U.S. futures subdued as government shutdown stretches into second week

Introduction & Market Context

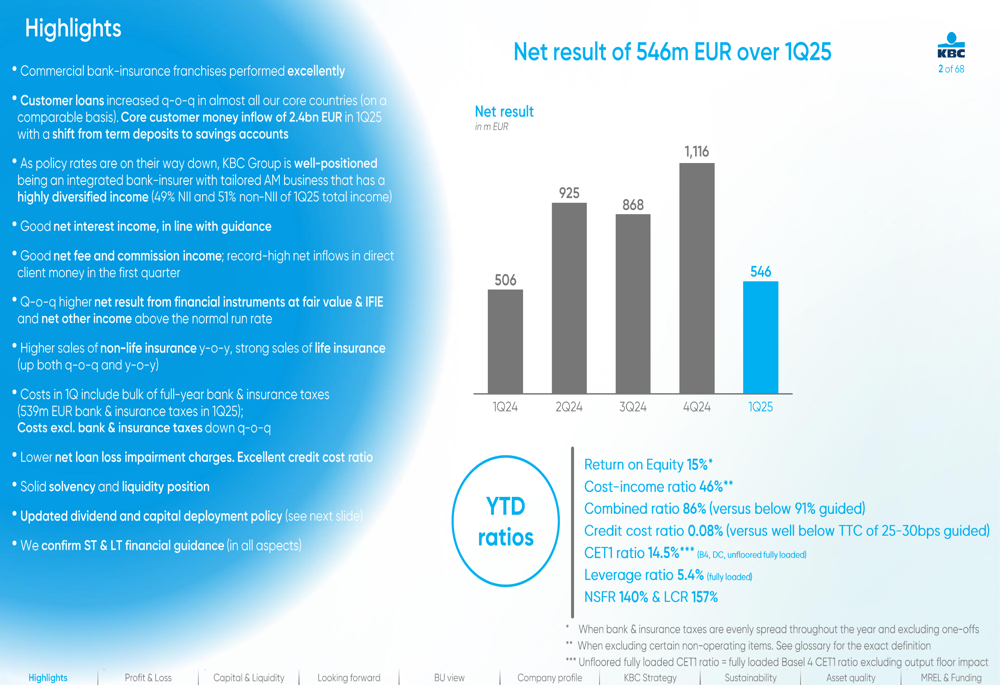

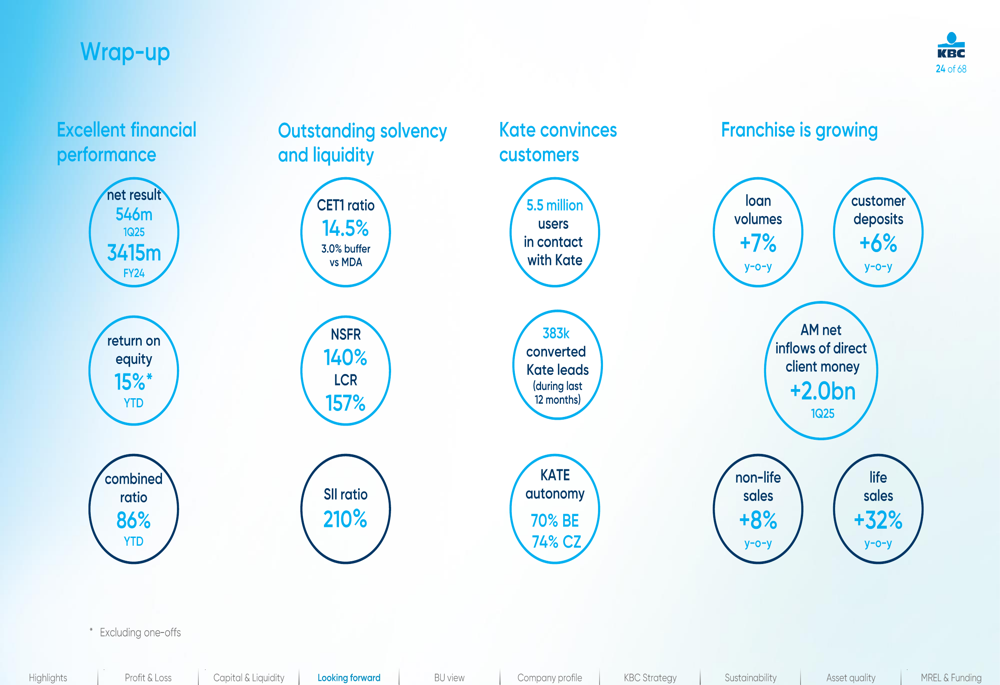

KBC Group (OTC:KBCSY) (EURONEXT:KBC) presented its first quarter 2025 results on May 15, showcasing a solid start to the year with a net profit of €546 million, up 8% from €506 million in the same period last year. The Belgian bank-insurance group demonstrated resilience across its diversified business model, with balanced contributions from both interest income and non-interest income sources.

The quarter was marked by customer loan growth across most core markets, good net interest income in line with guidance, and strong fee and commission income. The company also announced a significant acquisition in Slovakia and updated its dividend policy, signaling confidence in its financial position and growth trajectory.

