Helen of Troy beats Q2 estimates, shares rise on better-than-expected results

Introduction & Market Context

Integrated Wind Solutions AS (IWS) presented its second quarter 2025 results on August 27, 2025, showcasing record financial performance driven by its expanding fleet of Commissioning Service Operation Vessels (CSOVs). The company, which positions itself as a fully integrated offshore wind solutions provider, reported substantial year-over-year growth as the offshore wind sector continues its expansion.

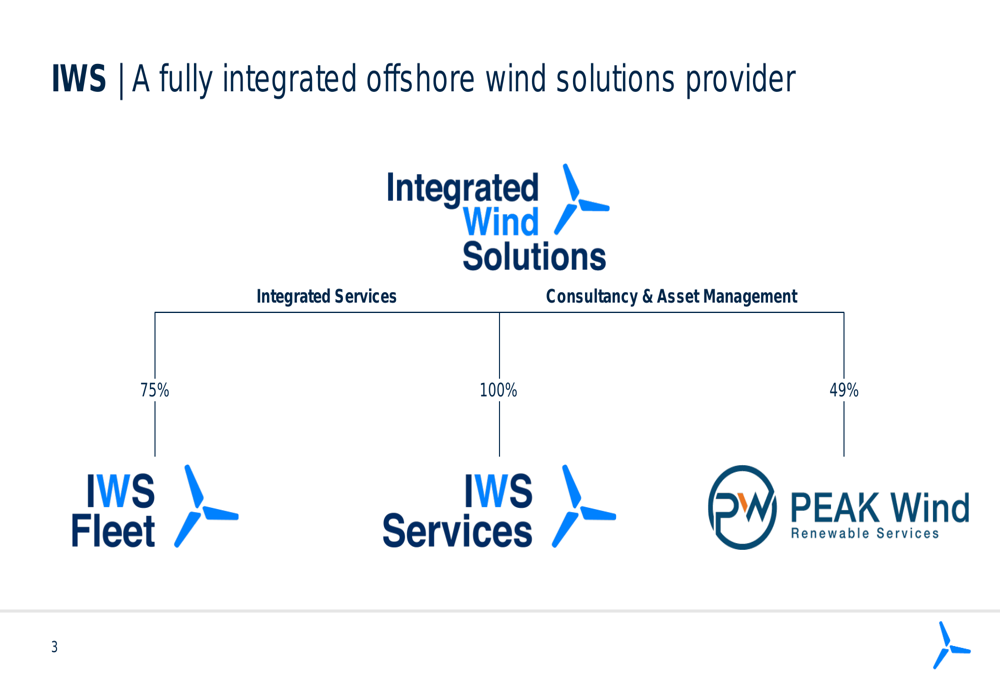

IWS operates through three main segments: IWS Fleet (75% ownership), which owns and operates CSOVs; IWS Services (100% ownership), which provides engineering and manpower services; and PEAK Wind (49% ownership), a renewable energy consultancy and asset management service company.

As shown in the following organizational structure, the company has created an integrated approach to serving the offshore wind market:

Quarterly Performance Highlights

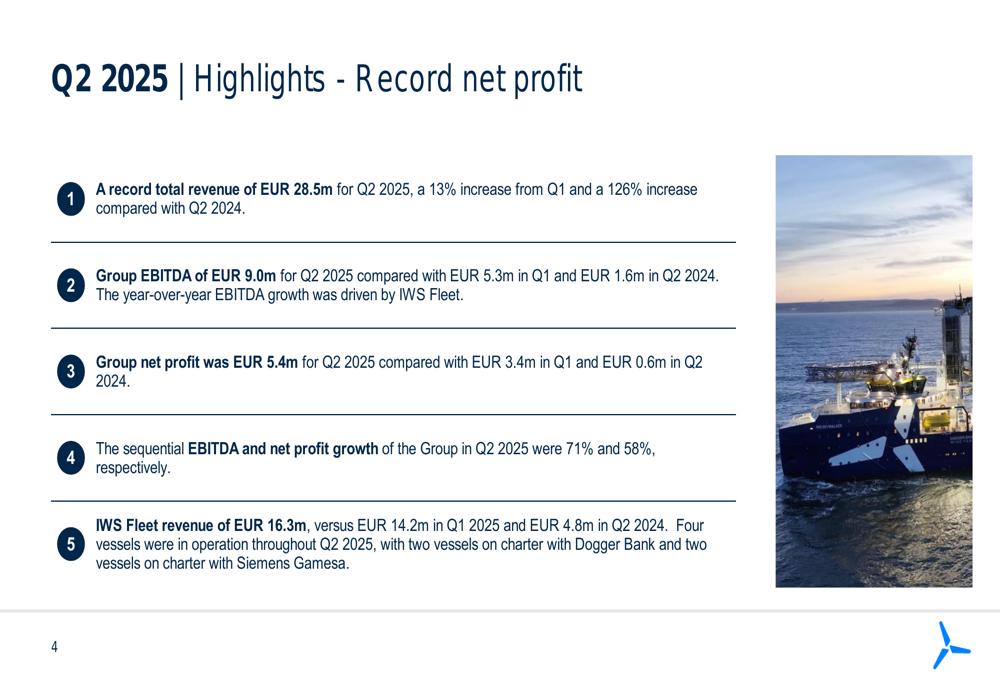

Integrated Wind Solutions reported record total revenue of EUR 28.5 million for Q2 2025, representing a 13% increase from Q1 and a remarkable 126% increase compared to Q2 2024. This growth translated into substantial profit improvements, with Group EBITDA reaching EUR 9.0 million, up from EUR 5.3 million in Q1 and EUR 1.6 million in Q2 2024.

The company’s net profit more than doubled sequentially to EUR 5.4 million in Q2 2025, compared to EUR 3.4 million in Q1 and just EUR 0.6 million in Q2 2024. This represents sequential EBITDA and net profit growth of 71% and 58%, respectively.

The following slide highlights these key financial metrics alongside an image of one of the company’s vessels:

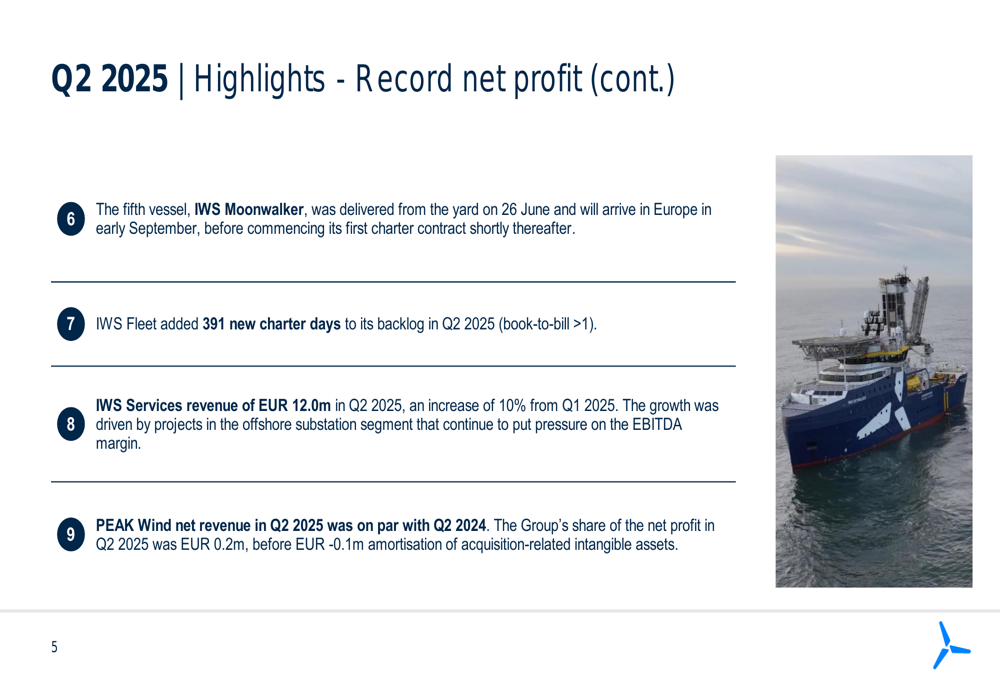

Additional financial highlights include the delivery of the fifth vessel, IWS Moonwalker, on June 26, which will arrive in Europe in early September before beginning its first charter contract. IWS Fleet also added 391 new charter days to its backlog during the quarter, achieving a book-to-bill ratio greater than 1, indicating strong future demand.

Fleet Expansion and Backlog

IWS Fleet, the primary growth driver for the company, generated revenue of EUR 16.3 million in Q2 2025, compared to EUR 14.2 million in Q1 and EUR 4.8 million in Q2 2024. Four vessels were operational throughout Q2, with two vessels on charter with Dogger Bank and two with Siemens Gamesa.

