IREN proposes $875 million convertible notes offering due 2031

Introduction & Market Context

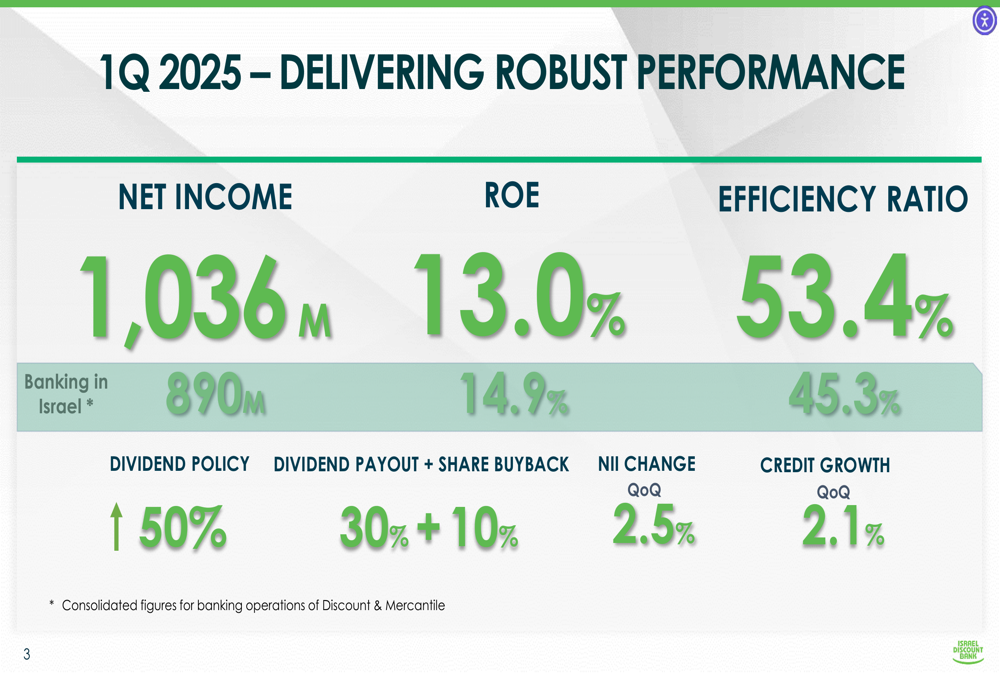

Israel Discount Bank Ltd (TASE:DSCT) reported a solid performance for the first quarter of 2025, with net income reaching NIS 1,036 million and return on equity (ROE) of 13.0%, according to the bank’s quarterly presentation released on May 19, 2025. The results come as Israel’s economy shows signs of recovery following the impact of war in 2024, with GDP growth expected to rebound to 3.5% in 2025 from just 0.9% in the previous year.

The bank’s shares were trading at NIS 2,939 on the day of the presentation, near its 52-week high of NIS 2,995, reflecting investor confidence in the bank’s performance and strategic direction.