As shown in the following quarterly performance chart, KBC’s results have remained strong despite seasonal fluctuations in bank taxes:

Quarterly Performance Highlights

KBC reported a return on equity of 15% for the first quarter, positioning it as one of the most profitable financial institutions in Europe. The cost-income ratio stood at 46%, while the combined ratio for insurance operations was 86%, reflecting strong underwriting discipline.

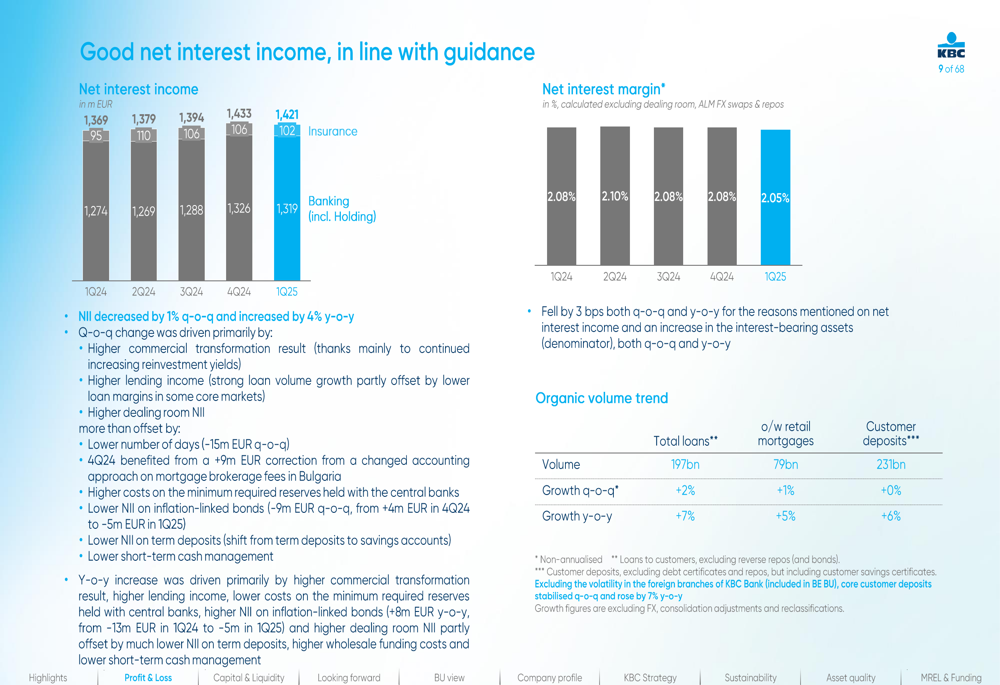

Net interest income reached €1,421 million, up 4% year-over-year but down 1% quarter-over-quarter, with a net interest margin of 2.05%. The slight quarterly decline was attributed to competitive pressures in certain markets, though loan volume growth of 7% year-over-year helped support overall interest income.

