Gold is 2025’s best performer. UBS sees more upside

Introduction & Market Context

Jæren Sparebank (OB:JAREN) reported its Q1 2025 results on May 15, showing stable revenue but slightly declining profitability metrics, offset by robust loan and deposit growth that significantly outpaced the broader market. The stock closed at NOK 355 on May 14, up 1.72% ahead of the presentation, reflecting investor confidence in the regional bank’s market position.

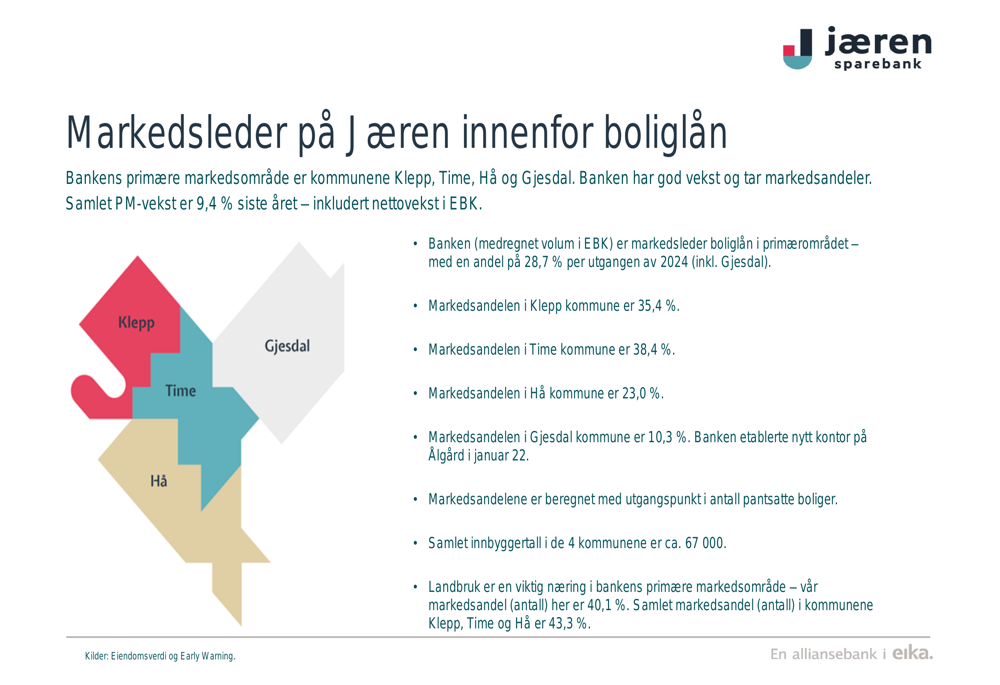

The A- rated bank (Nordic Credit Rating, with positive outlook) continues to strengthen its position as the market leader in mortgage loans across its primary operating region of Jæren, with particularly strong showings in the municipalities of Klepp and Time.

