BigBear.ai appoints Sean Ricker as chief financial officer

Introduction & Market Context

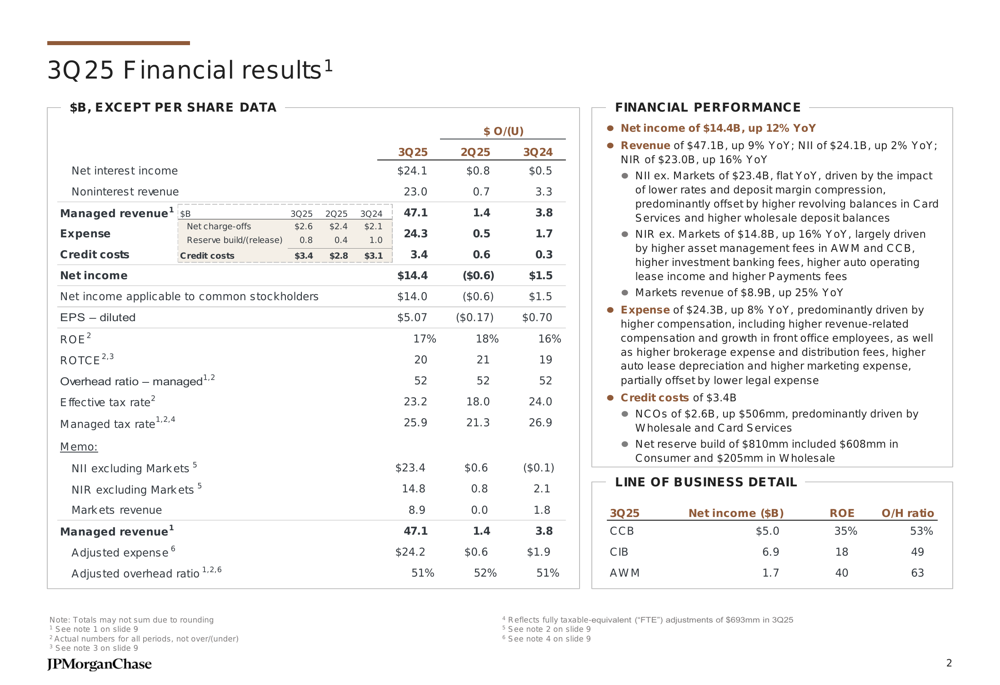

JPMorgan Chase & Co. (NYSE:JPM) released its third quarter 2025 financial results presentation on October 14, 2025, reporting strong performance across all business segments. The banking giant posted a net income of $14.4 billion, representing a 12% year-over-year increase, with earnings per share of $5.07, exceeding analyst expectations of $4.84.

Despite these robust results, JPMorgan’s stock fell 1.78% in pre-market trading, closing at $302.50, reflecting broader market uncertainties and investor concerns about potential regulatory changes and lending risks. The stock is currently trading near its 52-week high of $318.01, with a market capitalization of approximately $830.45 billion.

