Bitcoin price today: falls to 2-week low below $113k ahead of Fed Jackson Hole

Introduction & Market Context

KCB Group Plc presented its H1 2025 financial performance on August 13, 2025, highlighting an 8% increase in net profit amid a challenging but stabilizing regional economic environment. The East African banking giant maintained its position as the largest financial institution in the region with a steady balance sheet of Ksh 2.0 trillion following the strategic divestiture of National Bank of Kenya (NBK).

The presentation revealed that KCB operated in a context of "higher-for-longer interest rates" while benefiting from "stable currencies in most markets," with the Kenyan, Tanzanian, and Ugandan shillings appreciating against the US dollar year-over-year. The bank also noted "resilient GDP growth" projected at 5.7% across its markets despite ongoing global geopolitical challenges.

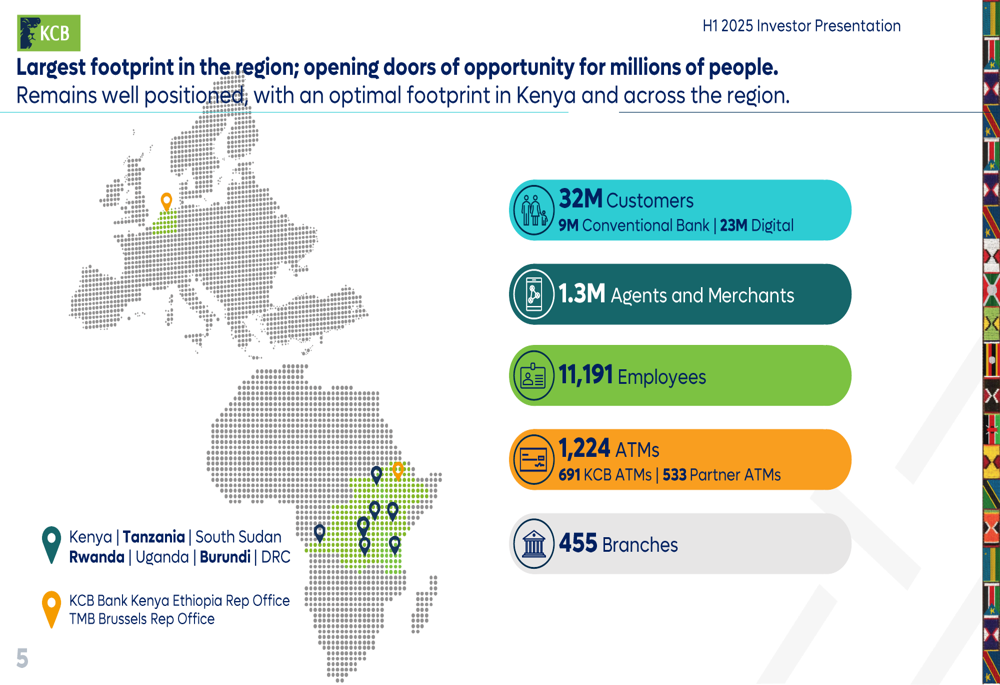

As shown in the following regional footprint map, KCB maintains a significant presence across East Africa:

Financial Performance Highlights

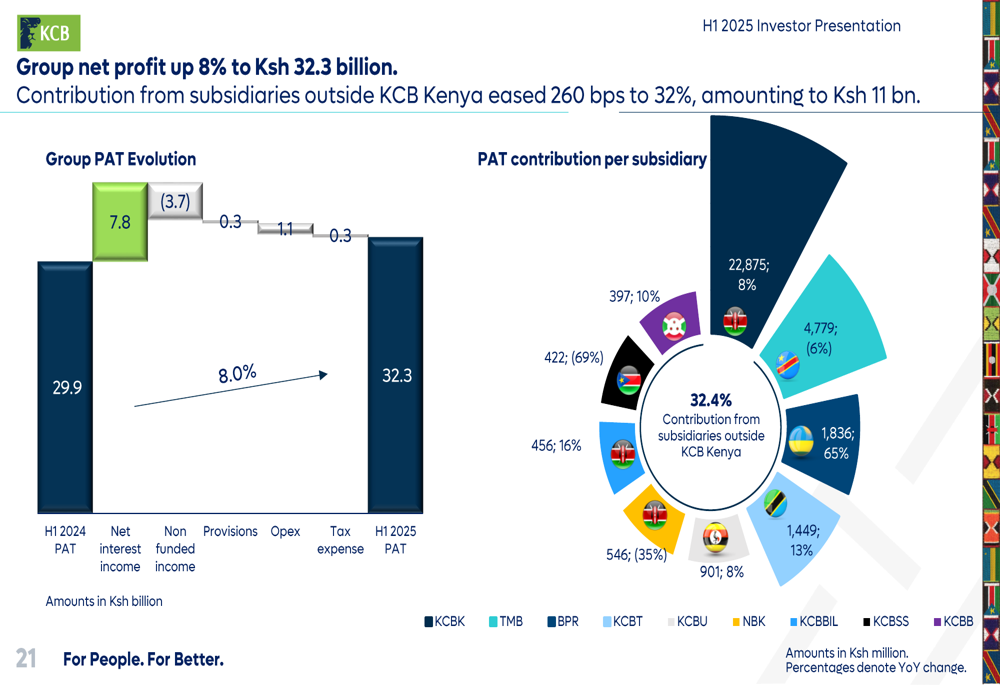

KCB Group reported a net profit of Ksh 32.3 billion for H1 2025, representing an 8% increase compared to the same period in 2024. The bank announced its largest interim and special dividend to date, amounting to Ksh 13 billion, demonstrating confidence in its financial position and commitment to shareholder returns.

The presentation highlighted that while subsidiaries outside Kenya continue to make substantial contributions to the group’s performance, their share of profits decreased slightly:

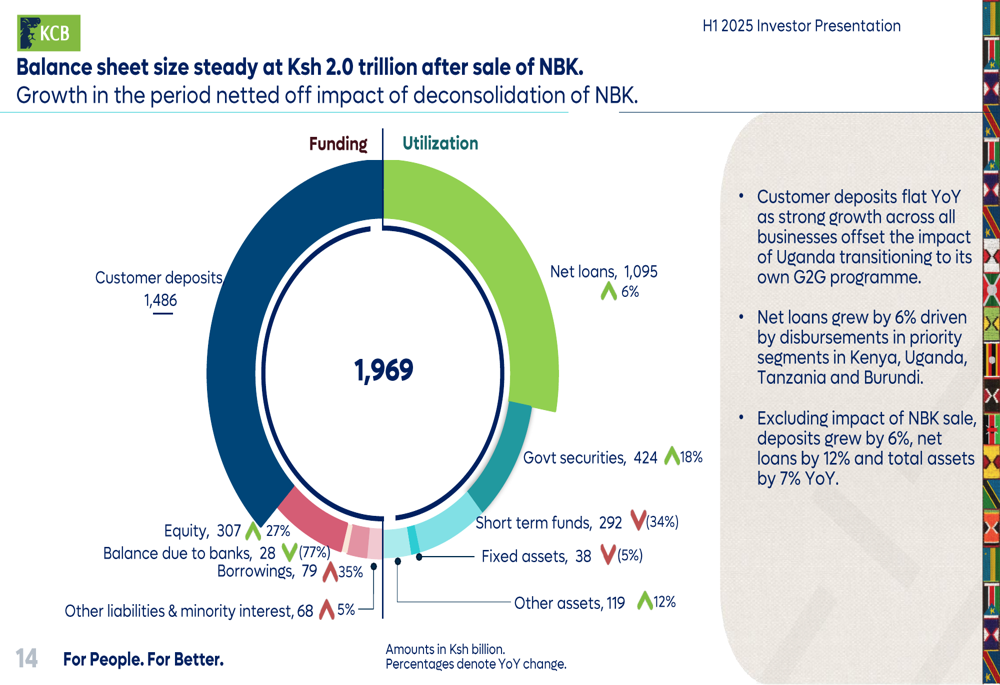

The bank’s balance sheet remained steady at Ksh 2.0 trillion, with customer deposits of Ksh 1,486 billion and net loans of Ksh 1,095 billion. Government securities accounted for Ksh 424 billion, while equity stood at Ksh 307 billion. This balanced asset allocation is illustrated in the following chart:

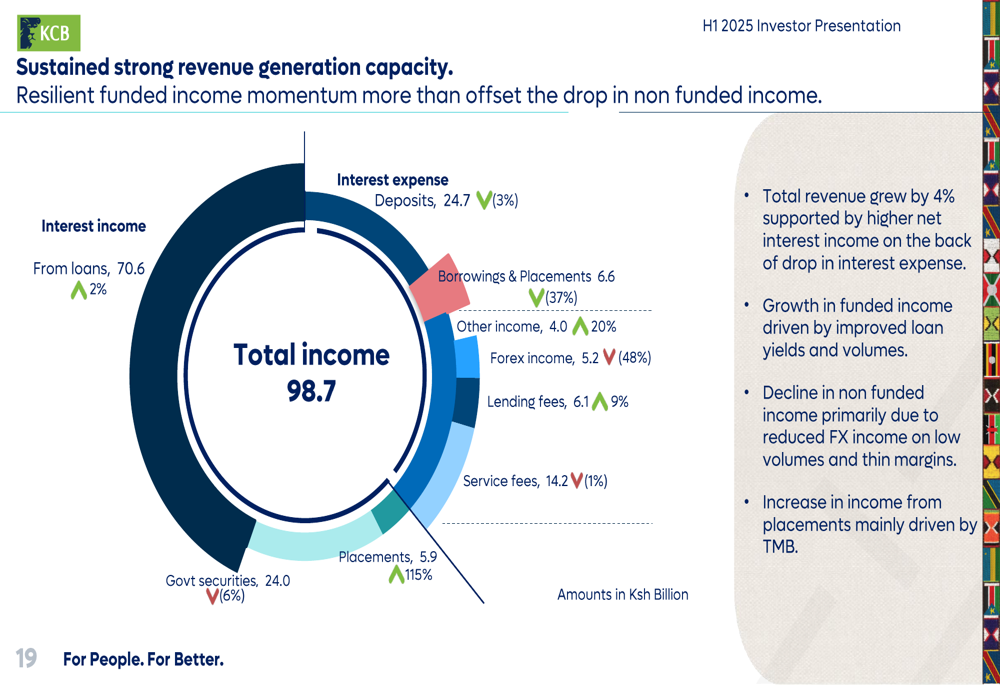

Revenue generation remained strong with total income growing by 4%, driven primarily by resilient funded income which offset a decrease in non-funded income. The bank’s cost-to-income ratio improved to 46.0%, down from 46.8% in H1 2024, reflecting positive cost management despite a 2.4% increase in total operating costs related to variable expenses and strategic investments.