Quarterly Performance Highlights

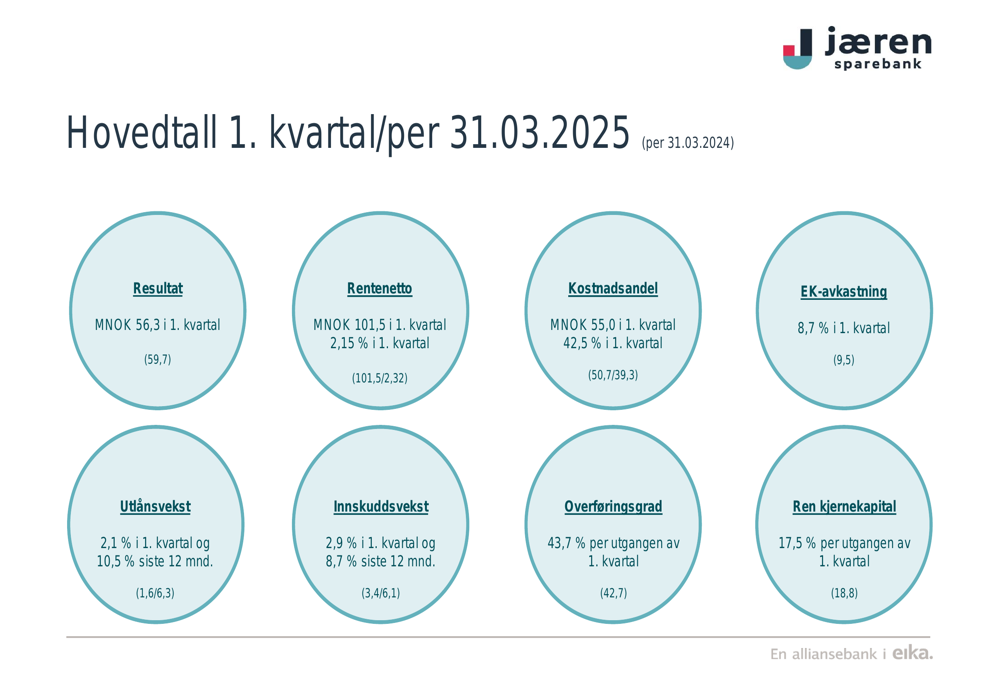

Jæren Sparebank reported a Q1 2025 profit of NOK 56.3 million, down from NOK 59.7 million in Q1 2024. Net interest income remained flat year-over-year at NOK 101.5 million, though it declined as a percentage of capital from 2.32% to 2.15%. The cost-to-income ratio increased to 42.5% from 39.3% a year earlier, while return on equity decreased to 8.7% from 9.5%.

As shown in the following comprehensive overview of key financial metrics:

Despite the slight decline in profitability metrics, the bank delivered impressive growth figures. Loan growth reached 2.1% for the quarter and 10.5% year-over-year, significantly outpacing the 1.6% quarterly and 6.3% annual growth rates from Q1 2024. Similarly, deposit growth was robust at 2.9% for the quarter and 8.7% year-over-year, compared to 3.4% and 6.1% respectively in Q1 2024.

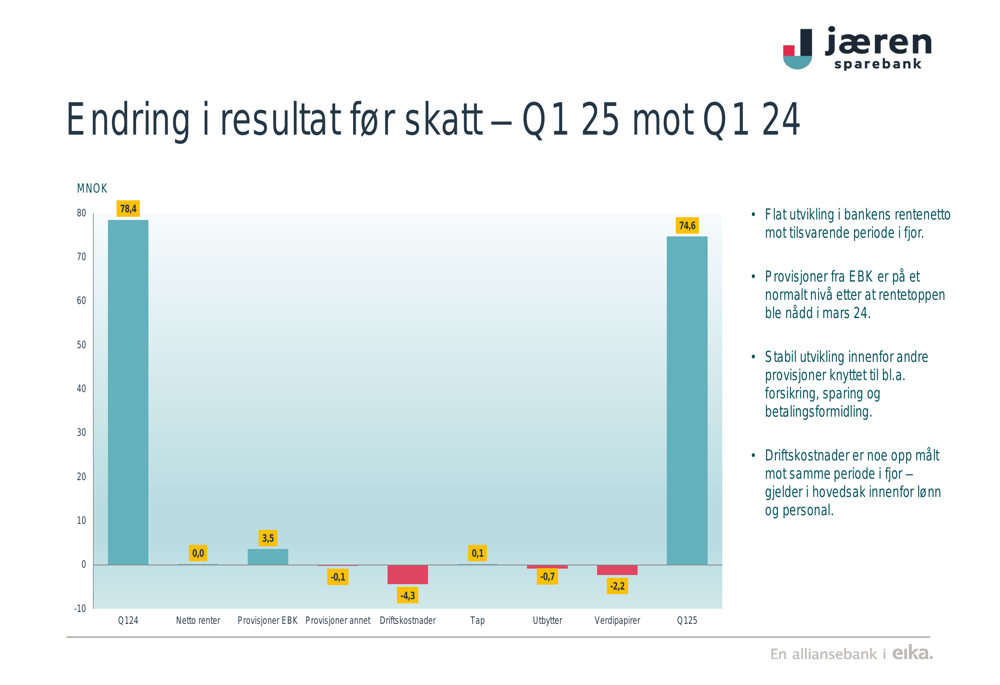

The bank’s presentation highlighted the factors contributing to the year-over-year change in profit before tax:

Market Position and Growth

Jæren Sparebank continues to strengthen its position as the market leader in mortgage loans across its primary operating region. The bank holds a 28.7% market share in mortgage loans across Klepp, Time, Hå, and Gjesdal municipalities, with particularly strong positions in Klepp (35.4%) and Time (38.4%).

The following map illustrates the bank’s market penetration across its core geographic area:

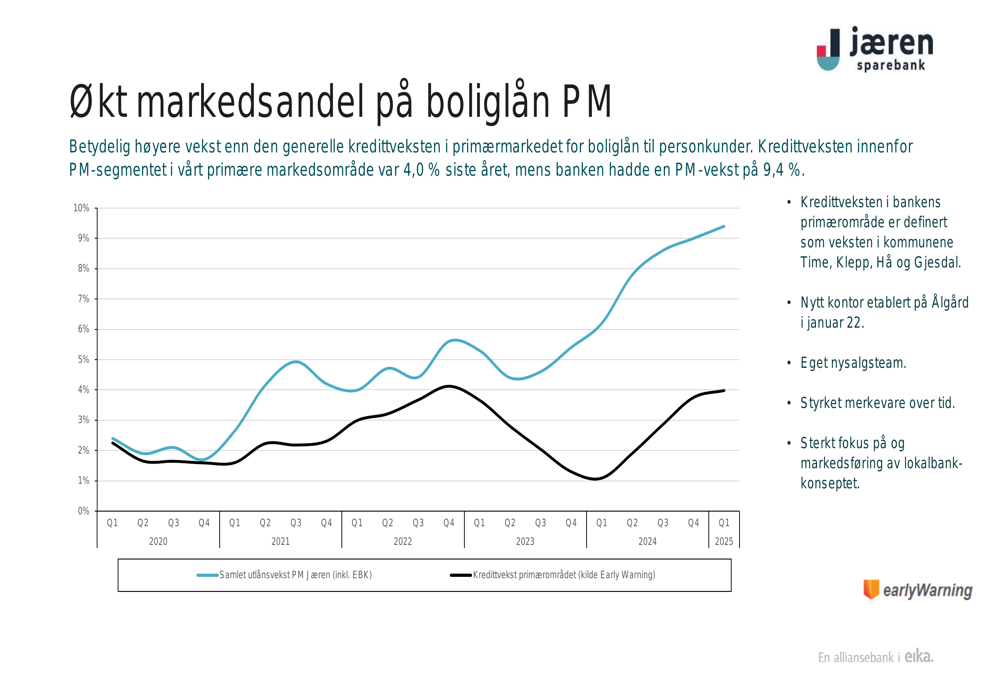

The bank’s personal market (PM) loan growth of 9.4% over the last year significantly outpaced the general credit growth of 4.0% in its primary market. This growth has been supported by the bank’s strategic expansion, including the opening of a new office in Ålgård (Gjesdal) in January 2022 and the creation of a dedicated sales team.

As demonstrated in this chart showing the bank’s consistent outperformance of market credit growth:

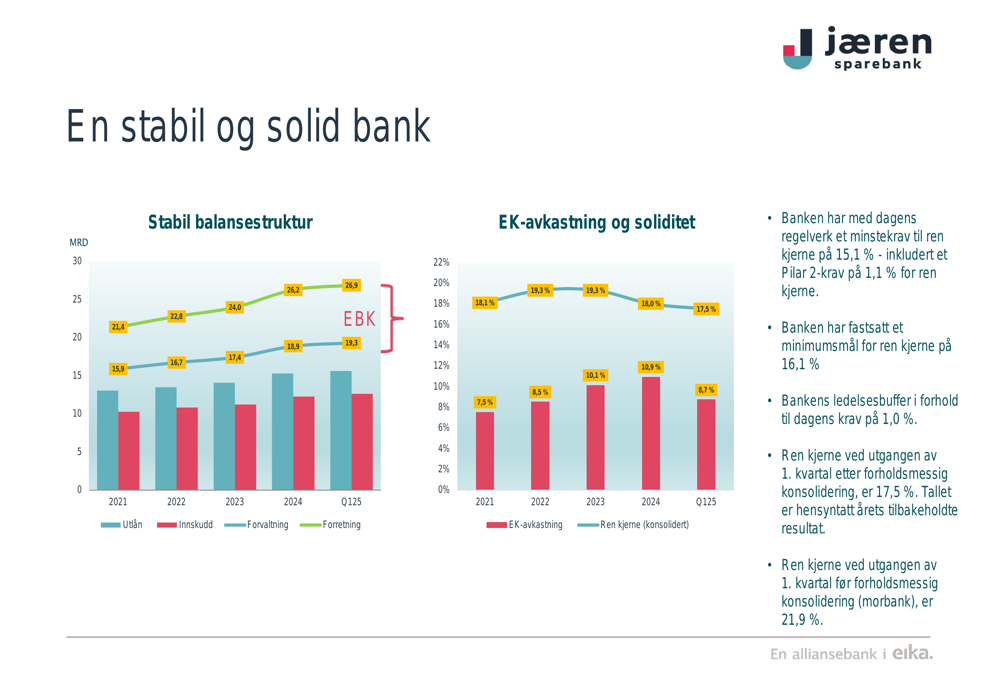

Balance Sheet and Capital Position

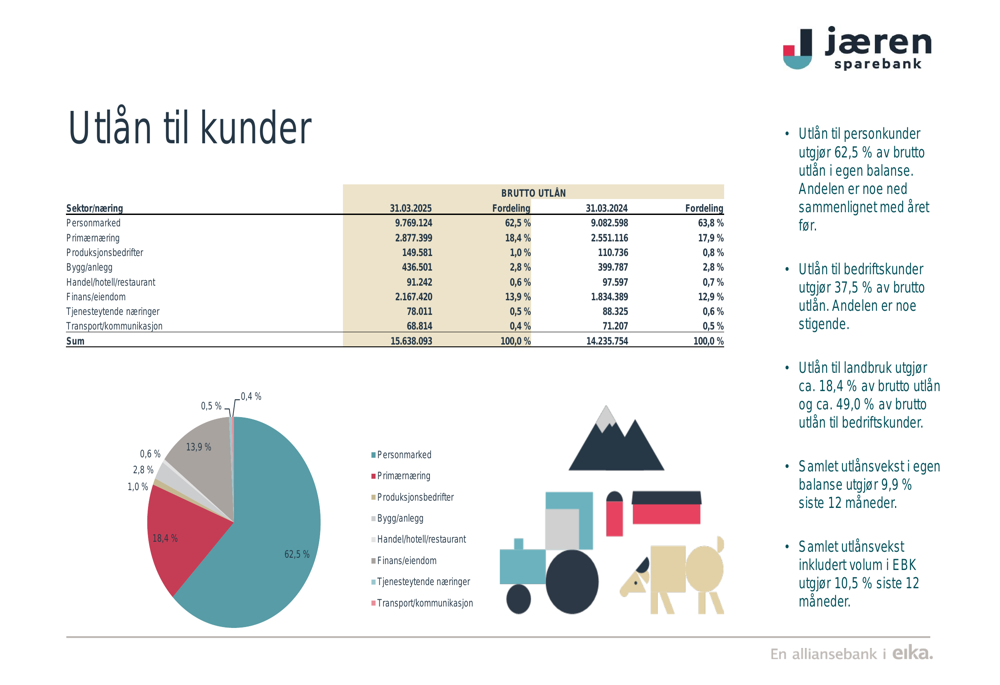

Jæren Sparebank maintains a well-structured loan portfolio with 63% of loans to personal customers and 37% to business customers, of which 86% is concentrated in agriculture and real estate sectors. The bank’s strong position in the agricultural sector is reflected in its 40.1% market share in this segment.

