Nvidia among investors in xAI’s $20 bln capital raise- Bloomberg

Introduction & Market Context

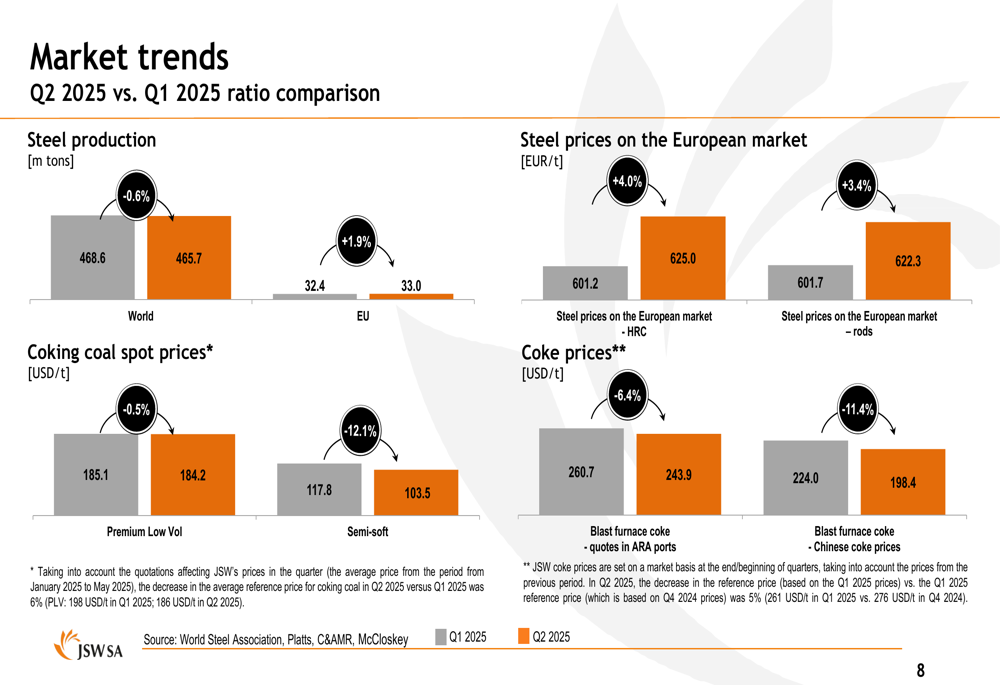

Jastrzebska Spotka Weglowa SA (JSW) released its H1 2025 financial results presentation on September 29, 2025, revealing a complex picture of operational improvements offset by persistent financial challenges. The Polish coal and coke producer continues to navigate difficult market conditions, with global steel production declining slightly from 468.6 million tons in Q1 2025 to 465.7 million tons in Q2 2025, though EU production saw a modest increase from 32.4 to 33.0 million tons.

The market environment showed mixed signals, with European steel prices increasing while coking coal and coke prices declined. This pricing pressure directly impacted JSW’s financial performance despite operational improvements.

As shown in the following chart of market trends comparing Q2 2025 to Q1 2025, the company faced headwinds from declining coking coal and coke prices despite some strengthening in steel prices:

Quarterly Performance Highlights

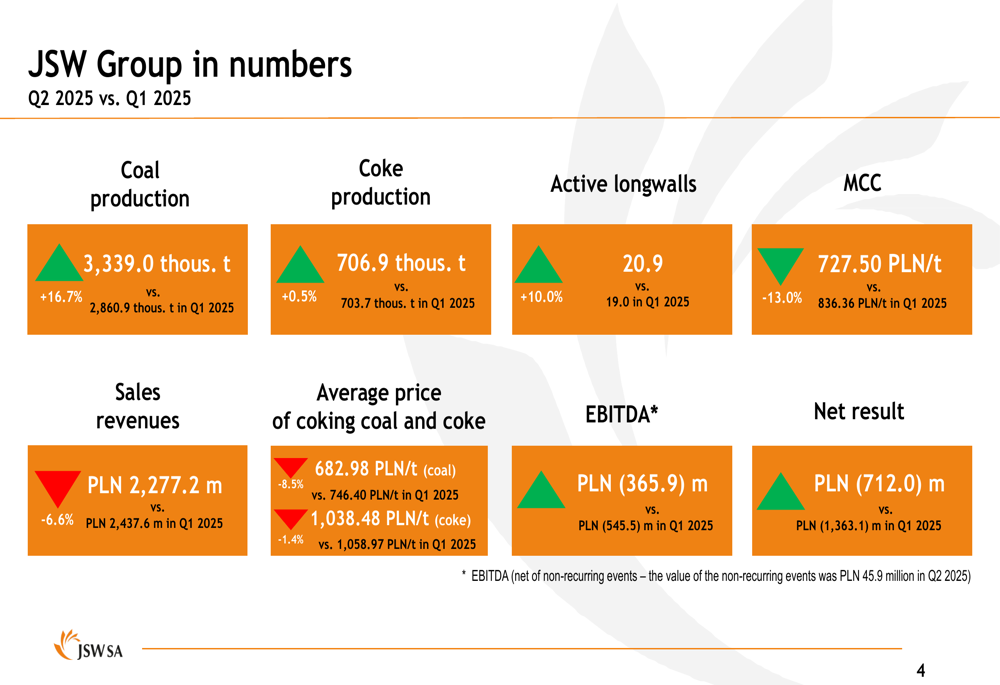

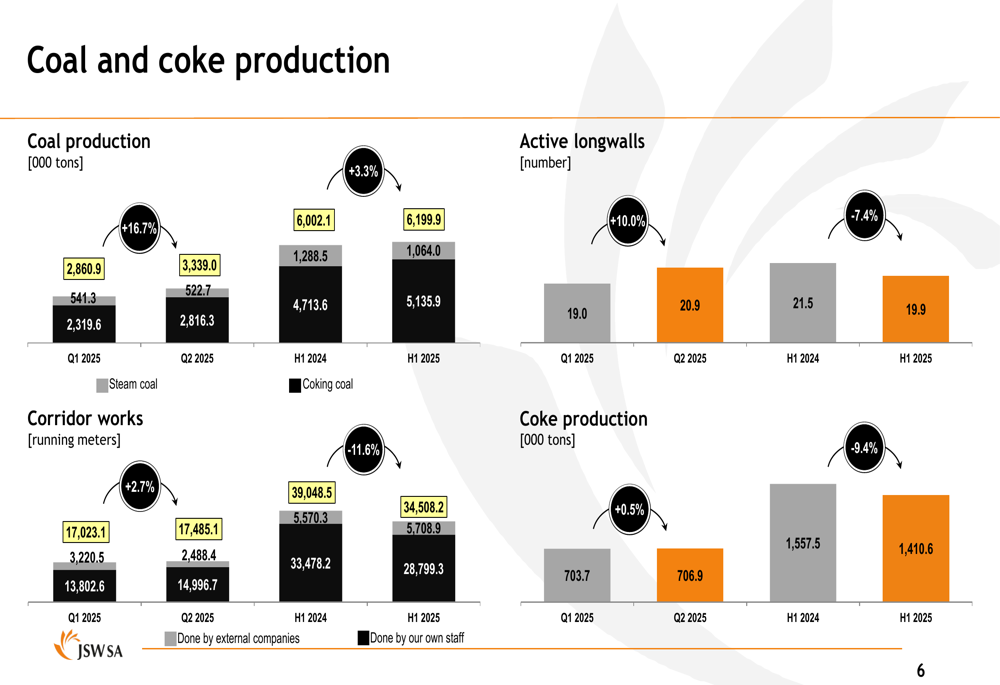

JSW Group reported significant production increases in Q2 2025, with coal production rising 16.7% quarter-over-quarter to 3,339.0 thousand tonnes and coke production edging up slightly by 0.5% to 706.9 thousand tonnes. The company also increased its active longwalls by 10% to 20.9.

