TSX slides as gold price drops

Executive Summary

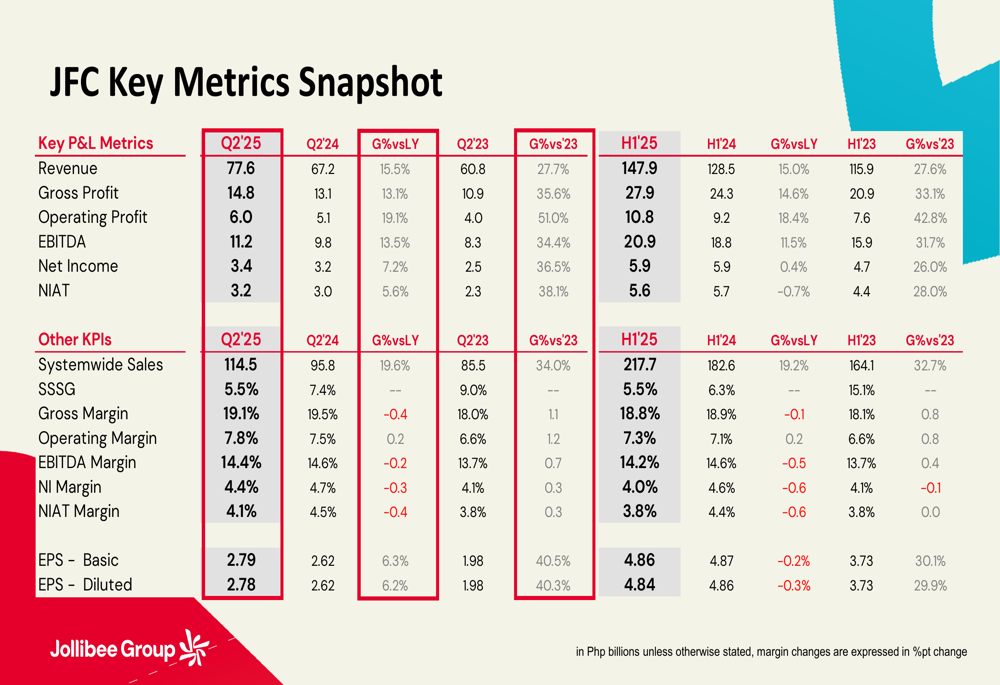

Jollibee Foods Corporation (JFC) reported strong financial results in its Q2 2025 earnings presentation, with system-wide sales increasing by 19.6% year-over-year to Php114.5 billion. The company’s revenue rose 15.5% to Php77.6 billion, while net income after tax grew 5.6% to Php3.2 billion.

The impressive performance was driven by robust international expansion, particularly in the Europe, Middle East, Africa, and Asia (EMEAA) region, which saw 20.2% system-wide sales growth. The company’s Coffee and Tea segment, now representing over 52% of JFC’s global network footprint, delivered exceptional results with a 76.8% increase in EBITDA.

JFC maintained its strong position in the Philippines market while continuing to gain traction in international markets, with the company’s flagship Jollibee brand outperforming global competitors in topline growth metrics.

Quarterly Performance Highlights

Jollibee’s Q2 2025 results demonstrated continued momentum across key performance indicators. The company achieved 5.5% same-store sales growth, with transaction count up 2.8% and average check increasing 2.7%.

As shown in the following comprehensive snapshot of key financial metrics:

The company’s operating profit grew by 19.1% to Php6.0 billion, representing a 7.8% margin. EBITDA increased by 13.5% to Php11.2 billion, while gross profit rose 13.1% to Php14.8 billion with a 19.1% margin.

