S&P 500 jumps as tech rallies as investors eye end of government shutdown

Introduction & Market Context

KBR Inc (NYSE:KBR) released its second quarter 2025 earnings presentation on July 31, 2025, revealing a mixed financial picture with solid bottom-line growth despite challenges in certain business segments. The company’s stock traded down in pre-market activity, falling 1.76% to $44.72, extending the previous day’s 2.28% decline.

The engineering and government services contractor reported revenue and profit growth while simultaneously announcing a significant reduction to its full-year revenue guidance, maintaining its profitability targets. This comes as KBR navigates a complex environment of government contract delays, geopolitical tensions, and strategic repositioning following the wind-down of its HomeSafe Alliance joint venture.

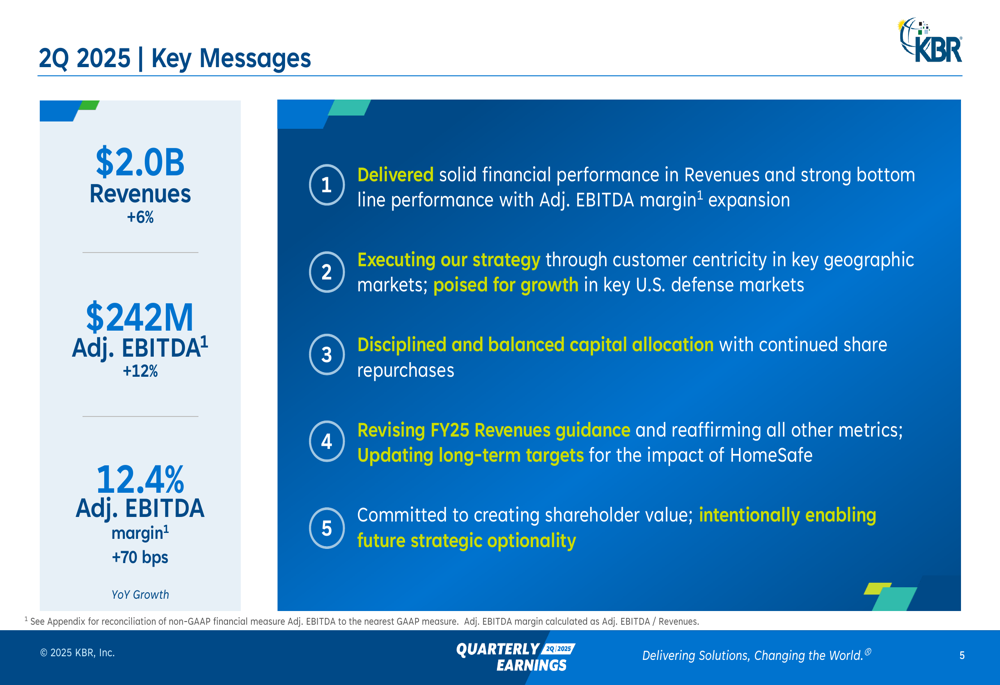

As shown in the following summary slide from KBR’s presentation, the company achieved solid financial performance with expanding margins:

Quarterly Performance Highlights

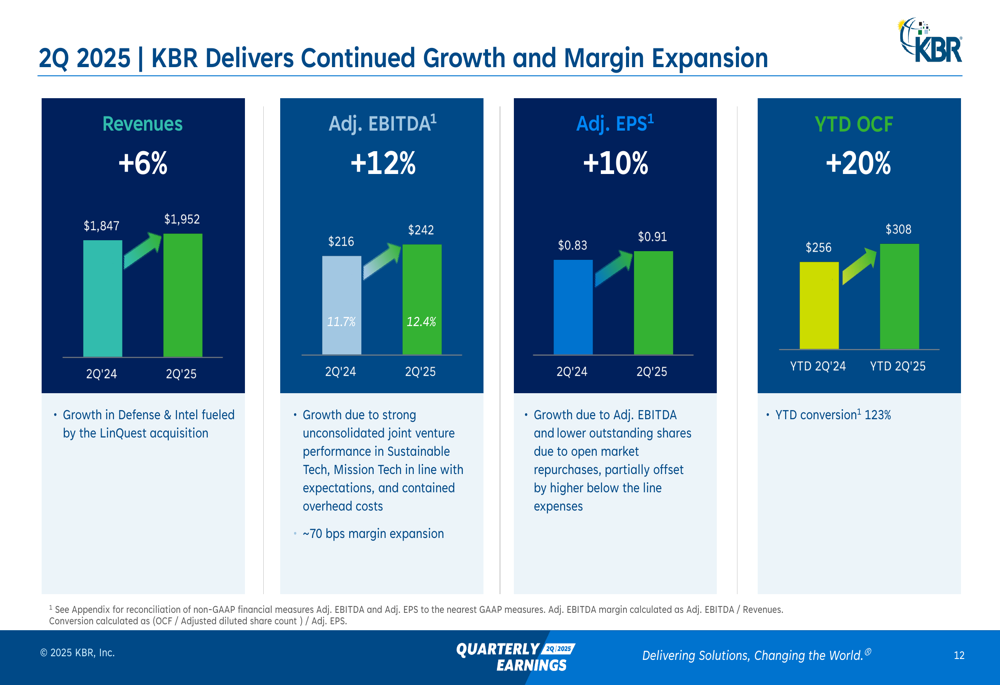

KBR delivered revenue of $1.952 billion in Q2 2025, representing a 6% increase year-over-year. More impressively, adjusted EBITDA grew 12% to $242 million, resulting in a 70 basis point expansion in adjusted EBITDA margin to 12.4%. Adjusted earnings per share increased 10% to $0.91, while year-to-date operating cash flow showed robust 20% growth to $308 million.

The company’s performance is visually represented in the following financial results slide:

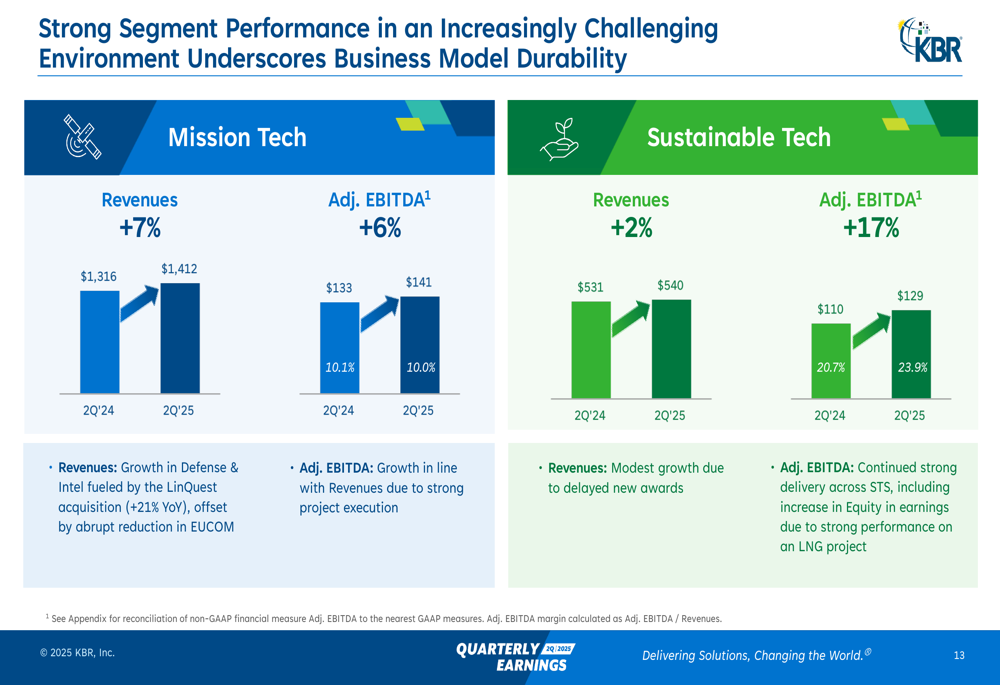

KBR’s business segments showed divergent performance patterns. The Mission Technology Solutions (MTS) segment, which accounts for approximately 72% of total revenue, grew 7% to $1.412 billion with a 6% increase in adjusted EBITDA to $141 million. This growth was primarily driven by the LinQuest acquisition in the Defense & Intelligence sector, though partially offset by an unexpected reduction in EUCOM activities.

