Goldman Sachs raises its gold price target to $4,900 by end-2026

ING Group (NYSE:ING) ( AMS (VIE:AMS2):INGA) presented its second quarter 2025 results on July 31, showcasing continued strong commercial growth across key metrics and an improved outlook for the full year. The Dutch banking giant reported resilient net interest income, double-digit fee growth, and significant increases in both lending and deposits.

Commercial Performance Highlights

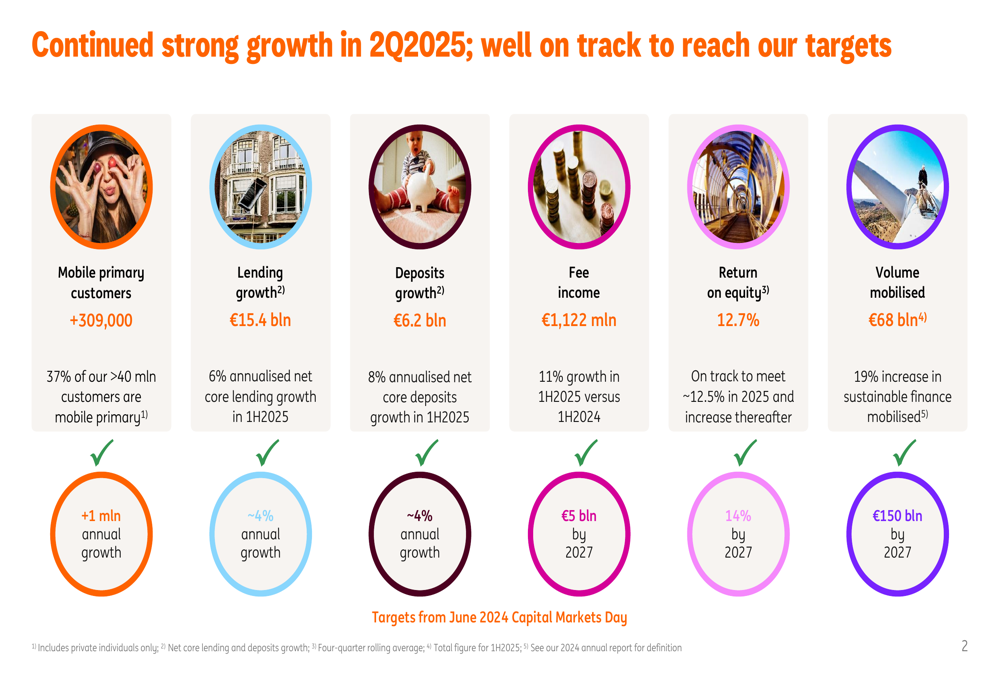

ING reported substantial commercial growth in Q2 2025, with net core lending increasing by €15.4 billion and net core deposits growing by €6.2 billion. The company achieved 6% annualized net core lending growth and 8% annualized net core deposits growth in the first half of 2025, both well above the target of ~4% annual growth.

As shown in the following chart of key performance indicators, ING is on track to meet or exceed all its targets from the June 2024 Capital Markets Day:

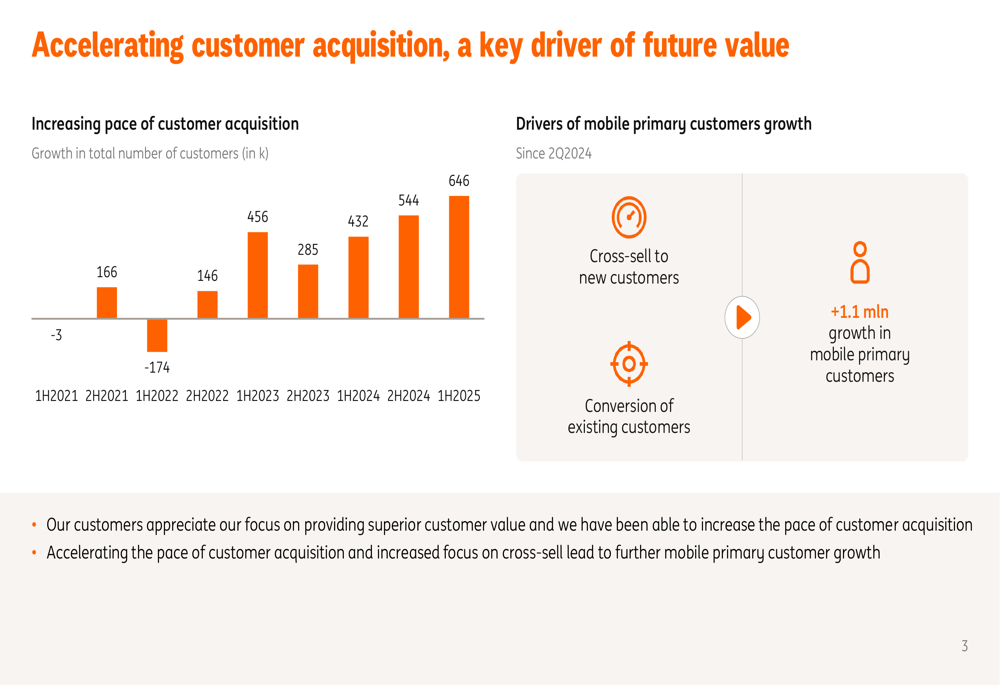

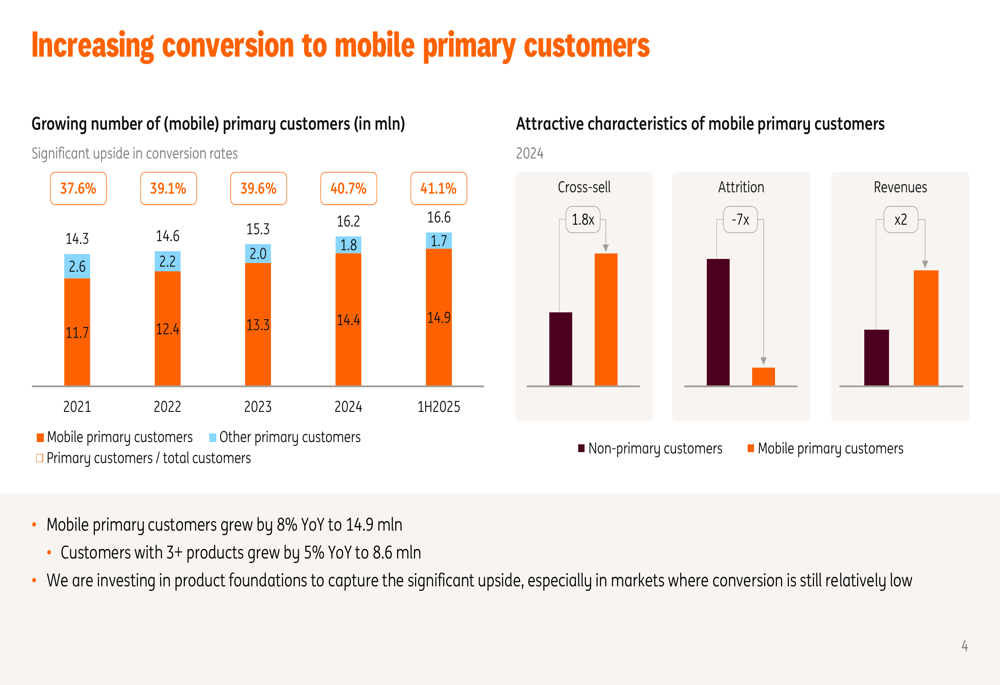

The bank continued its strong customer acquisition momentum, adding 646,000 new customers in the first half of 2025, maintaining the accelerated pace seen in the second half of 2024. Mobile primary customers grew by 8% year-over-year to 14.9 million, now representing 41.1% of ING’s total customer base of over 40 million.