Quarterly Performance Highlights

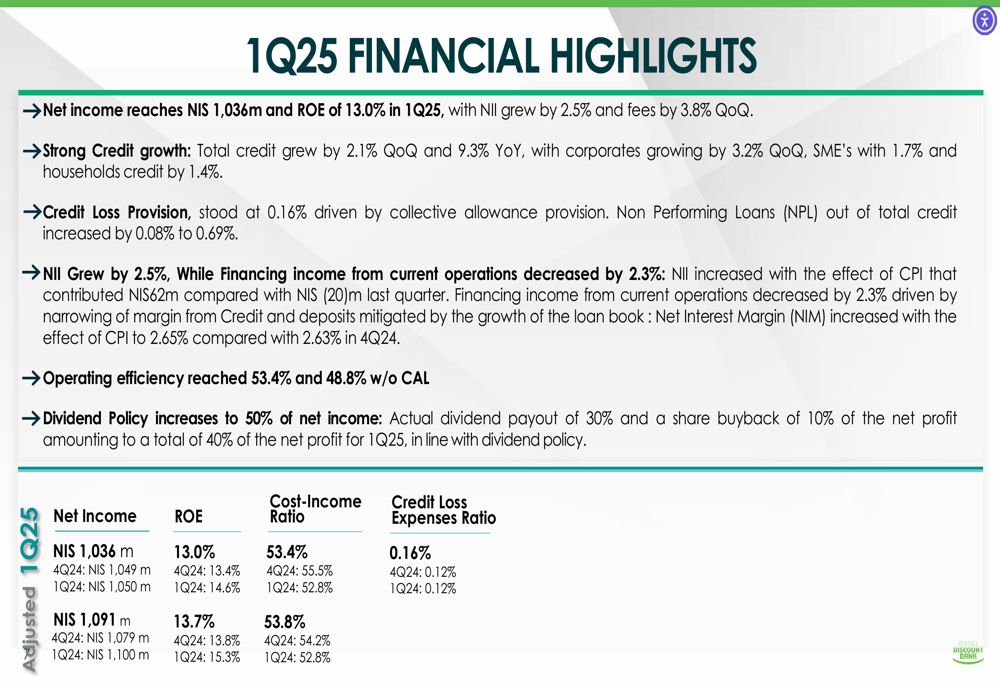

Israel Discount Bank delivered robust financial results in Q1 2025, maintaining strong profitability despite challenging market conditions. The bank reported net income of NIS 1,036 million, slightly down from NIS 1,049 million in Q4 2024, with an ROE of 13.0%.

As shown in the following summary of key performance metrics:

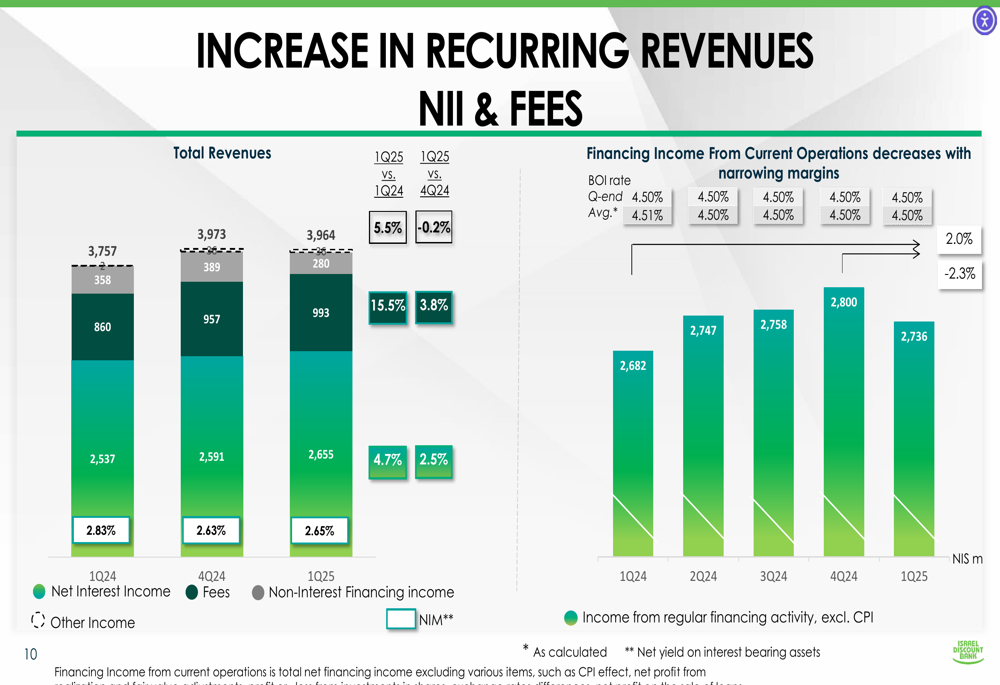

Net interest income (NII) grew by 2.5% quarter-over-quarter to NIS 2,655 million, while fee income increased by 3.8% to NIS 993 million. The bank’s efficiency ratio improved to 53.4% from 55.5% in the previous quarter, reflecting successful cost containment efforts.

