Trump signs order raising Canada tariffs to 35% from 25%

Introduction & Market Context

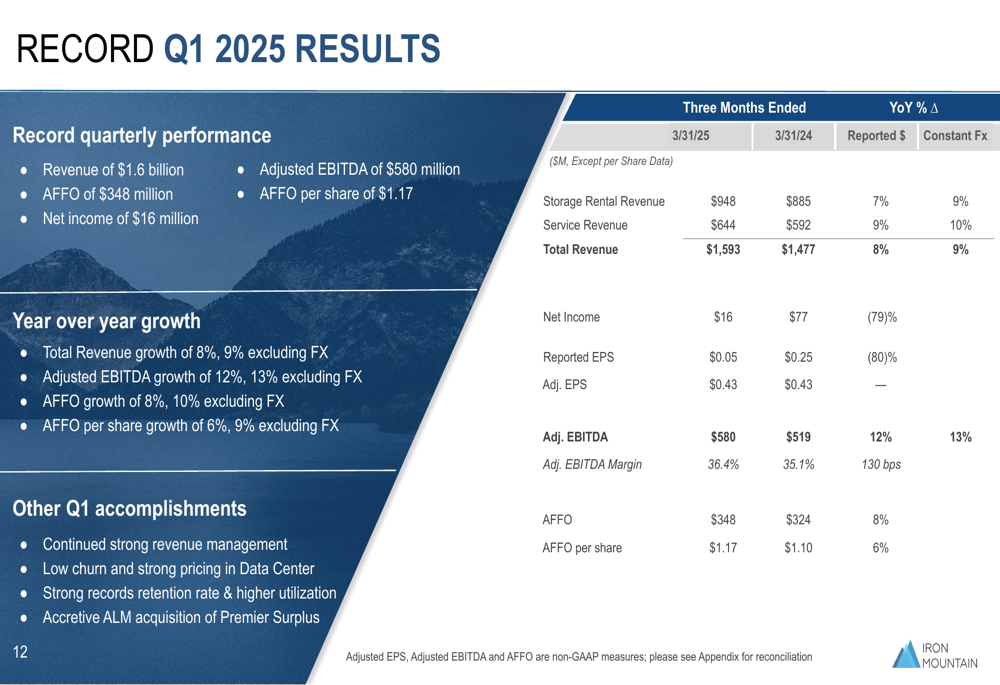

Iron Mountain Incorporated (NYSE:IRM) released its Q1 2025 earnings presentation on May 1, 2025, showcasing strong financial performance across all key metrics and raising its full-year guidance. The information management and storage company reported record quarterly results, with revenue reaching $1.6 billion, up 8% year-over-year (9% excluding foreign exchange impacts).

The company continues to execute its "Matterhorn" strategy, which focuses on accelerating enterprise growth through its traditional Records and Information Management (RIM) business while expanding rapidly in high-growth areas including Data Centers, Digital Solutions, and Asset Lifecycle Management (ALM).

Quarterly Performance Highlights

Iron Mountain delivered record quarterly performance in Q1 2025, with revenue of $1.6 billion, Adjusted EBITDA of $580 million, and AFFO (Adjusted Funds From Operations) of $348 million. The company’s net income was $16 million, with AFFO per share reaching $1.17.

As shown in the following detailed financial results table, the company achieved solid growth across all key metrics compared to Q1 2024:

Storage rental revenue, which forms the backbone of Iron Mountain’s business model, grew by 7% (9% in constant currency) to $948 million. Service revenue increased by 9% (10% in constant currency) to $644 million. The company’s Adjusted EBITDA margin expanded by 130 basis points to 36.4%, demonstrating improved operational efficiency.

