Nvidia among investors in xAI’s $20 bln capital raise- Bloomberg

Introduction & Market Context

Kennametal Inc (NYSE:KMT) released its fourth quarter and full-year fiscal 2025 results on August 6, 2025, revealing persistent challenges across its industrial markets. The company’s shares tumbled 8.52% in premarket trading to $22.99, reflecting investor concerns about both the quarterly performance and the weaker-than-expected outlook for fiscal 2026.

The industrial tooling and materials specialist faced significant headwinds from softening industrial demand, supply chain disruptions, and tariff uncertainties, which collectively pressured sales volumes and margins throughout the quarter and fiscal year.

Quarterly Performance Highlights

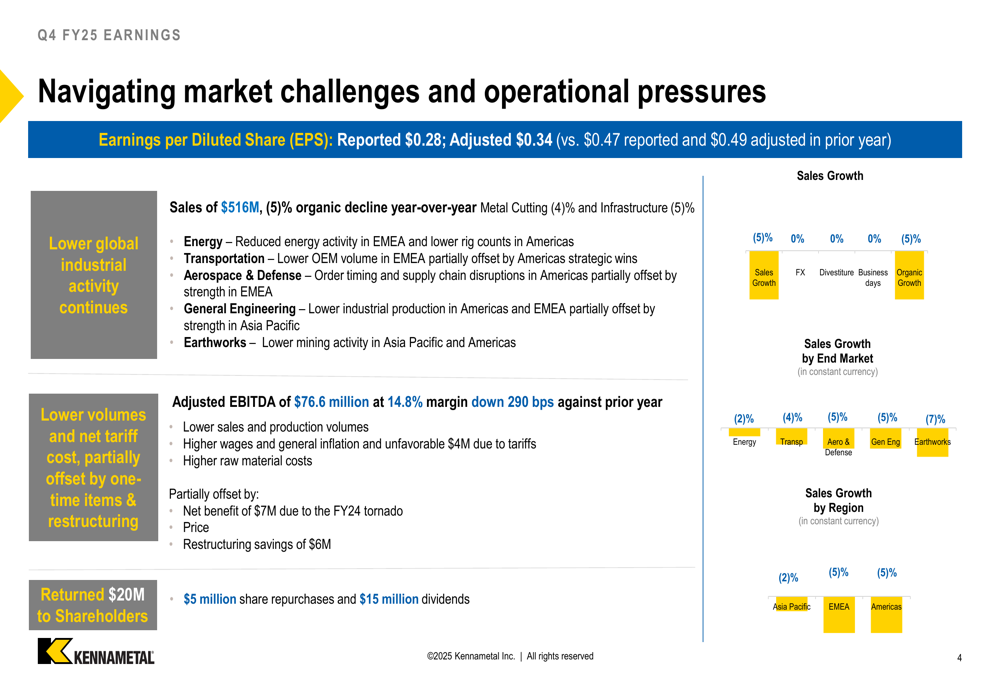

For the fourth quarter of fiscal 2025, Kennametal reported sales of $516 million, representing a 5% organic decline compared to the same period last year. Adjusted earnings per share fell to $0.34, down 31% from $0.49 in Q4 FY24, as operational challenges offset restructuring benefits.

The company’s performance was impacted by weakness across multiple sectors, including reduced activity in energy, lower OEM volume in transportation, order timing issues in aerospace and defense, lower production in general engineering, and decreased mining activity in earthworks.

As shown in the following quarterly performance breakdown:

Adjusted EBITDA for the quarter came in at $76.6 million with a margin of 14.8%, down 290 basis points year-over-year. The decline was primarily attributed to lower sales and production volumes, higher wages and general inflation, unfavorable tariffs, and higher raw material costs. These headwinds were partially offset by restructuring savings of $6 million and pricing actions.

