AlphaTON stock soars 200% after pioneering digital asset oncology initiative

Introduction & Market Context

Jastrzebska Spotka Weglowa SA (JSW) released its first quarter 2025 results on June 30, 2025, revealing significant financial challenges amid production difficulties and unfavorable market conditions. The Polish coal and coke producer faced headwinds from both internal operational issues and external market pressures, resulting in widening losses compared to the previous quarter.

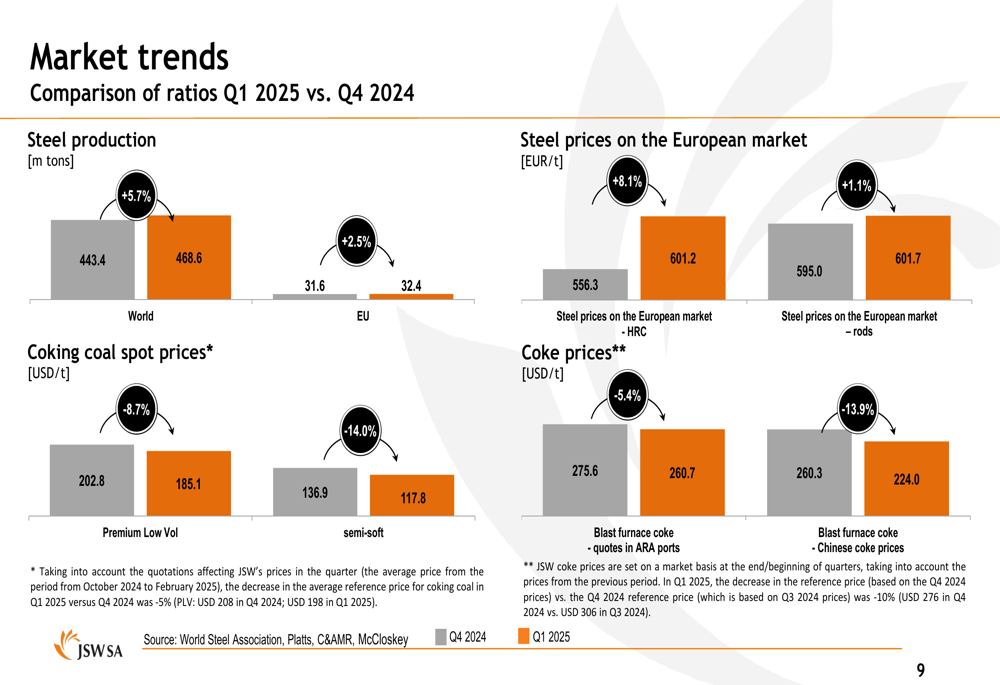

The company’s performance occurred against a backdrop of mixed global market conditions. While global steel production increased by 5.7% and EU steel production rose by 2.5% compared to Q4 2024, coking coal spot prices declined significantly, with Premium Low Vol prices falling 8.7% and Semi-soft prices dropping 14.0%. The company also highlighted growing market protectionism, including customs tariffs introduced (though temporarily suspended) by the USA and import limits on coke imposed by India.

As shown in the following chart of key market trends, steel prices on the European market showed some improvement, but coke prices continued to decline:

Quarterly Performance Highlights

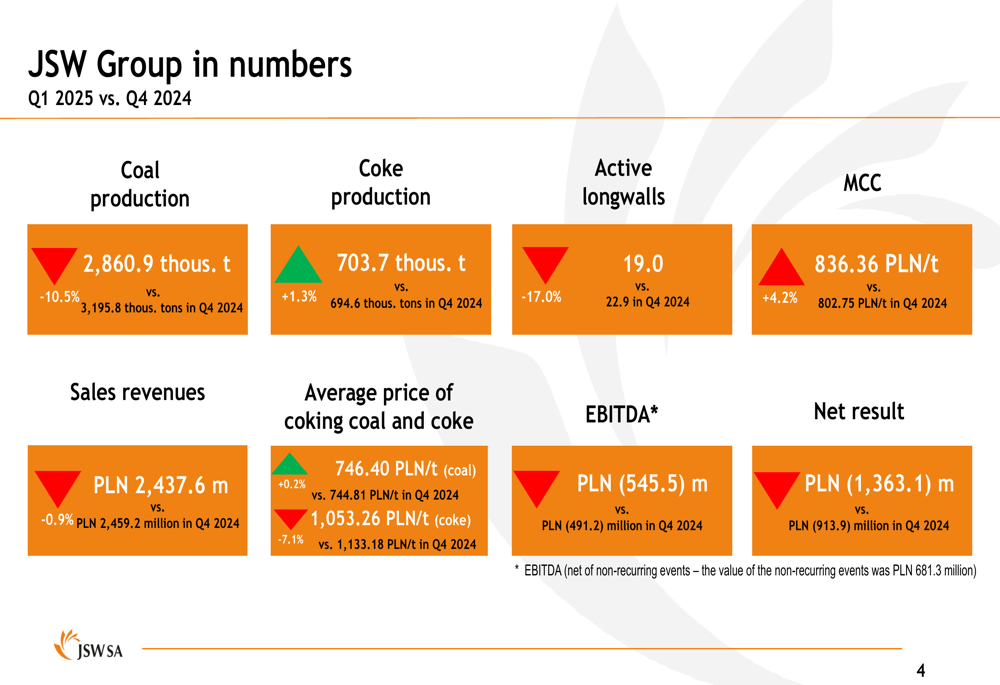

JSW Group reported a substantial net loss of PLN 1,363.1 million in Q1 2025, a significant deterioration from the PLN 913.9 million loss in Q4 2024. The company’s EBITDA (excluding non-recurring events) was negative at PLN 545.5 million, compared to negative PLN 491.2 million in the previous quarter. Non-recurring events in Q1 2025 amounted to PLN 681.3 million.

The following chart highlights key performance indicators for Q1 2025 compared to Q4 2024:

Coal production decreased by 10.5% to 2,860.9 thousand tons in Q1 2025 from 3,195.8 thousand tons in Q4 2024, while coke production increased slightly by 1.3% to 703.7 thousand tons. The number of active longwalls decreased by 17.0% to 19.0, which significantly impacted production volumes. Sales revenues declined marginally by 0.9% to PLN 2,437.6 million.

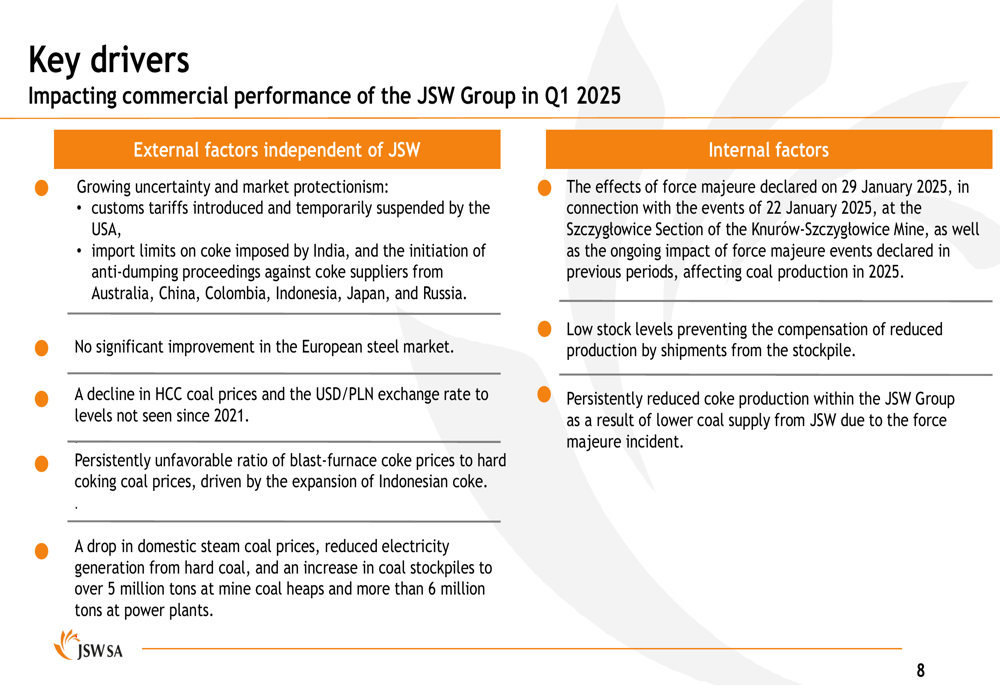

The company attributed the production challenges primarily to a force majeure event declared on January 29, 2025. As outlined in the key drivers slide, low stock levels prevented the company from compensating for reduced production, and persistently reduced coke production resulted from lower coal supply:

Detailed Financial Analysis

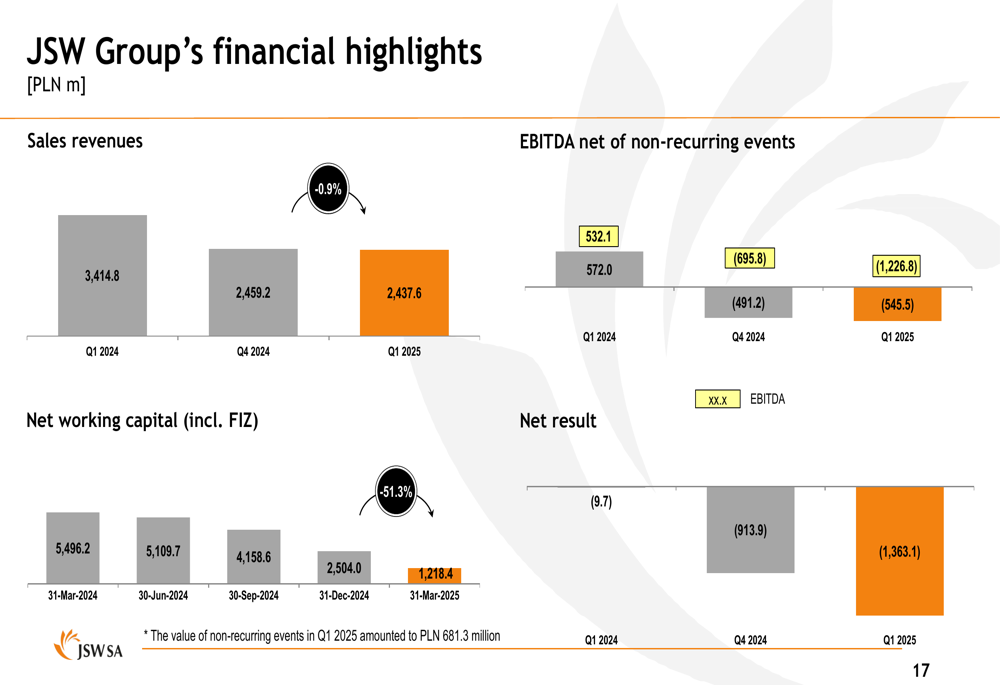

JSW Group’s financial performance deteriorated across multiple metrics in Q1 2025. Sales revenues decreased slightly to PLN 2,437.6 million from PLN 2,459.2 million in Q4 2024, while EBITDA and net result both worsened significantly.

The following chart illustrates the company’s key financial highlights:

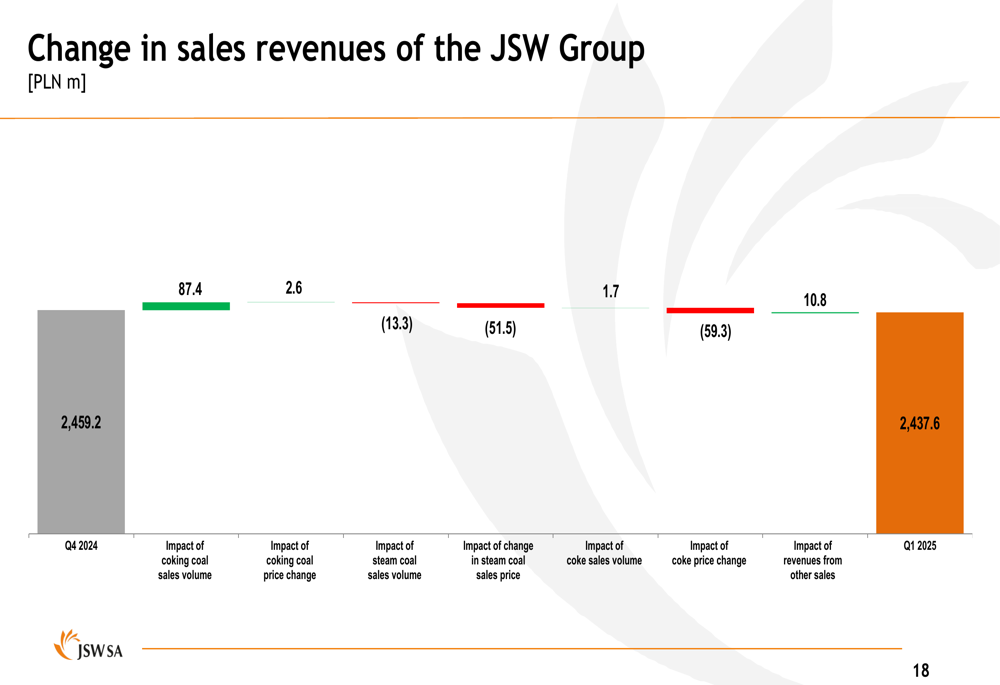

The decline in sales revenue was primarily driven by lower coke prices, which fell by 7.1% to 1,053.26 PLN/t, while coking coal prices remained relatively stable with a slight increase of 0.2% to 746.40 PLN/t. Steam coal prices also declined significantly.

A detailed breakdown of the changes in sales revenue reveals that while higher coking coal sales volumes provided a positive contribution of PLN 87.4 million, this was offset by negative impacts from lower steam coal and coke prices:

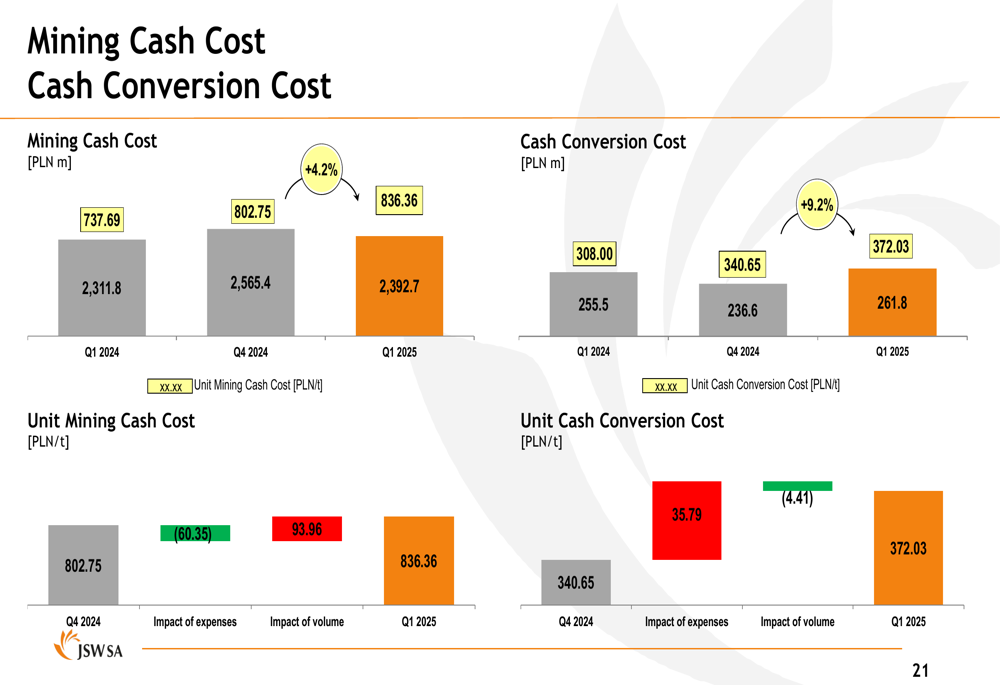

On the cost side, JSW Group’s mining cash cost increased to 836.36 PLN/t in Q1 2025 from 802.75 PLN/t in Q4 2024, representing a 4.2% increase. Similarly, the cash conversion cost rose to 372.03 PLN/t from 340.65 PLN/t, a 9.2% increase. The following chart details these cost metrics:

The company’s net working capital (including FIZ) continued its declining trend, falling to PLN 1,218.4 million as of March 31, 2025, from PLN 2,504.0 million at the end of December 2024. This significant reduction indicates increasing liquidity pressure on the company.