The following chart illustrates ING’s accelerating customer acquisition trend since 2021:

Financial Results

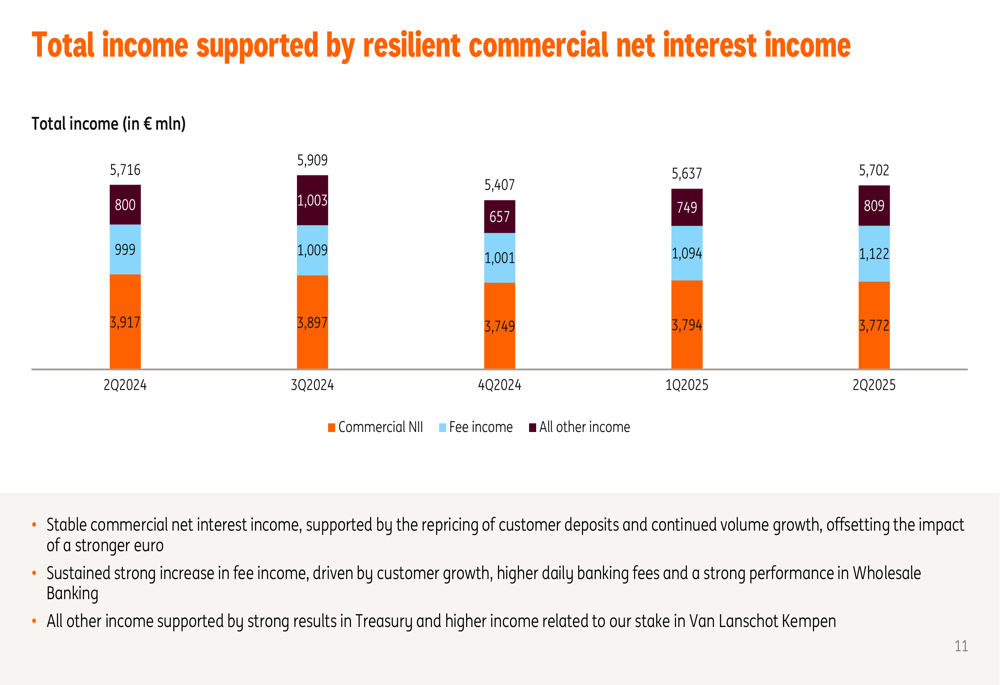

ING’s total income for Q2 2025 reached €5,702 million, showing stability compared to previous quarters. Commercial net interest income (NII) remained resilient at €3,772 million despite ECB deposit rate changes and a stronger euro, which had an estimated negative impact of approximately €150 million.

The breakdown of total income components is illustrated in the following chart:

