BofA lifts gold target to $5,000/oz, sees silver staying in deficit

Introduction & Market Context

JINS Holdings Inc. (TYO:3046), the Japanese eyewear retailer, presented its financial results for the fiscal year ended August 2025 on October 10, revealing record-high sales and profits that significantly exceeded company forecasts. The company’s stock closed at 8,490 yen on the presentation day, down slightly by 0.12%.

The strong performance comes amid JINS’s continued expansion in both domestic and international markets, with particular success in Japan and Taiwan offsetting challenges in other regions. The company also outlined ambitious plans for FY8/26, including strategic investments in flagship stores and system upgrades to support its global growth strategy.

Executive Summary

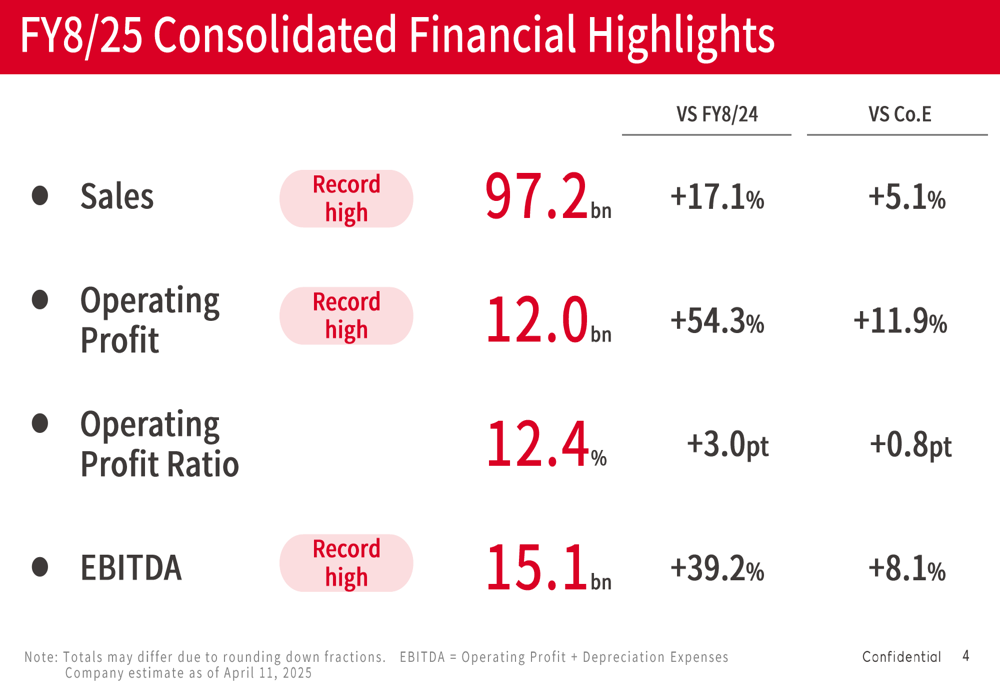

JINS Holdings achieved exceptional financial results for FY8/25, with consolidated sales reaching 97.2 billion yen, up 17.1% year-over-year and exceeding the company’s forecast by 5.1%. Operating profit surged by 54.3% to 12.0 billion yen, 11.9% above the company’s estimate.

As shown in the following consolidated financial highlights, the company’s operating profit ratio improved by 3.0 percentage points to 12.4%, while EBITDA increased by 39.2% to 15.1 billion yen:

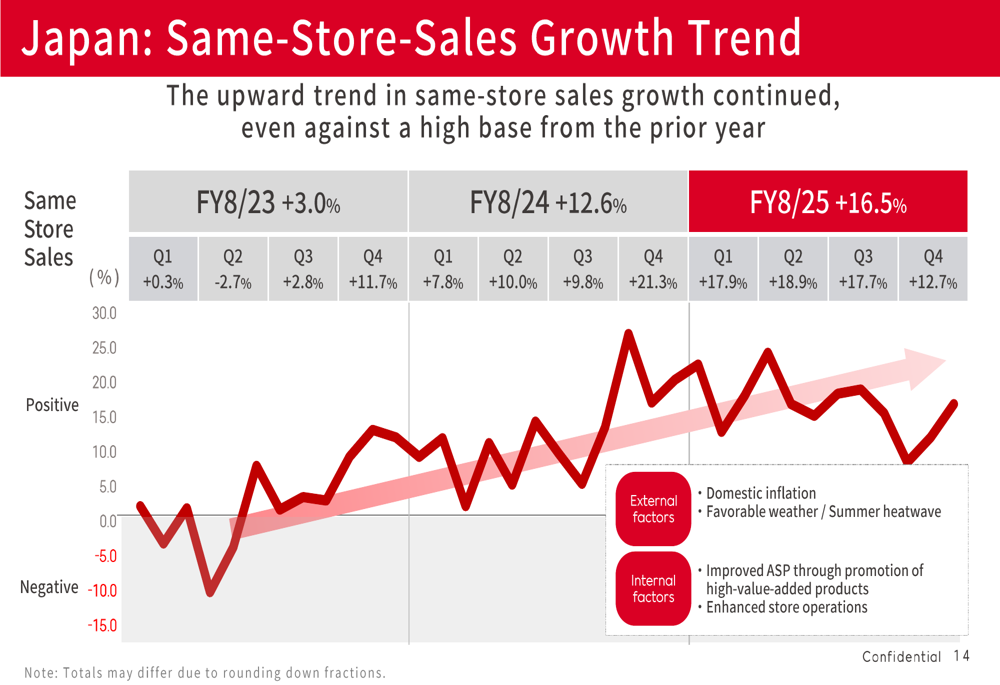

The strong performance was driven by sustained high same-store sales growth of 16.5% in Japan, coupled with improved profitability in overseas operations, particularly in Taiwan and China. The company also expanded its global footprint, increasing its total store count from 736 to 789 locations.

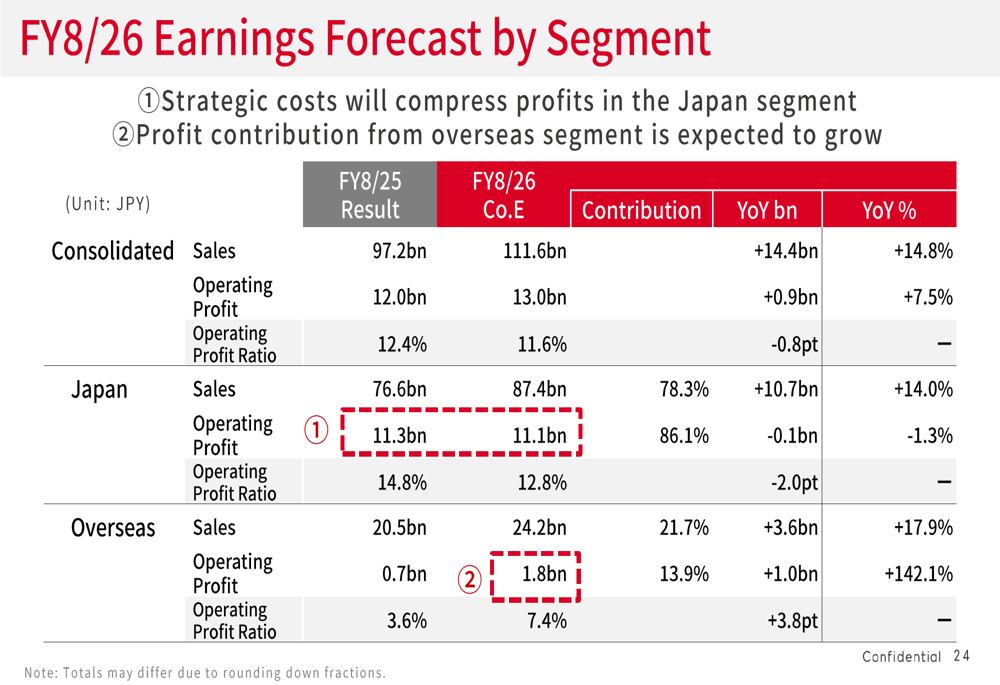

For FY8/26, JINS forecasts continued growth with sales projected to reach 111.6 billion yen (+14.8%) and operating profit expected to increase to 13.0 billion yen (+7.5%), although the operating profit margin is anticipated to contract slightly to 11.6% due to strategic investments.

