FINAL HOURS: Lock in your InvestingPro subscription for 50% off before sale ends

Introduction & Market Context

John B. Sanfilippo & Son, Inc. (NASDAQ:JBSS), one of the largest nut processors and snack bar manufacturers in the world, recently presented its fiscal year 2024 investor update, highlighting long-term financial strength and strategic initiatives. While the presentation showcased the company’s historical growth trajectory, recent earnings results for Q3 2025 reveal emerging challenges, with net sales declining 4% to $260.9 million despite a 50% increase in earnings per share.

The company’s stock has experienced significant volatility, trading at $63.18 as of June 2025, down from the FY24 average daily price of $101.65 mentioned in the presentation. This decline reflects investor concerns about sales volume and market conditions, despite JBSS’s strong financial foundation and strategic positioning.

Financial Performance Highlights

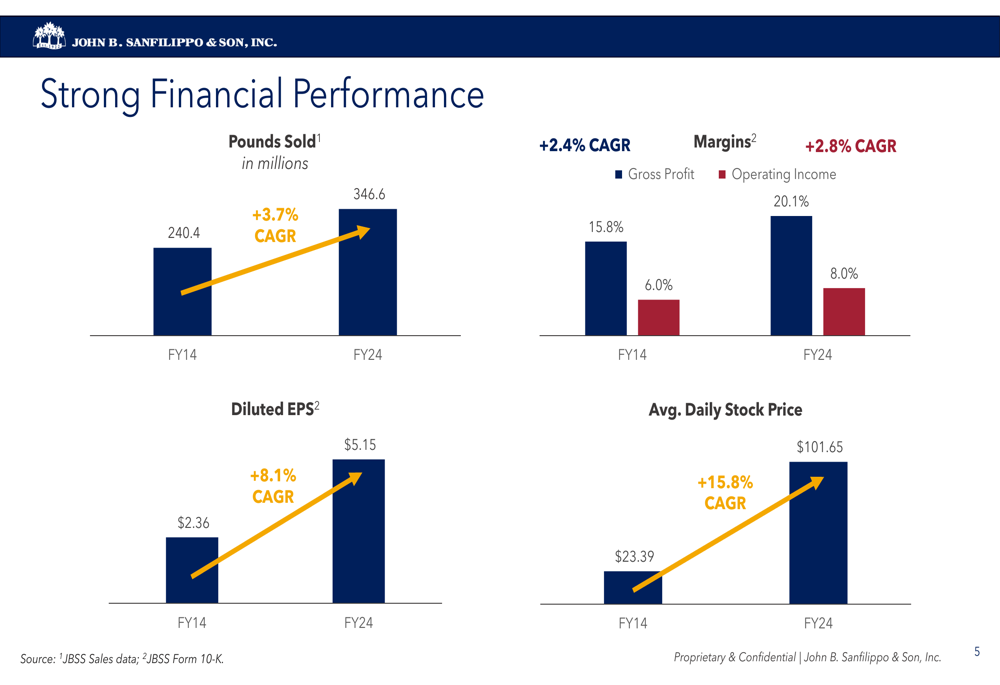

JBSS reported FY24 net sales of approximately $1.07 billion, maintaining a decade-long growth trajectory. The company has demonstrated consistent improvement in key financial metrics since FY14, with gross profit margin expanding from 15.8% to 20.1% and operating income margin increasing from 6.0% to 8.0% (representing a CAGR of +2.8%).

As shown in the following chart of financial performance metrics, diluted EPS grew from $2.36 in FY14 to $5.15 in FY24, achieving a CAGR of +8.1%:

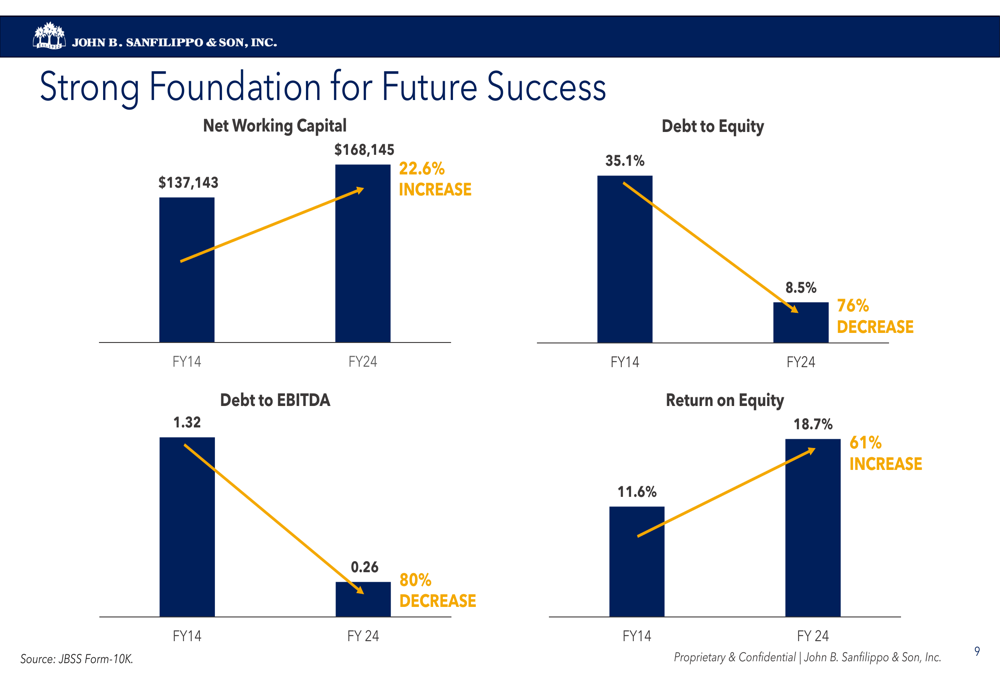

The company has maintained a strong financial foundation while returning cash to shareholders through regular and special dividends. In calendar year 2024, JBSS paid a regular dividend of $0.85 per share and a special dividend of $2.25 per share, representing a yield of 3.1%. This dividend policy has been supported by decreasing debt ratios, with debt-to-equity falling from 35.1% in FY14 to 8.5% in FY24 and debt-to-EBITDA decreasing from 1.32 to 0.26 over the same period.

The following chart illustrates the company’s improving financial ratios:

Despite these positive long-term trends, recent results from Q3 2025 indicate emerging challenges. While EPS increased by 50% to $1.72 per diluted share, net sales decreased by 4% and sales volume declined by 7.9% compared to the previous year. This divergence suggests effective cost management but potential headwinds in market demand.

Strategic Initiatives

A cornerstone of JBSS’s strategy has been its shift toward consumer channels, which now represent 82% of total net sales, up from 58% in FY14. This transformation has been accompanied by reduced reliance on commercial ingredients (down from 25% to 10%) and contract packaging (from 13% to 8%).

In September 2023, JBSS completed a strategic acquisition of a manufacturing facility in Lakeville, Minnesota, for approximately $59 million. This acquisition, which contributed approximately $120 million in net sales during FY24, accelerated the company’s product diversification strategy and enhanced its capabilities in the snack bar category.

The company’s mission and strategic focus are illustrated in the following framework:

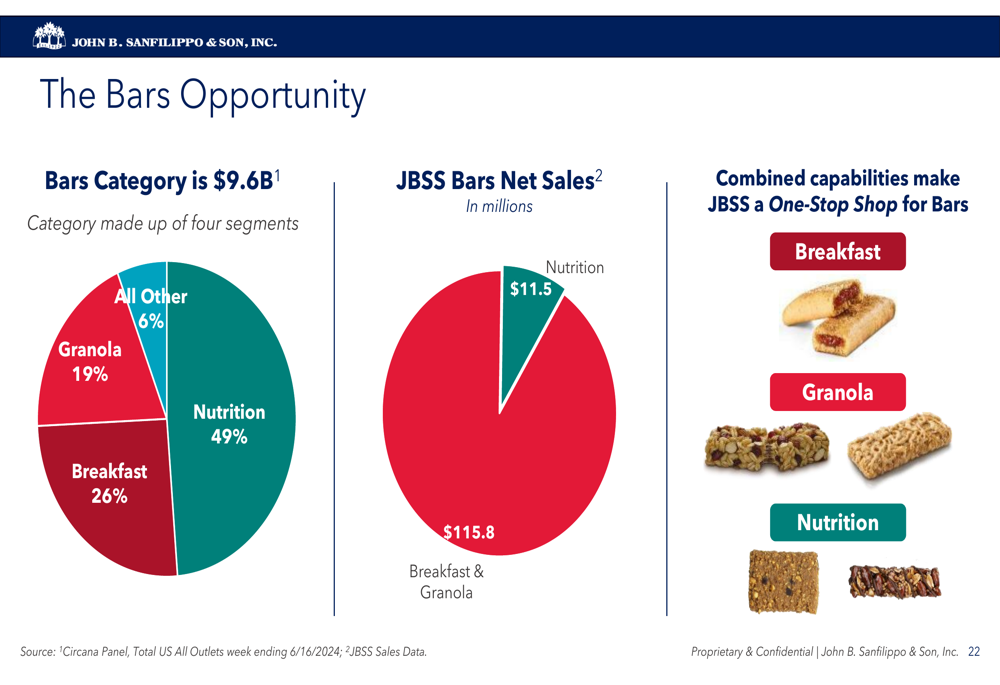

The bars category represents a significant growth opportunity for JBSS, with the total market valued at $9.6 billion. The company’s combined capabilities now position it as a one-stop shop for bars across multiple segments:

JBSS’s consumer channel, which generated $872 million in net sales (an 11% increase versus FY23), has been driven by private label growth in snack nuts, trail mixes, and bars, as well as expansion in e-commerce and club channels. However, the commercial ingredients channel ($110 million, -10% versus FY23) and contract manufacturing ($84 million, -8% versus FY23) faced challenges due to competitive pricing pressures and canceled product launches.