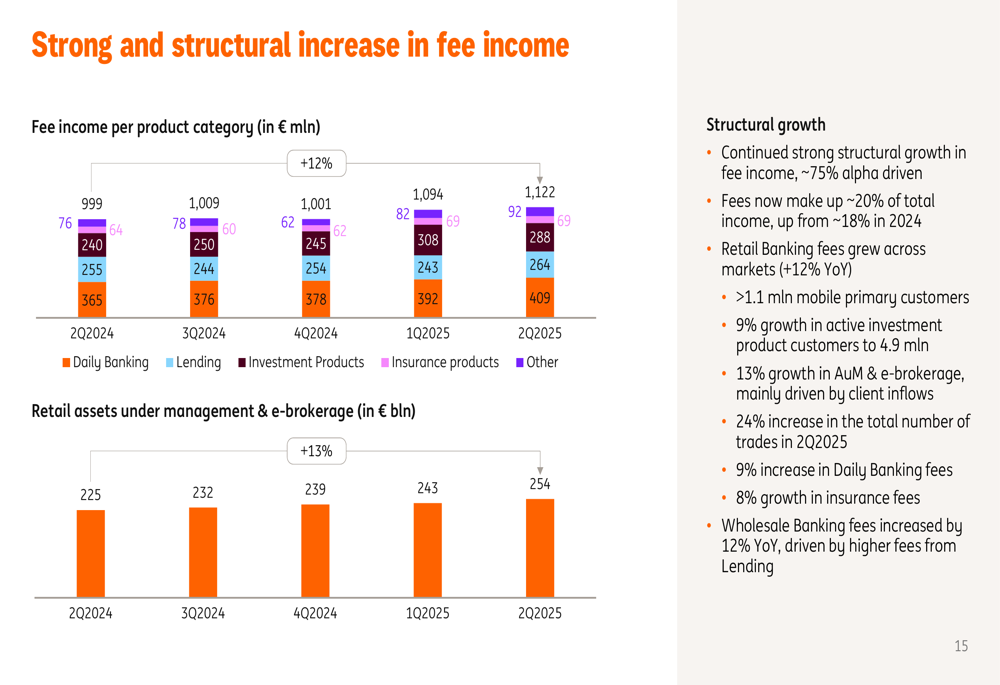

Fee income continued its strong structural growth, reaching €1,122 million in Q2 2025, representing 11% growth in the first half of 2025 compared to the same period in 2024. Fees now make up approximately 20% of total income, up from 18% in 2024, with Retail Banking fees growing 12% year-over-year across markets.

The drivers behind this fee income growth are shown in the following breakdown:

Operating expenses remained well-controlled at €3,146 million for Q2 2025, with the company expecting to achieve the lower end of its €12.5-€12.7 billion expense guidance for the full year. Risk costs were €299 million, or 17 basis points of average customer lending, below the through-the-cycle average of approximately 20 basis points.

Strategic Focus on Mobile Primary Customers

ING continues to focus on converting customers to mobile primary relationships, as these customers generate twice the revenue, have 1.8 times better cross-sell rates, and 7 times lower attrition compared to non-primary customers.

The bank’s success in increasing conversion to mobile primary customers is illustrated in the following chart, showing the conversion rate reaching 41.1% in the first half of 2025:

This strategic focus has also contributed to growing customer balances, with average customer lending and liabilities showing consistent growth that outpaces customer growth. In the last year, lending grew by 6% while customer liabilities increased by 7%.

Capital Position and Shareholder Returns

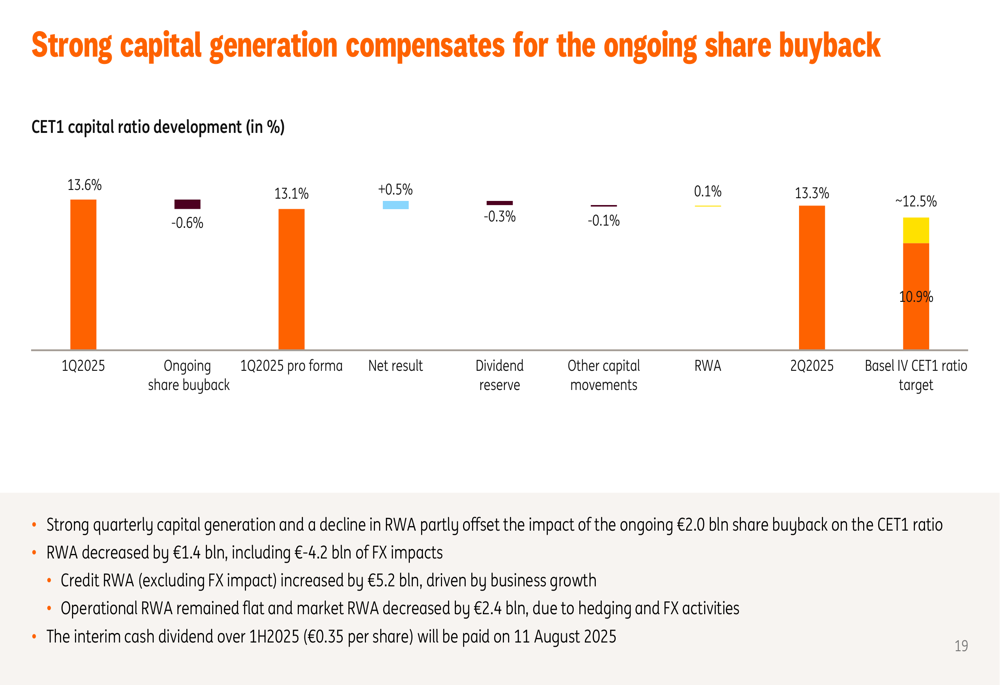

ING maintained a strong capital position with quarterly capital generation partly offsetting the impact of the ongoing €2.0 billion share buyback program. The company announced an interim cash dividend of €0.35 per share for the first half of 2025, to be paid on August 11, 2025.