Detailed Financial Analysis

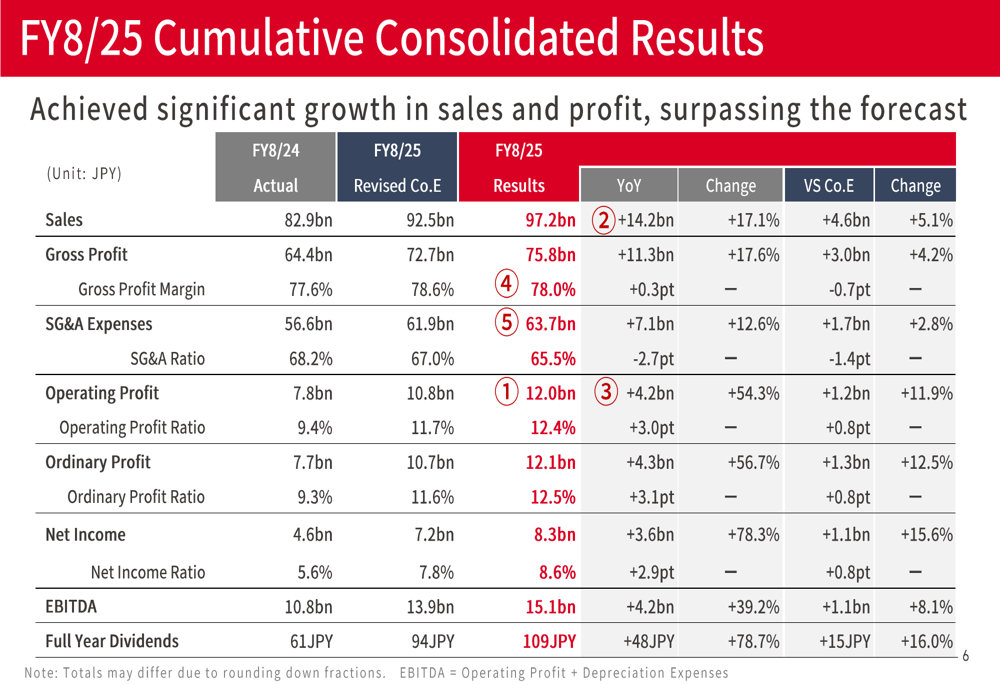

The company’s FY8/25 consolidated results show impressive growth across all key financial metrics. Gross profit increased by 17.6% to 75.8 billion yen, with the gross profit margin improving from 77.6% to 78.0%. Despite a 12.6% increase in SG&A expenses to 63.7 billion yen, the SG&A ratio decreased from 68.2% to 65.5%, contributing to the substantial improvement in operating profit.

The detailed consolidated results table below highlights the company’s strong financial performance:

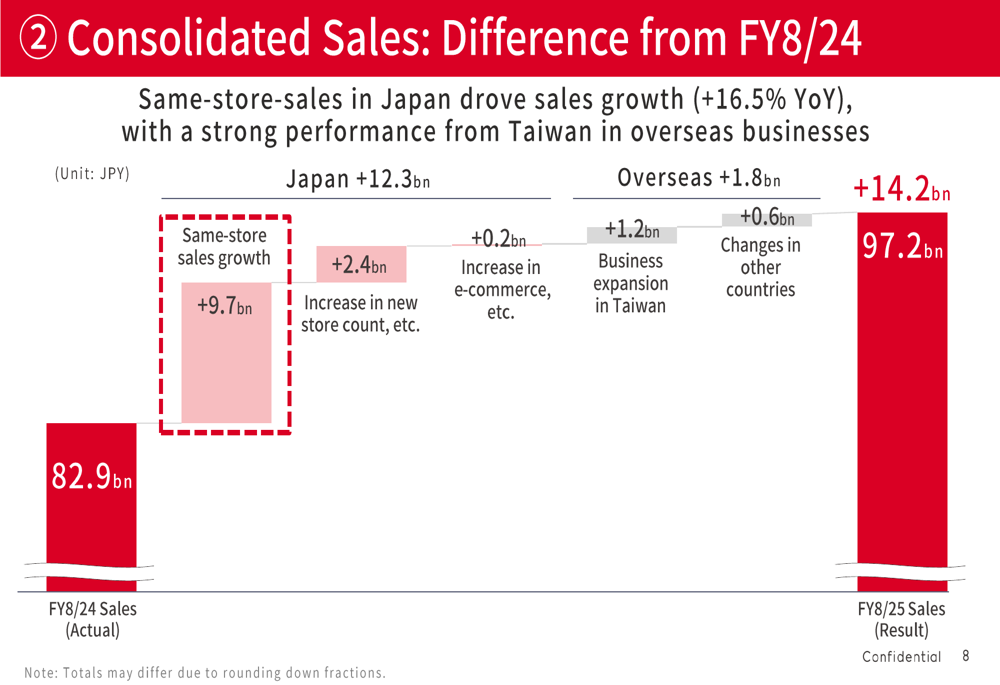

Breaking down the sales growth of 14.2 billion yen compared to FY8/24, the largest contributor was same-store sales growth in Japan (+9.7 billion yen), followed by new store openings (+2.4 billion yen) and business expansion in Taiwan (+1.2 billion yen):

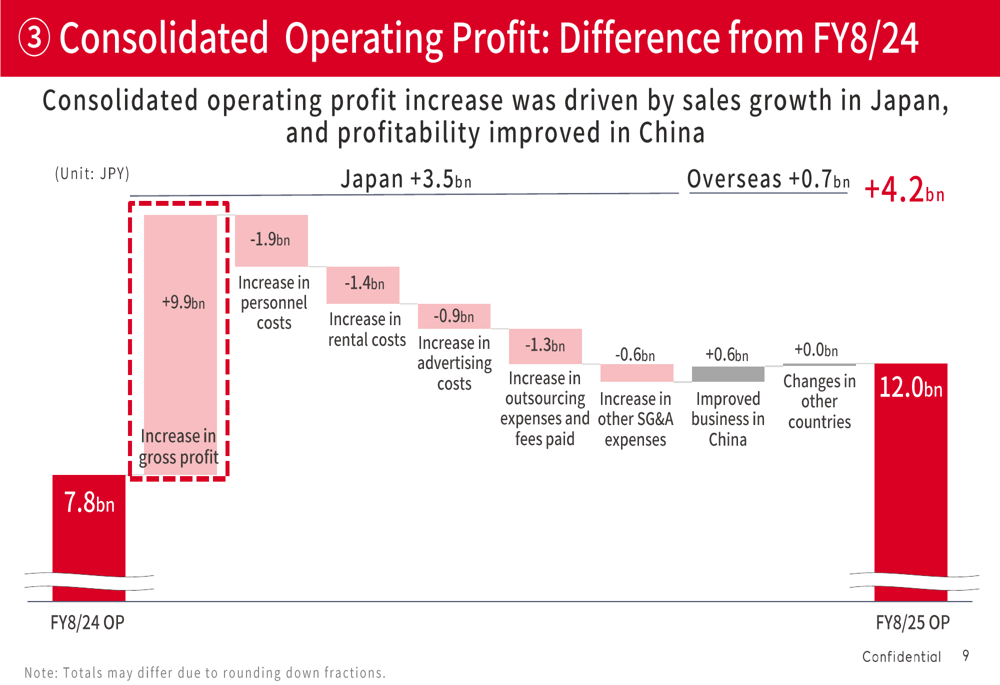

Similarly, the 4.2 billion yen increase in operating profit was primarily driven by gross profit growth (+9.9 billion yen), partially offset by increases in personnel costs (-1.9 billion yen), rental costs (-1.4 billion yen), and other SG&A expenses. The company’s operations in China contributed 0.6 billion yen to the profit improvement:

JINS maintained strong inventory management throughout the year, with the inventory-to-monthly-sales ratio decreasing to 0.64 by the end of FY8/25, reflecting efficient operations despite the business expansion.

Segment Performance

Japan remained the primary driver of JINS’s performance, with sales increasing by 19.2% to 76.6 billion yen and operating profit surging by 46.8% to 11.3 billion yen. The segment’s operating profit margin improved to 14.8%, up from 12.1% in the previous year.

The strong performance in Japan was underpinned by consistent same-store sales growth, which reached 16.5% for the full year. As illustrated in the following chart, this growth continued even against the high base from the prior year:

The overseas segment also showed significant improvement, with sales increasing by 9.9% to 20.5 billion yen and operating profit reaching 0.7 billion yen, compared to near-breakeven in the previous year. Taiwan was a standout performer, contributing significantly to both sales and profit growth, while China achieved profitability following restructuring efforts.

