EU and US could reach trade deal this weekend - Reuters

Introduction & Market Context

Italgas SpA (BIT:IG) presented its Q1 2025 financial results on May 7, 2025, revealing solid growth across all business segments despite regulatory challenges. The company’s stock responded positively, rising 2.02% to €7.17 on the day of the presentation.

The results come at a pivotal moment for Italgas, as the company has just completed its transformational acquisition of 2i Rete Gas on April 1, 2025, approximately 11 months after beginning exclusive negotiations. This acquisition significantly expands Italgas’ footprint in the Italian gas distribution market.

Quarterly Performance Highlights

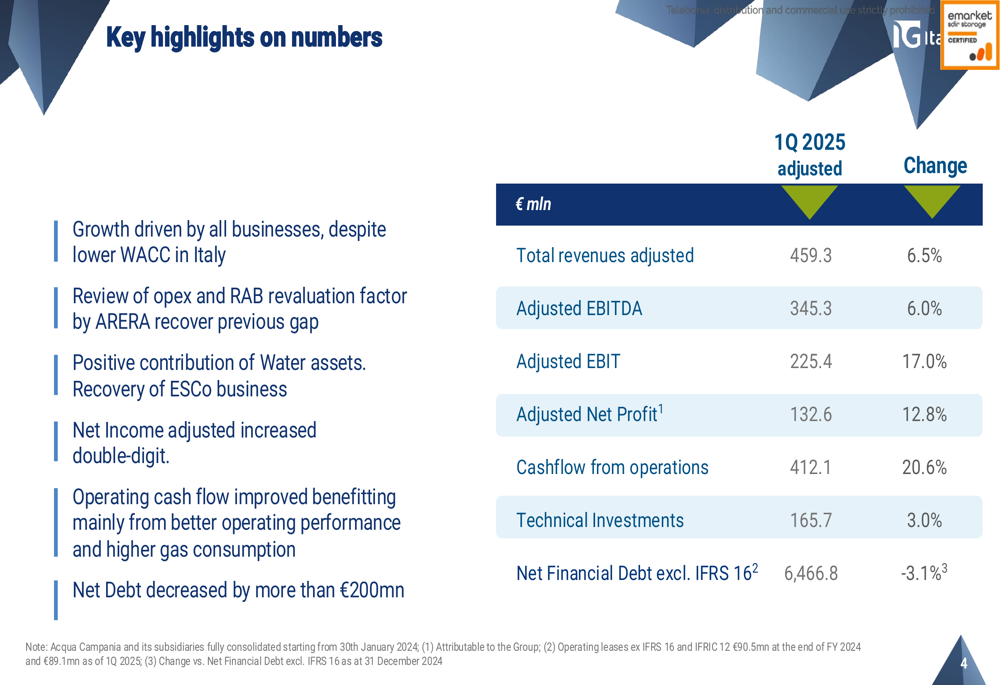

Italgas reported strong financial performance for the first quarter of 2025, with growth across all key metrics despite the lower WACC (Weighted Average Cost of Capital) in Italy.

As shown in the following comprehensive financial summary:

Total (EPA:TTEF) adjusted revenues reached €459.3 million, a 6.5% increase compared to Q1 2024. Adjusted EBITDA grew by 6.0% to €345.3 million, while adjusted EBIT saw an impressive 17.0% jump to €225.4 million. The company’s adjusted net profit increased by 12.8% to €132.6 million, demonstrating Italgas’ ability to improve profitability despite regulatory headwinds.

Cash flow from operations showed particularly strong improvement, rising 20.6% to €412.1 million, while net financial debt excluding IFRS 16 decreased by 3.1% to €6,466.8 million.