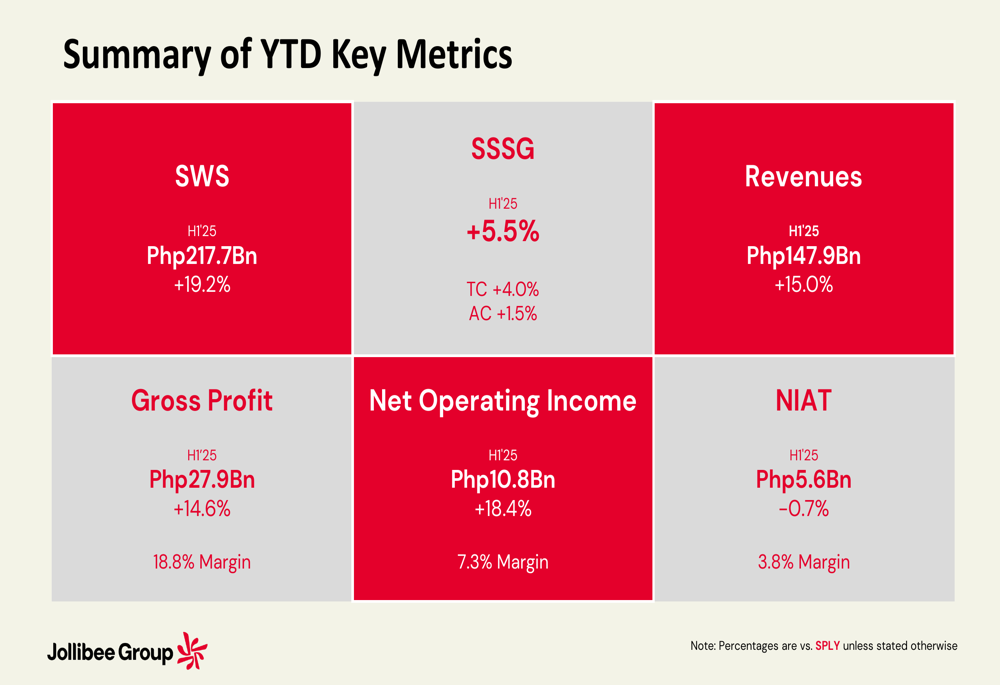

Year-to-date performance also remained strong, as illustrated in this summary:

Store expansion continued at a rapid pace, with the total store count reaching 10,119, a 45.5% increase from the previous year. During the quarter, JFC opened 531 new stores while closing 178 underperforming locations.

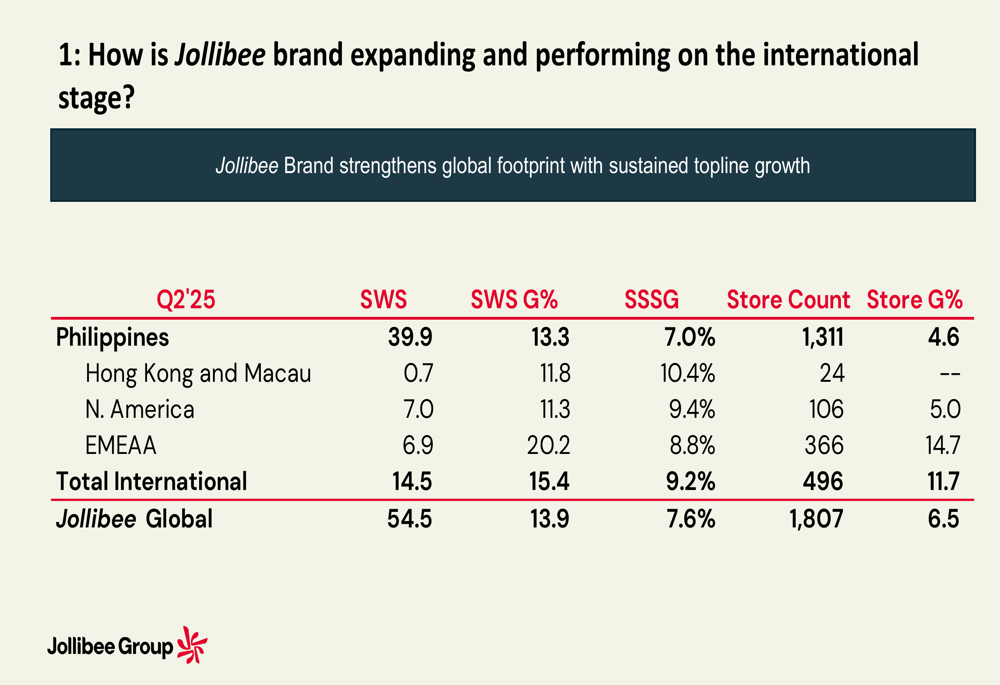

International Expansion

The Jollibee brand’s international expansion has been a key growth driver, with the company strengthening its global footprint through sustained topline growth across all regions. The brand achieved 15.4% system-wide sales growth internationally, with particularly strong performance in EMEAA (20.2%) and Hong Kong and Macau (11.8%).