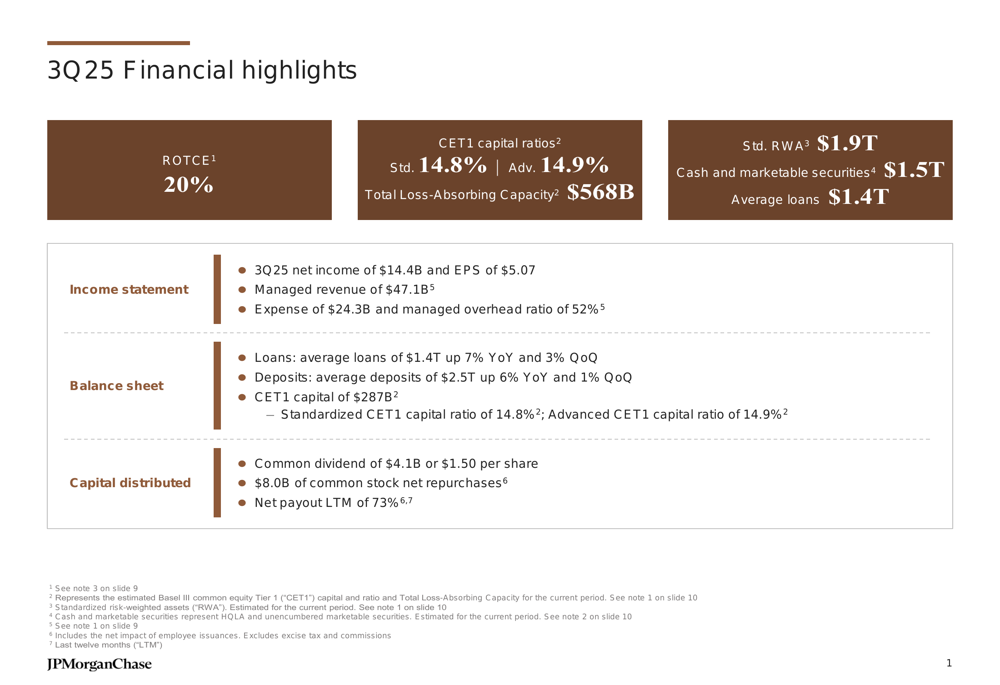

As shown in the following financial highlights slide, JPMorgan maintained strong capital and liquidity positions while delivering solid returns:

Quarterly Performance Highlights

JPMorgan reported managed revenue of $47.1 billion for Q3 2025, marking a 9% increase compared to the same period last year. The company’s expenses rose by 8% year-over-year to $24.3 billion, resulting in a managed overhead ratio of 52%. Credit costs for the quarter stood at $3.4 billion.

The bank’s return on tangible common equity (ROTCE) reached an impressive 20%, while maintaining strong capital ratios with a standardized Common Equity Tier 1 (CET1) ratio of 14.8% and an advanced CET1 ratio of 14.9%. JPMorgan continued its robust capital return program, distributing $4.1 billion in common dividends ($1.50 per share) and executing $8.0 billion in net stock repurchases.

The comprehensive financial results demonstrate JPMorgan’s continued strength across key metrics:

Detailed Financial Analysis

Balance Sheet Strength

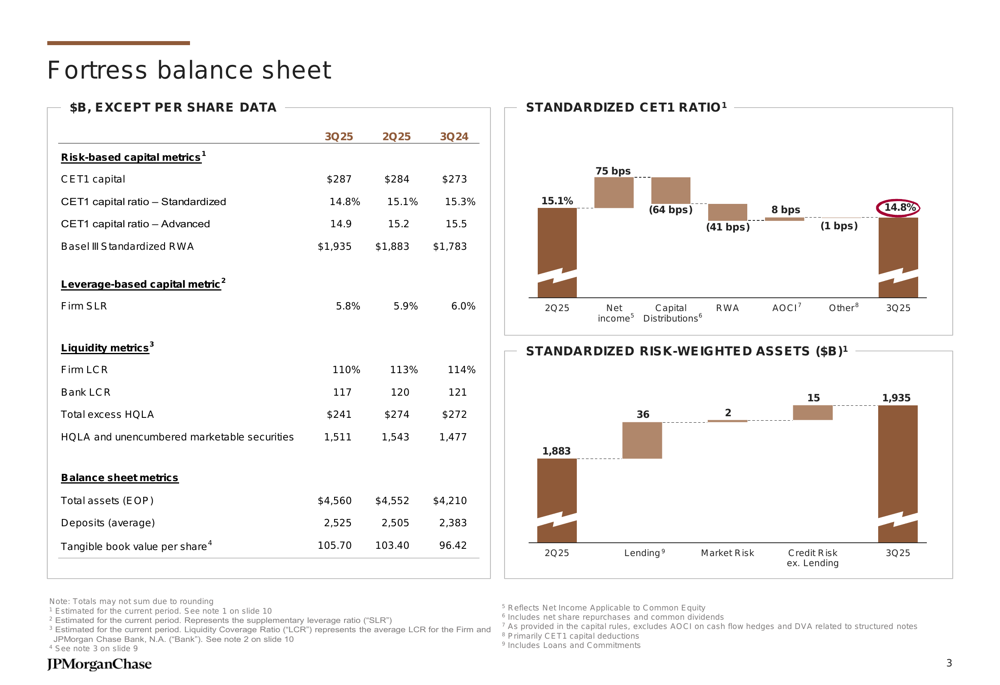

JPMorgan’s "fortress" balance sheet remained a cornerstone of its financial stability in Q3 2025. The bank reported total assets of $4.56 trillion at quarter-end, with average deposits of $2.53 trillion (up 6% year-over-year and 1% quarter-over-quarter). Average loans increased to $1.4 trillion, representing a 7% year-over-year growth and a 3% increase from the previous quarter.