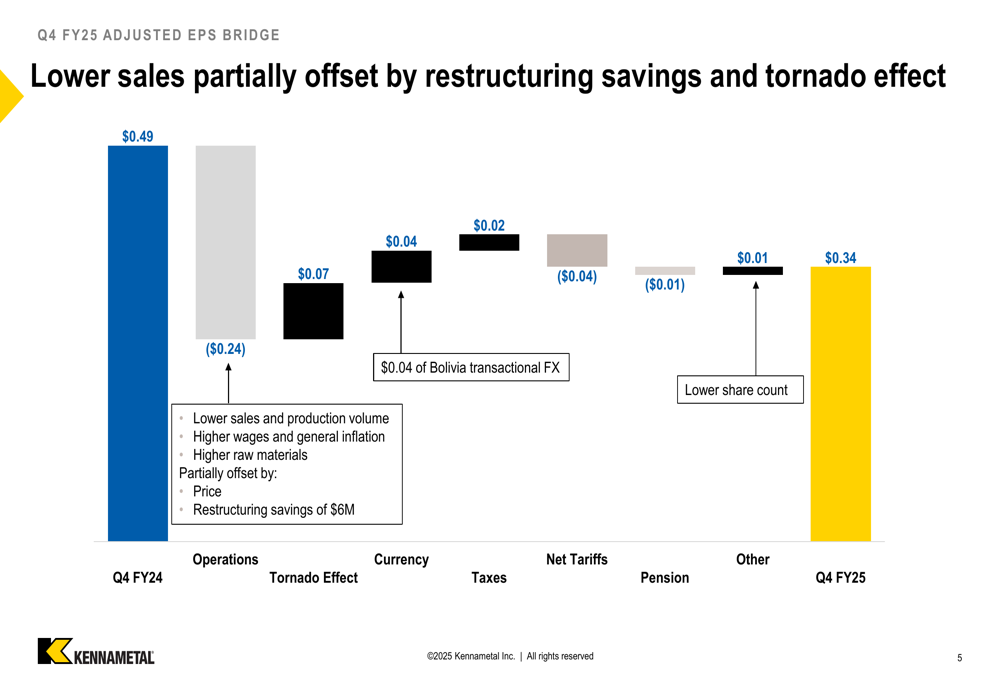

The following chart illustrates the factors affecting the company’s adjusted EPS performance:

Segment Performance

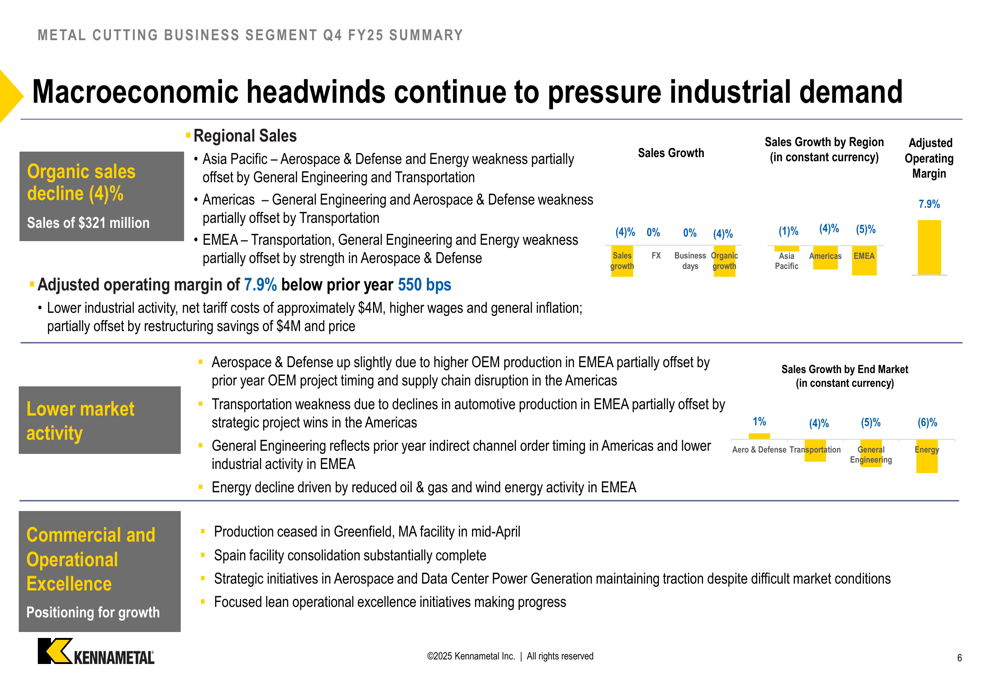

Kennametal’s Metal Cutting segment, which accounted for approximately 62% of total sales, experienced a 4% organic sales decline in Q4. The adjusted operating margin contracted significantly to 7.9%, down 550 basis points from the prior year, reflecting the impact of lower industrial activity, net tariff costs, and inflationary pressures.