Competitive Industry Position

JBSS maintains a dual consumer strategy, offering both branded nut and dried fruit programs (Fisher, Orchard Valley Harvest, Squirrel Brand, and Southern Style Nuts) and private label products. The company’s brand portfolio is led by Fisher (59% of branded sales), followed by Orchard Valley Harvest (27%) and other brands (14%).

The retail nut category has faced challenges, with category pound sales decreasing from 1,109 million pounds in FY20 to 1,047 million pounds in FY24. However, price per pound has increased from $6.14 to $6.48 over the same period, partially offsetting volume declines.

Private label products significantly over-index in the snack nuts and trail mix category, with a 47.2% dollar share compared to 19.8% for total edible food. This positions JBSS favorably given its strength in private label manufacturing. Conversely, private label bars currently under-index at 7.0% but have been growing, presenting an opportunity that aligns with the company’s recent acquisition and strategic focus.

Forward Outlook

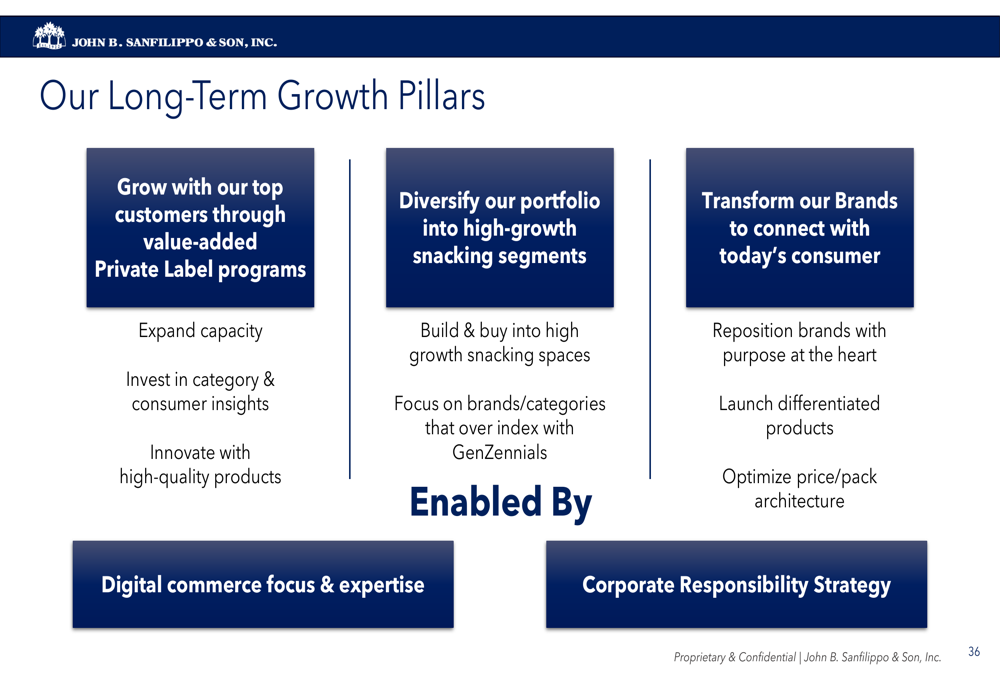

Looking ahead, JBSS has outlined three key growth pillars that will guide its long-term strategy:

The company remains focused on adapting to macroeconomic challenges, with plans to adjust prices in response to potential commodity price stabilization. Strategic investments, including a $90 million commitment to production equipment by fiscal 2026 (as mentioned in the Q3 2025 earnings call), are expected to enhance operational efficiency and support growth in key product categories.

CEO Jeffrey Sanfilippo emphasized the importance of agility and adaptation during the recent earnings call, stating, "Maintaining agility and swiftly adapting to the dynamic external environment is imperative to our business." He also highlighted the company’s commitment to growth, saying, "We have the right strategies, talent, and commitment to quality and service to continue to grow."

Conclusion

John B. Sanfilippo & Son presents a mixed picture of long-term financial strength and strategic positioning against near-term market challenges. The company’s decade-long improvements in margins, earnings per share, and financial ratios provide a solid foundation, while its strategic shift toward consumer channels and diversification into snack bars positions it for future growth.

However, recent sales volume declines and stock price pressure indicate that JBSS faces headwinds in the current market environment. The company’s ability to navigate commodity price fluctuations, competitive pressures, and changing consumer preferences will be critical to bridging the gap between its long-term strategic vision and near-term performance.

Investors should monitor the company’s progress in leveraging its Lakeville acquisition, expanding its private label bar business, and maintaining cost discipline as key indicators of future performance. With a dividend yield of 4.68% and trading near its 52-week low, JBSS may present value for investors who believe in the company’s long-term strategic direction despite current challenges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.