Street Calls of the Week

Introduction & Market Context

Intact Financial Corporation (TSX:IFC) presented its second-quarter 2025 results on July 30, showcasing solid financial performance across most business segments. Despite reporting earnings that exceeded analyst expectations, the company’s stock dropped 6.47% following the announcement, closing at $285.45, significantly below its 52-week high of $317.35.

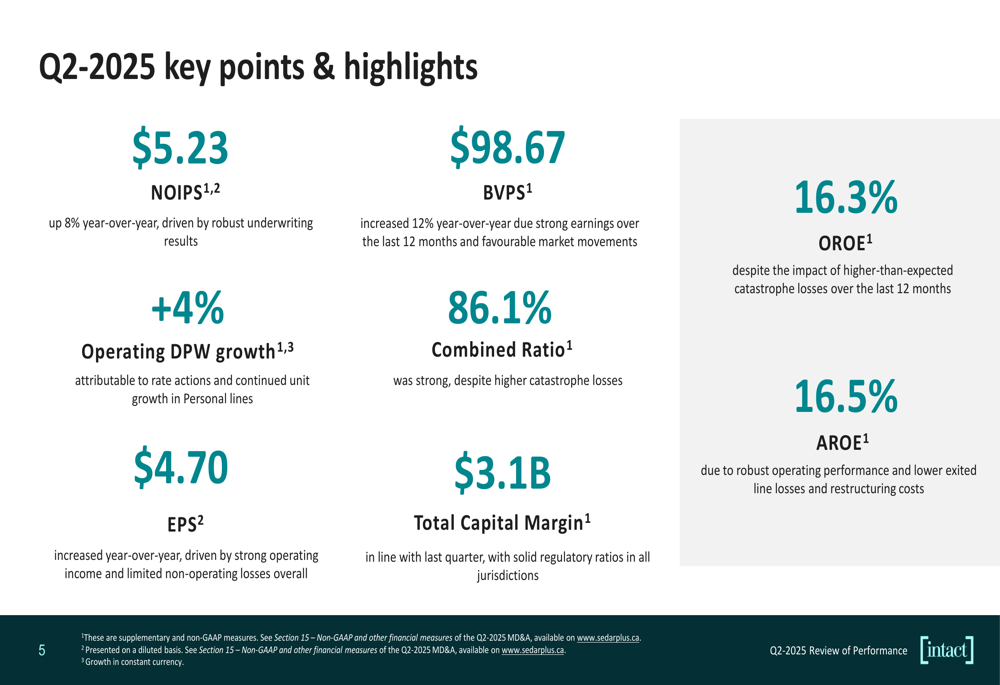

The Canadian property and casualty insurer delivered an 8% year-over-year increase in net operating income per share (NOIPS), reaching $5.23 compared to the forecasted $3.93. This marks a substantial 33.08% positive surprise, continuing the company’s trend of outperforming market expectations.

Quarterly Performance Highlights

Intact reported strong fundamental metrics for the quarter, with operating return on equity (OROE) at 16.3% and a combined ratio of 86.1%, indicating profitable underwriting operations. The company’s book value per share increased 12% year-over-year to $98.67, reflecting sustained growth in shareholder value.

As shown in the following key performance indicators:

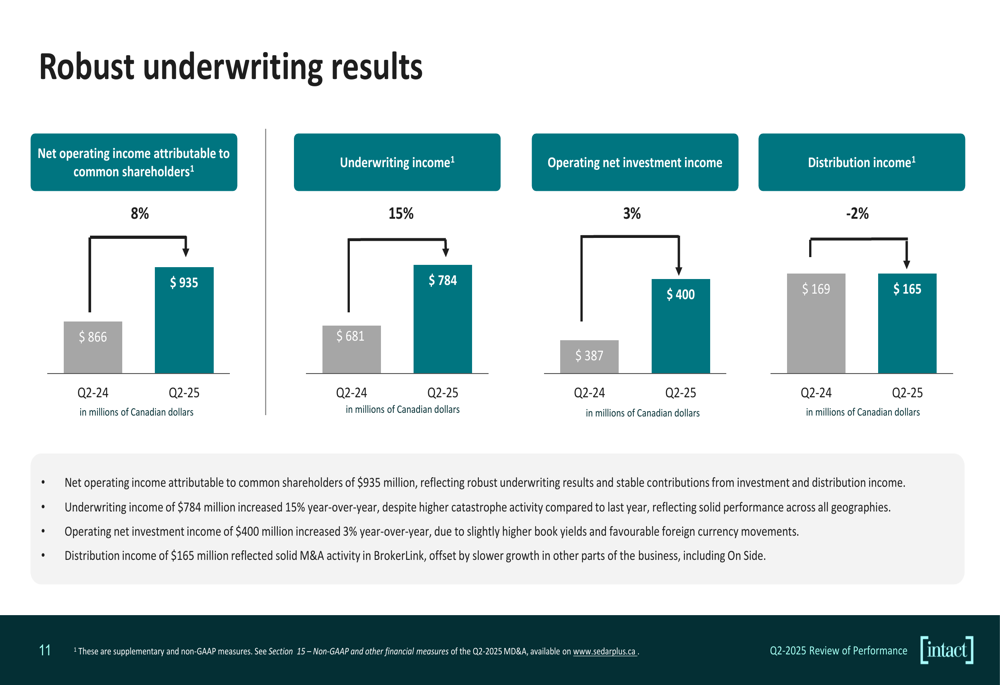

Underwriting income reached $784 million, representing a 15% increase compared to the same period last year. This growth occurred despite higher catastrophe activity, demonstrating the resilience of Intact’s underwriting approach. Operating net investment income grew by 3% to $400 million, while distribution income slightly decreased by 2% to $165 million.

The following chart illustrates these income components:

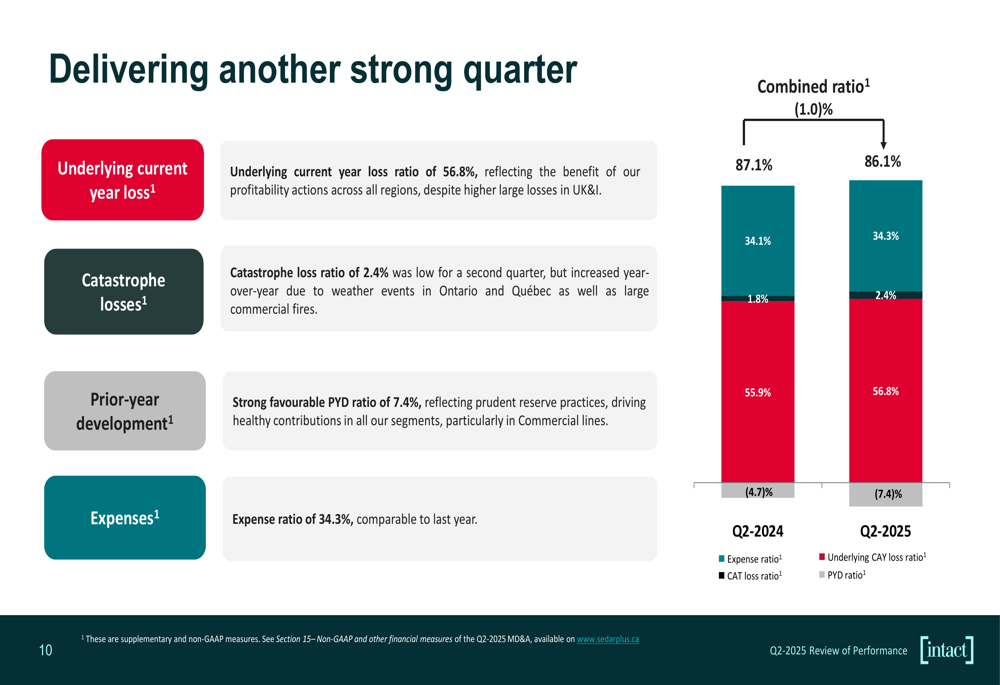

A detailed analysis of the combined ratio shows improvement in prior year development (PYD), which contributed to the strong underwriting performance. The PYD ratio improved from -4.7% in Q2 2024 to -7.4% in Q2 2025, offsetting a slight increase in the underlying current year loss ratio (56.8% vs. 55.9%) and catastrophe loss ratio (2.4% vs. 1.8%).

