CSL shares plunge to 7-year low on delay in US vaccine business spinoff

Introduction & Market Context

Itera ASA presented its Q3 2025 interim results on October 24, 2025, highlighting modest revenue growth and significant margin improvement in a market characterized by stability without major shifts. The company emphasized that AI is rapidly emerging as the defining force in digital transformation, while defense and protection of critical infrastructure are becoming high-growth areas for digitalization.

As shown in the company’s market assessment, these trends are being fueled by rising investments and innovation in response to geopolitical tensions:

The stock closed at NOK 8.02 on the presentation day, showing a slight decline of 1.25% from the previous close. The company’s shares have traded between NOK 7.86 and NOK 11.20 over the past 52 weeks, currently sitting near the lower end of that range despite operational improvements.

Quarterly Performance Highlights

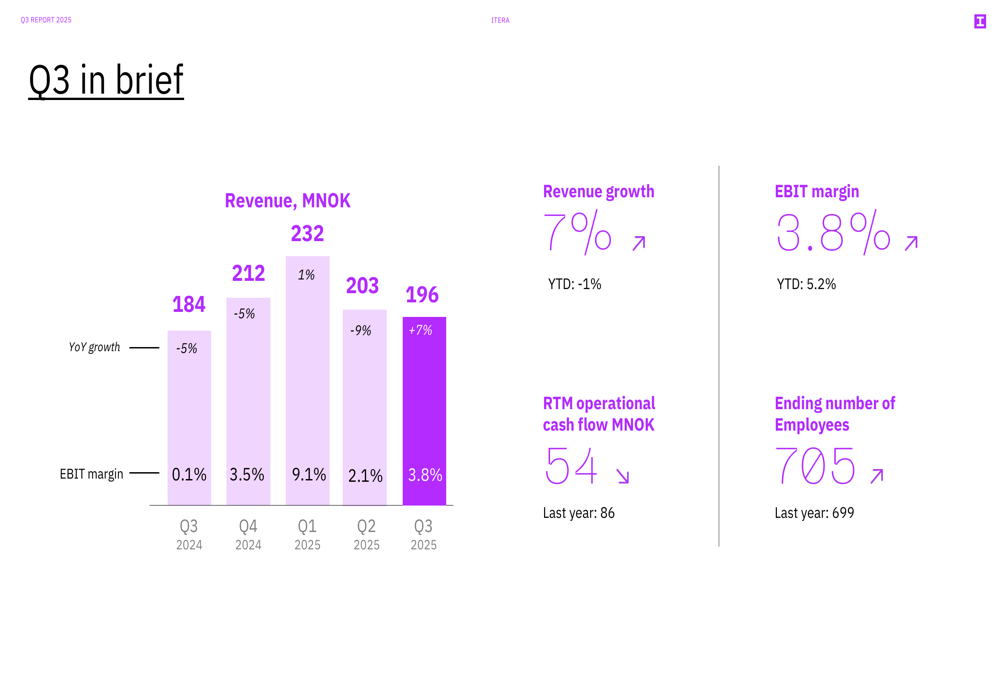

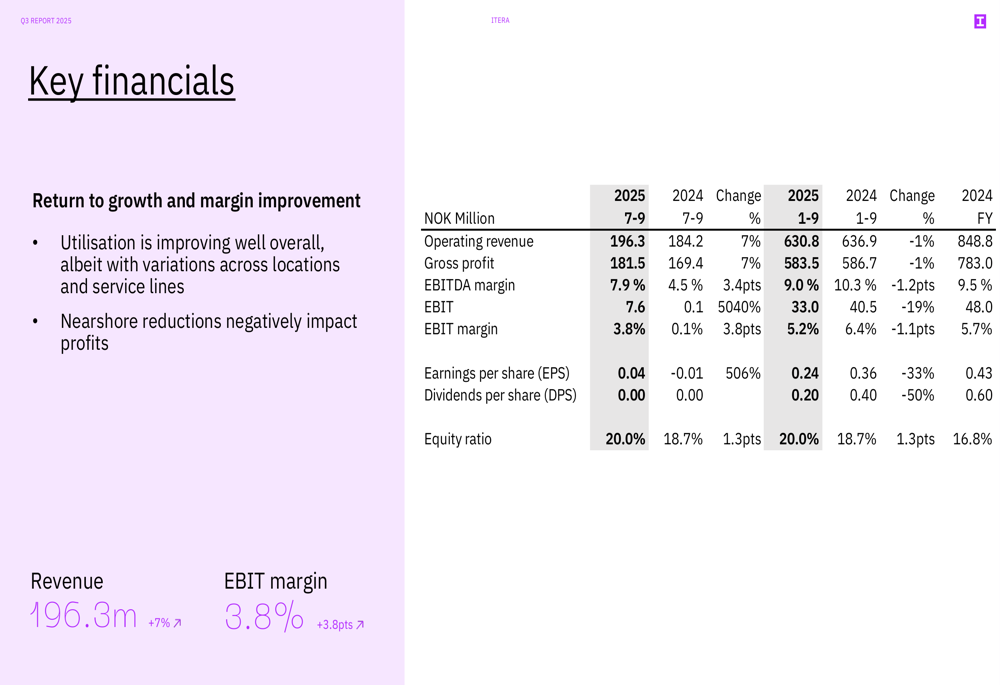

Itera reported 7% revenue growth in Q3 2025, reaching MNOK 232 compared to MNOK 212 in Q3 2024. The EBIT margin improved significantly to 3.8% from just 0.1% in the same quarter last year, driven by higher billable utilization and the company’s operational improvement program. However, year-to-date revenue showed a slight decline of 1%, with the YTD EBIT margin at 5.2%.

The following slide summarizes the key financial metrics for the quarter:

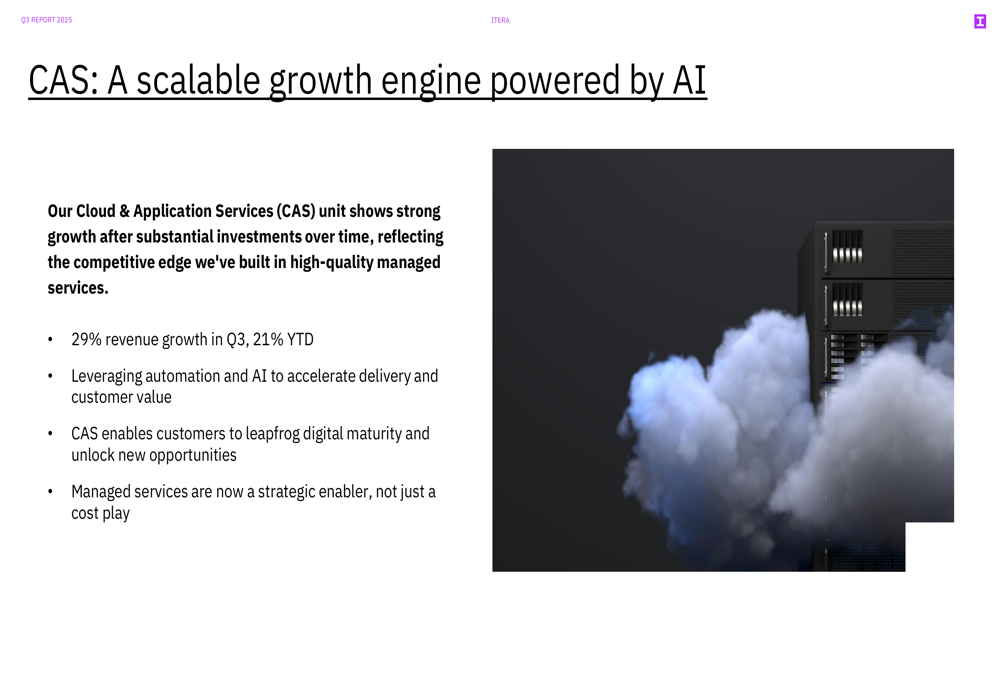

Cloud and Application Services emerged as a standout performer with 29% revenue growth in Q3 and 21% year-to-date. The company attributes this success to investments in high-quality managed services and AI-powered automation.