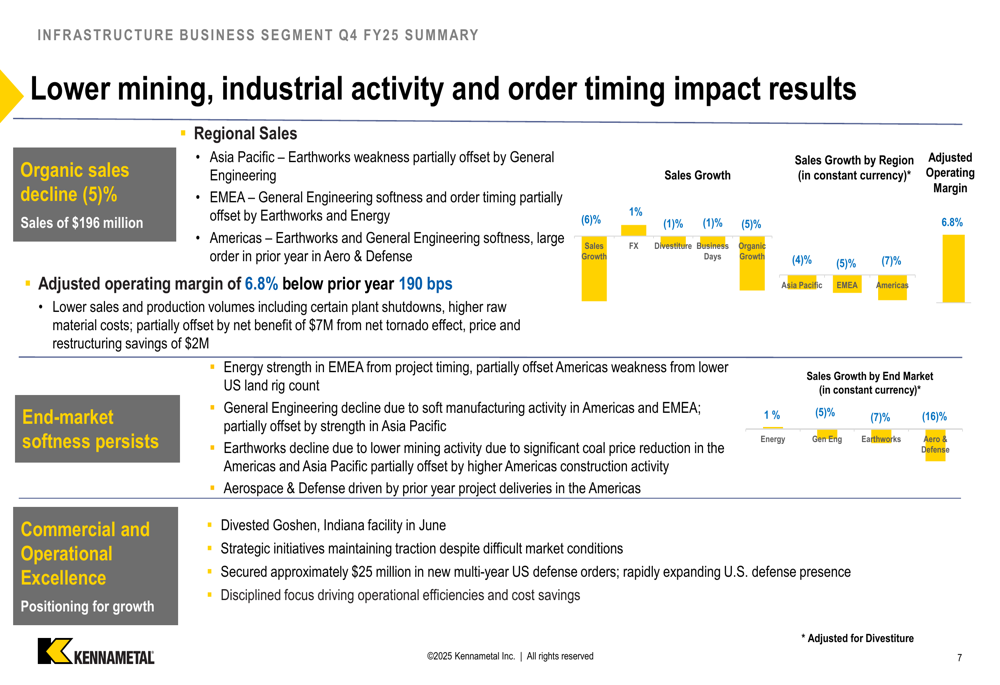

Similarly, the Infrastructure segment saw a 5% organic sales decline, with sales of $196 million. The adjusted operating margin was 6.8%, down 190 basis points from the previous year due to decreased sales, production volumes, and higher raw material expenses.

Full-Year Results

For the full fiscal year 2025, Kennametal reported:

- Sales of $1.967 billion, reflecting a 4% organic decline

- Adjusted EPS of $1.34, down from $1.50 in the prior year

- Adjusted EBITDA of $299 million with a 15.2% margin

- Cash from operations of $208 million, generating free operating cash flow of $121 million