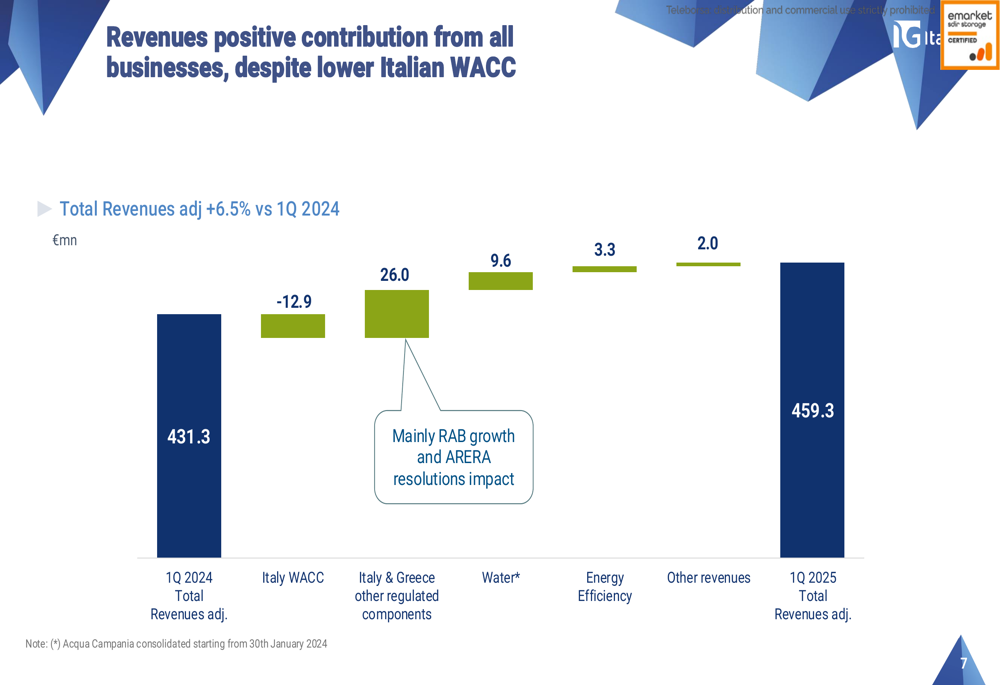

The revenue growth was driven by positive contributions from all business segments, as illustrated in this breakdown:

Despite a negative impact of €12.9 million from the lower Italian WACC, the company managed to offset this with €26.0 million in other regulated components from Italy and Greece, €9.6 million from water assets, €3.3 million from energy efficiency operations, and €2.0 million from other revenue sources.

Strategic Initiatives: 2i Rete Gas Acquisition

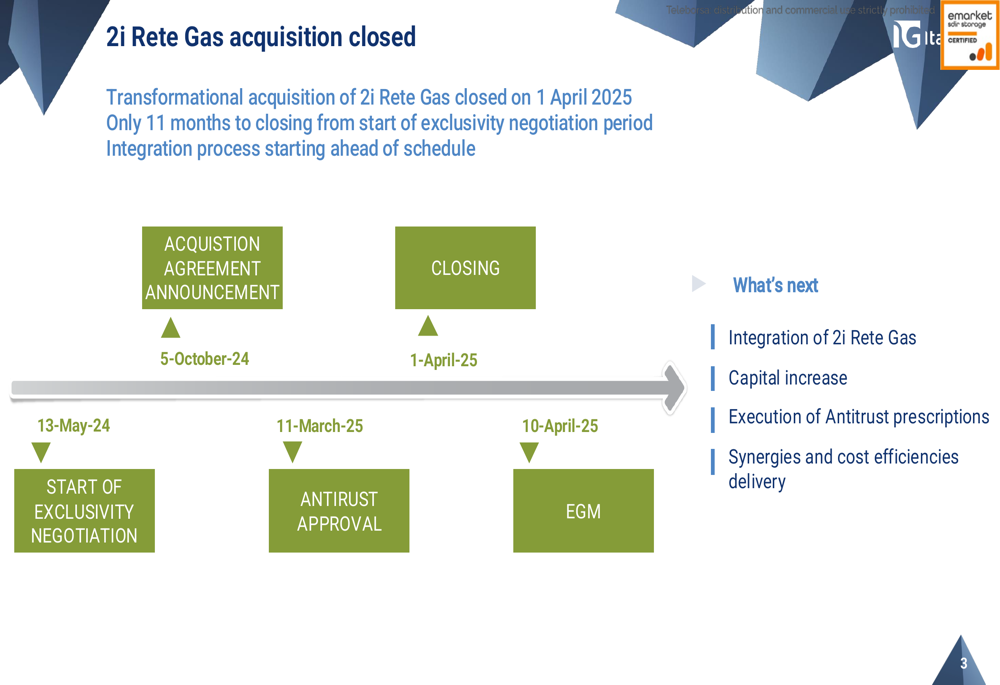

The most significant strategic development for Italgas was the completion of the 2i Rete Gas acquisition, which closed on April 1, 2025. This transformational deal represents a major milestone in the company’s expansion strategy.

The acquisition process and next steps are outlined in this timeline:

According to the presentation, the integration process is starting ahead of schedule. The next steps include the full integration of 2i Rete Gas, a capital increase, execution of antitrust prescriptions, and delivery of synergies and cost efficiencies.