The following data highlights Jollibee’s international expansion metrics:

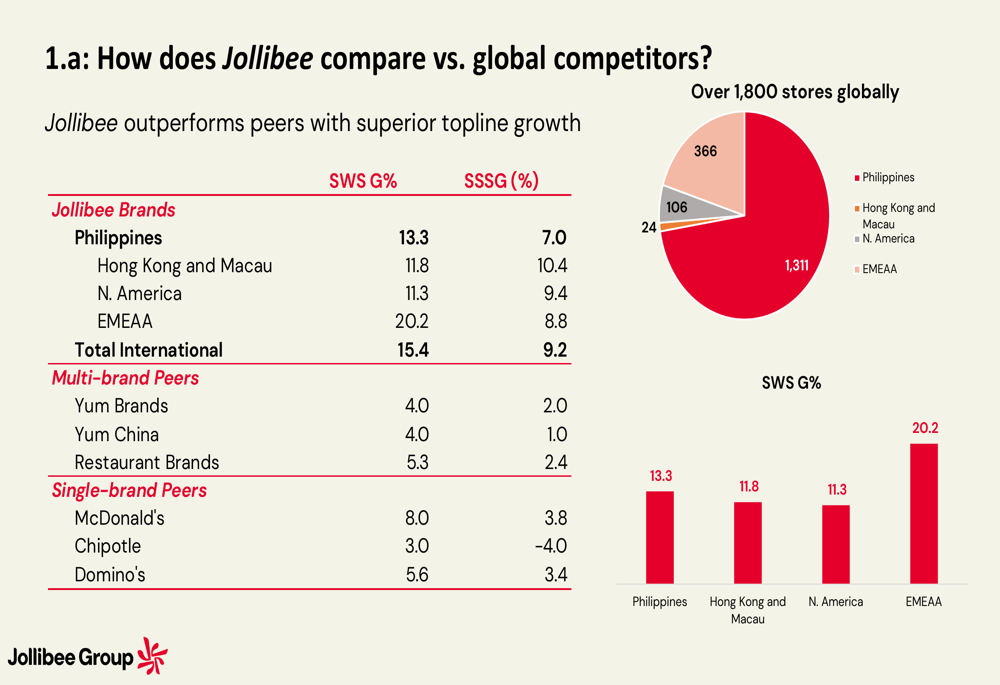

Notably, Jollibee has outperformed major global competitors in both system-wide sales growth and same-store sales growth. While competitors like McDonald’s, Yum Brands, and Restaurant Brands International posted single-digit growth, Jollibee delivered double-digit increases across most regions.

As shown in this comparative analysis against global competitors:

In North America, Jollibee’s Chickenjoy was recognized as the "#1 Best Fast-Food Fried Chicken" by USA TODAY for the second consecutive year. The region has maintained a 54-month streak of sustained same-store sales growth, with consistent above-industry average daily sales in both Canada (~USD 16,400) and the US (~USD 14,000).

The company is also making significant inroads in Vietnam, where it holds the #1 position in market share, revenue, and net income despite being third in store network size behind Lotteria and KFC.

