Oil prices rebound sharply on smaller-than-feared OPEC+ output hike

Introduction & Market Context

International Money Express Inc. (NASDAQ:IMXI) presented its first quarter 2025 earnings on May 7, 2025, revealing significant year-over-year declines in revenue and profitability despite growth in digital transactions and principal sent. The company’s stock continued its downward trend, trading at $10.70 in premarket, down 13.64% following the earnings release, approaching its 52-week low.

The Q1 results follow a disappointing Q4 2024 performance when the company missed both earnings and revenue expectations, triggering a major stock selloff. Today’s presentation highlighted what the company described as a "unique US-Latam market dynamic" affecting its core business.

Quarterly Performance Highlights

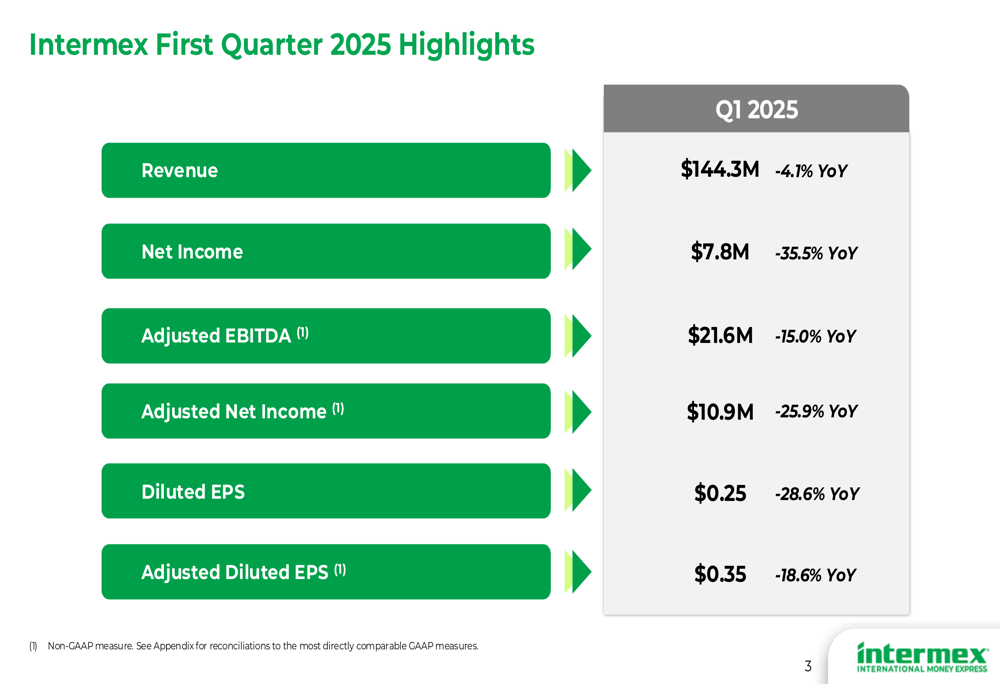

Intermex reported broad-based declines across key financial metrics for Q1 2025. Revenue fell 4.1% year-over-year to $144.3 million, while net income dropped 35.5% to $7.8 million. Adjusted EBITDA decreased 15.0% to $21.6 million, and diluted EPS fell 28.6% to $0.25 per share.

As shown in the following financial highlights:

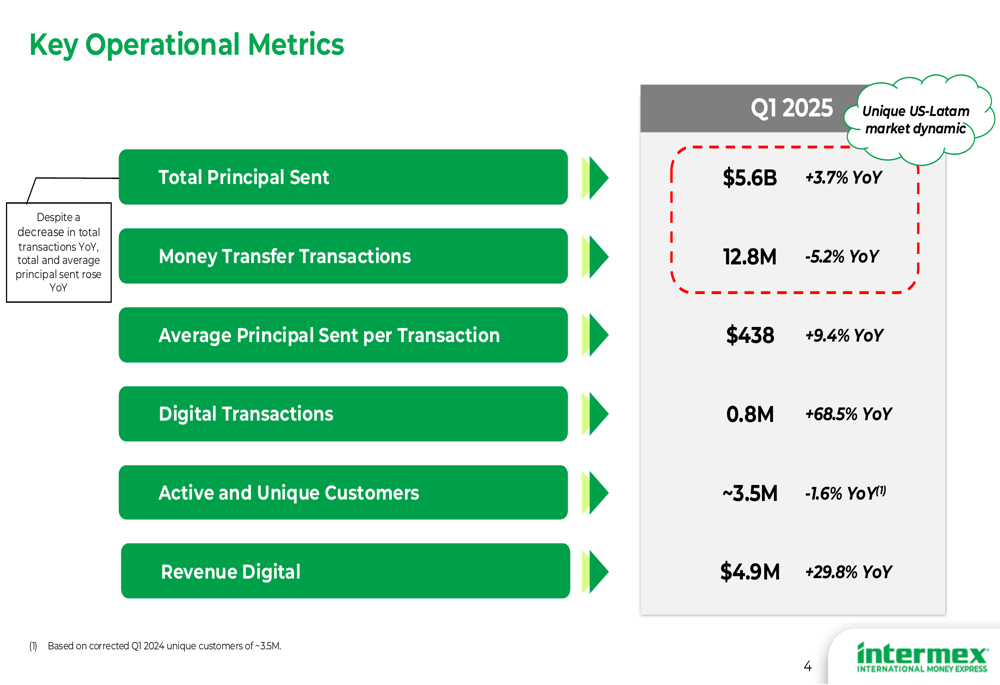

The company’s operational metrics presented a mixed picture. While total money transfer transactions decreased 5.2% year-over-year to 12.8 million, the total principal sent increased 3.7% to $5.6 billion. This was driven by a 9.4% increase in average principal sent per transaction, which reached $438.

The following operational metrics chart illustrates these trends:

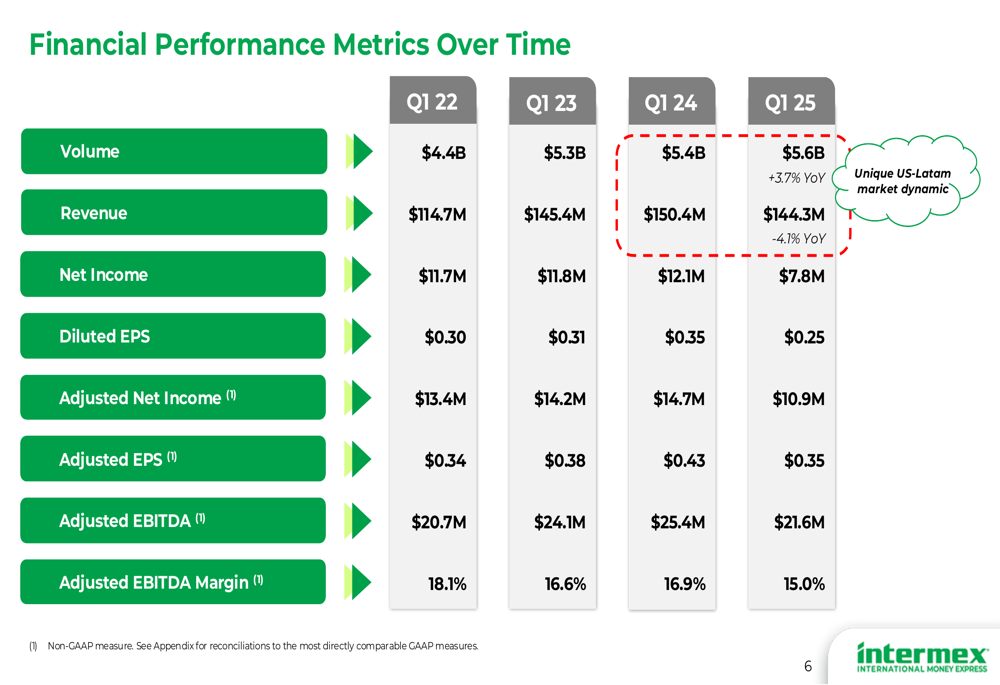

Looking at historical performance, Q1 2025 represents a notable reversal from the growth trajectory seen in previous years. The company’s volume has continued to grow, but revenue and profitability metrics have declined significantly compared to Q1 2024.

Digital Growth as a Bright Spot

Despite overall challenges, Intermex’s digital business showed robust growth, with digital transactions increasing 68.5% year-over-year to 0.8 million. Digital revenue grew 29.8% to $4.9 million, representing a small but growing portion of the company’s overall business.

This digital growth aligns with the company’s previous strategic focus on expanding its digital capabilities, as mentioned in earlier earnings calls where CEO Bob Lizzie emphasized an "omni-channel strategy" and the CFO expressed confidence in scaling the digital segment.