As illustrated in this slide, Itera positions its Cloud & Application Services unit as a scalable growth engine:

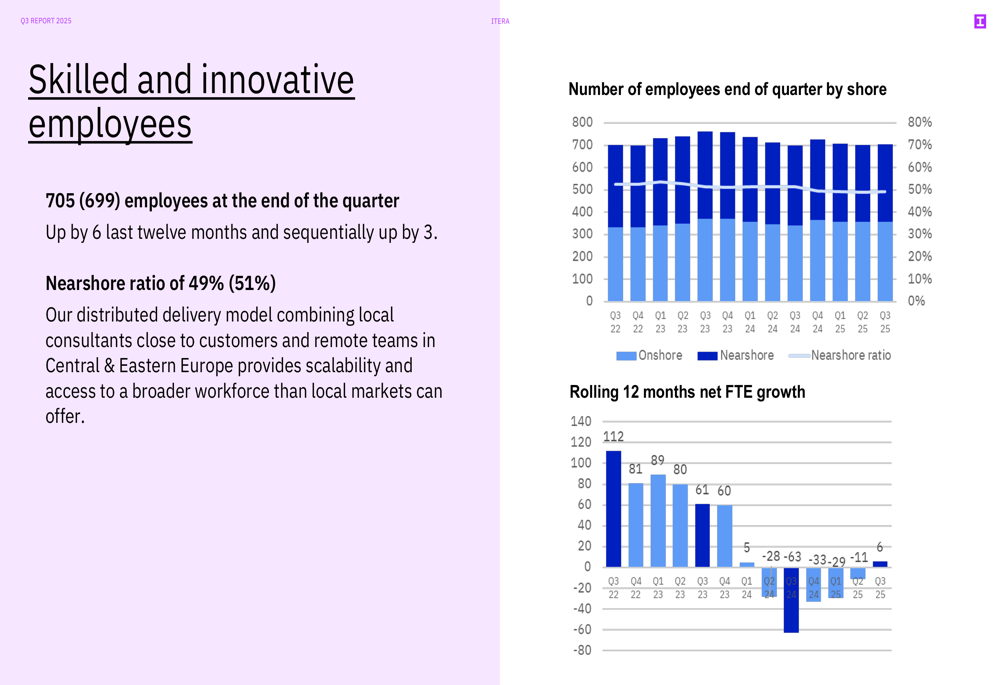

The company maintained its workforce at 705 employees, slightly up from 699 at the end of Q3 2024. The nearshore ratio stood at 49%, down from 51% a year earlier, reflecting the company’s distributed delivery model that combines local consultants with remote teams in Central and Eastern Europe.

The following chart details the employee distribution and growth trends:

Strategic Initiatives

Itera highlighted its operational improvement program aimed at enhancing profitability, competitiveness, and resilience. Key focus areas include empowering regional units, simplifying processes, leveraging AI for efficiency, reducing overhead costs, and driving regional growth through 14 local units.

The strategic framework is outlined in this slide:

The company continues to position itself with "Nordic roots, European presence," operating 14 offices across 8 countries. Notably, Itera has maintained a 17-year presence in Ukraine, which it now leverages for insights into the defense industry – a sector it identifies as having significant growth potential.

Itera’s business is structured around two main offerings: digitalization services across various sectors and responsible business advisory, particularly for companies looking to enter or rebuild in Ukraine.