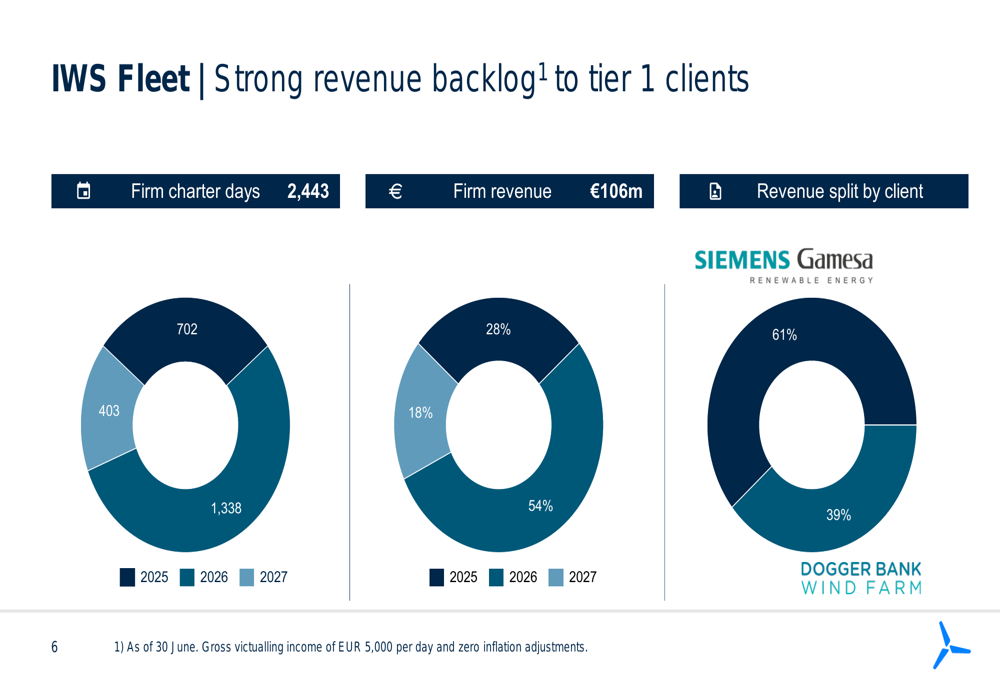

The company’s revenue backlog provides strong visibility into future earnings. As of June 30, 2025, IWS had 2,443 firm charter days booked, translating to EUR 106 million in firm revenue. This backlog is distributed across 2025 (18%), 2026 (28%), and 2027 (54%), with 61% of revenue coming from Siemens Gamesa and 39% from Dogger Bank Wind Farm.

The following chart illustrates this revenue backlog distribution:

The company’s fleet of six Skywalker-class vessels is in various stages of operation and delivery, with four currently operating, one in transit to Europe, and one in final commissioning. This visual overview shows the current status of each vessel:

Segment Performance

While IWS Fleet drove the majority of the company’s profitability, IWS Services also contributed to growth with revenue of EUR 12.0 million in Q2 2025, a 10% increase from Q1. However, projects in the offshore substation segment put pressure on EBITDA margins in this division.

The company highlighted its integrated service model, where IWS Fleet and IWS Services work together to provide comprehensive solutions to clients. The following image shows ProCon technicians working for a turbine OEM on board the IWS Skywalker, representing the first integrated services delivered jointly by both divisions:

PEAK Wind’s performance remained stable, with Q2 2025 net revenue on par with Q2 2024. The Group’s share of net profit from this segment was EUR 0.2 million before EUR -0.1 million amortization of acquisition-related intangible assets.

Forward-Looking Statements

Looking ahead, IWS maintains an optimistic outlook based on expected double-digit industry growth in the offshore wind sector. The company expects continued ramp-up of activity as two additional vessels enter operation in the second half of 2025.

Management anticipates strong net profit growth in 2025, primarily driven by IWS Fleet. IWS Services is expected to maintain strong performance in its core transition piece business, while PEAK Wind is positioned to expand its geographical scope and offerings.

As illustrated in the company’s outlook slide:

The company’s stock closed at EUR 45.01 on August 26, 2025, down 1.08% ahead of the earnings presentation. The shares have traded between EUR 36.99 and EUR 56.00 over the past 52 weeks.

With a growing fleet, expanding backlog, and integrated service model, Integrated Wind Solutions appears well-positioned to capitalize on the continued growth in offshore wind energy development, though investors will be watching to see if the company can maintain its margin expansion as it scales operations.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.