Bullish indicating open at $55-$60, IPO prices at $37

Introduction & Market Context

Karyopharm Therapeutics (NASDAQ:KPTI) presented its second quarter 2025 financial results and business update on August 11, 2025, highlighting a strategic pivot toward myelofibrosis as a transformative opportunity while reporting mixed financial performance. The company is positioning selinexor, its lead product, as a potential game-changer in the myelofibrosis market while maintaining its commercial foundation in multiple myeloma.

The presentation comes as Karyopharm navigates a challenging financial landscape, with the stock trading at $3.94, down 0.76% in the most recent session, and significantly below its 52-week high of $16.95. The company’s strategic focus on myelofibrosis represents a bid to transform its growth trajectory amid competitive pressures in its core multiple myeloma market.

Quarterly Performance Highlights

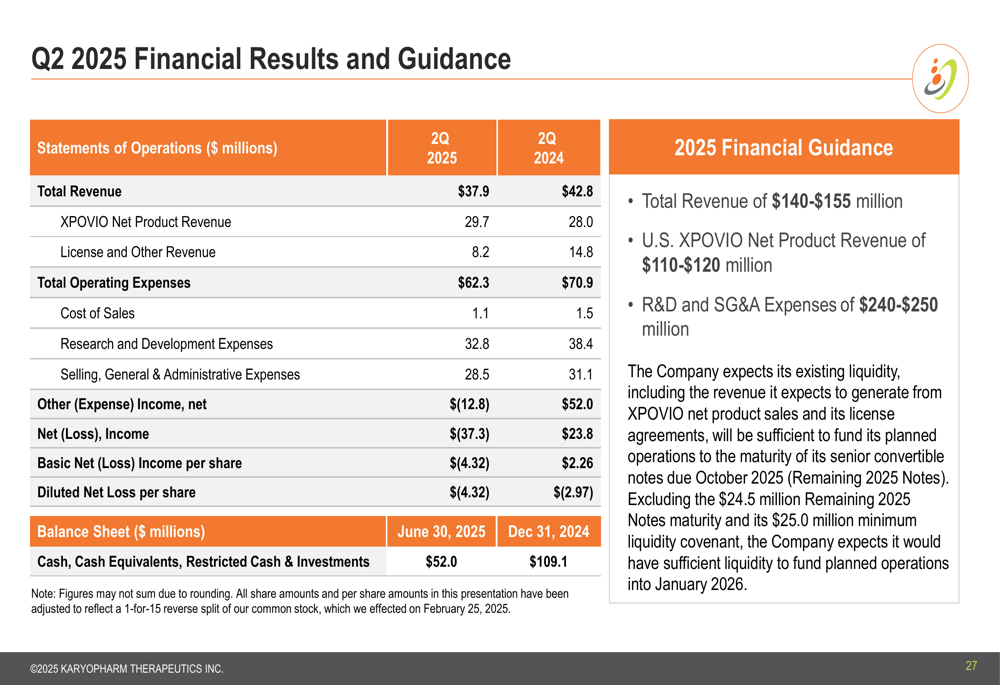

Karyopharm reported U.S. net product revenue of $29.7 million in Q2 2025, representing a 6% year-over-year increase from $28.0 million in Q2 2024. This growth occurred despite a highly competitive multiple myeloma market, with the community setting continuing to drive approximately 60% of overall U.S. net product revenue.

As shown in the following financial results slide, total revenue was $37.9 million, down from $42.8 million in the same quarter last year, primarily due to lower license and other revenue, which fell to $8.2 million from $14.8 million. The company reported a net loss of $37.3 million, compared to net income of $23.8 million in Q2 2024:

Total (EPA:TTEF) operating expenses decreased to $62.3 million from $70.9 million in the prior year period, reflecting the company’s cost management efforts. For the full year 2025, Karyopharm provided revenue guidance of $140-$155 million, with U.S. XPOVIO net product revenue expected to be $110-$120 million.

This guidance represents a slight downward adjustment from the Q1 2025 U.S. XPOVIO revenue projection of $115-$130 million, suggesting some challenges in the competitive multiple myeloma landscape. The company is also exploring financing transactions and strategic alternatives to extend its cash runway, which had declined to $70.3 million as of Q1 2025, down from $109.1 million previously.