The following chart illustrates KBC’s net interest income performance over the past five quarters:

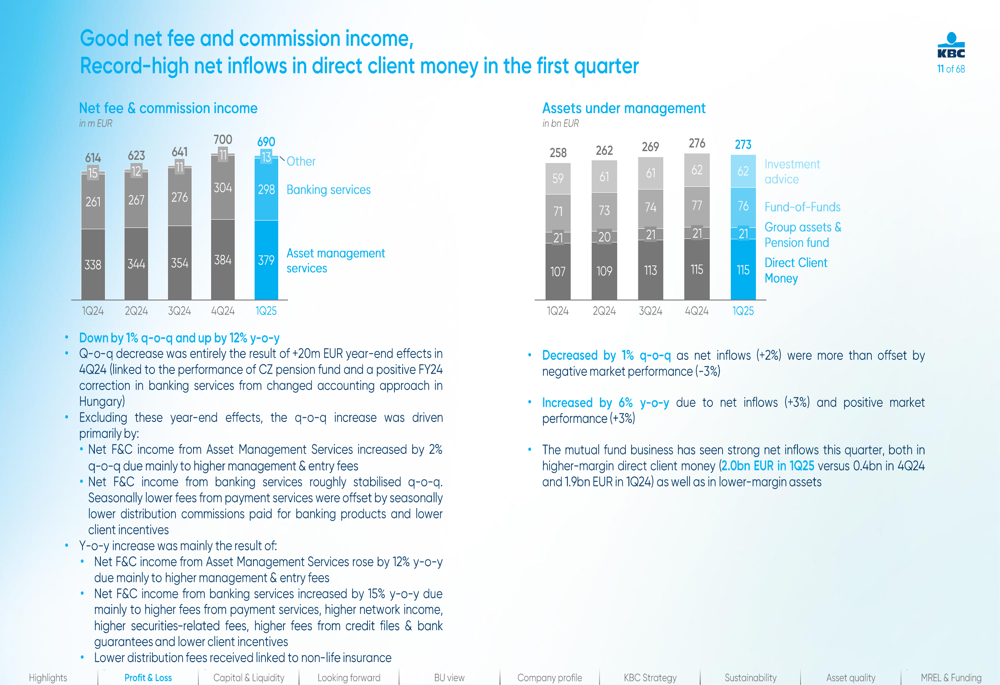

Fee and commission income showed particularly strong performance, reaching €690 million, up 12% year-over-year despite a slight 1% decrease from the previous quarter. Assets under management stood at €273 billion, with net inflows of direct client money reaching €2 billion during the quarter, offset partially by negative market performance of -3%.

The fee and commission income growth reflects KBC’s successful efforts to diversify revenue streams, as illustrated in this breakdown:

Insurance activities continued to contribute significantly to KBC’s results, with non-life sales increasing by 8% year-over-year to €792 million. Life insurance sales showed even stronger growth, rising 39% quarter-over-quarter to €1,013 million, driven primarily by higher sales of unit-linked products.