Strategic Growth Initiatives

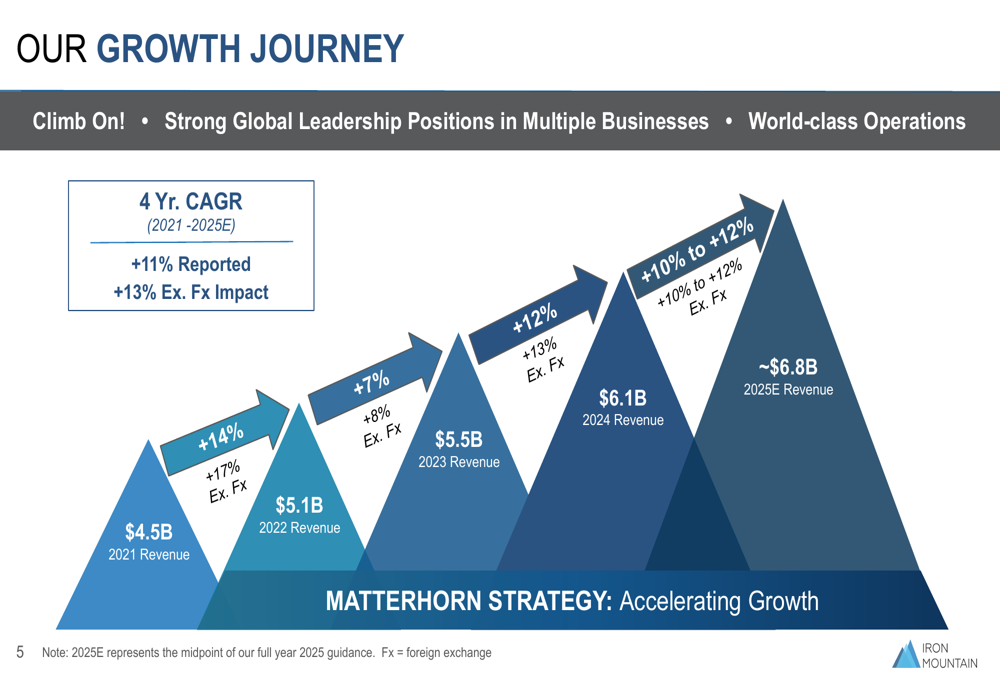

Iron Mountain’s growth strategy centers on expanding its high-growth businesses while maintaining its core Records and Information Management operations. The company’s revenue has grown at an 11% CAGR from 2021 to 2025 (estimated), with even stronger growth when excluding foreign exchange impacts.

The following chart illustrates the company’s impressive revenue growth trajectory over this period:

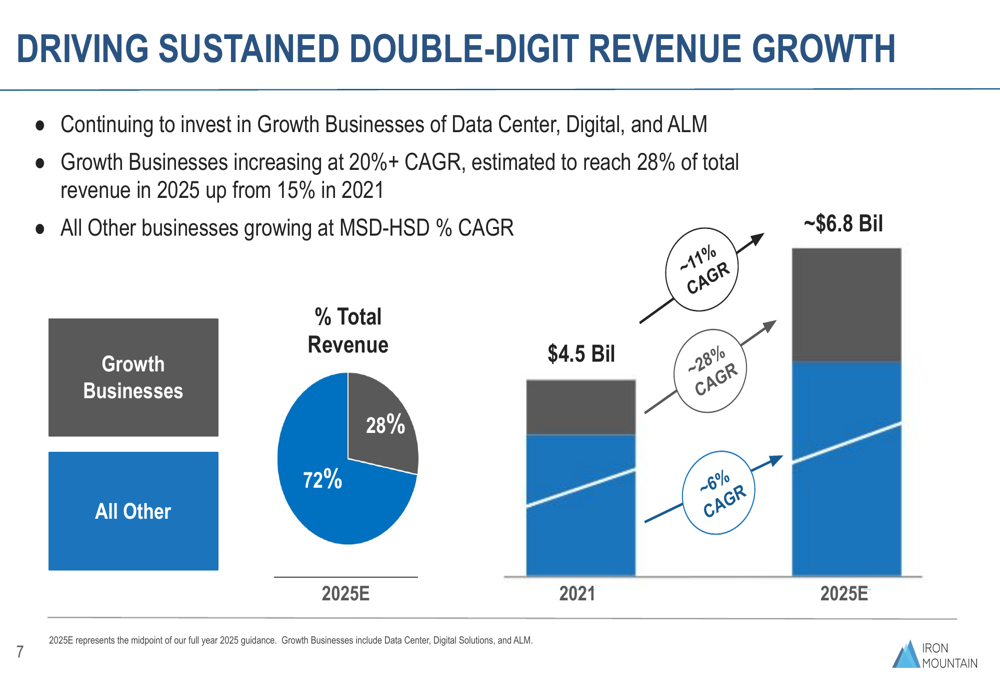

A key driver of this growth is the company’s strategic shift toward high-growth businesses, which are increasing at a 20%+ CAGR. These businesses, which include Data Center, Digital Solutions, and Asset Lifecycle Management, are expected to represent 28% of total revenue in 2025, up from just 15% in 2021.