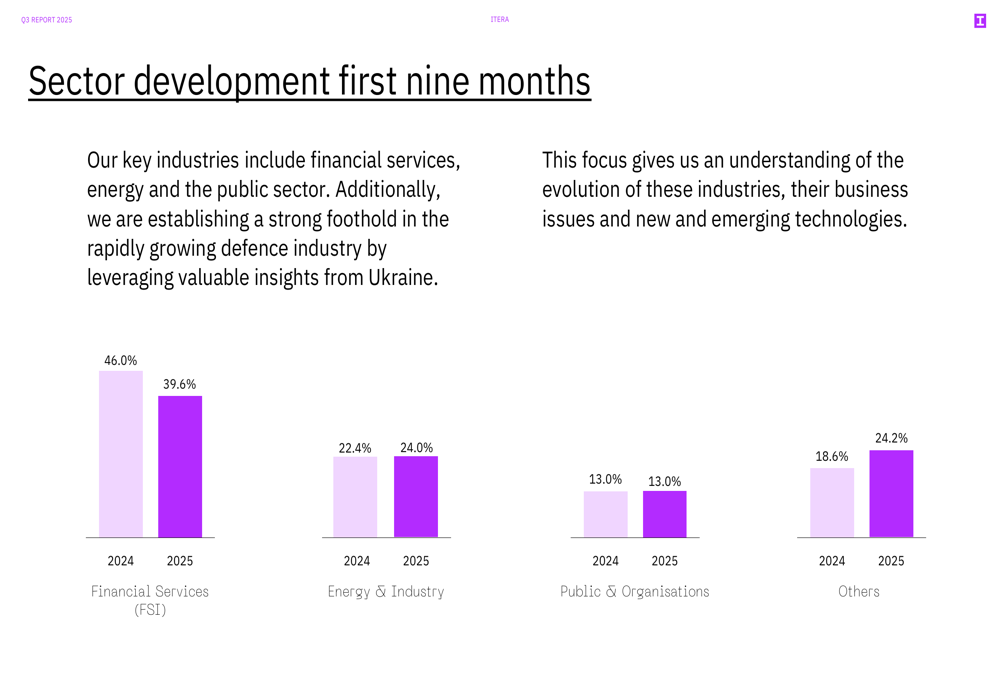

The company’s sector focus has shifted somewhat over the past year, with Financial Services decreasing from 46.0% to 39.6% of revenue, while Energy & Industry increased from 22.4% to 24.0%, and the "Others" category grew from 18.6% to 24.2%. Public & Organizations remained stable at 13.0%.

Detailed Financial Analysis

Itera’s detailed financials show that while Q3 revenue grew by 7%, the company’s operating revenue for the first nine months of 2025 was 630.8M NOK, representing a 1% decline from 636.9M NOK in the same period last year. The EBIT for Q3 2025 was 7.6M NOK (up dramatically from 0.1M NOK), while the 1-9 2025 EBIT was 33.0M NOK, down 19% from 40.5M NOK in the comparable period.

The comprehensive financial overview is presented in this table:

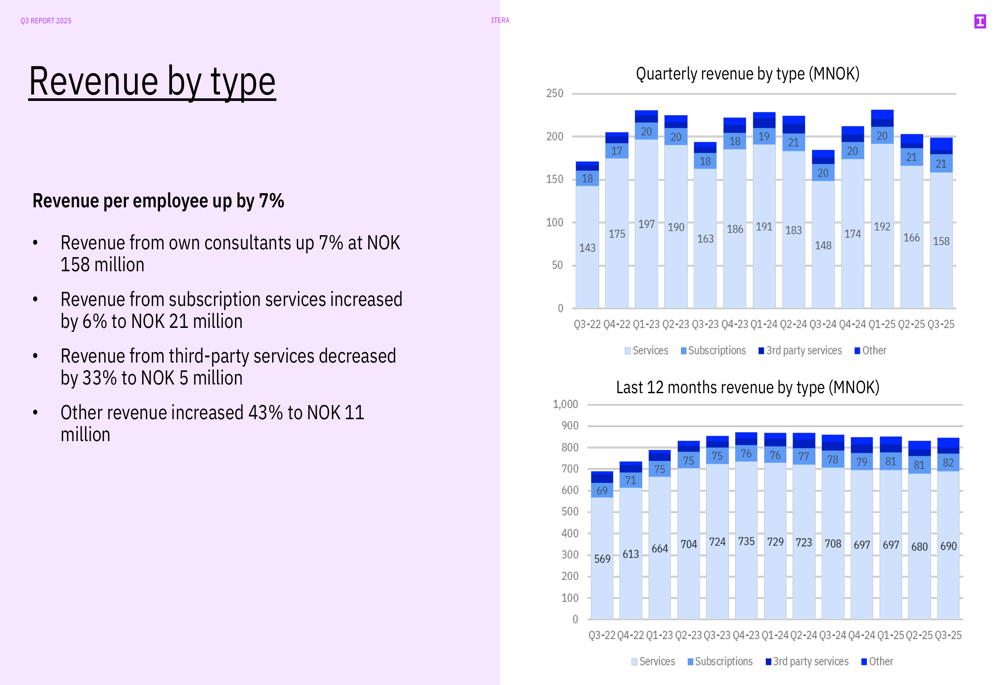

Revenue per employee increased by 7%, with revenue from own consultants up 7% to NOK 158 million and subscription services up 6% to NOK 21 million. However, revenue from third-party services decreased by 33% to NOK 5 million.