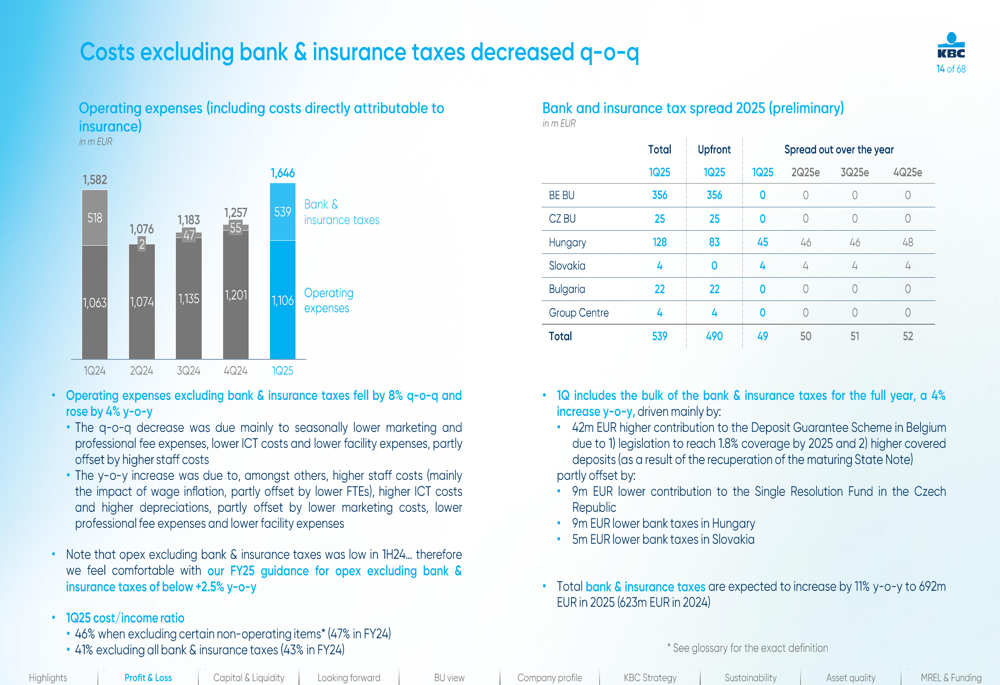

The first quarter traditionally includes the bulk of bank and insurance taxes for the full year, which amounted to €539 million. Excluding these taxes, operating expenses increased by 4% year-over-year to €1,646 million, reflecting inflationary pressures and continued investments in digital transformation.

Credit quality remained strong, with the credit cost ratio at just 0.08%, well below the through-the-cycle guidance of 25-30 basis points. The impaired loans ratio stood at 1.9%, reflecting the bank’s prudent risk management approach.

Strategic Initiatives

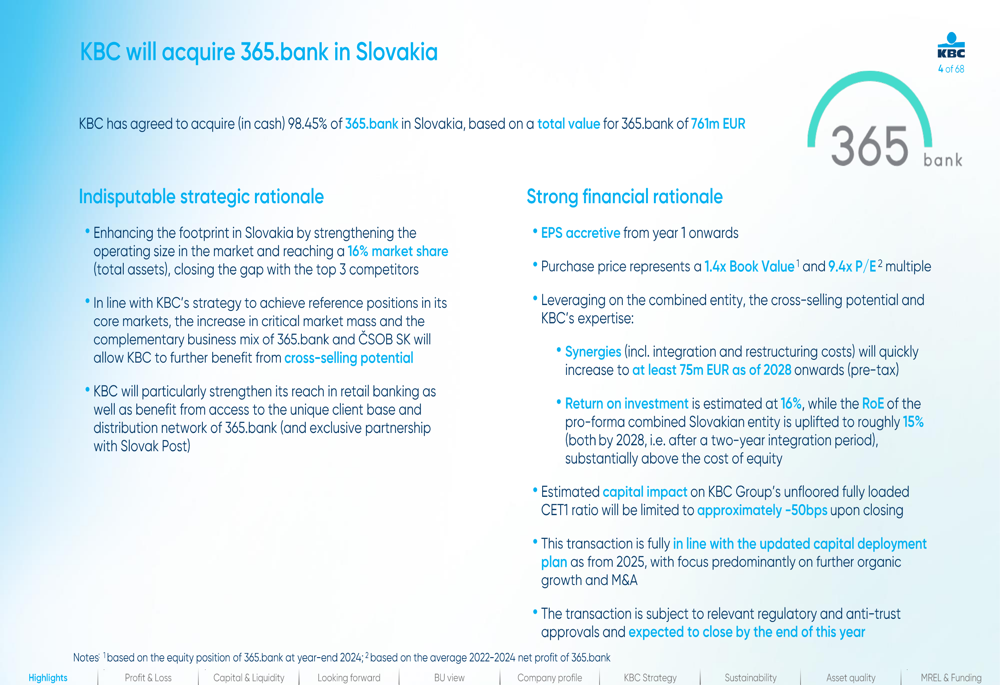

A major highlight of the quarter was KBC’s agreement to acquire 98.45% of 365.bank in Slovakia for €761 million, a strategic move to strengthen its position in Central and Eastern Europe. The acquisition will enhance KBC’s footprint in Slovakia, increasing its market share to 16% and creating significant cross-selling opportunities.