Meanwhile, the Sustainable Technology Solutions (STS) segment demonstrated modest 2% revenue growth to $540 million but delivered impressive 17% adjusted EBITDA growth to $129 million. This strong bottom-line performance was attributed to successful project execution and increased equity earnings from an LNG project.

The segment breakdown is illustrated in the following slide:

Guidance Revision & Long-Term Outlook

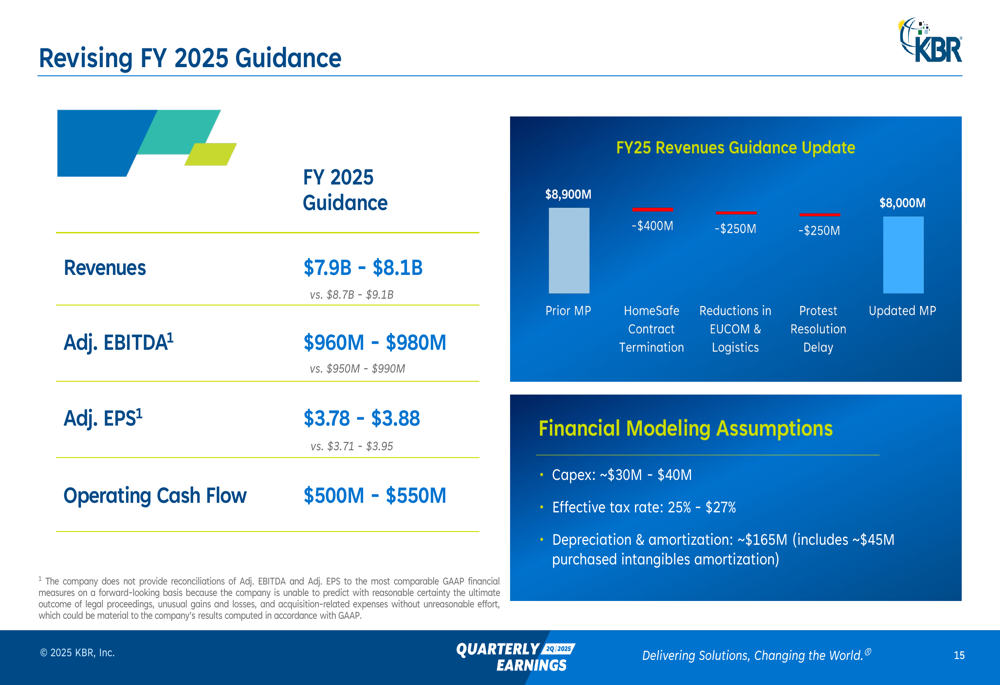

In a significant development, KBR revised its fiscal year 2025 revenue guidance downward to $7.9-$8.1 billion from the previous $8.7-$9.1 billion. This reduction was attributed to three main factors: reductions in EUCOM and logistics operations, the HomeSafe contract termination, and delays in protest resolution for pending contract awards.

Despite the revenue guidance cut, the company maintained its adjusted EBITDA guidance at $960-$980 million (slightly narrowed from $950-$990 million) and adjusted EPS at $3.78-$3.88 (tightened from $3.71-$3.95). This suggests management’s confidence in achieving margin expansion and cost efficiencies despite top-line challenges.