Segment Analysis

Canadian Operations

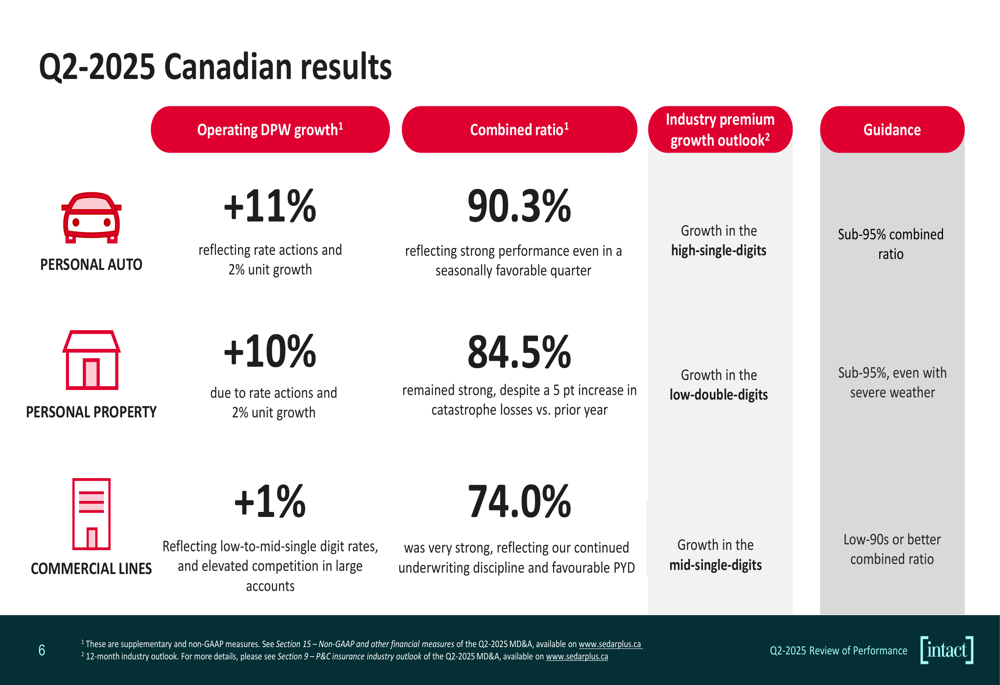

Intact’s Canadian operations delivered particularly strong results, with personal lines showing double-digit premium growth. Personal auto premiums increased by 11% with a combined ratio of 90.3%, while personal property grew by 10% with an 84.5% combined ratio. Commercial lines showed more modest growth at 1% but maintained an impressive 74.0% combined ratio.

The following breakdown shows the Canadian segment performance:

International Operations

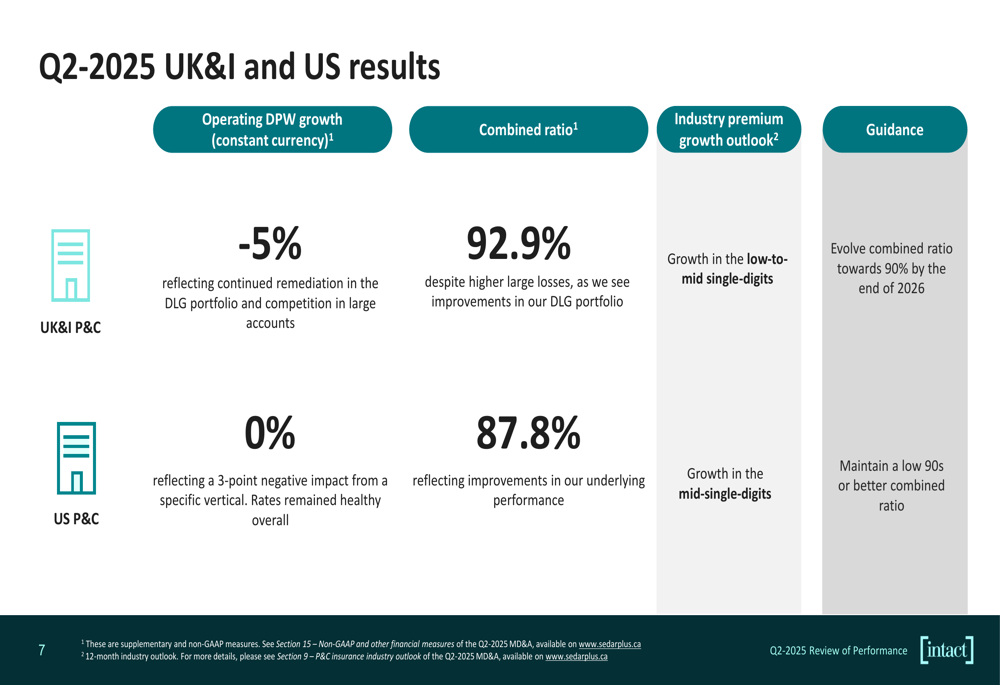

The company’s international segments presented a more challenging picture. The UK and Ireland operations experienced a 5% decline in premium growth (at constant currency) with a combined ratio of 92.9%. Management indicated plans to improve this ratio to 90% by the end of 2026.

US operations reported flat premium growth but maintained a solid combined ratio of 87.8%, outperforming the company’s guidance of low 90s.

Strategic Initiatives & Outlook

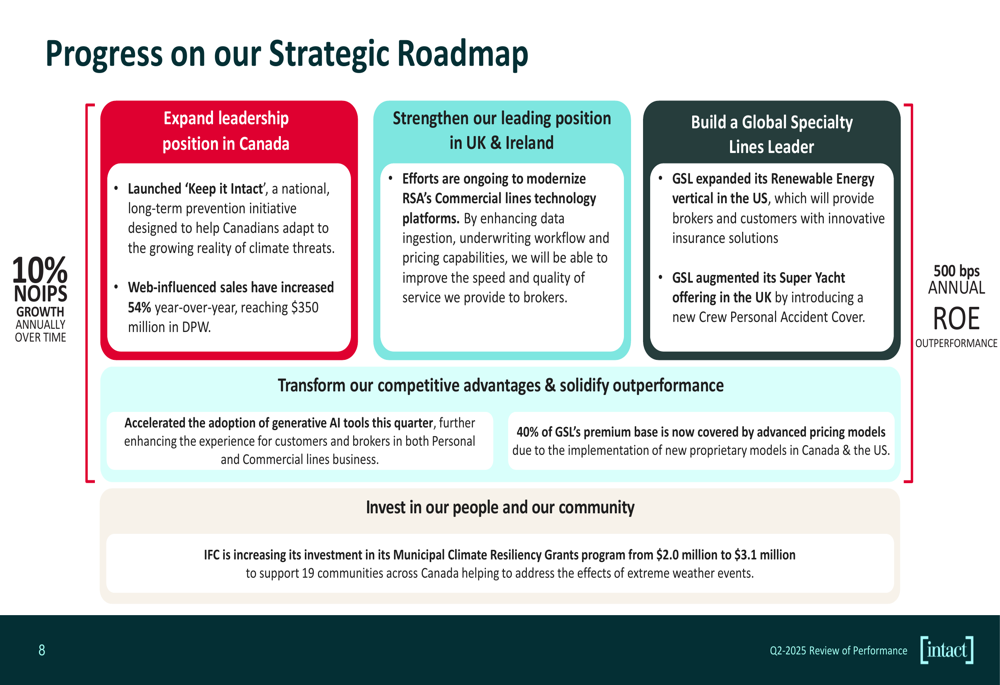

Intact outlined progress on its strategic roadmap, focusing on three key areas: expanding leadership in Canada, strengthening its position in the UK and Ireland, and building a global specialty lines business. Notable initiatives include the launch of "Keep it Intact," a national prevention initiative, and modernization of RSA’s commercial lines technology platforms.