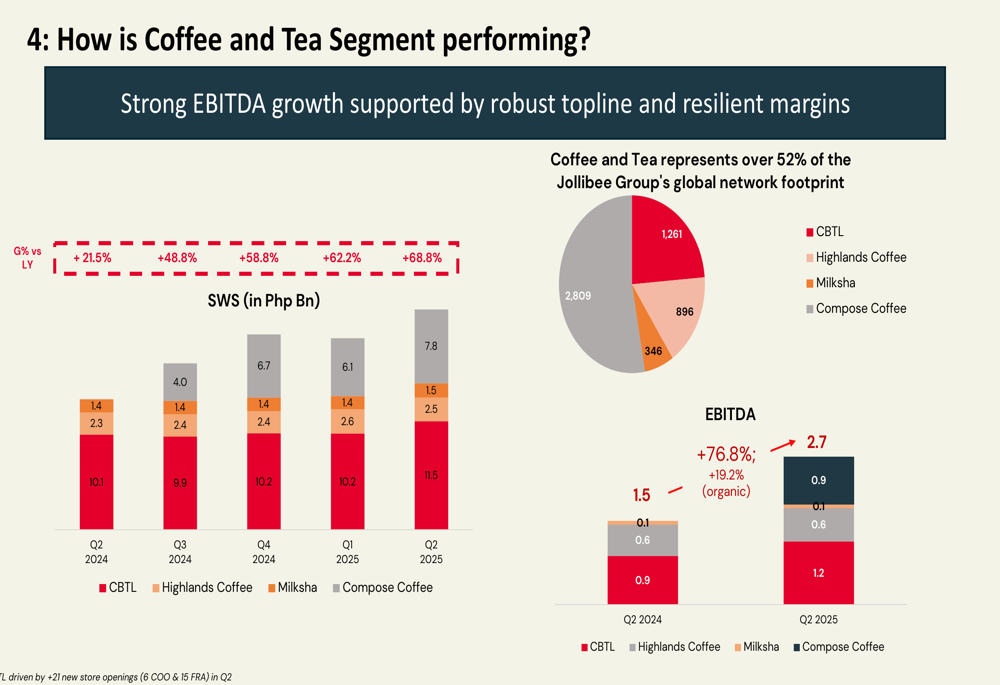

Coffee and Tea Segment Performance

The Coffee and Tea segment has emerged as a major growth driver for JFC, now representing over 52% of the company’s global network footprint. This segment includes brands like The Coffee Bean & Tea Leaf (CBTL), Highlands Coffee, Milksha, and Compose Coffee.

The segment delivered exceptional performance in Q2 2025, as illustrated in this detailed breakdown:

EBITDA for the Coffee and Tea segment grew by an impressive 76.8% year-over-year, reaching Php2.7 billion in Q2 2025. This growth was supported by robust topline performance and resilient margins.

Compose Coffee, a recent acquisition, is targeted to deliver a 36% return on invested capital (ROIC). The company’s asset-light model (100% franchised) is expected to result in rapid payback of the acquisition loan through strong dividend inflows.

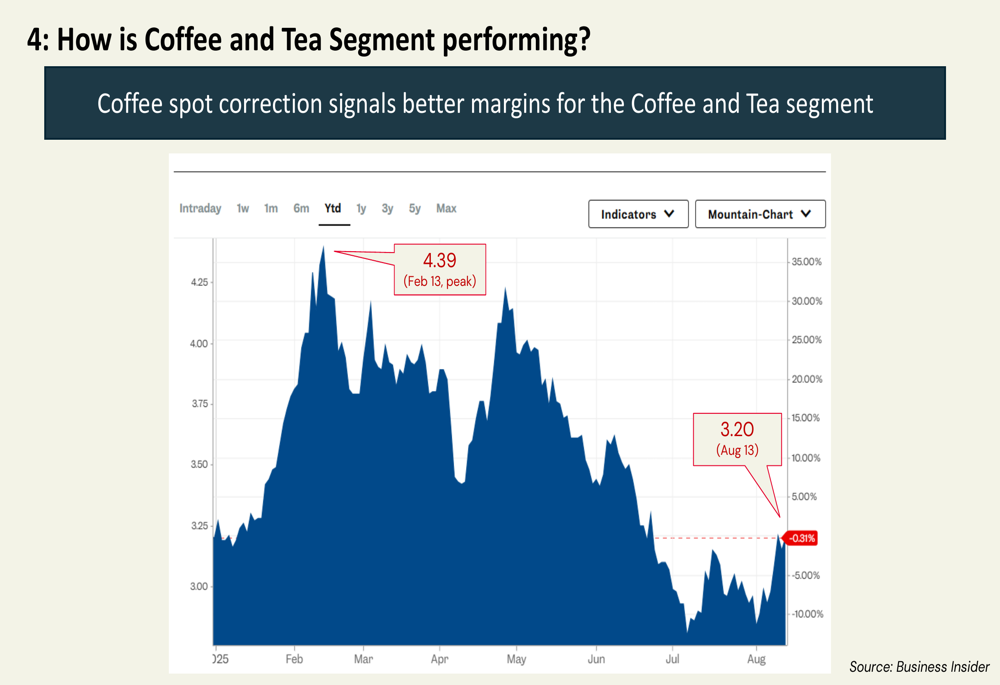

A recent correction in coffee spot prices is expected to further improve margins for this segment:

The company is also leveraging strategic partnerships to drive growth, including a collaboration between Compose Coffee and BTS member V, which is expected to boost brand visibility and customer engagement.