Digital Transformation & Channel Performance

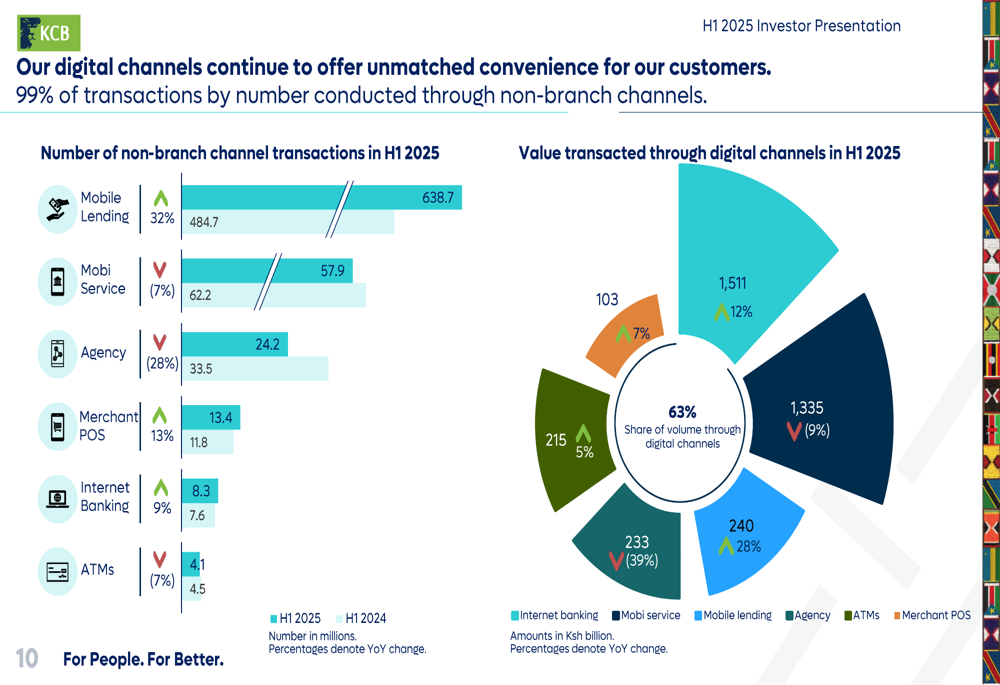

KCB’s digital transformation strategy continued to yield impressive results, with 99% of all transactions now conducted through non-branch channels. Mobile lending dominated the digital landscape with 638.7 million transactions in H1 2025, representing a 32% year-over-year increase.

The following chart illustrates the distribution of transactions across KCB’s digital channels:

The bank’s customer base has grown to 32 million, with 23 million using digital channels and 9 million utilizing conventional banking services. This digital-first approach is supported by 1.3 million agents and merchants, complementing the physical network of 455 branches and 1,224 ATMs across the region.