The distribution of the loan portfolio is illustrated in the following breakdown:

The bank’s deposit coverage ratio improved slightly to 80.6% at the end of Q1 2025, well above its target minimum of 70%. Personal market customers account for 69.5% of total deposits, with deposit growth in this segment reaching 6.7% over the past 12 months.

Capital adequacy remains solid with a core capital ratio of 17.5% after proportional consolidation, though this represents a decrease from 18.8% in Q1 2024. This level remains comfortably above both the regulatory minimum requirement of 15.1% and the bank’s internal minimum target of 16.1%.

As shown in this detailed breakdown of the bank’s capital position:

Asset quality remains strong, with problem loans at a very low level of 0.45% of gross loans including EBK volume, down from 0.50% at the end of Q4 2024. The bank notes that this level is "very low compared to most other banks."

Strategic Outlook

Looking ahead to its 2025-2027 strategic period, Jæren Sparebank highlighted several key initiatives. The conversion to a new core banking solution is expected to deliver annual IT savings of approximately NOK 10-11 million. The bank has also raised its minimum ROE target from 10% to 11% for this strategic period.

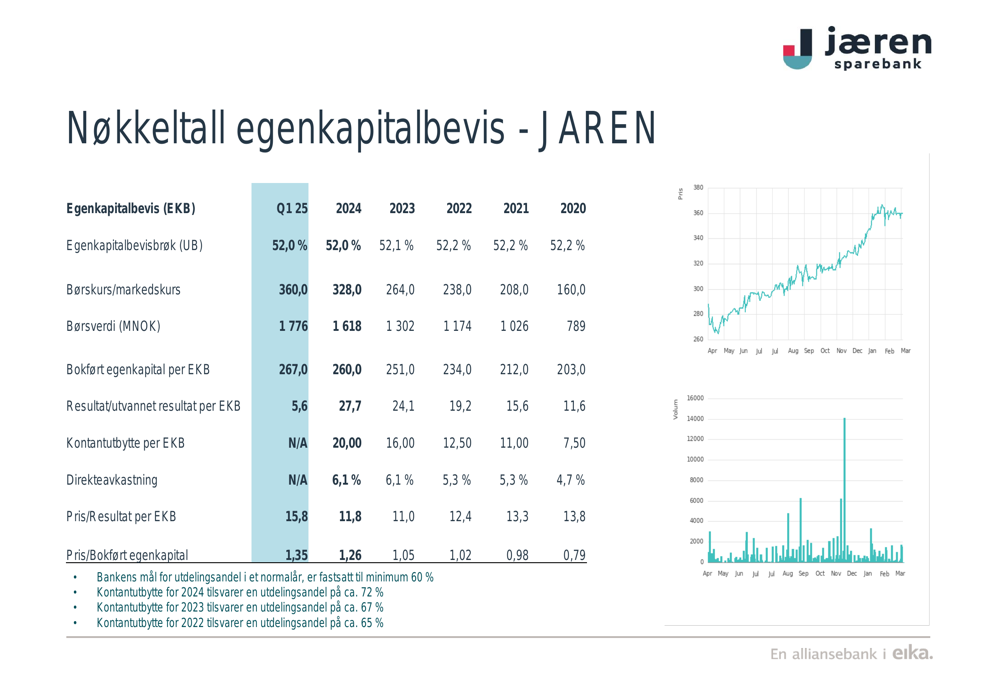

The bank’s equity certificate data reveals a dividend payout ratio of approximately 72% for 2024, exceeding its target minimum of 60% for a normal year:

Management emphasized that the bank continues to gain market share, with growth significantly outpacing credit growth in its primary market area. This growth strategy, combined with operational efficiencies from its new banking platform, forms the foundation of the bank’s approach to maintaining profitability despite margin pressures in a stable interest rate environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.