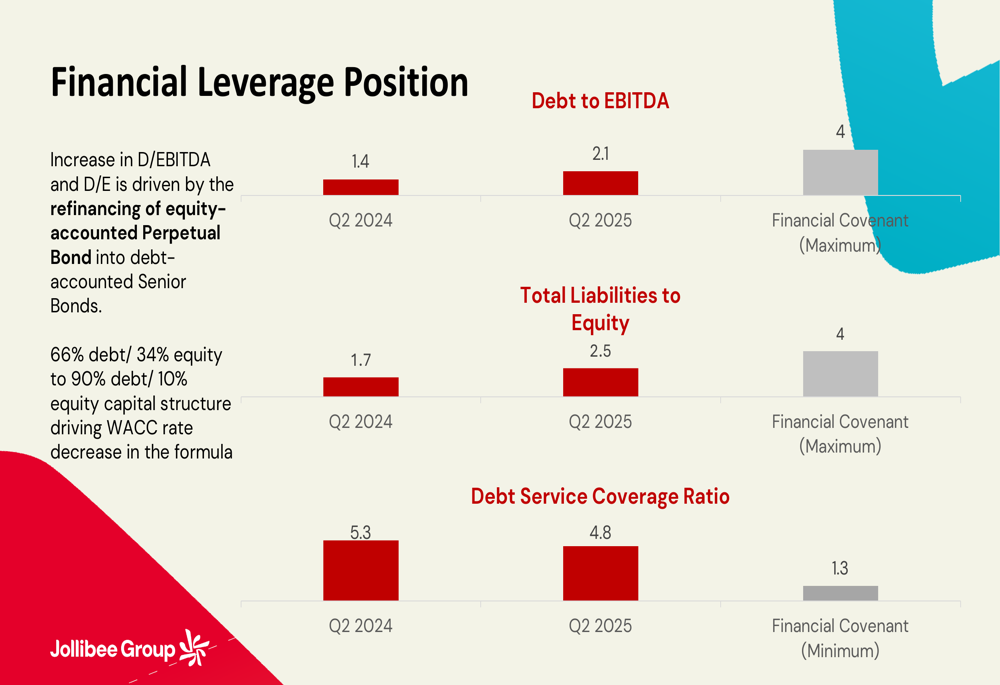

Financial Position and Capital Structure

JFC has undertaken strategic refinancing to optimize its capital structure and fund growth initiatives. The company refinanced its US$396 million perpetual bond (previously carried at 3.9%) through loans and a US$300 million senior bond (5.4%), maintaining a competitive effective interest rate of approximately 5.0%.

This refinancing has shifted JFC’s capital structure from 66% debt/34% equity to 90% debt/10% equity, which is expected to improve the company’s weighted average cost of capital (WACC) going forward.

The company’s financial leverage position remains strong, as shown in the following analysis:

Despite the increase in leverage ratios due to the refinancing, JFC remains well within its financial covenants. The Debt to EBITDA ratio increased from 1.4 to 2.1, still significantly below the maximum covenant of 4.0.

Free cash flow from operations was Php8.0 billion in Q2 2025, representing 10.3% of revenue, while free cash flow excluding lease payments was Php5.1 billion or 6.6% of revenue.

Strategic Initiatives

JFC is implementing several strategic initiatives to drive sustainable growth and improve profitability across its brand portfolio.

In China, the company is seeing signs of recovery following a strategic pivot toward value positioning. Same-store sales grew by 4%, underpinned by robust traffic gains of 15%. Yonghe King is leading the recovery with 3.4% same-store sales growth and 16.6% traffic growth, reversing previous quarters’ decline.

For Tim Ho Wan, which JFC took over management of in January 2025, the company has assembled a new leadership team and fully integrated JFC’s Shared Service Model. The brand has been repositioned to return to its authentic Hong Kong roots, with revamped menu, product enhancements, and price adjustments to appeal to local consumers.

Smashburger is on a path to financial viability under new CEO Jim Sullivan. The brand is driving traffic recovery through a refocused menu strategy, highlighted by the "Summer of Smash" campaign featuring value-led offerings. The company is also pursuing a refranchising strategy for approximately 100 corporate Smashburger stores to unlock capital, with each sale tied to store development commitments.

Forward-Looking Statements

JFC’s presentation indicates confidence in continued growth, with particular emphasis on international expansion and the Coffee and Tea segment. The company’s strategic refinancing and capital structure optimization are designed to support value-accretive growth while safeguarding liquidity during periods of volatility.

The company is focused on improving return on invested capital, with new investments targeted to deliver a 10.5% ROIC and Compose Coffee expected to achieve a 36% ROIC.

JFC anticipates minimal impact from tariffs on its operations across various markets, with virtually zero impact expected in the Philippines and China, and low impact in other regions due to primarily domestic sourcing strategies.

The company’s strong performance in Q2 2025 builds on its momentum from previous quarters, positioning JFC for continued growth as it expands its global footprint and enhances its brand portfolio.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.