Strategic Initiatives & Regional Expansion

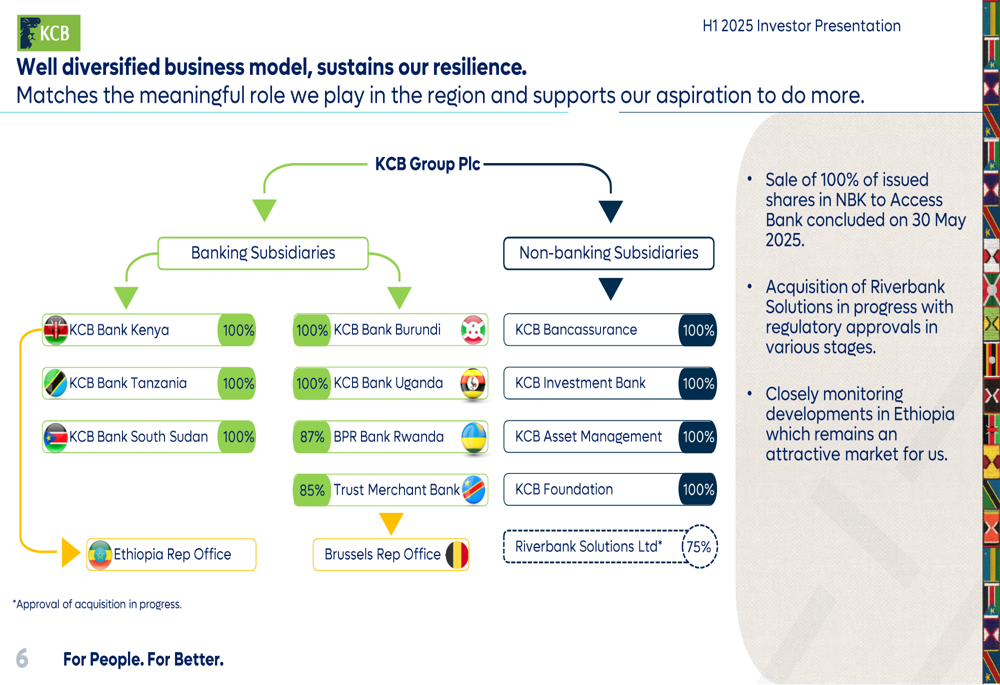

KCB completed several strategic initiatives during the period, most notably concluding the sale of National Bank of Kenya (NBK) to Access Bank on May 30, 2025. The group is also in the process of acquiring a 75% stake in Riverbank Solutions Ltd, which will further enhance its digital capabilities.

The bank’s diversified business model spans both banking and non-banking subsidiaries across seven countries, creating a resilient operational structure:

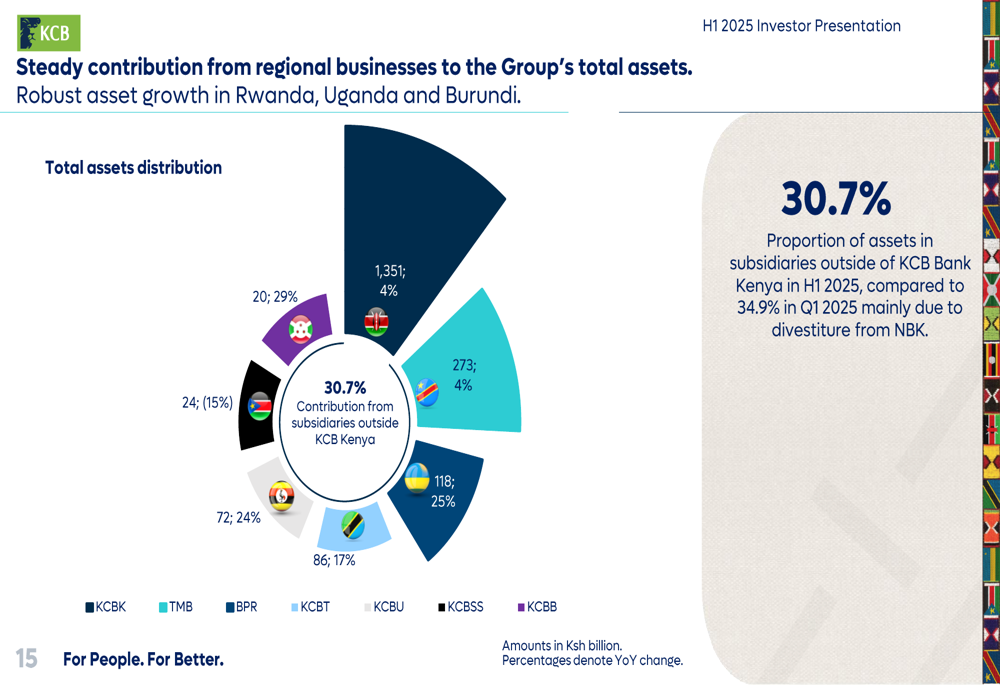

Regional subsidiaries contributed 30.7% to the group’s total assets, with particularly robust asset growth in Rwanda, Uganda, and Burundi. This geographic diversification helps mitigate country-specific risks while providing multiple growth avenues.

