Trump/Cook, Nissan weakness, more tariffs and gold - what’s moving markets

Introduction & Market Context

Integra LifeSciences (NASDAQ:IART) released its second quarter 2025 earnings presentation on July 31, showing continued pressure on both top and bottom lines while projecting a significant rebound in the second half of the year. The medical technology company reported a slight revenue decline amid ongoing operational challenges and international weakness.

The presentation comes as Integra’s stock trades near 52-week lows at $12.37, down 3.81% on the day of the announcement. The company has faced significant headwinds in recent quarters, with its Q1 2025 results missing analyst expectations and triggering a 24.63% stock price decline at that time.

Quarterly Performance Highlights

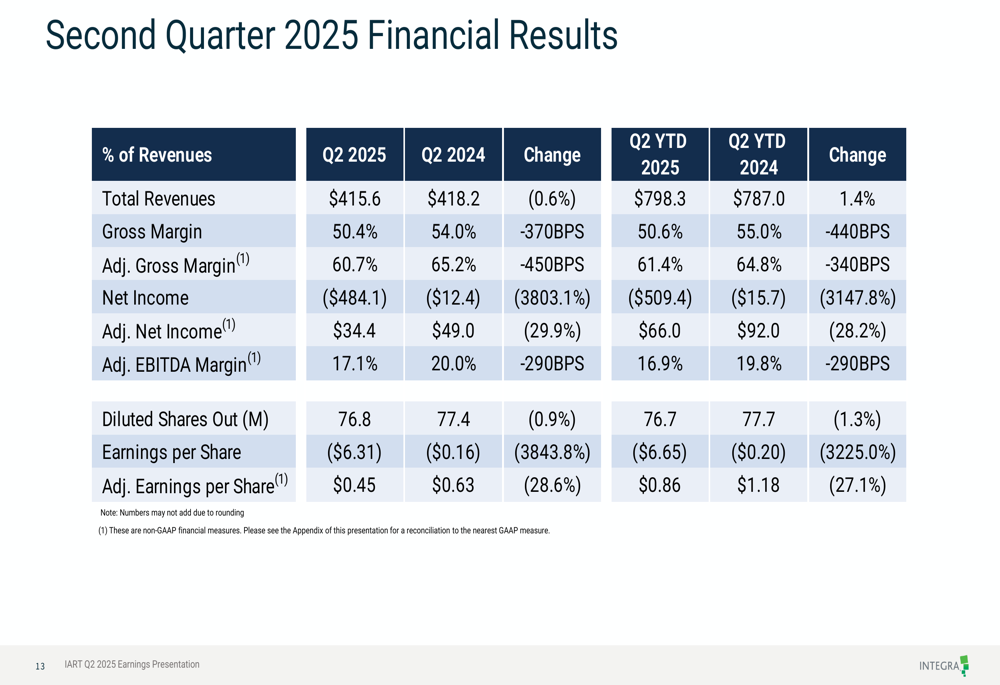

Integra reported Q2 2025 revenue of $415.6 million, representing a 0.6% decrease from the $418.2 million reported in Q2 2024. On an organic basis, which excludes currency effects and acquisitions, revenue declined 1.4% year-over-year.

Profitability metrics showed significant pressure, with adjusted earnings per share falling 28.6% to $0.45 compared to $0.63 in the prior year period. Adjusted EBITDA margin contracted 290 basis points to 17.1%, while adjusted gross margin declined 450 basis points to 60.7%.

As shown in the following comprehensive financial results chart:

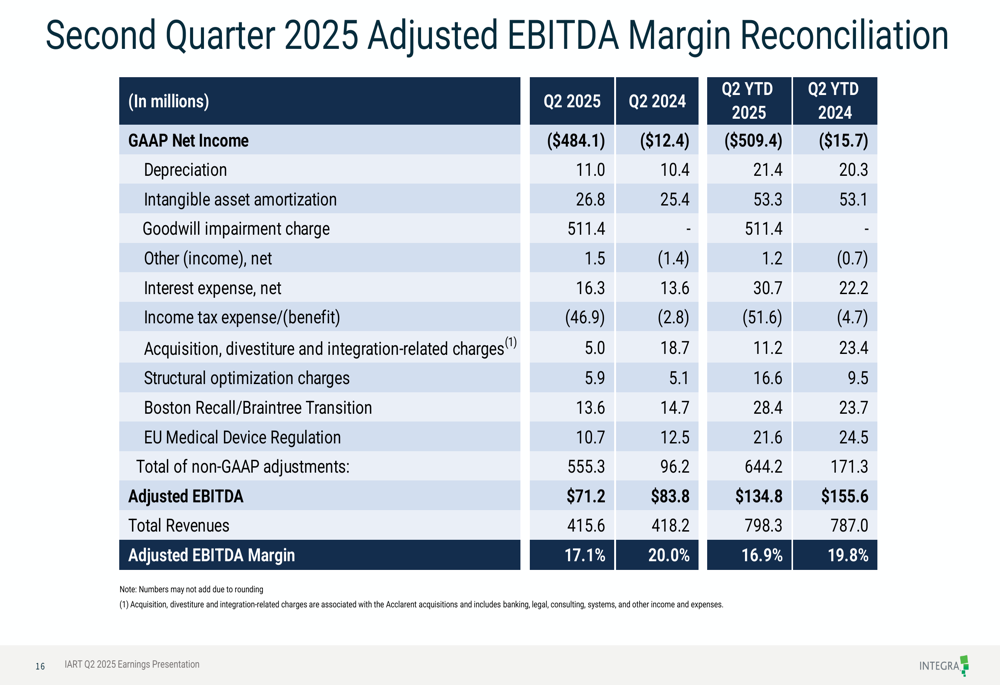

The most notable item impacting GAAP results was a substantial $511.4 million goodwill impairment charge, which drove a GAAP net loss of $484.1 million or $6.31 per share. This compares to a much smaller loss of $12.4 million or $0.16 per share in Q2 2024.

Segment Analysis

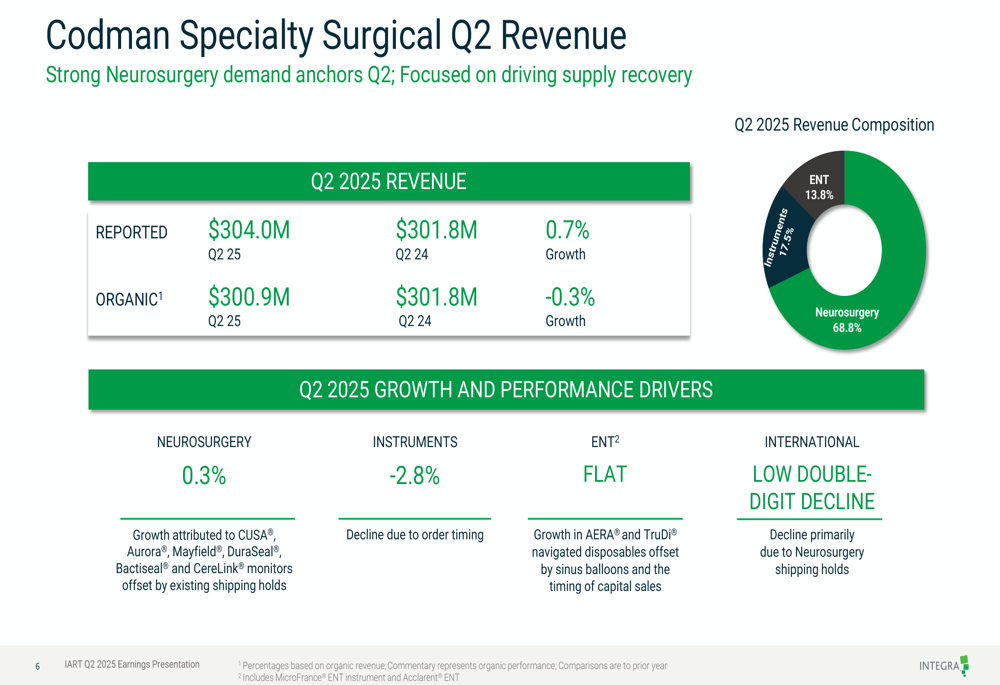

Integra operates through two main business segments: Codman Specialty Surgical and Tissue Technologies. The Codman segment showed relative stability with a 0.7% reported revenue increase to $304.0 million, though organic revenue declined slightly by 0.3%.

The segment breakdown is illustrated in the following chart:

Within Codman, Neurosurgery (68.8% of segment revenue) grew 0.3%, while Instruments (17.5%) declined 2.8%, and ENT (13.8%) remained flat. International revenues experienced a low double-digit decline, offsetting domestic performance.