Detailed Financial Analysis

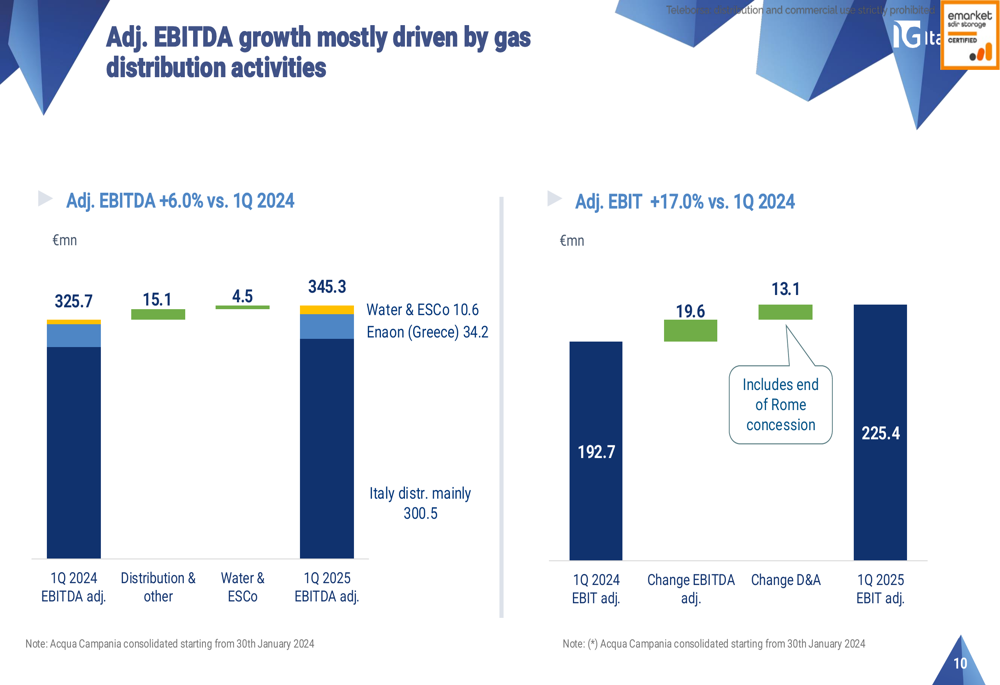

Italgas’ adjusted EBITDA and EBIT growth was primarily driven by gas distribution activities, with additional positive contributions from water assets and energy service companies.

The following chart illustrates the components of this growth:

The adjusted EBITDA increase of 6.0% was composed of €15.1 million from distribution and other activities, plus €4.5 million from water and ESCo businesses. The adjusted EBIT grew by 17.0%, benefiting from both the EBITDA improvement and a positive change in depreciation and amortization.

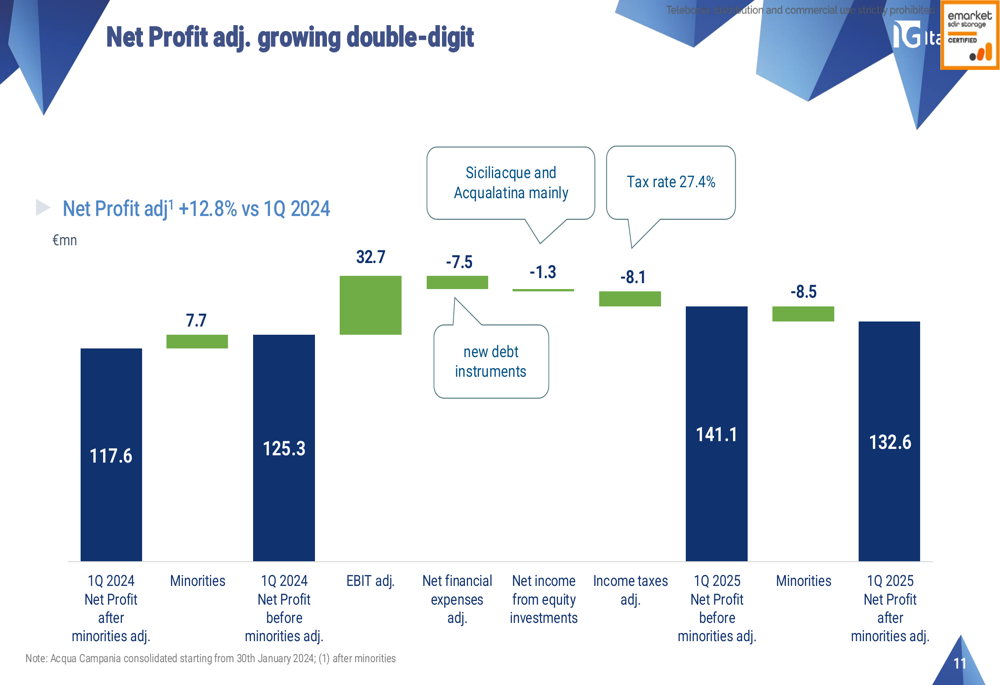

The company’s net profit growth can be attributed to several factors, as shown in this breakdown:

Despite higher net financial expenses and income taxes, the strong EBIT performance drove a 12.8% increase in adjusted net profit. The company maintained a tax rate of 27.4% during the quarter.