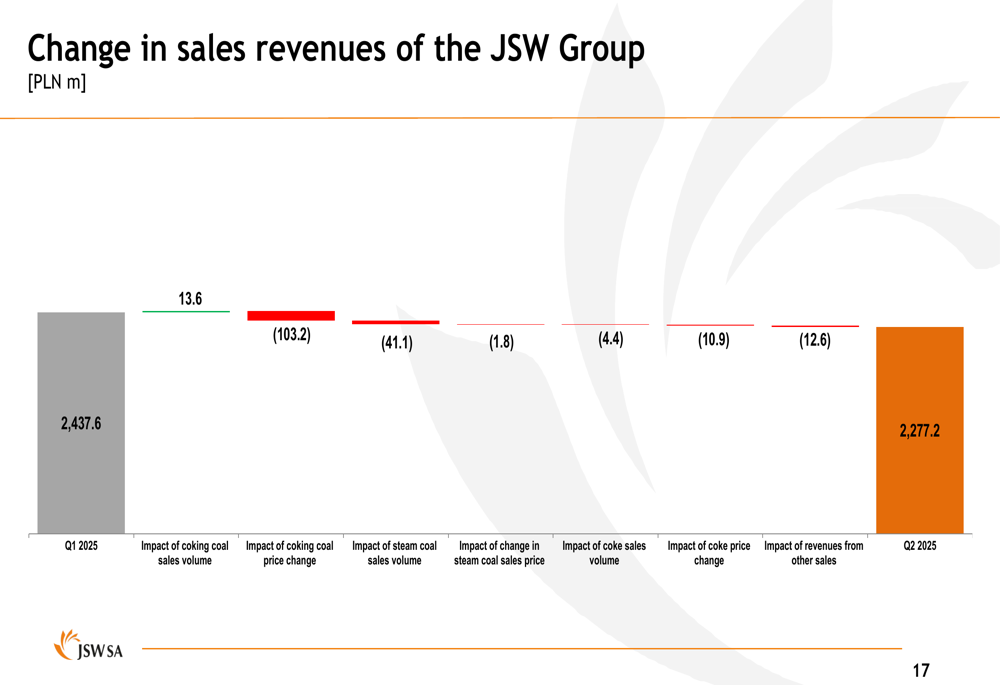

However, these operational improvements couldn’t offset price declines, as the average price of coking coal fell 8.5% to 682.98 PLN/t and coke prices decreased 1.4% to 1,038.48 PLN/t. Consequently, sales revenues declined 6.6% to PLN 2,277.2 million.

The following chart highlights key performance indicators comparing Q2 2025 to Q1 2025:

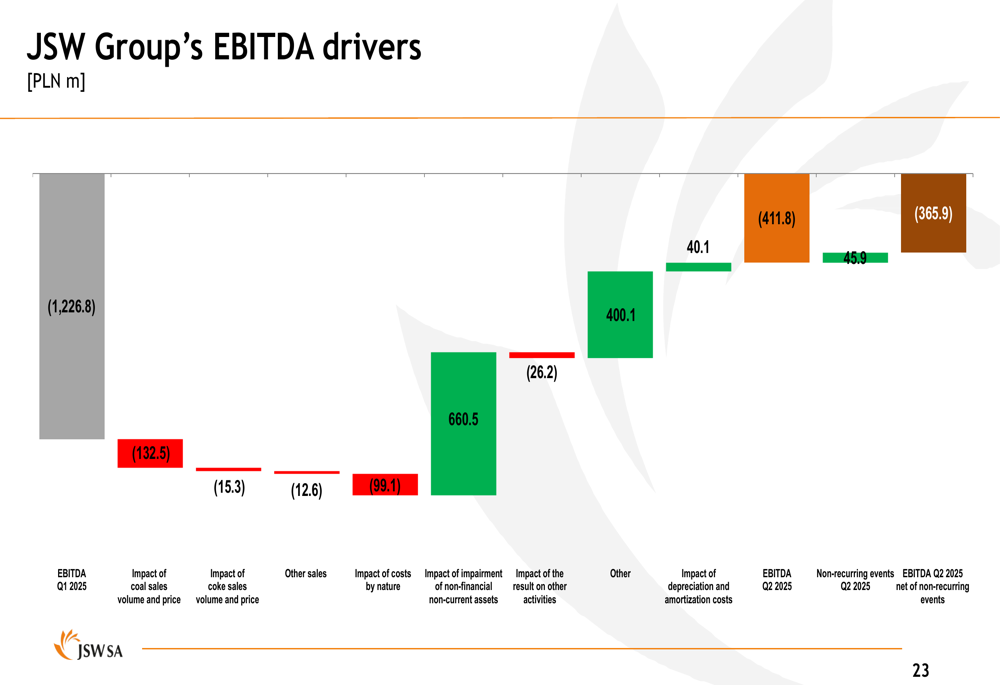

Despite the revenue decline, JSW managed to improve its EBITDA, though it remained negative at PLN (365.9) million in Q2 compared to PLN (545.5) million in Q1. Similarly, net losses narrowed to PLN (712.0) million from PLN (1,363.1) million in the previous quarter.