The bank maintained strong liquidity metrics with a firm Liquidity Coverage Ratio (LCR) of 110% and total high-quality liquid assets (HQLA) and unencumbered marketable securities of $1.51 trillion. Tangible book value per share increased to $105.70.

Business Segment Performance

# Consumer & Community Banking (CCB)

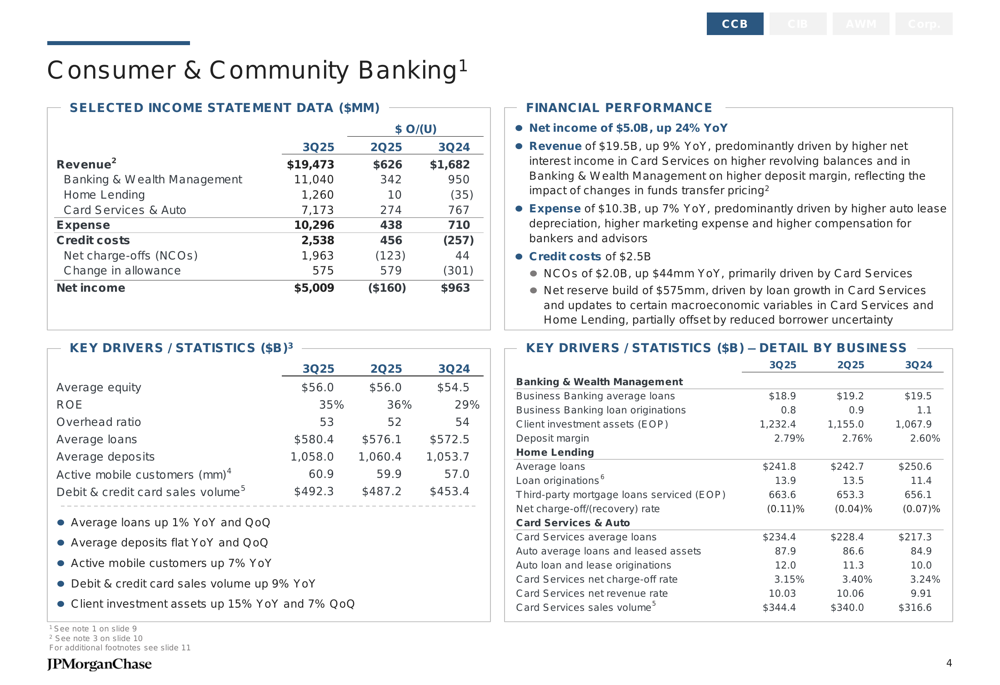

The Consumer & Community Banking segment delivered exceptional results, with net income of $5.0 billion, up 24% year-over-year. Revenue increased by 9% to $19.5 billion, driven by strong performance across banking, wealth management, home lending, and card services. The segment maintained a return on equity of 35% and an overhead ratio of 53%.

Average loans in the CCB segment reached $580.4 billion, while average deposits stood at $1.06 trillion. Client investment assets at period-end were $1.23 trillion, reflecting JPMorgan’s strong position in wealth management services.