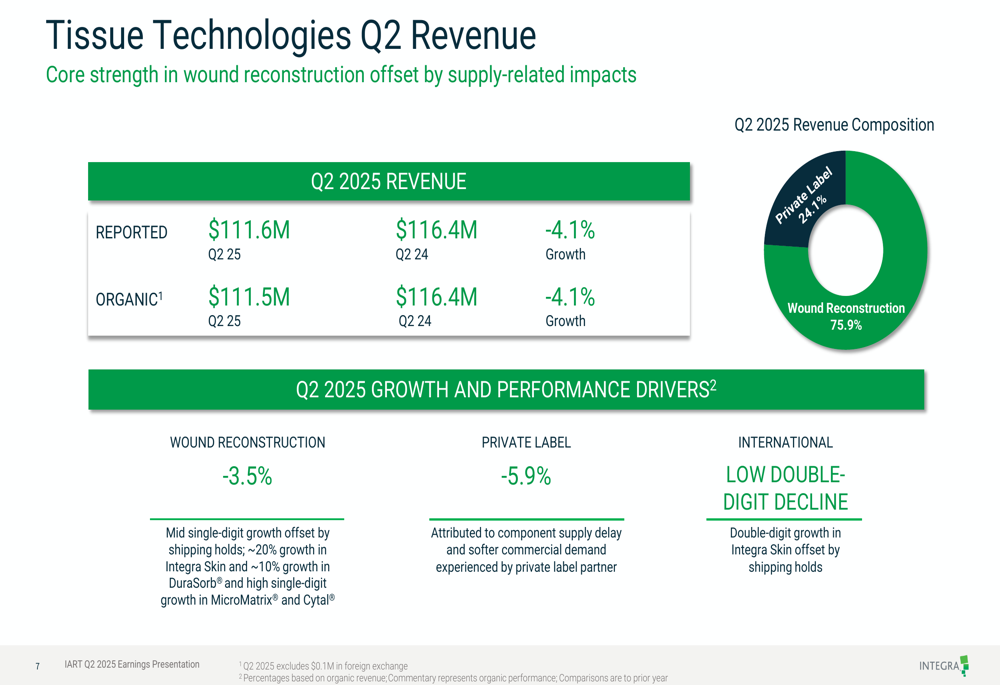

The Tissue Technologies segment faced more significant challenges, with revenue declining 4.1% to $111.6 million. This segment’s performance is detailed in the following chart:

Despite the overall decline in Tissue Technologies, there were some bright spots, including approximately 20% growth in Integra Skin and 10% growth in DuraSorb®, along with high single-digit growth in MicroMatrix® and Cytal®. However, these gains were offset by weakness in other areas and international markets, which saw low double-digit declines.

Balance Sheet and Cash Flow

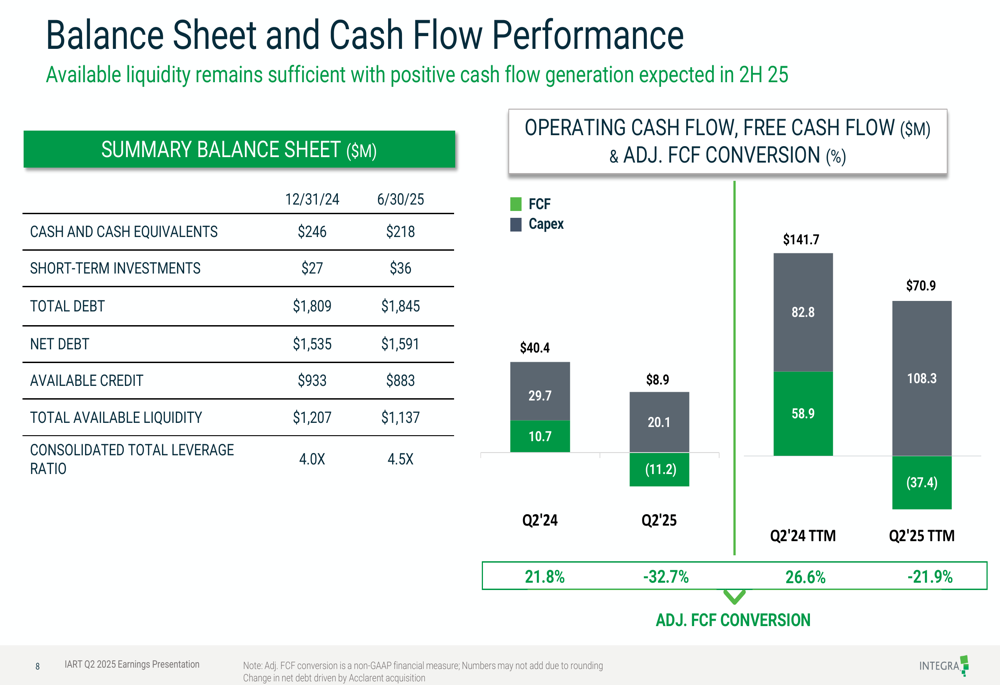

Integra’s financial position showed some concerning trends, with net debt increasing to $1,591 million as of June 30, 2025, compared to $1,535 million at the end of 2024. The consolidated total leverage ratio increased to 4.5X from 4.0X.