The company’s coal and coke production volumes over recent quarters are detailed in the chart below:

Detailed Financial Analysis

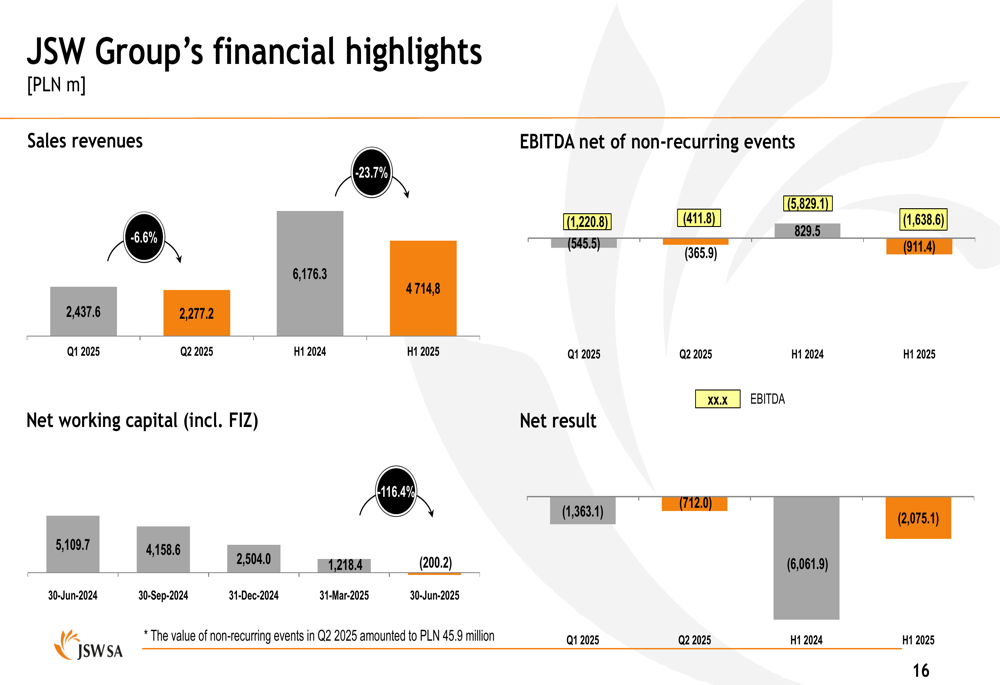

JSW’s financial performance continues to be challenged, with H1 2025 sales revenues of PLN 4,714.8 million representing a significant decline from PLN 6,176.3 million in H1 2024. The company’s EBITDA remained deeply negative at PLN (1,638.6) million for H1 2025, compared to a positive PLN 829.5 million in H1 2024.

The following chart illustrates JSW Group’s key financial metrics:

A detailed breakdown of the quarter-over-quarter sales revenue decline reveals that the primary drivers were coking coal price changes (PLN -103.2 million) and, to a lesser extent, coking coal sales volume (PLN +13.6 million), as shown in this waterfall chart:

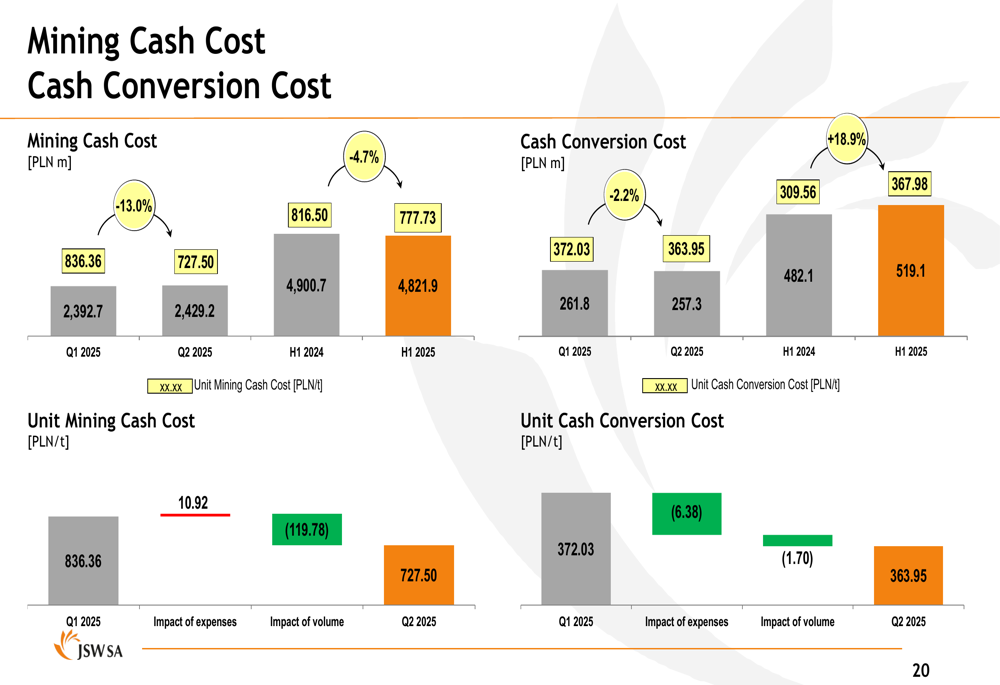

On the cost side, JSW made progress in reducing its unit mining cash cost, which decreased 13.0% quarter-over-quarter to 727.50 PLN/t. This improvement was primarily driven by higher production volumes, which had a PLN 119.78/t positive impact, partially offset by increases in external services and employee benefits.

The mining cash cost and cash conversion cost metrics are detailed in the following chart:

JSW’s working capital position deteriorated significantly, turning negative at PLN (200.2) million as of June 30, 2025, compared to positive PLN 1,218.4 million at the end of March 2025. This decline reflects the company’s ongoing financial challenges.

The breakdown of JSW’s EBITDA drivers shows multiple factors contributing to the improved but still negative Q2 result:

Strategic Initiatives

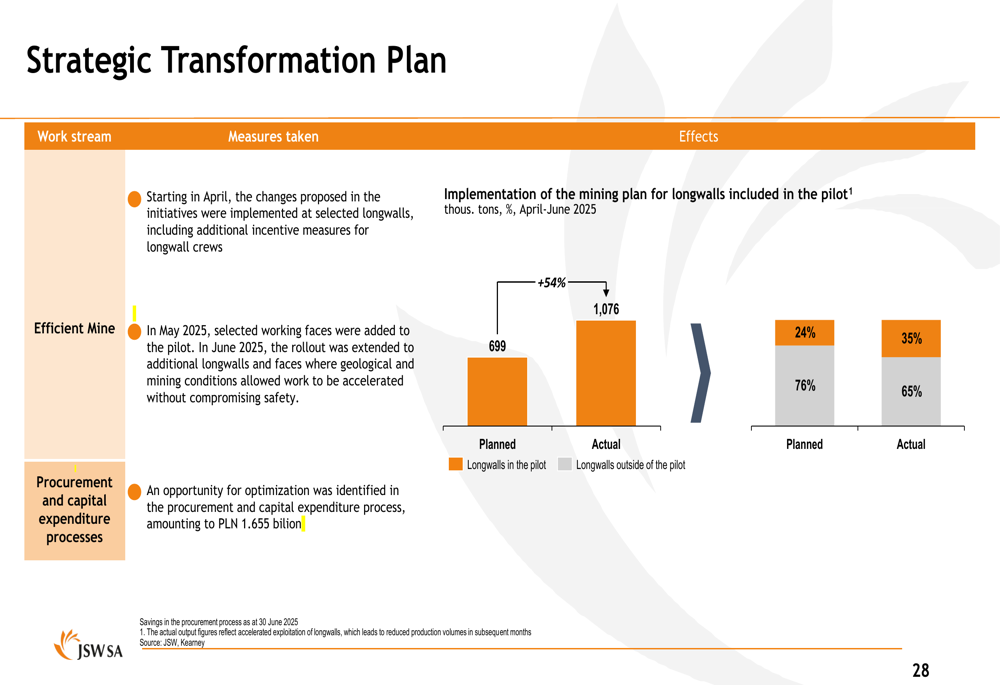

JSW is implementing a Strategic Transformation Plan to improve operational efficiency. Early results from the "Efficient Mine" initiative show a 54% improvement in performance for planned tonnes in pilot longwalls. The company is also focusing on optimizing procurement and capital expenditure processes.

The following chart details the progress of the Strategic Transformation Plan:

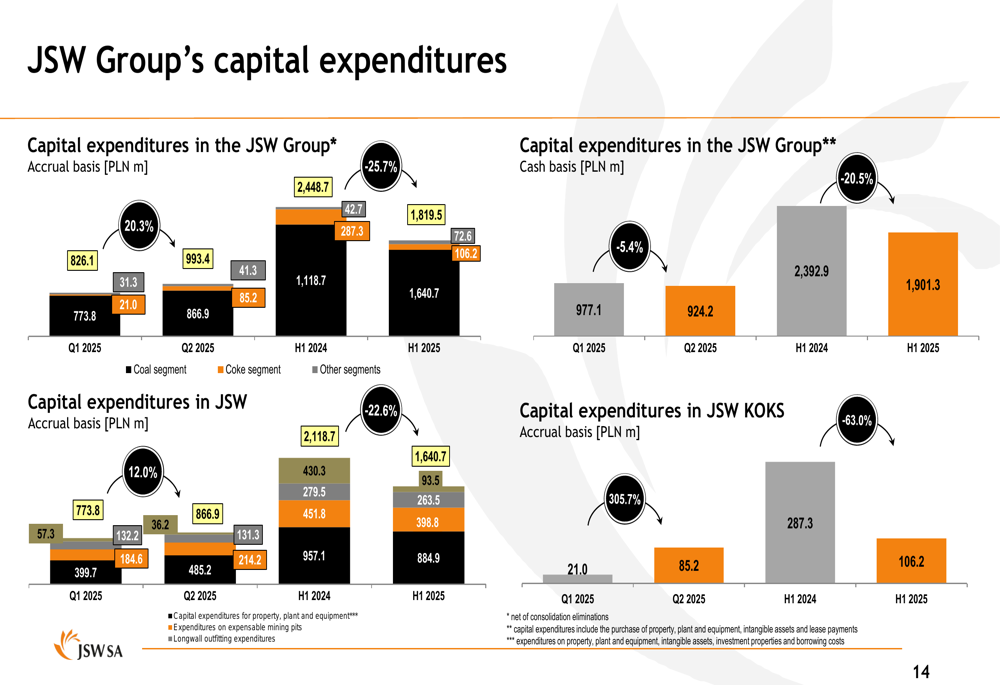

Capital expenditures for the JSW Group in H1 2025 totaled PLN 1,819.5 million, down from PLN 2,448.7 million in H1 2024. The coal segment accounted for the majority of this spending.

The breakdown of capital expenditures is shown in the following chart:

Forward-Looking Statements

While JSW did not provide explicit forward guidance, the company’s Strategic Transformation Plan represents its primary vehicle for improving future performance. Management emphasized the early positive results from efficiency initiatives, particularly in mining operations.

The persistent negative EBITDA and net results, coupled with deteriorating working capital, indicate that JSW continues to face significant challenges. The company will need to achieve further operational improvements and hope for more favorable market conditions, particularly regarding coking coal and coke prices, to return to profitability.

The effectiveness of cost-cutting measures, particularly the 13% reduction in unit mining cash cost achieved in Q2, will be crucial for the company’s ability to weather the current market environment. However, with coal inventories increasing to 1,545.7 thousand tonnes by the end of June 2025 (up from 1,187.8 thousand tonnes at the end of March), JSW may face additional pressure if market demand does not strengthen.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.