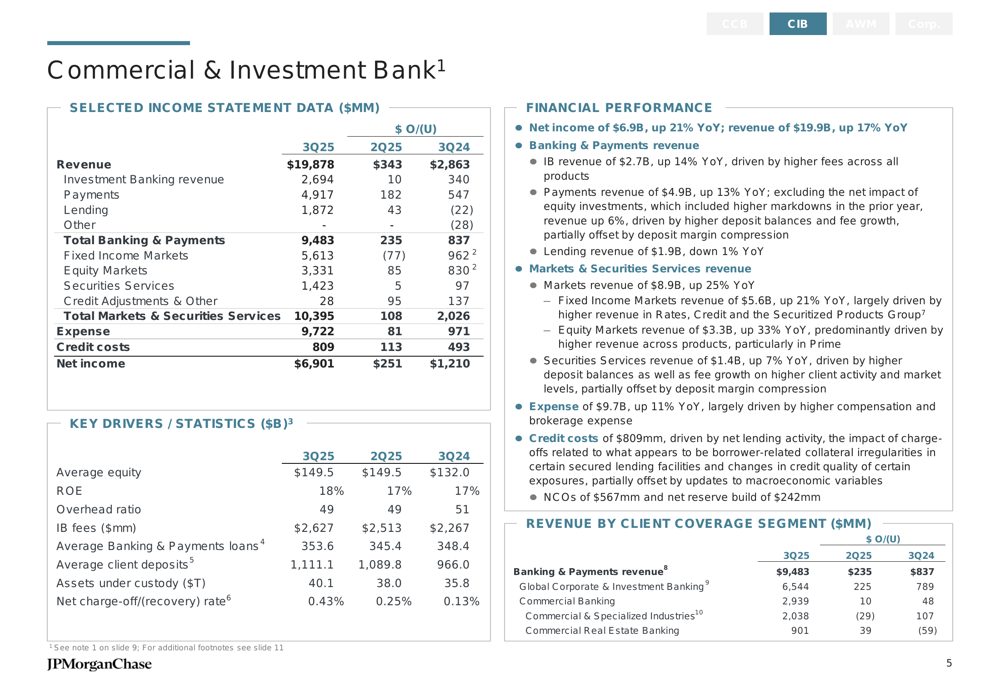

# Commercial & Investment Bank (CIB)

The Commercial & Investment Bank segment reported net income of $6.9 billion, a 21% increase compared to Q3 2024. Revenue rose by 17% year-over-year to $19.9 billion, demonstrating strong performance across banking, payments, and markets activities.

The CIB segment maintained a return on equity of 18% with an overhead ratio of 49%. Average Banking & Payments loans were $353.6 billion, while average client deposits reached $1.11 trillion. Banking & Payments revenue totaled $9.5 billion, with Global Corporate & Investment Banking contributing $6.5 billion and Commercial Banking adding $2.9 billion.

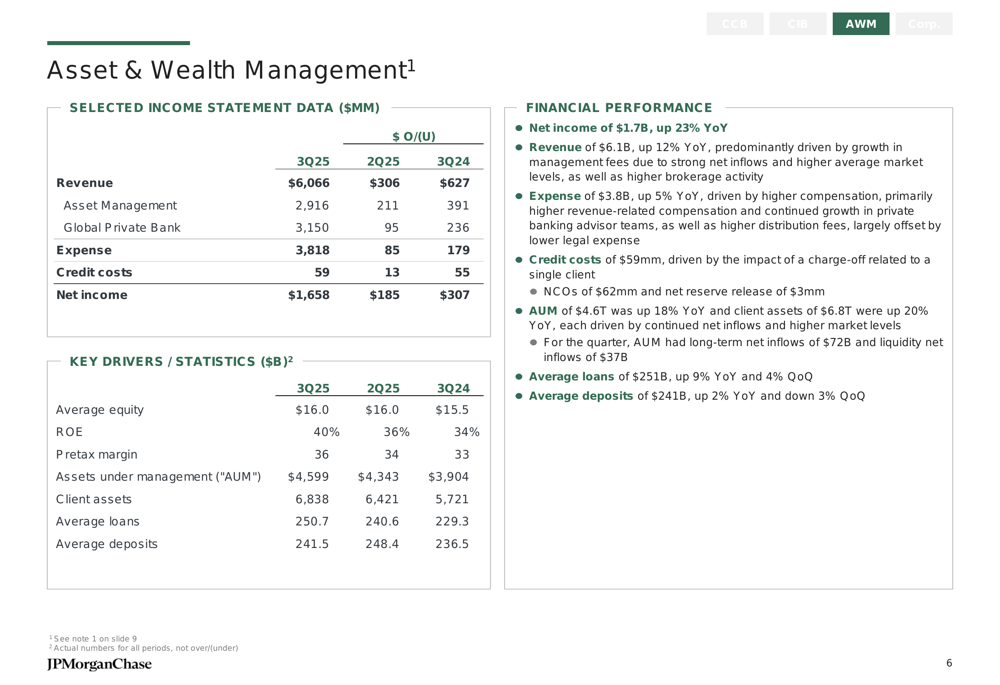

# Asset & Wealth Management (AWM)

The Asset & Wealth Management segment continued its strong trajectory with net income of $1.7 billion, up 23% year-over-year. Revenue increased by 12% to $6.1 billion, driven by growth in assets under management and client relationships.