Strategic Initiatives

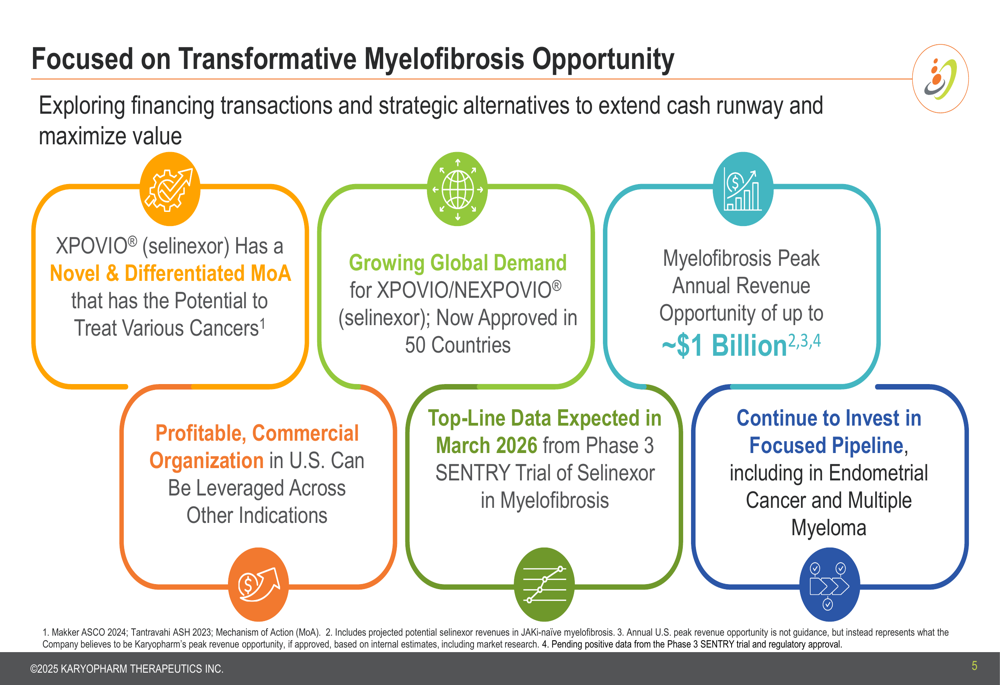

The cornerstone of Karyopharm’s strategy is its focus on myelofibrosis as a transformative opportunity. The company highlighted several key aspects of this strategy, including XPOVIO’s novel mechanism of action, growing global demand with approvals in 50 countries, and a profitable U.S. commercial organization that can be leveraged across other indications:

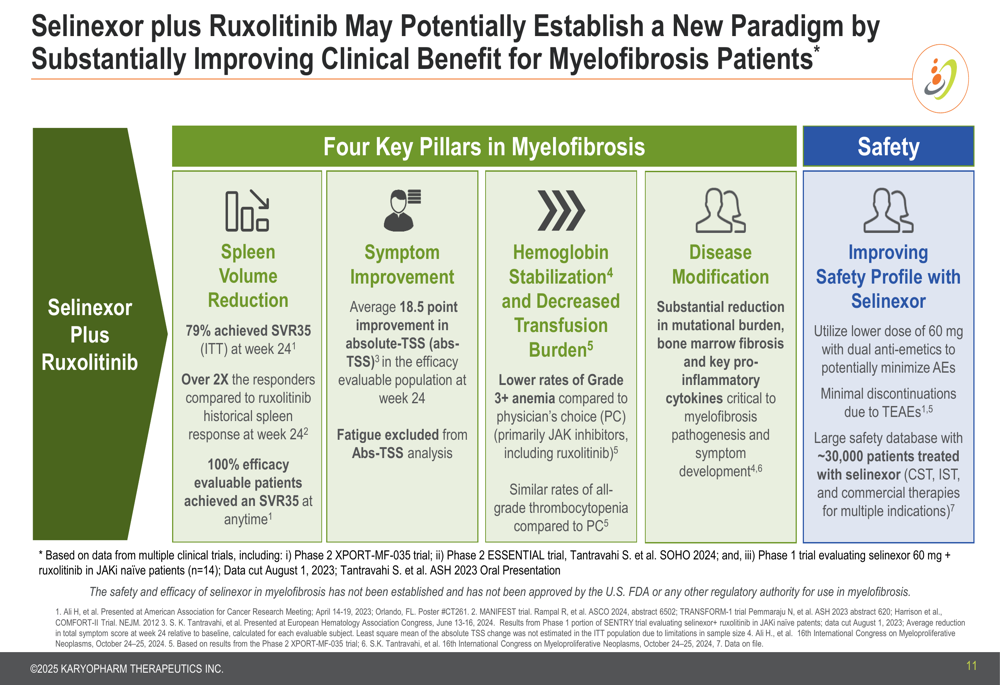

The company is positioning selinexor plus ruxolitinib as a potential new paradigm in myelofibrosis treatment, highlighting impressive clinical data including 79% of patients achieving SVR35 (spleen volume reduction of ≥35%) at week 24 in the intent-to-treat population. This represents more than double the historical response rate with ruxolitinib alone:

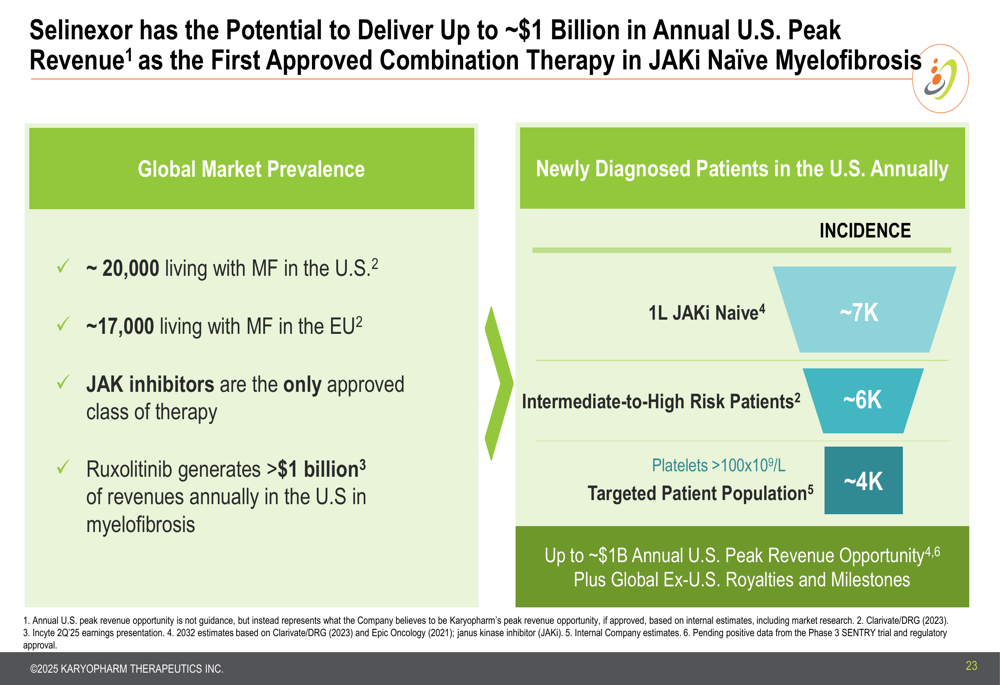

Karyopharm estimates the myelofibrosis opportunity could generate up to $1 billion in peak annual U.S. revenue, based on a market of approximately 20,000 patients living with myelofibrosis in the U.S. and ruxolitinib’s current annual U.S. sales exceeding $1.1 billion:

Pipeline Progress

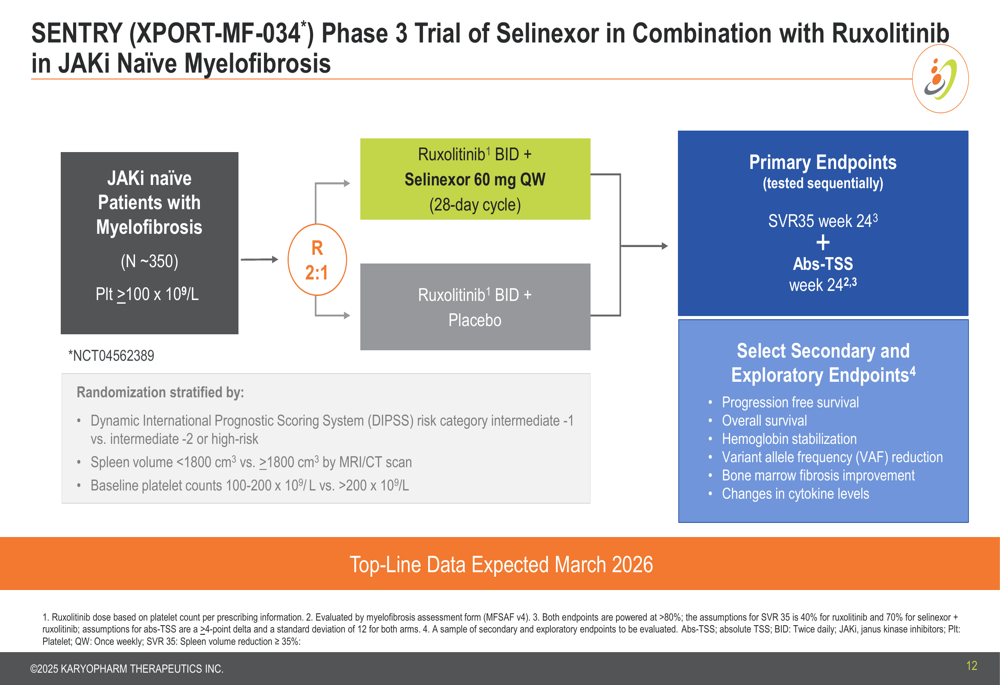

The Phase 3 SENTRY trial evaluating selinexor in combination with ruxolitinib in JAK inhibitor-naïve myelofibrosis patients is a key focus, with top-line data expected in March 2026. The trial is designed to evaluate the combination’s efficacy in improving spleen volume reduction and symptom scores:

Preliminary safety data from the blinded Phase 3 SENTRY trial suggests an improved safety profile compared to historical data with ruxolitinib alone, with potentially lower rates of grade 3+ anemia and fewer treatment discontinuations due to adverse events.

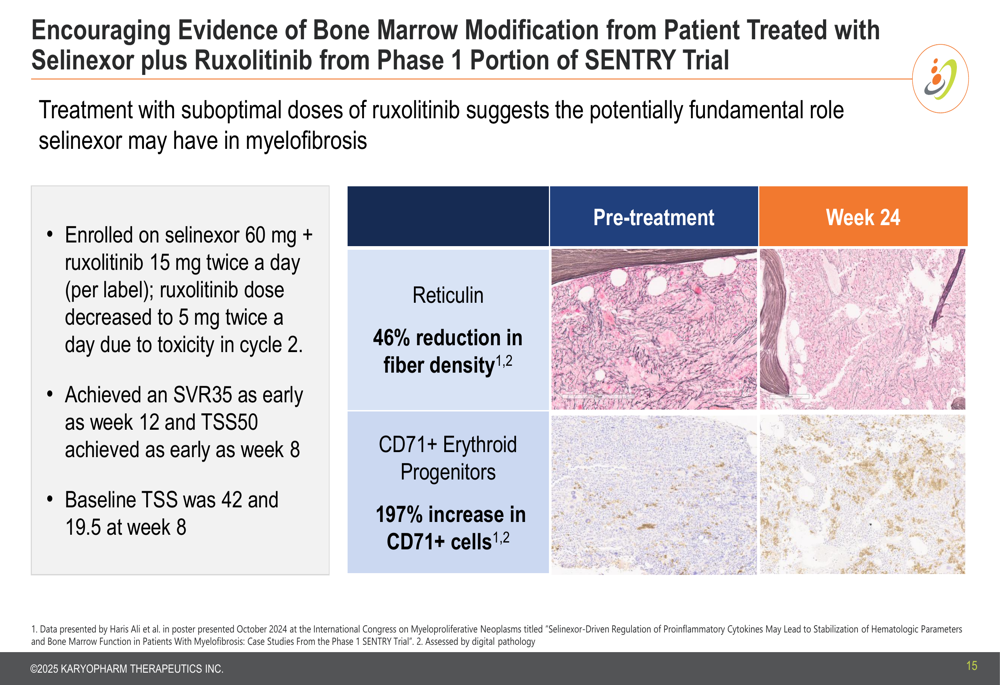

The company also presented encouraging evidence of bone marrow modification in a patient treated with selinexor plus ruxolitinib, showing a 46% reduction in reticulin fiber density and a 197% increase in CD71+ erythroid progenitor cells at week 24 compared to baseline:

Beyond myelofibrosis, Karyopharm is advancing two other Phase 3 programs: XPORT-EC-042 in endometrial cancer (top-line data anticipated mid-2026) and XPORT-MM-031 in multiple myeloma (top-line data expected in 1H-2026). The endometrial cancer program is targeting TP53 wild-type patients, with a potential addressable population of approximately 6,000 patients in the U.S.