Balance Sheet Strength & Cash Generation

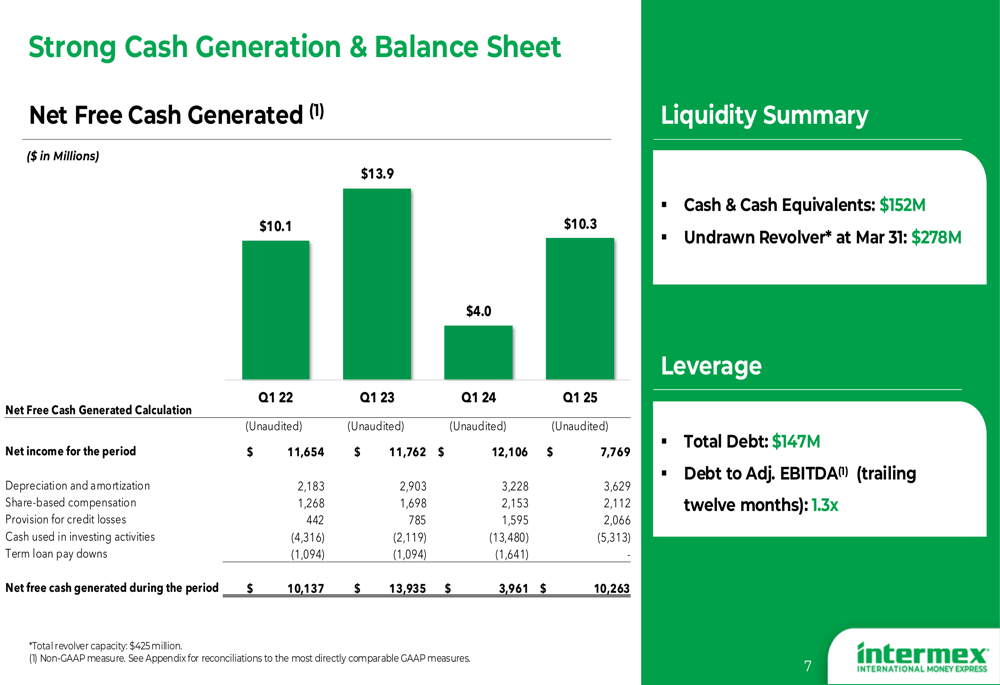

Intermex maintained a strong balance sheet with $152 million in cash and cash equivalents as of March 31, 2025. The company’s total debt stood at $147 million, resulting in a debt-to-adjusted EBITDA ratio of 1.3x, indicating conservative leverage.

Net free cash generation improved significantly to $10.3 million in Q1 2025, compared to $4.0 million in Q1 2024, demonstrating the company’s ability to generate cash despite profitability challenges.

The following chart illustrates the company’s cash generation over recent quarters:

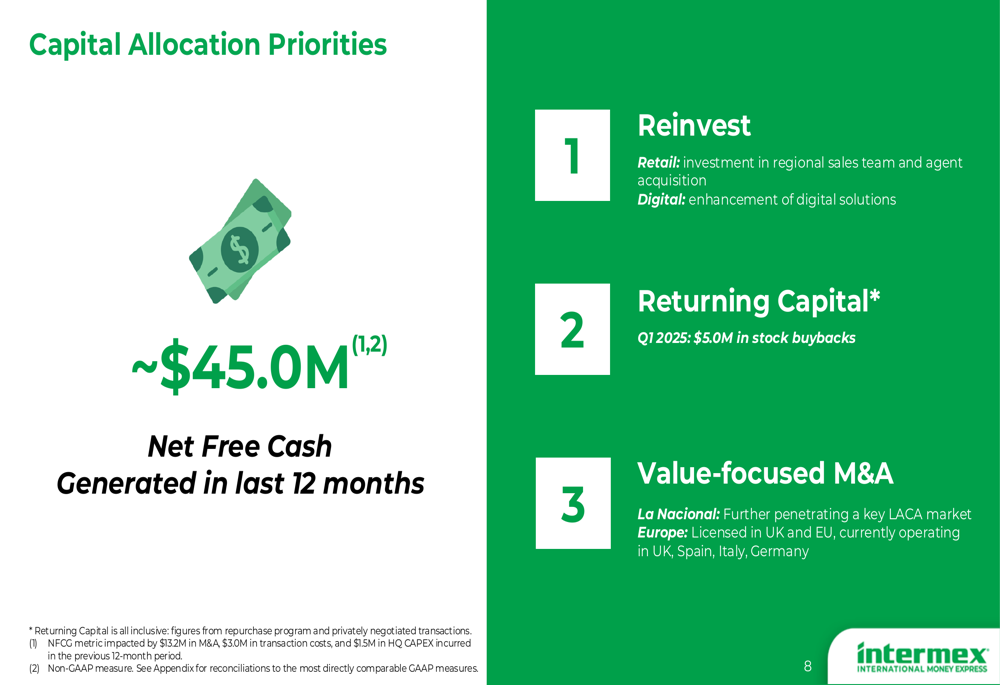

Capital Allocation Strategy

Intermex outlined three main capital allocation priorities: reinvesting in the business, returning capital to shareholders, and pursuing value-focused acquisitions. During Q1 2025, the company repurchased $5.0 million in stock.

The company highlighted its recent acquisition of La Nacional to further penetrate key Latin American and Caribbean markets, as well as its European expansion with operations in the UK, Spain, Italy, and Germany.

As shown in the capital allocation priorities slide:

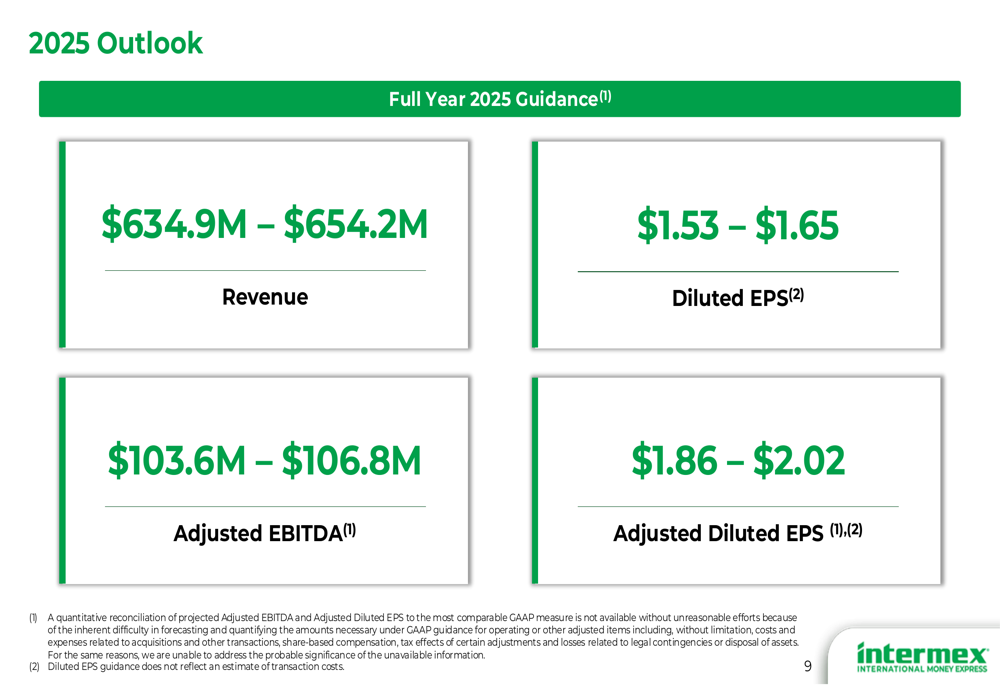

2025 Outlook & Forward Guidance

Looking ahead, Intermex provided full-year 2025 guidance with revenue expected between $634.9 million and $654.2 million. Adjusted EBITDA is projected to range from $103.6 million to $106.8 million, while diluted EPS is forecast between $1.53 and $1.65.

The guidance suggests management anticipates continued challenges throughout 2025, with the midpoint of the revenue range ($644.6 million) representing a slight decrease from the $658.6 million reported for full-year 2024 in their previous earnings release.

Analyst Perspectives

While specific analyst questions weren’t detailed in the presentation, the company’s performance must be viewed in the context of its recent struggles. The significant stock price decline following both Q4 2024 and now Q1 2025 results indicates investor concerns about the company’s growth trajectory and profitability.

According to the previous earnings call information, analysts had inquired about the company’s acquisition strategy and digital marketing ROI. The continued growth in digital transactions suggests the company is making progress on its digital initiatives, though not enough to offset declines in its traditional business.

The remittance market slowdown in Mexico, increased digital marketing expenditures, and macroeconomic conditions including immigration policies remain key challenges for Intermex as it navigates through 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.