Cash flow metrics deteriorated significantly, with operating cash flow of just $8.9 million in Q2 2025 compared to $40.4 million in Q2 2024. Free cash flow turned negative at -$11.2 million, resulting in a negative adjusted free cash flow conversion of -32.7%.

The following chart illustrates these balance sheet and cash flow trends:

The reconciliation of adjusted EBITDA provides further insight into the company’s operational performance, highlighting the significant impact of the goodwill impairment charge:

Outlook and Guidance

Despite the challenging first half of 2025, Integra provided an optimistic outlook for the remainder of the year. For Q3 2025, the company expects reported revenue of $410-$420 million, representing growth of 7.7% to 10.3% (7.3% to 9.9% organic), with adjusted EPS of $0.40-$0.45.

For the full year 2025, Integra maintained guidance for revenue of $1.655-$1.680 billion, representing growth of 2.8% to 4.3% (0.6% to 2.1% organic), with adjusted EPS of $2.19-$2.29.

The company’s forward guidance is illustrated in the following chart:

Key assumptions underlying this guidance include seasonal volume increases and ramping Integra Skin sales in the second half of 2025. The company also noted that gross margins are expected to be down approximately 280 basis points versus 2024, with about 80 basis points of this decline attributed to tariff impacts.

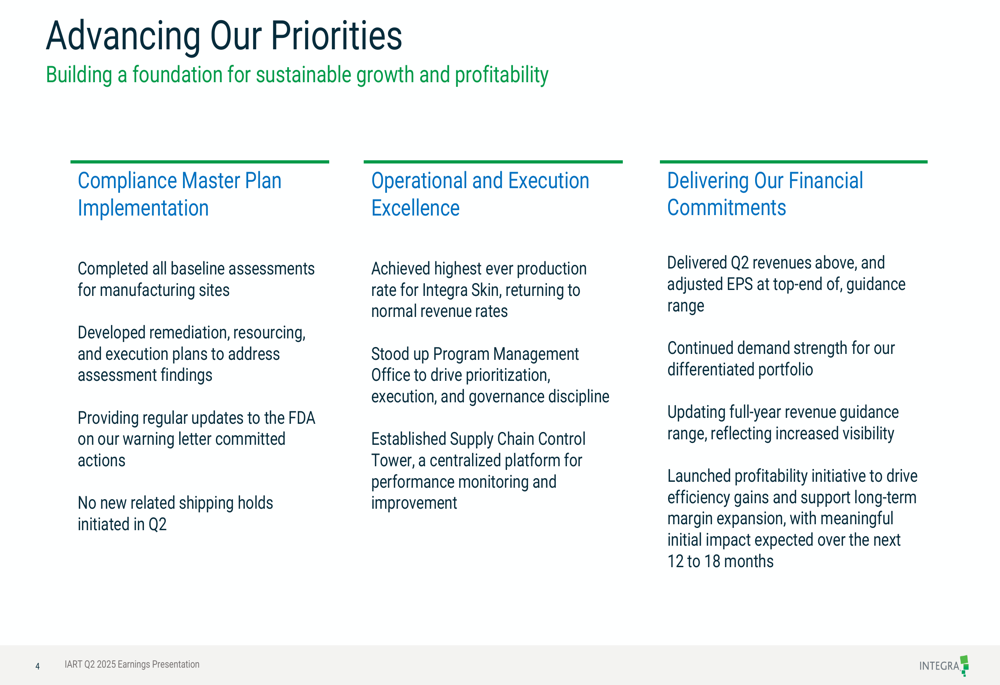

Strategic Initiatives

Integra highlighted several strategic priorities aimed at addressing its operational challenges. The company reported progress on its Compliance Master Plan Implementation, noting that all baseline assessments for manufacturing sites are complete and remediation plans have been developed. Regular updates are being provided to the FDA, and no new related shipping holds were initiated in Q2.

The company’s key strategic initiatives are outlined in the following chart:

Operational improvements include achieving the highest ever production rate for Integra Skin, establishing a Program Management Office, and implementing a Supply Chain Control Tower. The company has also launched a profitability initiative to address margin pressures.

These strategic initiatives will be crucial for Integra to achieve its projected second-half rebound and meet its full-year guidance. Given the significant challenges faced in the first half of 2025 and the ongoing stock price pressure, investors will likely be closely monitoring the company’s execution in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.