2025 with record deposit growth, solid fee income performance, and continued capital strength supporting shareholder returns. The bank appears well-positioned to execute on its strategy and support the European economy while maintaining its financial targets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.