The company highlighted that web-influenced sales increased 54% year-over-year, reaching $350 million in direct premiums written, demonstrating success in digital transformation efforts.

Management remains confident in achieving its long-term targets of 10% annual NOIPS growth and 500 basis points of ROE outperformance over time. However, the market’s negative reaction to the earnings release suggests investors may have concerns about future growth prospects and competitive pressures not directly addressed in the presentation.

Financial Position & Market Reaction

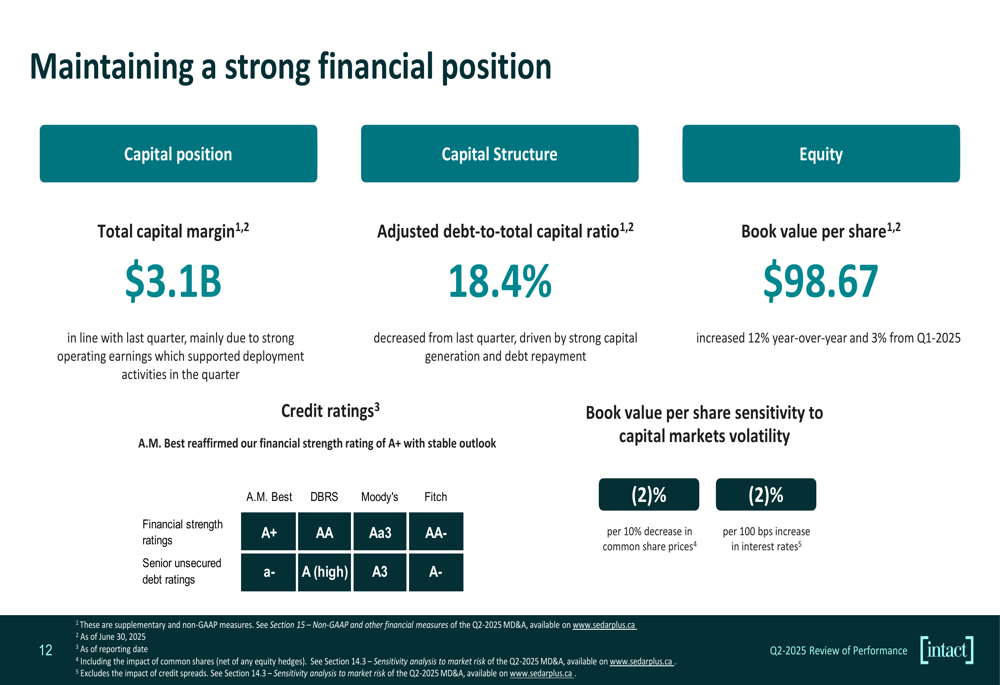

Intact maintains a strong financial position with a total capital margin of $3.1 billion and an adjusted debt-to-total capital ratio of 18.4%. A.M. Best reaffirmed the company’s financial strength rating of A+ with a stable outlook, underscoring its solid financial foundation.

Despite these positive indicators, Intact’s stock fell 6.47% following the earnings announcement. This decline may reflect broader market concerns about the insurance industry, potential challenges in maintaining growth momentum, or the slight decline in distribution income despite overall strong performance.

The company’s book value per share sensitivity analysis indicates a potential 2% decrease for every 10% drop in common share prices or 100 basis point increase in interest rates, suggesting some vulnerability to market volatility.

While Intact’s presentation emphasized its strong operational performance and strategic progress, investors appear to be taking a more cautious view, potentially focusing on challenges in the UK and Ireland segment, flat US growth, and the competitive landscape in key markets. As the company continues to execute its strategic initiatives, bridging this gap between operational performance and market perception will likely be a key focus for management in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.