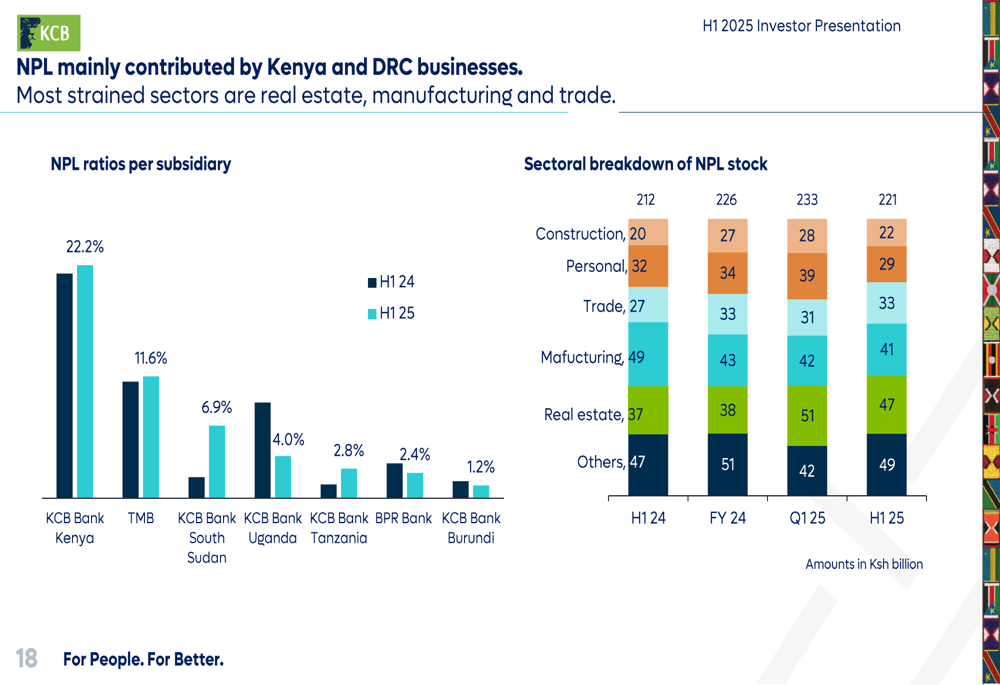

Asset Quality & Risk Management

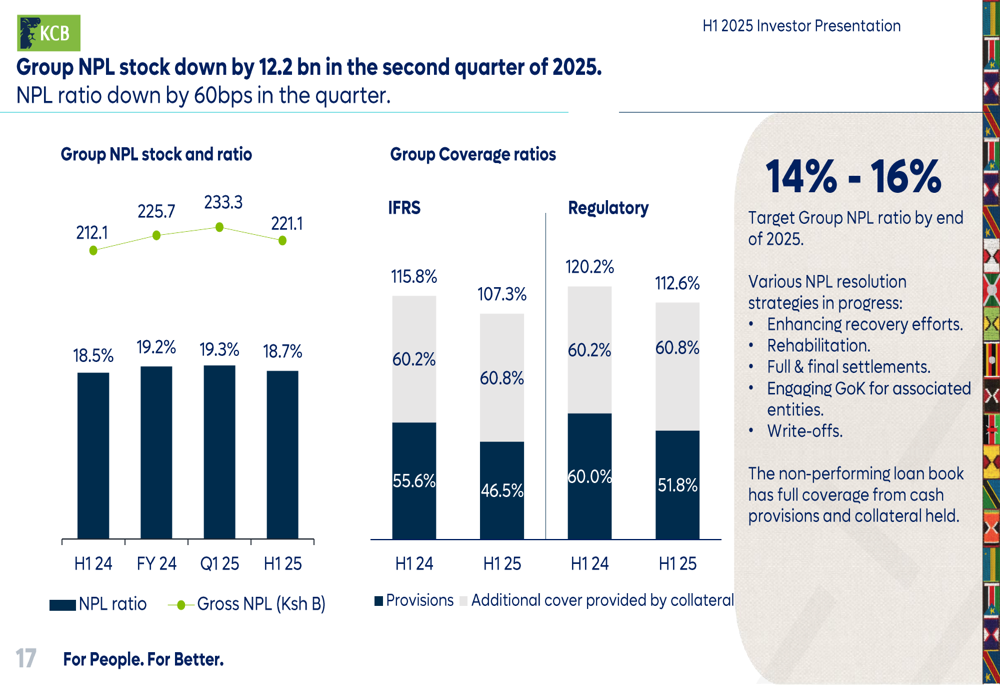

KCB reported significant improvement in asset quality, with Group NPL stock decreasing by Ksh 12.2 billion in the second quarter of 2025. The NPL ratio declined by 60 basis points during the quarter, though the bank continues to target an NPL ratio of 14%-16% by the end of 2025.