The revised guidance is detailed in the following slide:

Looking further ahead, KBR also updated its FY 2027 financial targets to account for the HomeSafe impact. The company now projects revenues of $9.0+ billion, with Mission Tech growing at 5-8% CAGR and Sustainable Tech at 11-15% CAGR. Adjusted EBITDA is targeted at $1.15+ billion with segment margins of 10%+ for MTS and 20%+ for STS. Operating cash flow is expected to reach $650+ million with cumulative deployable free cash of approximately $2.0 billion.

The long-term targets are presented in this slide:

Strategic Initiatives & Contract Wins

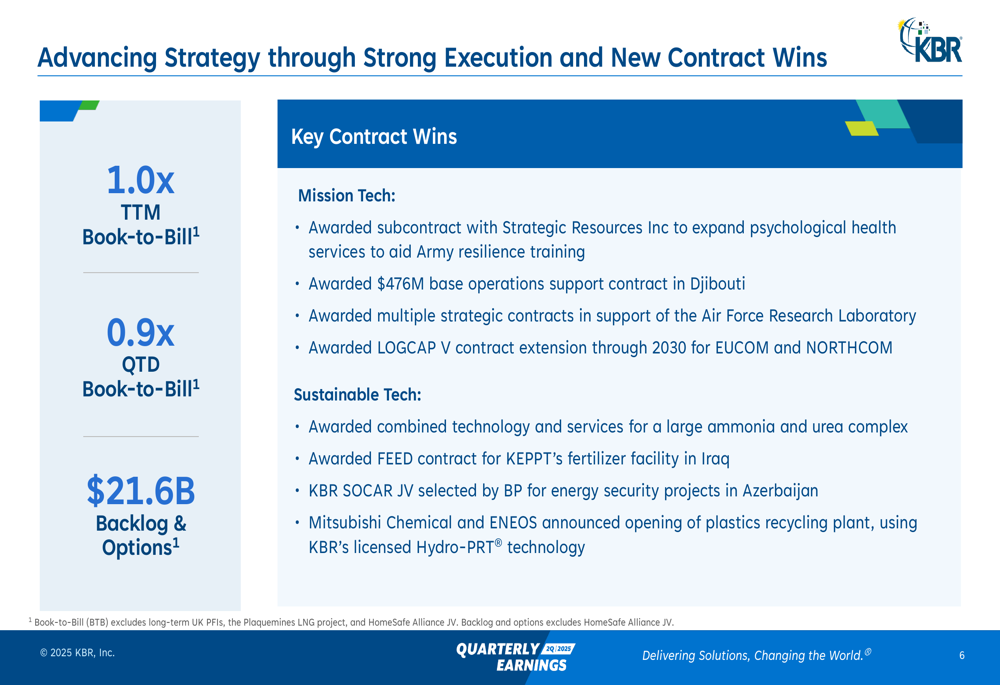

KBR continues to advance its strategy through new contract wins and market positioning. The company reported a trailing twelve-month book-to-bill ratio of 1.0x, indicating stable order momentum, though the quarter-to-date ratio was slightly lower at 0.9x. Total (EPA:TTEF) backlog and options stood at $21.6 billion, providing revenue visibility for future periods.

Notable contract wins in the Mission Tech segment included a $476 million base operations support contract in Djibouti, multiple strategic contracts supporting the Air Force Research Laboratory, and a LOGCAP V contract extension through 2030 for EUCOM and NORTHCOM. In the Sustainable Tech segment, KBR secured technology and services contracts for ammonia and urea complexes, a FEED contract for KEPPT’s fertilizer facility in Iraq, and selection by BP (NYSE:BP) for energy security projects in Azerbaijan.

The company’s contract momentum is highlighted in this slide:

KBR emphasized its strategic alignment with government budget priorities, particularly in defense, research, development, testing, and evaluation (RDT&E), and space exploration. The company noted increased funding for the U.S. Space Force, missile defense systems, and NASA’s space exploration initiatives, all areas where KBR has established capabilities and contracts.