The financial rationale for the acquisition includes expected earnings per share accretion from year one, with synergies of at least €75 million annually from 2028 onwards. The purchase price represents 1.4x book value and a 9.4x P/E multiple, with an estimated return on investment of 16%.

As shown in the following slide, the acquisition aligns with KBC’s strategy of achieving reference positions in its core markets:

KBC also announced an updated dividend and capital deployment policy effective January 1, 2025, under Basel 4 regulations. The new policy includes a payout ratio between 50%-65% of consolidated profit and an interim dividend of €1 per share in November of each accounting year as an advance on the total dividend.

The capital deployment policy emphasizes KBC’s aim to be among the better capitalized financial institutions in Europe, with a focus on organic growth and potential M&A opportunities. The bank has set a minimum unfloored fully loaded CET1 ratio of 13% under Basel 4.

Digital Transformation and Competitive Positioning

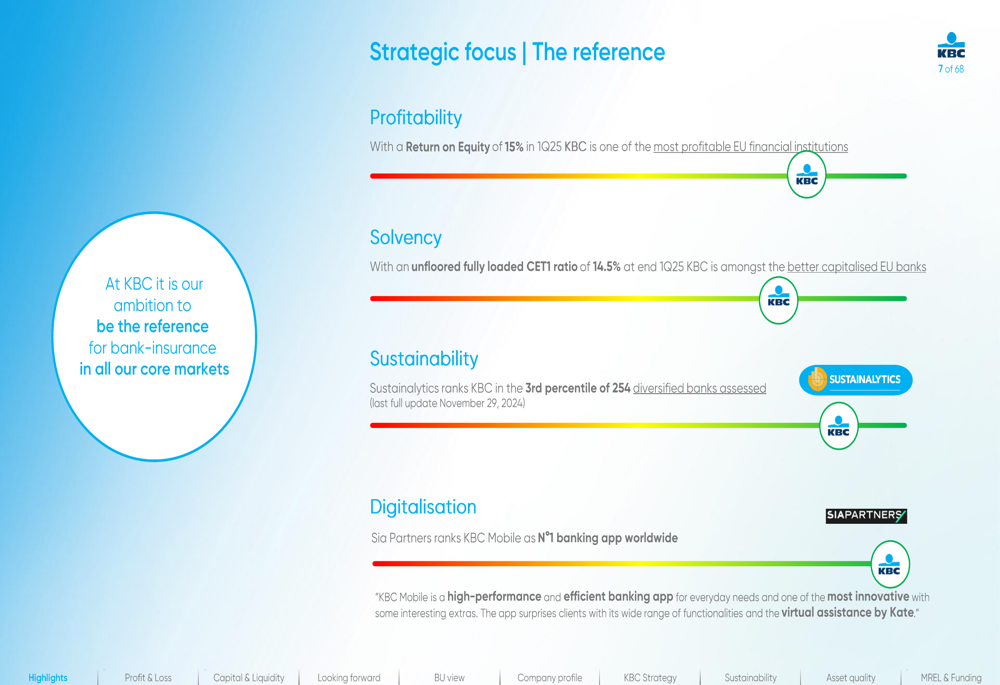

KBC continues to position itself as a digital-first, data-driven, and AI-led integrated bank-insurer. The company’s mobile banking app was ranked number one worldwide in 2024, according to Sia Partners, reinforcing its leadership in digital banking.

