Capstone Holding Corp. lowers convertible note conversion price to $1.00

Invivyd Inc (NASDAQ:IVVD) reported modest revenue growth in its Q1 2025 financial results presentation on May 15, while highlighting commercial progress for its COVID-19 antibody PEMGARDA and outlining strategies to overcome regulatory challenges. The company faces a narrowing cash runway as it pursues profitability.

Quarterly Performance Highlights

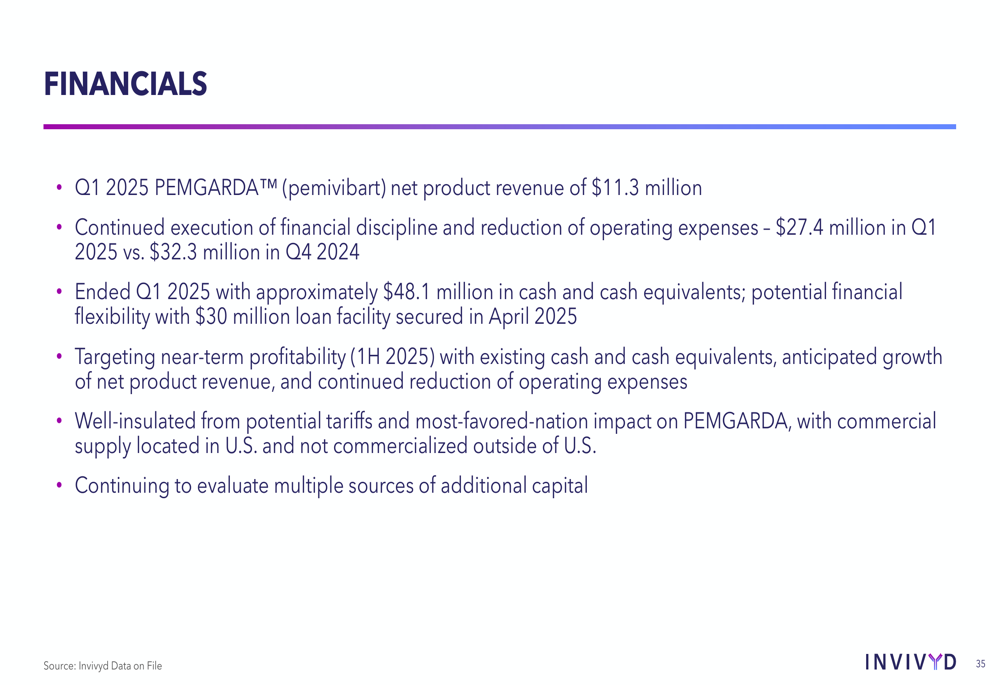

Invivyd reported Q1 2025 PEMGARDA (pemivibart) net product revenue of $11.3 million, showing growth from the $9.3 million reported in Q3 2024. The company ended the quarter with $48.1 million in cash and cash equivalents, a significant decrease from the $107 million reported at the end of Q3 2024, reflecting continued cash burn despite efforts to reduce operating expenses.

Operating expenses decreased to $27.4 million in Q1 2025 from $32.3 million in Q4 2024, demonstrating the company’s focus on financial discipline. To strengthen its financial position, Invivyd secured a $30 million loan facility in April 2025, providing additional flexibility.

As shown in the following financial summary, the company is targeting near-term profitability in the first half of 2025 through revenue growth and continued expense reduction:

Commercial Progress

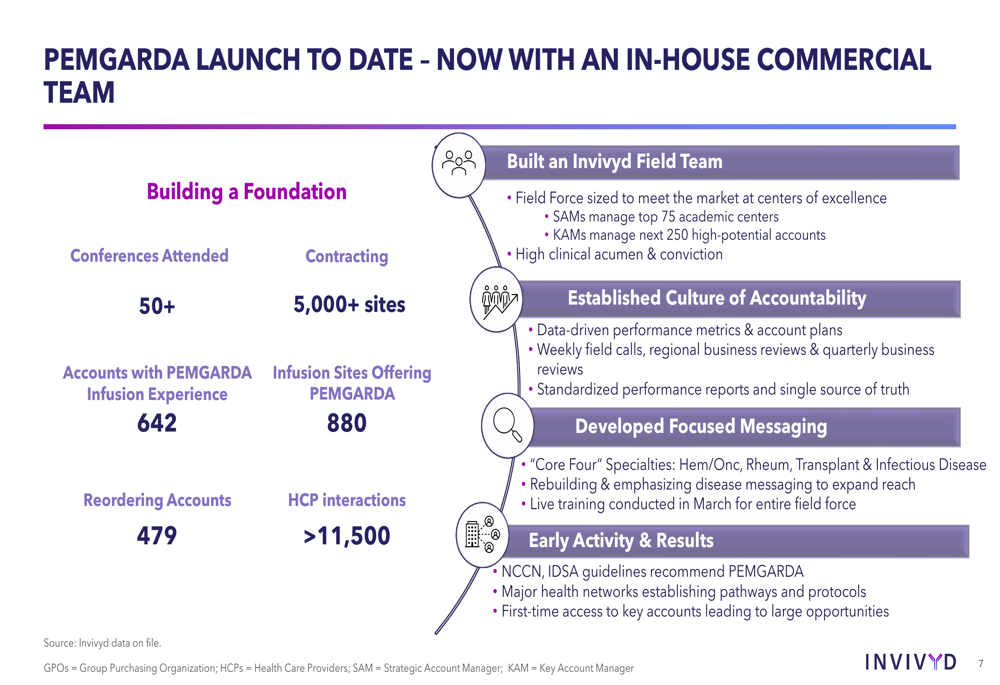

Invivyd has transitioned to an in-house commercial team, which is showing measured growth across key performance indicators. The company has established a significant commercial footprint with over 5,000 contracted sites and 642 accounts with PEMGARDA infusion experience, of which 479 are reordering accounts.

The following chart highlights the company’s commercial achievements to date:

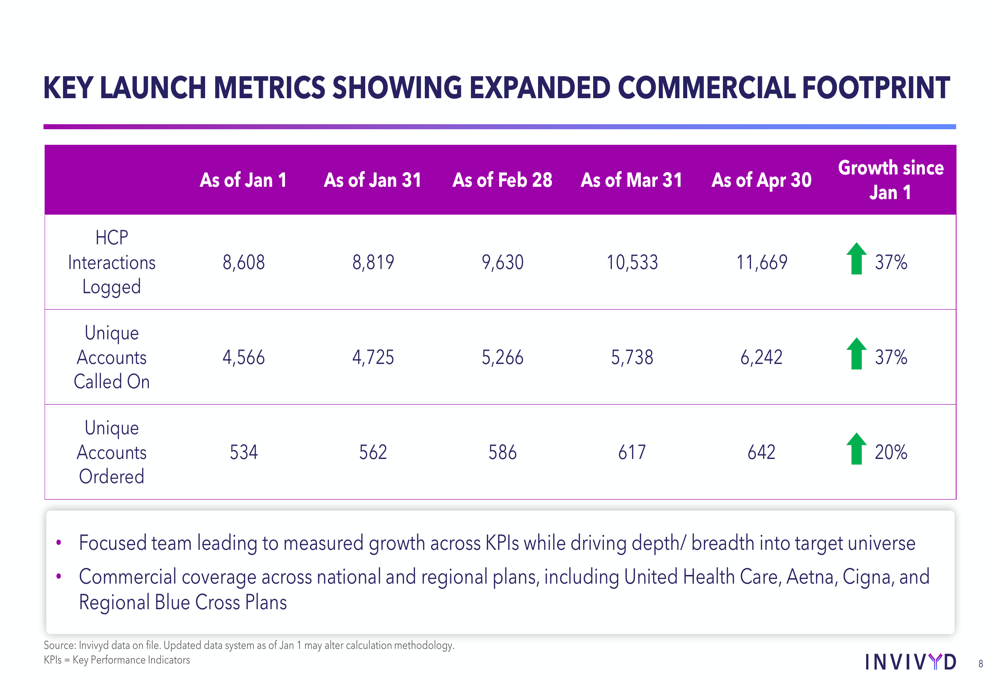

Commercial metrics from January through April 2025 demonstrate steady growth, with a 37% increase in healthcare provider interactions, a 37% increase in unique accounts called on, and a 20% increase in unique accounts ordered:

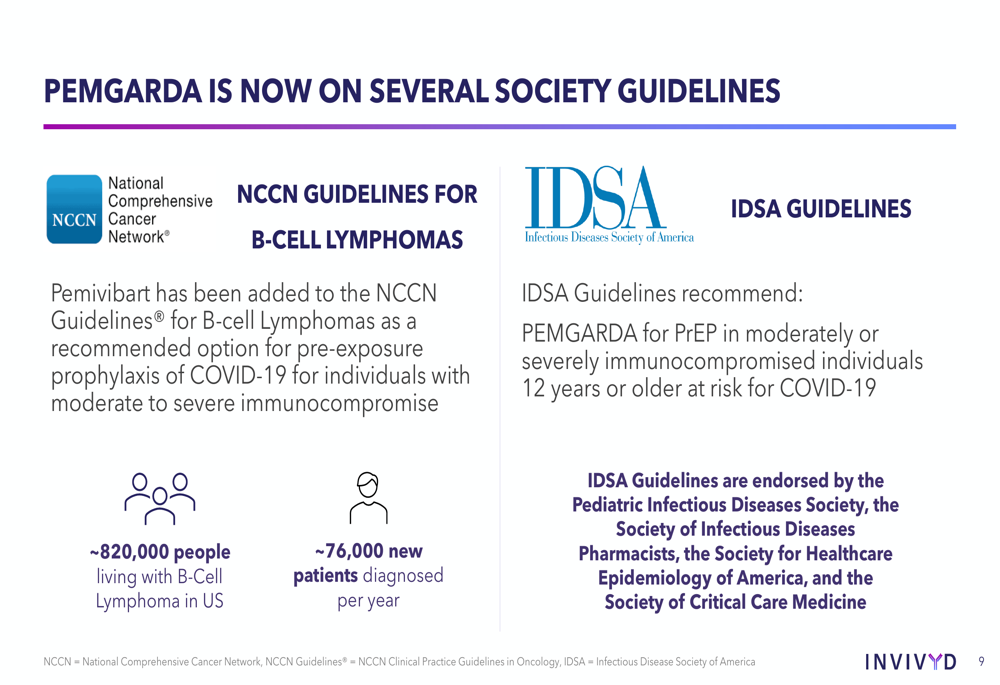

A significant milestone for PEMGARDA’s market acceptance is its inclusion in medical society guidelines. The National Comprehensive Cancer Network (NCCN) has added pemivibart to its guidelines for B-cell lymphomas as a recommended option for pre-exposure prophylaxis of COVID-19. Additionally, the Infectious Diseases Society of America (IDSA) recommends PEMGARDA for pre-exposure prophylaxis in moderately or severely immunocompromised individuals:

Market Positioning and Pricing Strategy

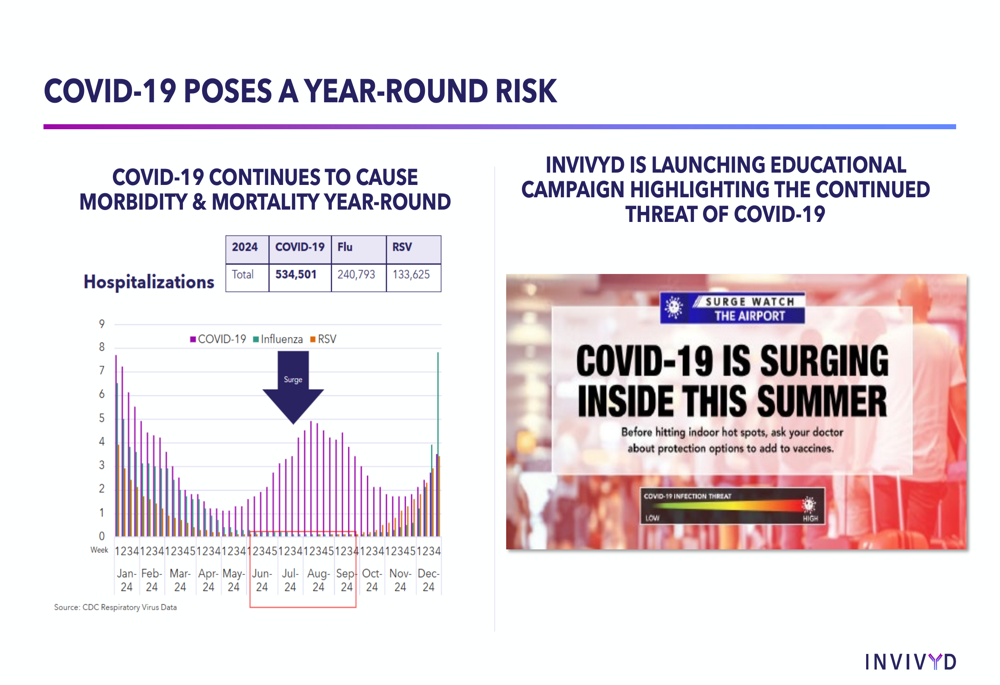

Invivyd emphasized that COVID-19 continues to pose a year-round risk, with CDC data showing higher hospitalizations from COVID-19 (240,793) compared to flu (133,625) and RSV (133,625) in 2024:

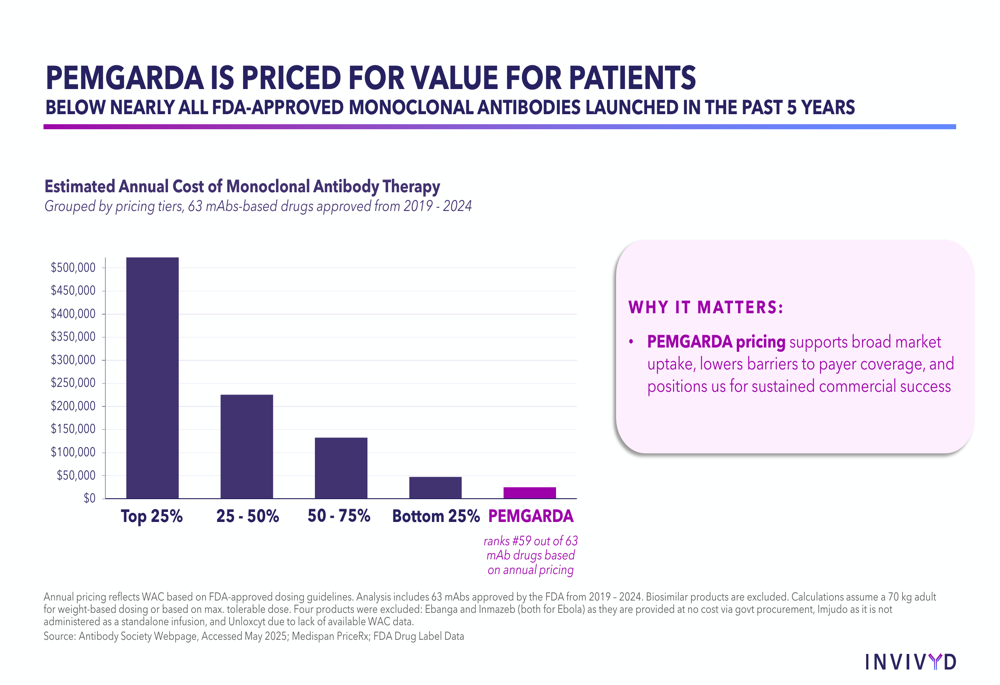

The company has positioned PEMGARDA competitively in the market, pricing it below nearly all FDA-approved monoclonal antibodies launched in the past five years. PEMGARDA ranks 59th out of 63 mAb drugs based on annual pricing, which the company believes supports broader market uptake and lowers barriers to payer coverage:

Regulatory Challenges and Strategic Response

A significant challenge for Invivyd has been regulatory hurdles. In February 2025, the FDA declined the company’s Emergency Use Authorization (EUA) request for pemivibart as a treatment for COVID-19 in immunocompromised patients. The FDA cited concerns about the duration of adequate antibody titers, comparative neutralization titers against variants, and optimal dosing for severely immunocompromised patients.