The following chart shows the declining trend in NPL stock and improving coverage ratios:

The presentation revealed that NPLs are primarily concentrated in the Kenya and DRC operations, with the most stressed sectors being real estate, manufacturing, and trade. This sectoral analysis provides insight into KCB’s credit risk exposure:

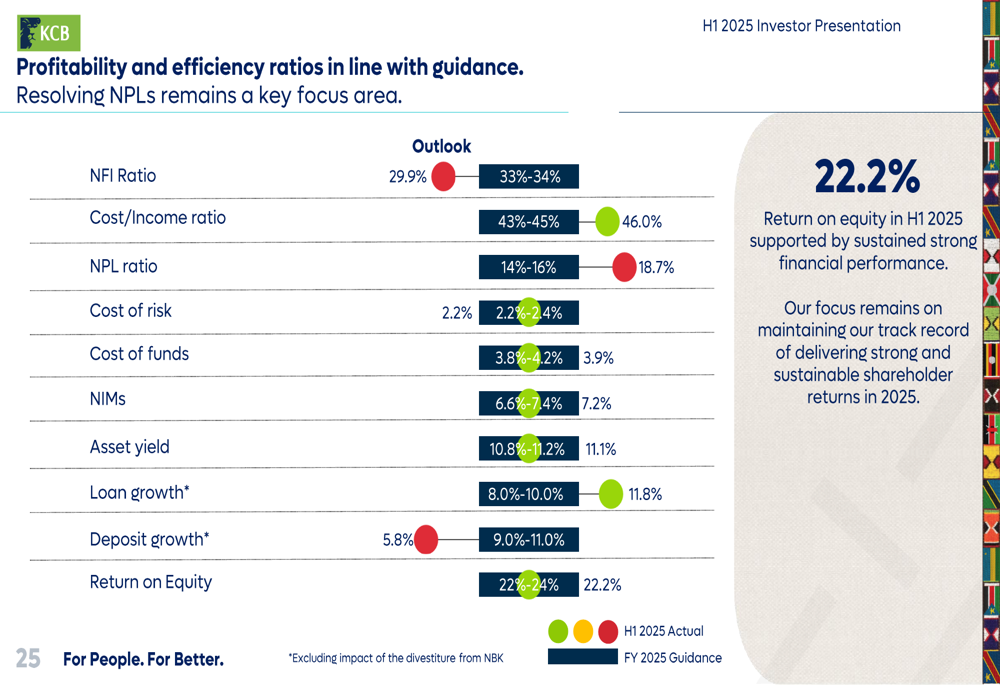

Forward Outlook

KCB’s profitability and efficiency ratios remain largely in line with management guidance, as shown in the comprehensive performance scorecard:

The bank maintains adequate capital to drive growth, with core capital buffers for KCB Bank Kenya standing at 470 basis points above the regulatory minimum. Return on Equity remains strong across all business units, reflecting efficient capital allocation strategies.

Looking ahead, KCB’s 2024-2026 strategy focuses on customer-centered value propositions, leveraging group capabilities for efficient scale, digital leadership, and optimizing data and analytics. The bank has expressed confidence in delivering incremental growth in shareholder returns through "diligent strategy execution" while continuing to address NPL resolution as a key focus area.

With its strong regional presence, improving operational efficiency, and strategic investments in digital transformation, KCB appears well-positioned to navigate the evolving financial landscape in East Africa despite ongoing macroeconomic challenges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.