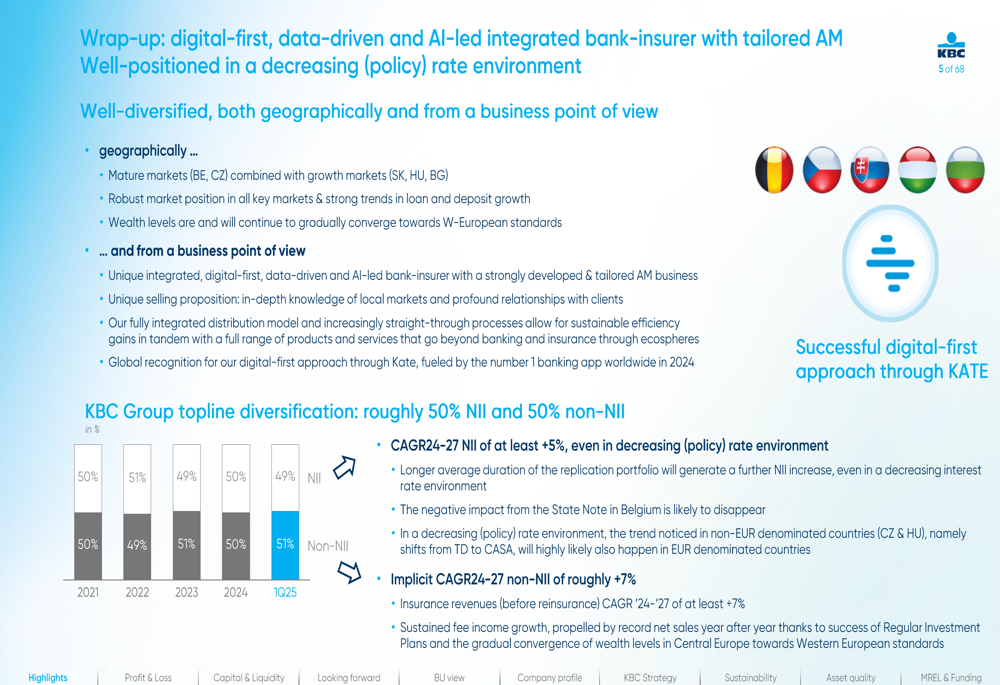

The bank’s digital assistant, Kate, now has 5.5 million users across the group, demonstrating strong customer adoption of KBC’s digital tools. This digital-first approach supports the bank’s diversified business model, which balances mature markets like Belgium and the Czech Republic with growth markets in Slovakia, Hungary, and Bulgaria.

The following slide illustrates KBC’s strategic positioning and competitive strengths:

KBC’s integrated bank-insurance model continues to deliver benefits in terms of income and risk diversification. Insurance activities contributed 26% of the group’s net result in the first quarter, highlighting the value of this integrated approach.

The bank’s business model is also well-diversified from a revenue perspective, with approximately 50% coming from net interest income and 50% from non-interest income sources. This balance provides resilience against fluctuations in interest rates and market conditions.

Forward-Looking Statements

Despite increasing volatility in the macroeconomic environment toward the end of the first quarter, KBC maintained its financial guidance for both 2025 and the longer term through 2027.

For the full year 2025, KBC expects total income growth of at least 5.5% year-over-year, with net interest income of at least €5.7 billion and organic loan volume growth of 4%. Insurance revenues are projected to increase by at least 7% year-over-year, while operating expenses (excluding bank/insurance taxes) are expected to grow by less than 2.5%.

Looking further ahead to 2027, KBC aims for a compound annual growth rate of at least 6% for total income between 2024 and 2027, with net interest income growing at a rate of at least 5% and insurance revenues at a minimum of 7%. The bank expects to maintain a combined ratio below 91% and a credit cost ratio well below its through-the-cycle guidance of 25-30 basis points.

As the first quarter results demonstrate, KBC’s diversified business model, strong capital position (CET1 ratio of 14.5%), and strategic initiatives position the bank well to achieve these targets despite potential economic headwinds.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.