Strategic Initiatives

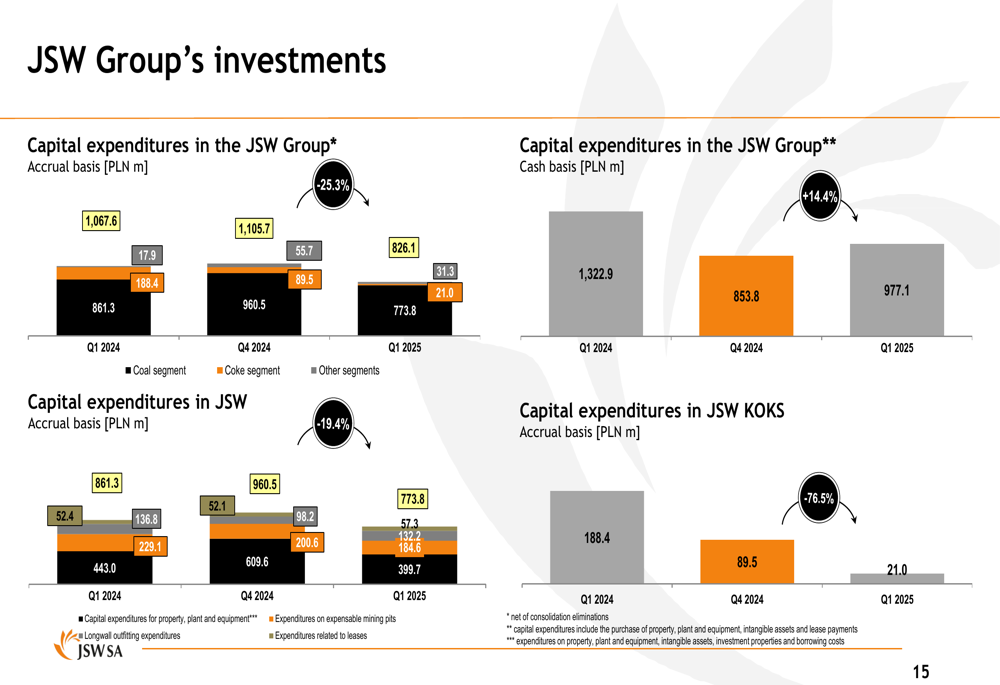

Despite financial challenges, JSW Group continued to invest in its operations, though at a reduced level compared to previous quarters. Capital expenditures on an accrual basis decreased to PLN 826.1 million in Q1 2025 from PLN 1,105.7 million in Q4 2024, representing a 25.3% reduction.

The following chart shows the breakdown of capital expenditures across the JSW Group:

The majority of capital expenditures were concentrated in JSW’s coal segment, which accounted for PLN 773.8 million of the total, while investments in the JSW KOKS division were significantly reduced to PLN 21.0 million, down from PLN 89.5 million in the previous quarter.

These investments are part of the company’s Strategic Transformation Plan, which was mentioned in the presentation agenda but not detailed in the slides provided. The plan likely focuses on improving operational efficiency and addressing the production challenges faced by the company.

Forward-Looking Statements

JSW Group faces significant challenges in the near term, with both internal operational issues and external market pressures impacting performance. The force majeure declared in January 2025 continues to affect coal production, while global market conditions remain challenging.

The company highlighted several external factors that are likely to continue impacting performance, including growing uncertainty and market protectionism, no significant improvement in the European steel market, unfavorable ratio of blast-furnace coke prices to hard coking coal prices, and a drop in domestic steam coal prices with increased coal stockpiles.

Inventories of coal decreased to 1,187.8 thousand tons as of March 31, 2025, from 1,407.1 thousand tons at the end of December 2024, while coke inventories decreased to 115.7 thousand tons from 147.1 thousand tons. These inventory reductions may provide some relief to working capital pressure but also indicate potential supply constraints if production challenges persist.

The company will need to address its rising costs and production challenges to improve financial performance in the coming quarters. The success of its Strategic Transformation Plan will be crucial in determining whether JSW Group can return to profitability amid challenging market conditions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.