The bank’s detailed financial highlights demonstrate consistent performance across key metrics:

Total (EPA:TTEF) income remained relatively stable at NIS 3,964 million, a slight decrease of 0.2% from the previous quarter but up 5.5% year-over-year. Operating expenses decreased by 4.0% quarter-over-quarter to NIS 2,116 million, contributing to the improved efficiency ratio.

Credit Growth and Asset Quality

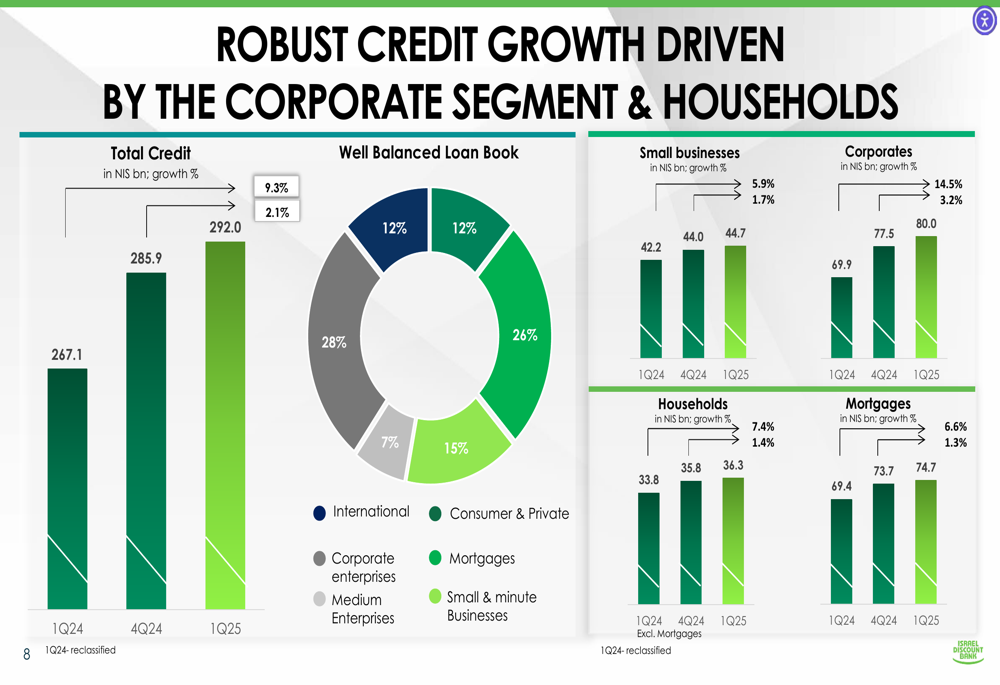

Israel Discount Bank continued to demonstrate strong credit growth across all segments, with total credit increasing by 2.1% quarter-over-quarter and 9.3% year-over-year to reach NIS 292.0 billion. The growth was particularly strong in the corporate segment, which expanded by 3.2% quarter-over-quarter, while small businesses and households grew by 1.7% and 1.4%, respectively.

The following chart illustrates the bank’s balanced loan book and robust credit growth across segments:

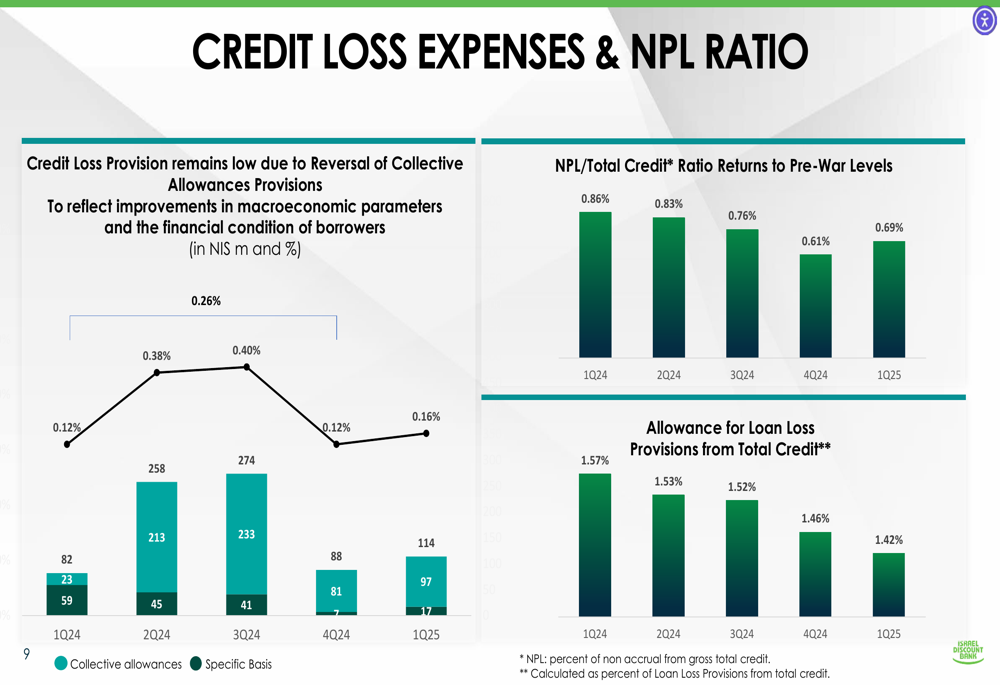

Despite the strong credit growth, the bank maintained prudent risk management. The credit loss provision ratio stood at 0.16% in Q1 2025, up slightly from 0.12% in the previous quarter, driven by collective allowance provisions. The non-performing loan (NPL) ratio increased to 0.69% from 0.61% in Q4 2024, returning to pre-war levels.

The trend in credit loss provisions and NPL ratio is illustrated in the following chart:

The bank’s allowance for loan loss provisions from total credit decreased to 1.42% in Q1 2025 from 1.46% in Q4 2024, reflecting the improvement in macroeconomic parameters and the financial condition of borrowers.

Revenue Composition and Expense Management

Israel Discount Bank’s recurring revenues showed positive momentum in Q1 2025, with net interest income and fees both increasing compared to the previous quarter. However, financing income from current operations decreased by 2.3% due to narrowing margins from credit and deposits, partially offset by growth in the loan book.

The following chart shows the breakdown of the bank’s revenue streams:

The bank maintained strong expense discipline, with total operating expenses decreasing by 4.0% quarter-over-quarter to NIS 2,116 million. This contributed to the improvement in the efficiency ratio to 53.4% from 55.5% in Q4 2024.

Funding Base and Capital Position

Israel Discount Bank maintained a robust and diversified funding base, with total deposits from the public reaching NIS 326.6 billion. Retail deposits accounted for 50% of the total, providing a stable funding source.

The bank’s capital ratios remained well above regulatory requirements, with a Total Capital Ratio of 13.49% (vs. requirement of 12.50%) and a Tier 1 Capital Ratio of 10.54% (vs. requirement of 9.19%). The Leverage Ratio stood at 6.8%, comfortably above the 4.5% regulatory requirement.

Strategic Initiatives and Dividend Policy

In a significant development, Israel Discount Bank announced an increase in its dividend policy to 50% of net income, demonstrating confidence in its sustainable profitability. For Q1 2025, the actual payout consists of a 30% dividend and a 10% share buyback, totaling 40% of net income.

This increase aligns with the bank’s long-term strategy to enhance shareholder value while maintaining strong capital ratios. The bank’s solid performance across key metrics supports this more generous shareholder return policy.