Competitive Industry Position

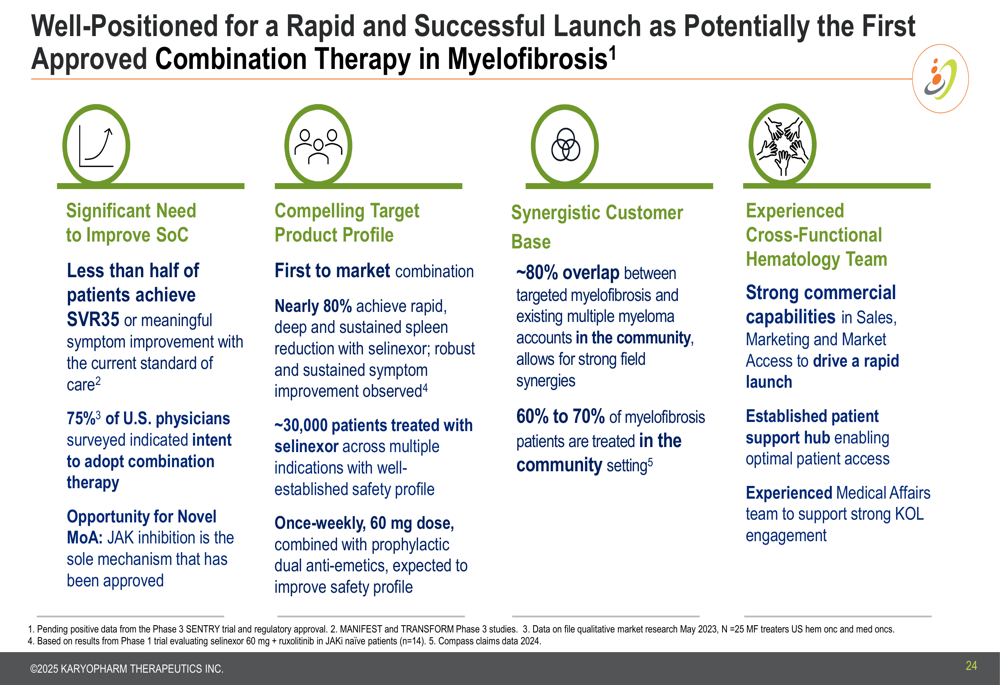

Karyopharm believes it is well-positioned for a rapid and successful launch in myelofibrosis, pending regulatory approval. The company noted that 75% of U.S. physicians surveyed indicated intent to adopt combination therapy, and approximately 80% of targeted myelofibrosis accounts overlap with existing multiple myeloma accounts in the community setting:

In the multiple myeloma space, Karyopharm acknowledged the highly competitive landscape but highlighted its established commercial presence and continued focus on driving XPOVIO adoption. The company’s global footprint continues to expand, with XPOVIO/NEXPOVIO now approved in 50 countries.

Forward-Looking Statements

Looking ahead, Karyopharm’s near-term focus is on completing enrollment of the pivotal Phase 3 SENTRY trial while maintaining its profitable commercial foundation. The company is targeting several key milestones in 2026, including top-line results from three Phase 3 trials: SENTRY in myelofibrosis, XPORT-EC-042 in endometrial cancer, and XPORT-MM-031 in multiple myeloma.

The company’s presentation emphasized the potential for these clinical programs to drive significant value, particularly the myelofibrosis opportunity. However, Karyopharm also acknowledged the need to explore financing transactions and strategic alternatives to support its pipeline advancement, reflecting the financial challenges evident in its Q2 results.

Dr. John Mascarenhas, Principal Investigator of the Phase 3 SENTRY Trial, provided a supportive perspective on the company’s myelofibrosis program: "I’m excited about the SENTRY trial because it is trying to move the myelofibrosis field forward by introducing combinations of therapy early on that don’t have overlapping mechanisms of action, to try to get the deepest response possible to control the disease and hopefully have that durability that benefits the patient long term."

As Karyopharm navigates the transition from a primarily multiple myeloma-focused company to one with broader hematological and oncological applications, the success of its myelofibrosis program will likely be critical to its long-term growth prospects and financial stability.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.