The following chart breaks down revenue by type:

Cash flow from operations was negative at MNOK -7.2 in Q3 2025, compared to a positive MNOK 7.0 in Q3 2024. For the last 12 months, operational cash flow reached MNOK 54.1, significantly down from MNOK 85.6 in the previous 12-month period. The company attributes this decline to revenue growth negatively impacting working capital.

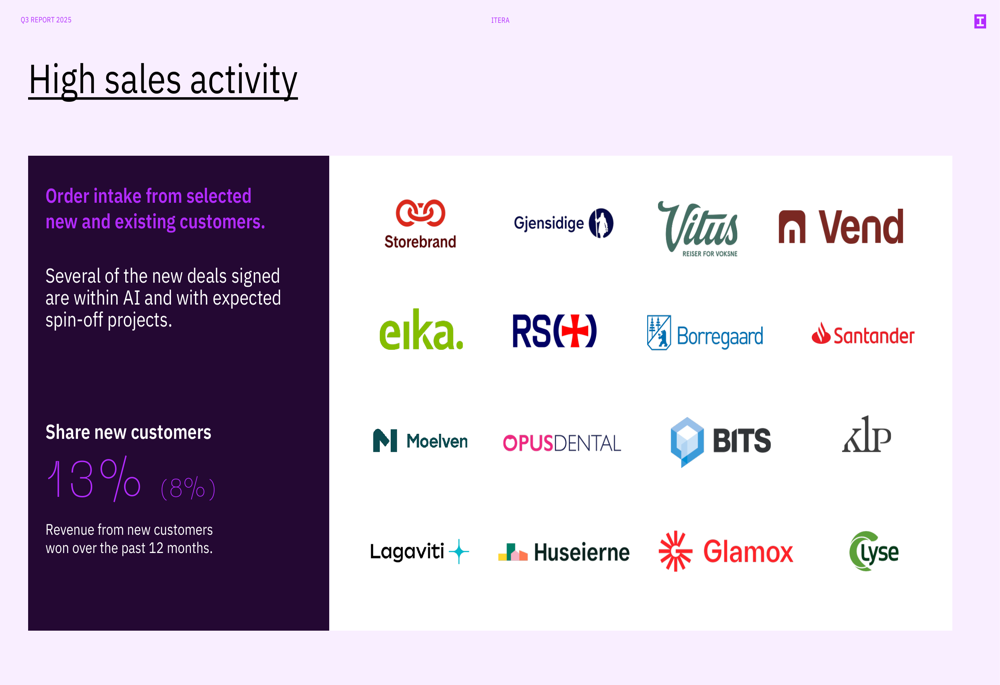

Customer diversification has improved, with the top 30 customers now representing 72% of revenues, down from 80% in the previous year. New customers accounted for 13% of revenue, up from 8% previously.

Forward-Looking Statements

Looking ahead, Itera expects the market for digital transformation to gradually recover. The company is focusing on scaling its cloud transformation capabilities to enable AI opportunities, leveraging its unique position in Ukraine to gain momentum in the defense industry, and pursuing profitable growth and cash flow generation.

The company paid an ordinary dividend of NOK 0.20 for 2024 in June and has announced a supplementary dividend of NOK 0.10 to be paid on December 9, 2025. However, Itera’s share price has declined by 18% (including dividends) over the past year, from NOK 10.95 to NOK 8.58 at the end of September 2025.

Itera maintains a high level of sales activity, with several new deals signed in the AI space that are expected to generate spin-off projects. The company highlighted its customer relationships with notable brands including Storebrand, Gjensidige, Vattenfall, and others.

In its outlook, Itera emphasized that it does not provide specific guidance to the market on future prospects but remains focused on leveraging AI as an expansionary force rather than a deflationary one, positioning the company for long-term growth as digital transformation continues to evolve.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.