As shown in the following visualization, this shift is significantly contributing to Iron Mountain’s sustained double-digit revenue growth:

The Data Center business has been particularly strong, with storage rental revenue growing 24% in Q1 2025. Iron Mountain currently has 424 MW of operating data center capacity (96% leased), 185 MW under construction (79% pre-leased), and 671 MW held for future development. The company serves 1,300+ data center customers, including five of the largest global hyperscalers.

The Asset Lifecycle Management (ALM) business also showed robust performance, with organic revenue growth of 22% year-over-year in Q1 2025. This segment, which provides services such as IT asset disposition, data erasure, and recycling, is expected to generate approximately $550 million in revenue in 2025.

2025 Outlook & Guidance

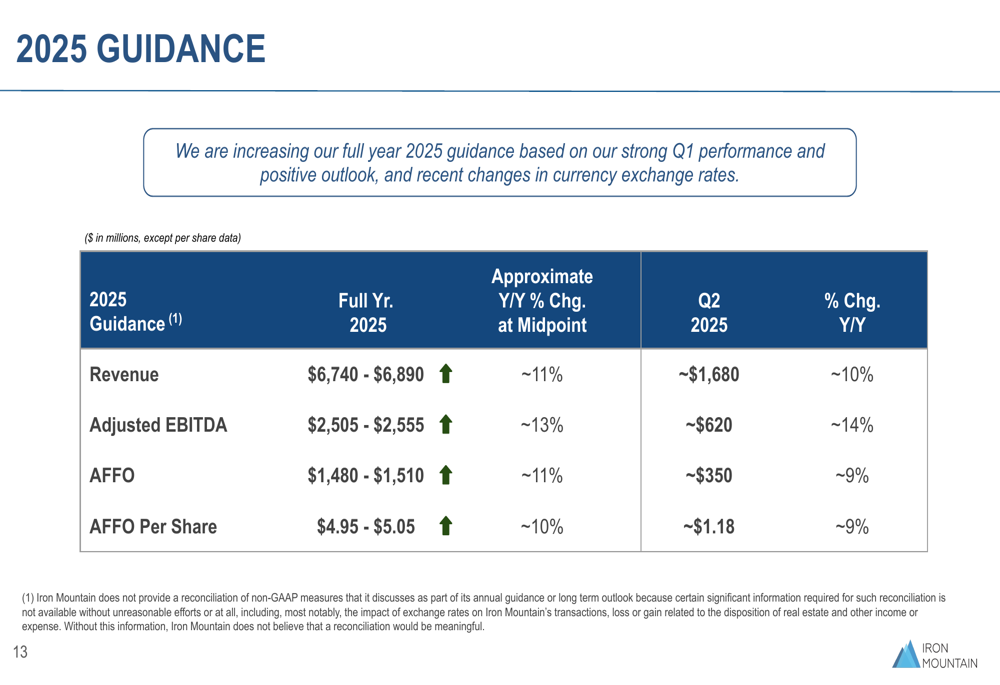

Based on strong Q1 performance and a positive outlook, Iron Mountain raised its full-year 2025 guidance. The company now expects:

The updated guidance represents approximately 11% year-over-year revenue growth, 13% Adjusted EBITDA growth, and 11% AFFO growth at the midpoint. For Q2 2025, the company projects revenue of approximately $1.68 billion (10% year-over-year growth) and Adjusted EBITDA of around $620 million (14% growth).

This outlook reflects Iron Mountain’s confidence in its ability to continue executing its growth strategy while maintaining strong margins and cash flow generation.