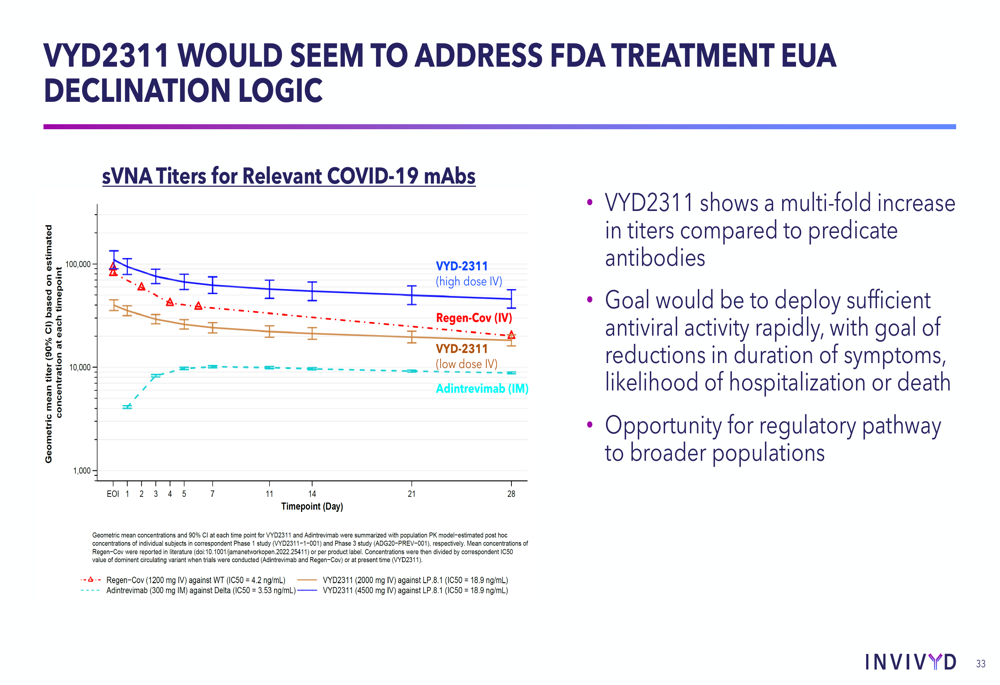

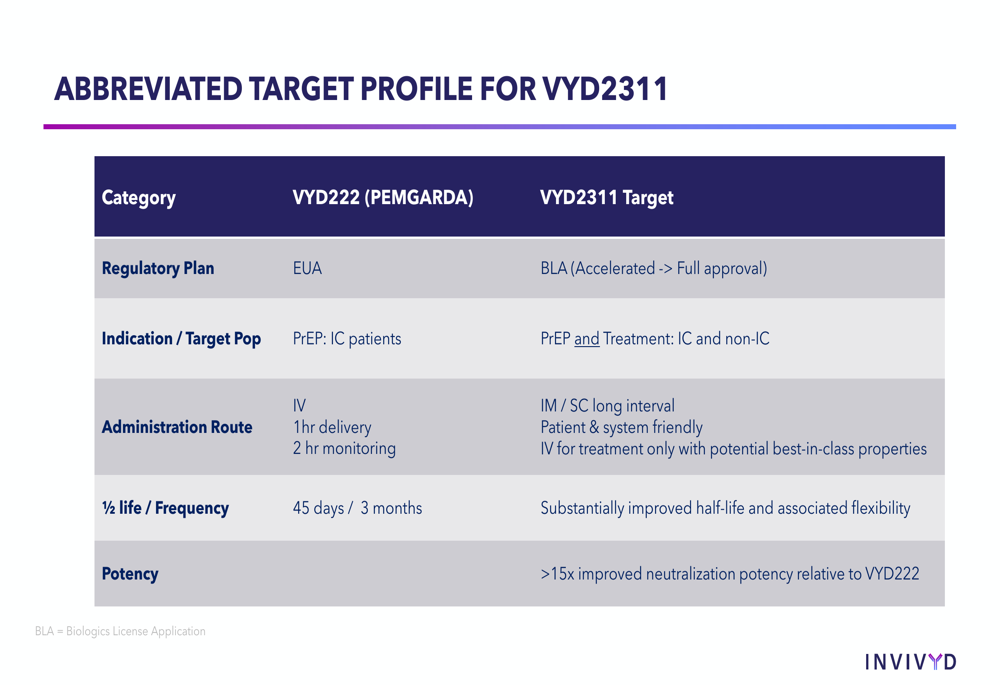

In response, Invivyd is advancing VYD2311, its next-generation antibody designed to address the FDA’s concerns. The company highlighted that VYD2311 shows improved neutralization potency relative to pemivibart:

Pipeline Development

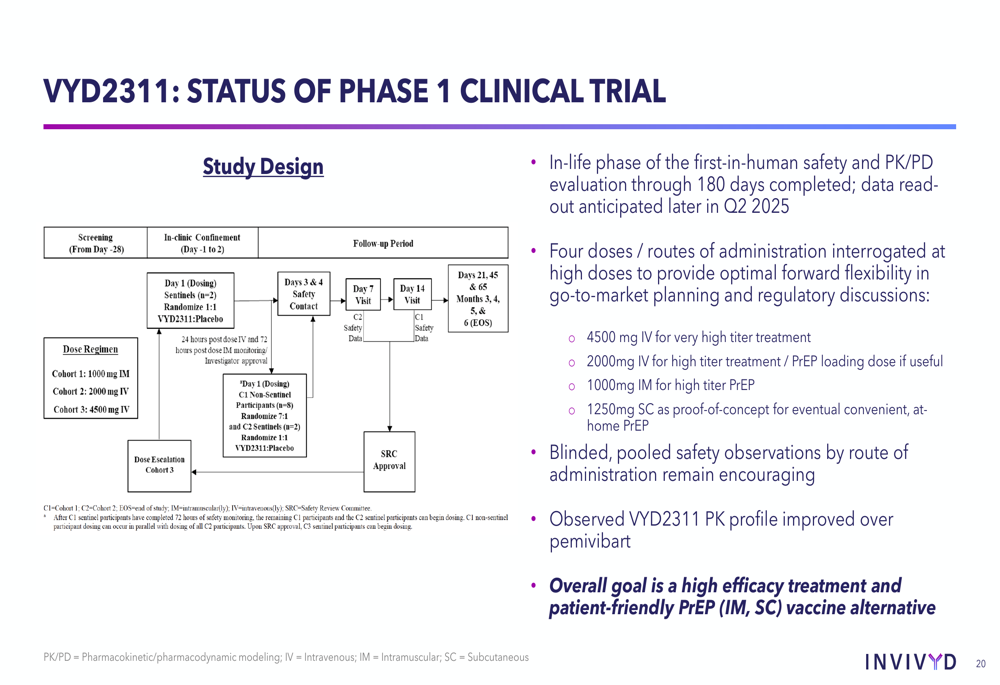

Invivyd’s Phase 1 clinical trial for VYD2311 has completed its in-life phase, with data expected in Q2 2025. The trial evaluated four doses/routes of administration (4500 mg IV, 2000mg IV, 1000mg IM, 1250mg SC), with the company noting that VYD2311’s pharmacokinetic profile shows improvement over pemivibart:

The company aims to position VYD2311 for both prevention and treatment indications with improved administration options and half-life compared to PEMGARDA:

Beyond COVID-19, Invivyd is expanding its pipeline with discovery programs in Respiratory Syncytial Virus (RSV) and measles. The company expects to identify a pre-clinical measles monoclonal antibody candidate in 2025.

Financial Outlook and Challenges

Invivyd’s rapid cash burn remains a concern. The company’s cash position has declined from $107 million in Q3 2024 to $48.1 million in Q1 2025, a steeper decline than previously anticipated. This aligns with InvestingPro data from the previous quarter, which noted the company was "quickly burning through cash."

The company is targeting profitability by the first half of 2025, consistent with its previous guidance of profitability by June 2025. This goal depends on continued revenue growth from PEMGARDA, further reductions in operating expenses, and potential regulatory progress with VYD2311.

Invivyd noted that it is "well-insulated from potential tariffs and most-favored-nation impact on PEMGARDA," as its commercial supply is located in the U.S. and not commercialized outside the country.

Forward-Looking Statements

Invivyd’s strategy focuses on three key areas: growing PEMGARDA revenue through expanded commercial reach, advancing VYD2311 to address FDA concerns and potentially expand market opportunities, and maintaining financial discipline to extend cash runway toward profitability.

The company believes the new U.S. administration’s views on infectious disease align with Invivyd’s strategy, including a favorable view on monoclonal antibodies compared to the previous administration’s focus on mRNA vaccines. Invivyd is engaging directly with the FDA and HHS regarding its pipeline and strategy, and submitted a Citizen Petition in May 2025.

With its stock trading near 52-week lows, Invivyd faces pressure to demonstrate commercial momentum and regulatory progress in the coming quarters to reassure investors about its path to profitability and long-term viability.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.