Assets under management (AUM) reached $4.60 trillion, while the segment maintained a return on equity of 40% with an overhead ratio of 63%. Average loans were $250.7 billion, and average deposits stood at $241.5 billion.

Forward-Looking Statements

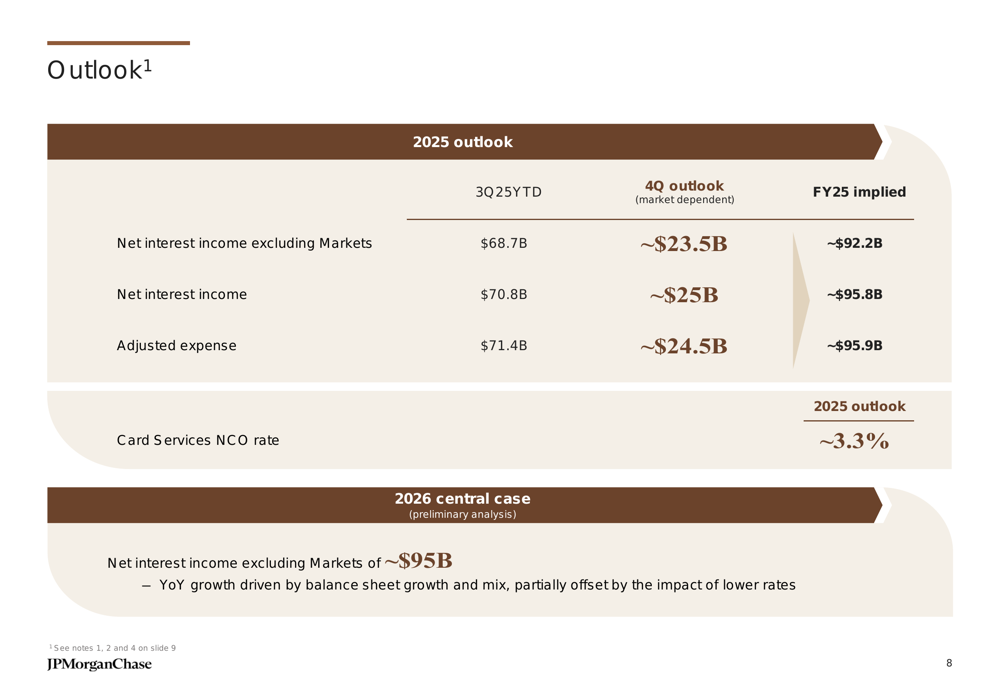

JPMorgan provided an optimistic outlook for the remainder of 2025 and preliminary guidance for 2026. For 2025, the bank expects net interest income excluding Markets to reach approximately $92.2 billion, with total net interest income of around $95.8 billion. Adjusted expenses are projected at approximately $95.9 billion, and the Card Services net charge-off rate is expected to be around 3.3%.

Looking ahead to 2026, JPMorgan’s central case projects net interest income excluding Markets of approximately $95 billion, driven by balance sheet growth and mix, partially offset by the impact of lower interest rates.

Market Reaction & Analyst Perspectives

Despite JPMorgan’s strong financial performance, the stock faced headwinds in the market, declining 1.78% in pre-market trading. This reaction may reflect broader economic uncertainties and investor concerns about potential regulatory changes and lending risks in the banking sector.

During the earnings call, CEO Jamie Dimon emphasized the resilience of customers amidst uncertainty, stating, "Customers are resilient, but there’s still massive amounts of uncertainty." CFO Jeremy Barnum highlighted the importance of expense control, noting, "The proof is going to be in the pudding in terms of actually slowing the growth of expenses."

Analysts focused their questions on non-bank financial institution lending risks, potential regulatory changes, deposit growth expectations, and the investment banking pipeline. The role of artificial intelligence in enhancing productivity was also a key topic of discussion, with executives expressing optimism about its potential benefits.

JPMorgan continues to demonstrate financial strength and resilience in a challenging market environment, maintaining its position as a leader in the banking sector with a focus on strategic investments, productivity initiatives, and shareholder returns.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.