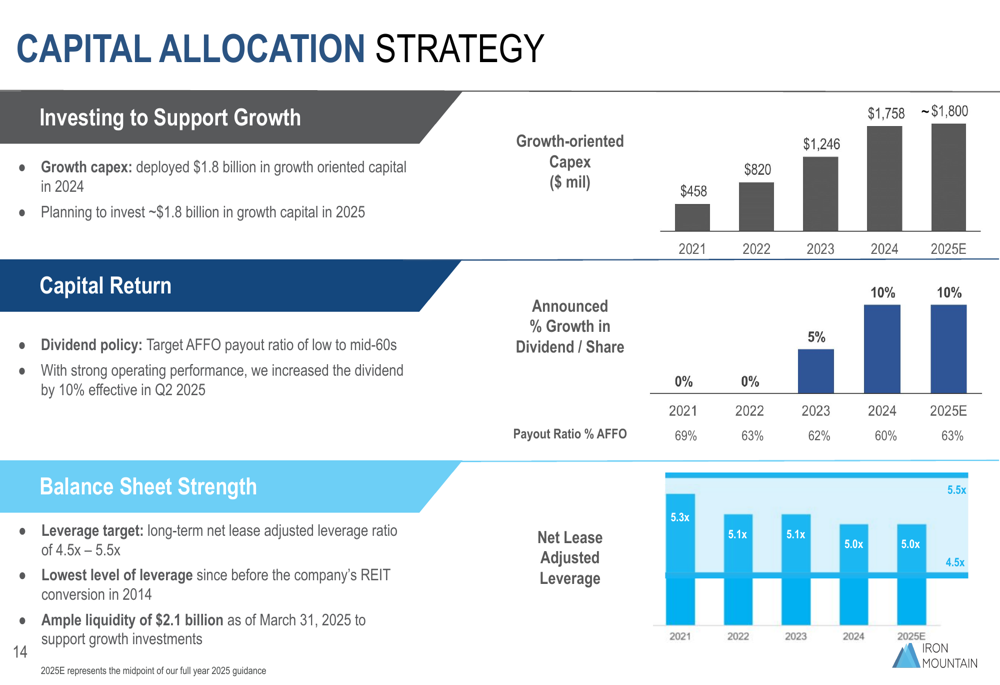

Capital Allocation Strategy

Iron Mountain’s capital allocation strategy balances investments in growth with returning capital to shareholders. The company deployed $1.8 billion in growth-oriented capital in 2024 and plans to invest approximately the same amount in 2025.

As illustrated in the following capital allocation overview, the company has consistently increased its dividend while maintaining a disciplined approach to leverage:

With strong operating performance, Iron Mountain increased its dividend by 10% in Q2 2025, maintaining its target AFFO payout ratio in the low to mid-60s. The company’s balance sheet remains strong, with a net lease adjusted leverage ratio expected to reach 4.5x by the end of 2025 – the lowest level since before its REIT conversion in 2014.

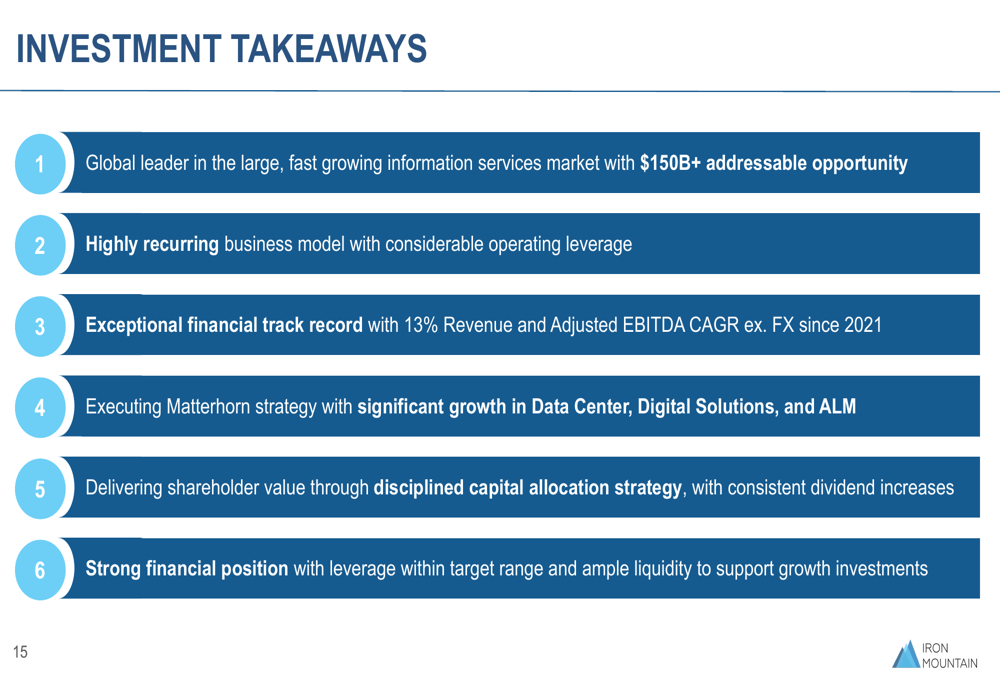

Investment Thesis

Iron Mountain summarizes its investment case with six key points that highlight its market position, business model, and growth trajectory:

The company emphasizes its leadership in the large, fast-growing information services market with an addressable opportunity exceeding $150 billion. Its highly recurring business model provides considerable operating leverage, while its exceptional financial track record demonstrates consistent execution.

With the continued implementation of its Matterhorn strategy, disciplined capital allocation, and strong financial position, Iron Mountain appears well-positioned to deliver continued growth and shareholder value in the coming years.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.