Technical investments for Q1 2025 totaled €165.7 million, a 3.0% increase compared to the same period in 2024. These investments were primarily allocated to development and repurposing (€104.8 million), digitalization (€37.8 million), and other initiatives (€23.1 million).

Regulatory Developments

Italgas highlighted two significant regulatory resolutions from ARERA (the Italian Regulatory Authority for Energy, Networks and Environment) that impact its operations:

1. Resolution 87/2025: Revised allowed operating expenditures and X-factor for 2020-2025 following Council of State rulings.

2. Resolution 130/2025: Changed RAB (Regulatory Asset Base) revaluation criteria, moving to Italy’s HICP (Harmonized Index of Consumer Prices) from 2024 RAB. This resulted in improved revaluation rates, with the end-2023 rate increasing to 6.2% (from 5.3%) and the end-2024 rate rising to 1.3% (from 0.3%).

Environmental Performance

The company reported increases in both energy consumption and emissions during Q1 2025. Net energy consumption rose by 4.7% compared to Q1 2024, primarily due to colder winter conditions. Scope 1 and 2 emissions increased by 24.9%, mainly attributed to gas leakages resulting from a higher amount of network inspected (20.9% more kilometers surveyed).

Forward-Looking Statements

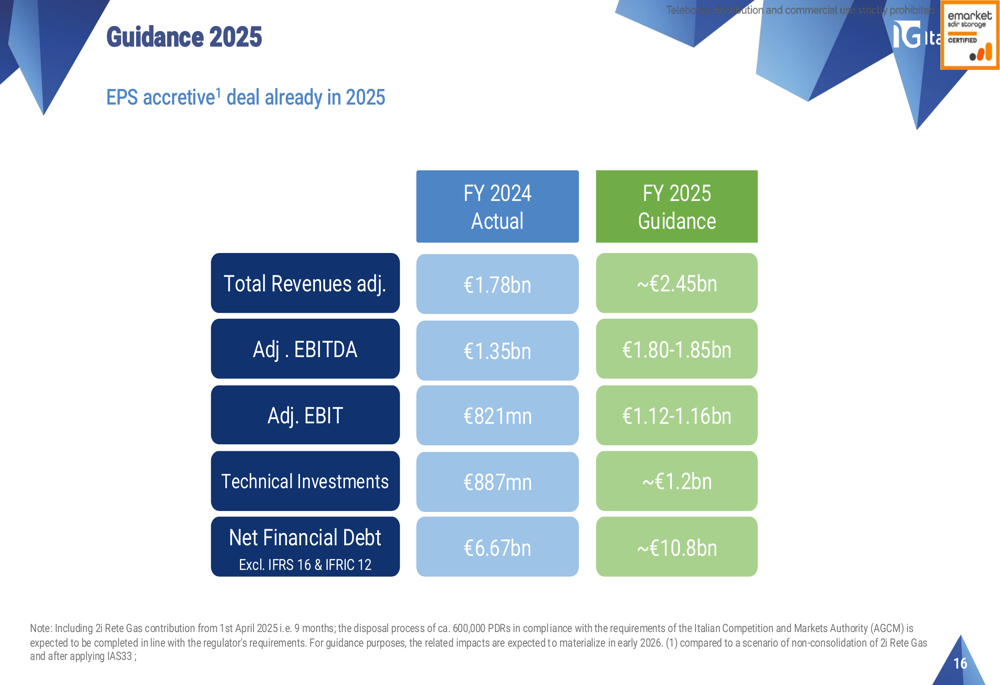

Italgas provided an optimistic outlook for 2025, reflecting the positive impact of the 2i Rete Gas acquisition, which the company describes as "EPS accretive" already in 2025.

The detailed guidance shows significant growth expectations across all metrics:

For full-year 2025, Italgas projects total adjusted revenues of approximately €2.45 billion (compared to €1.78 billion in FY 2024), adjusted EBITDA of €1.80-1.85 billion (vs. €1.35 billion), and adjusted EBIT of €1.12-1.16 billion (vs. €821 million). Technical investments are expected to reach approximately €1.2 billion, while net financial debt is projected to increase to around €10.8 billion due to the acquisition.

The company maintains a sound financial structure with low exposure to floating rates. As of Q1 2025, 87% of gross debt was fixed-rate, and 82% was in bonds. The average cost of debt was approximately 1.7% during the quarter, and the company issued a new €1 billion dual-tranche bond in Q1.

Italgas appears well-positioned to integrate the 2i Rete Gas acquisition while continuing to deliver growth across its existing business segments, despite regulatory changes and environmental challenges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.