The following chart illustrates ING’s CET1 capital ratio development:

The bank expects its year-end 2025 CET1 ratio to be between 12.8% and 13.0%, comfortably above its target level of approximately 12.5%.

Improved 2025 Outlook and Progress Toward 2027 Targets

Based on the strong performance in the first half of the year, ING has improved its outlook for 2025. The bank now expects return on equity to reach approximately 12.5%, up from the previous guidance of greater than 12%. Fee income is expected to be at the higher end of the 5-10% growth range, while total expenses are projected to be at the lower end of the €12.5-€12.7 billion range.

The comparison between the improved 2025 outlook and the 2027 targets is shown in the following chart:

Looking ahead, ING expects commercial NII to grow in the second half of 2025 compared to the first half, though a stronger euro is anticipated to have a negative impact of approximately €150 million. The bank expects lending NII to be supported by volume growth, while margin is expected to stabilize at around 125 basis points in 2025 and 125-130 basis points in 2026/27.

Regional Performance

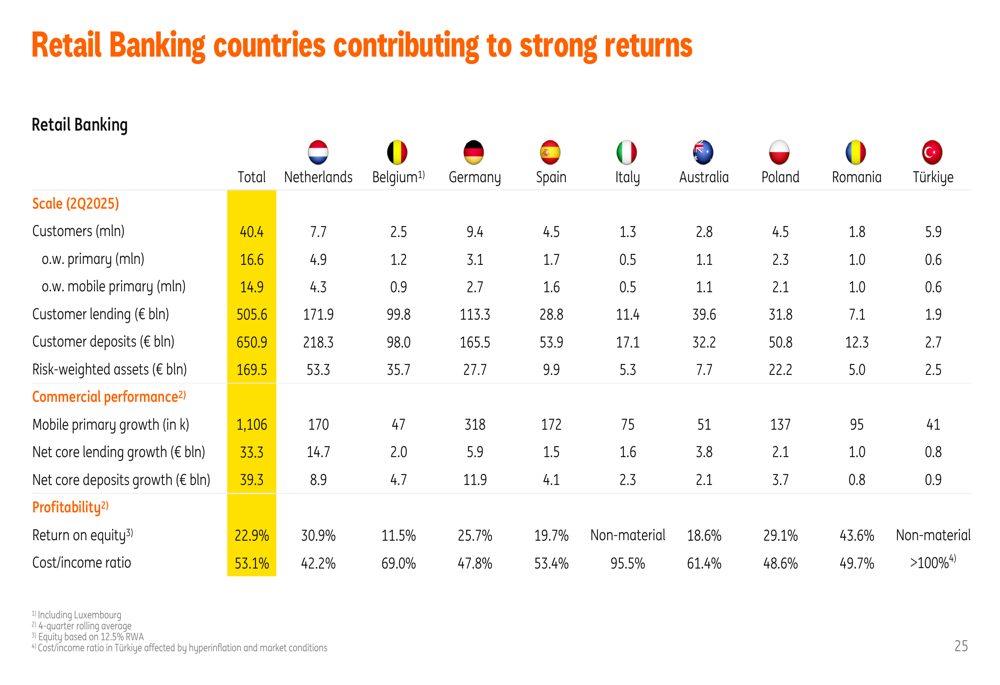

ING’s performance varied across regions, with particularly strong results in the Netherlands, Germany, and Australia. The bank’s diversified geographic presence continues to provide resilience against localized economic challenges.

The regional breakdown of key metrics is illustrated in the following table:

In conclusion, ING’s Q2 2025 results demonstrate continued strong commercial growth and improved profitability, leading to an enhanced outlook for the full year. The bank’s strategic focus on mobile primary customers and fee income growth, combined with disciplined cost management, positions it well to achieve its 2027 targets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.