The following chart shows the earnings forecast by segment for FY8/26, highlighting the expected growth in overseas profit contribution:

JINS expanded its store network to 789 locations by the end of FY8/25, with 540 stores in Japan and 249 overseas. The company accelerated store openings in Japan, achieving a net increase of 45 stores against a forecast of 31, while also expanding its presence in Taiwan from 61 to 78 stores.

Strategic Initiatives & Outlook

Looking ahead to FY8/26, JINS plans to continue its growth trajectory with sales projected to increase by 14.8% to 111.6 billion yen and operating profit expected to rise by 7.5% to 13.0 billion yen. However, the company anticipates a slight contraction in the operating profit margin to 11.6% due to strategic investments.

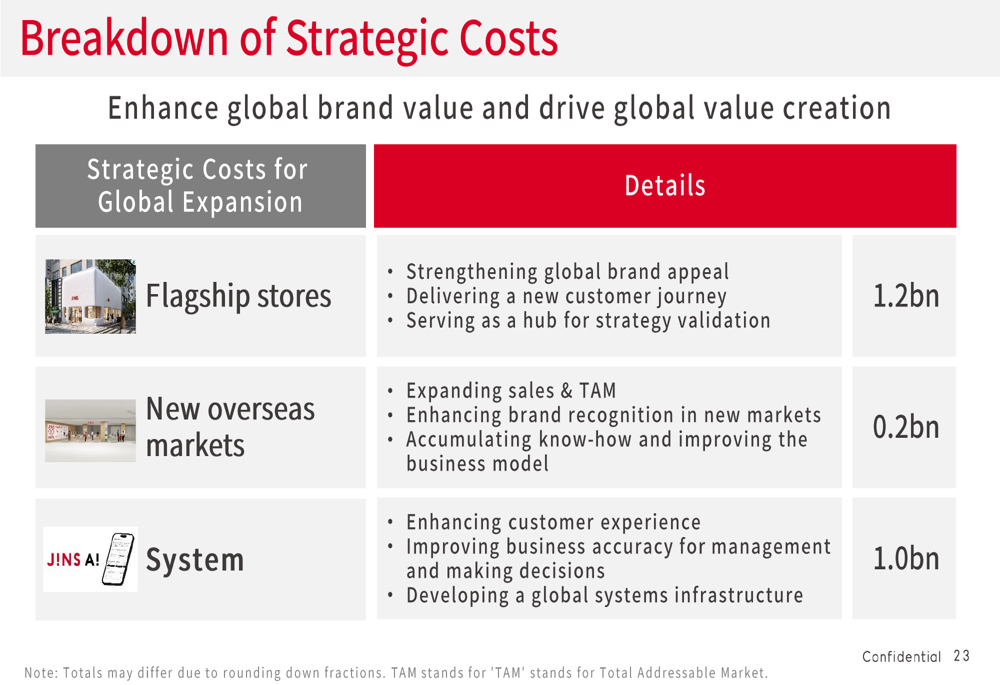

The company has outlined significant strategic costs totaling 2.4 billion yen for FY8/26, focused on global expansion initiatives. As shown in the breakdown below, these investments include flagship stores (1.2 billion yen), new overseas markets (0.2 billion yen), and system upgrades (1.0 billion yen):

JINS plans to accelerate store openings in FY8/26, targeting a net increase of over 90 stores to reach 882 locations globally. This expansion will be particularly focused on Japan and Taiwan, while the strategy for China involves closing underperforming stores and opening new ones in strategic areas.

The company also aims to improve its gross profit margin to 79.3% in FY8/26 by increasing the average selling price (ASP) and implementing strict inventory management. In Japan, the ASP is projected to increase from 12,039 yen to 13,058 yen, driven by the promotion of high-value-added products.

JINS will maintain its shareholder return policy with a dividend payout ratio of approximately 30%, resulting in a forecast dividend of 115 yen per share for FY8/26, up from 109 yen in FY8/25.

In summary, JINS Holdings delivered exceptional results in FY8/25 and has set ambitious targets for FY8/26 as it continues to strengthen its domestic business while expanding its global footprint. The company’s strategic investments in flagship stores and system upgrades are expected to support long-term growth, albeit with a temporary impact on profit margins in the coming year.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.