The Middle East remains a key growth market for KBR, where the company leverages its deep local engagement, strong partnerships, and advanced digital capabilities. This regional focus aligns with KBR’s broader strategy to thrive and expand in core markets while capturing new growth opportunities.

Capital Allocation & Balance Sheet

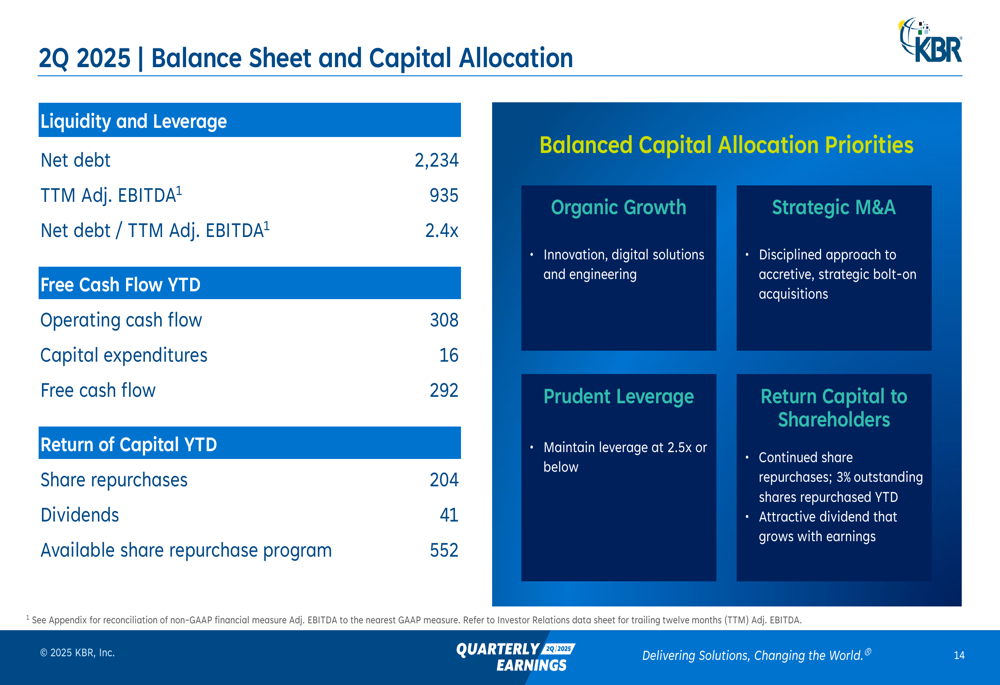

KBR maintained a disciplined approach to capital allocation, balancing investments in growth, strategic M&A, debt management, and shareholder returns. The company reported net debt of $2,234 million with a net debt to TTM adjusted EBITDA ratio of 2.4x, indicating reasonable leverage.

Year-to-date free cash flow reached $292 million, calculated as $308 million in operating cash flow less $16 million in capital expenditures. KBR returned significant capital to shareholders, with $204 million in share repurchases and $41 million in dividends year-to-date. The company has $552 million remaining in its share repurchase authorization.

The balance sheet and capital allocation details are presented in this slide:

Forward-Looking Statements

In summarizing the quarter, CEO Stuart Bradie emphasized KBR’s execution of its strategy through customer centricity in key geographic markets and positioning for growth in U.S. defense markets. The company remains committed to disciplined capital allocation and creating shareholder value while enabling future strategic optionality.

Despite the revenue guidance reduction, management expressed confidence in the company’s long-term growth trajectory, supported by its alignment with secular trends in global security, sustainability, and digitalization. The company’s investment thesis centers on its transformation into a provider of differentiated, innovative science, technology, and engineering solutions with global reach and expertise in complex, mission-critical work.

As KBR navigates the challenges of delayed contract decisions and shifting government priorities, its diversified business model, strong cash flow generation, and margin expansion capabilities position it to deliver long-term value to shareholders, even as near-term revenue growth faces headwinds.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.