Subsidiary Performance

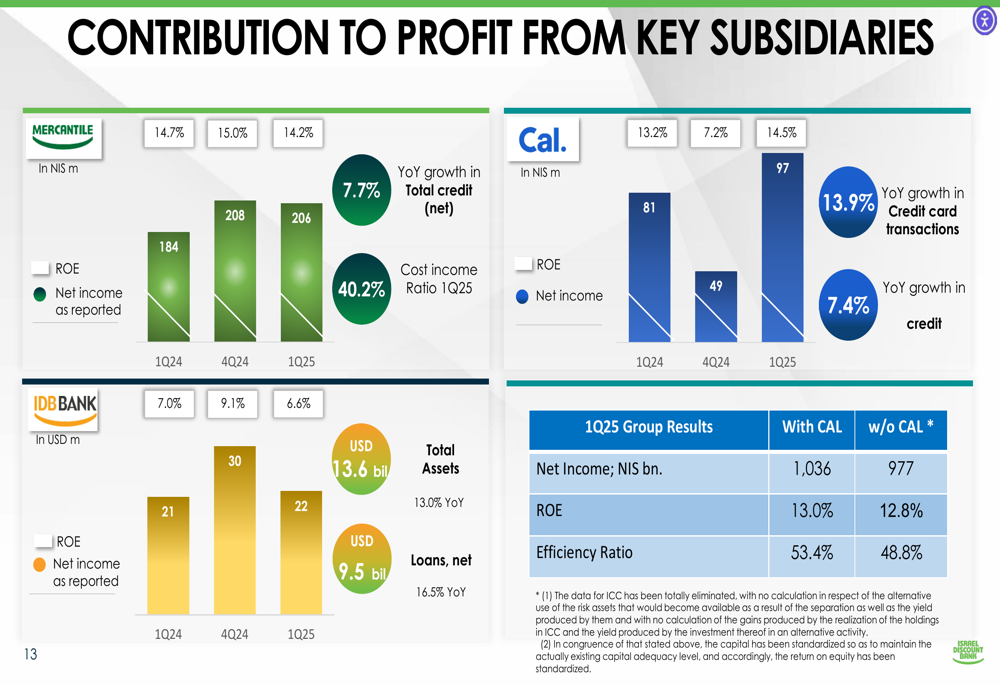

Israel Discount Bank’s key subsidiaries continued to contribute significantly to the group’s overall performance. Mercantile Bank (NASDAQ:MBWM) reported a net income of NIS 206 million with an ROE of 14.2%, while CAL (credit card subsidiary) contributed NIS 97 million with strong growth in credit card transactions.

The following chart details the contribution from each subsidiary:

Mercantile Bank demonstrated strong credit growth of 7.7% year-over-year and maintained an impressive efficiency ratio of 40.2%. CAL showed robust growth in credit card transactions (13.9% year-over-year) and credit portfolio (7.4% year-over-year). IDB Bank, the group’s U.S. subsidiary, reported total assets of USD 13.6 billion and net income of NIS 22 million.

Economic Outlook

The economic context for Israel Discount Bank’s performance shows signs of recovery, with GDP growth expected to rebound to 3.5% in 2025 after being impacted by war in 2024. The job market remains resilient, with unemployment at 2.9% as of March 2025, indicating full employment.

However, growth drivers remain uncertain, with housing market sales declining after a robust recovery in 2024 and private spending remaining flat. The Bank of Israel is expected to slowly reduce interest rates, with market expectations for the BOI rate to decrease to 3.85% by the end of 2025 from the current 4.50%.

Inflation is projected to converge within the BOI’s target range, with CPI forwards indicating 2.0% inflation for the next three years, well within the central bank’s upper limit of 3.0%.

Forward-Looking Statements

Looking ahead, Israel Discount Bank remains focused on maintaining strong credit growth while containing expenses. The bank’s increased dividend policy reflects confidence in its ability to generate sustainable profits while maintaining adequate capital levels.

The bank’s management summarized their outlook by highlighting the continuous strong results, solid credit growth momentum, low credit loss provisions, and restrained expenses. The increased dividend policy to 50% underscores their commitment to enhancing shareholder value as part of a long-term strategy.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.