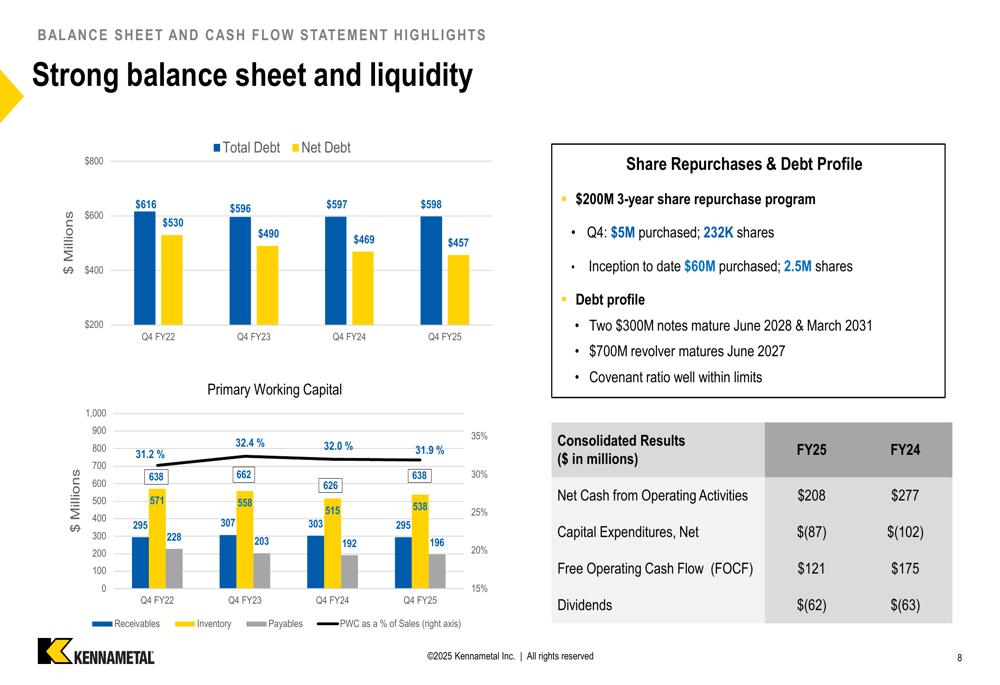

The company maintained its commitment to shareholder returns, distributing $122 million to shareholders through $60 million in share repurchases and $62 million in dividends. Kennametal also highlighted its strong balance sheet, with total debt of $598 million and net debt of $457 million at year-end.

Strategic Initiatives

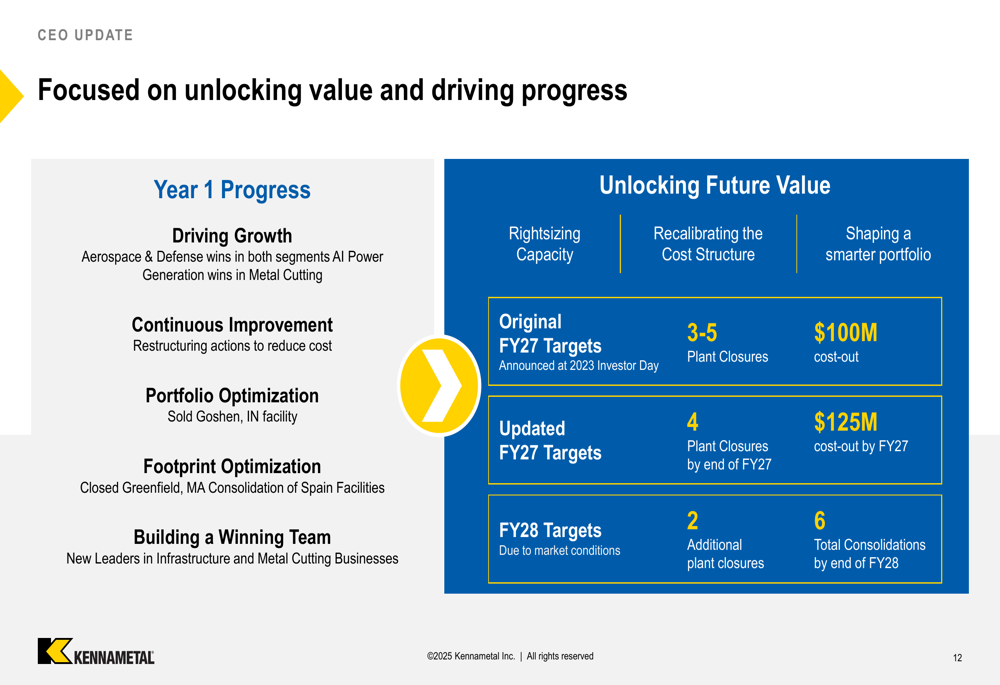

In response to the challenging market environment, Kennametal has accelerated its restructuring and cost-cutting initiatives. The company updated its restructuring targets, now planning to close four plants by the end of FY27 for a $125 million cost-out, followed by two additional plant closures by the end of FY28, bringing the total to six consolidations.

These strategic actions are part of the company’s broader effort to rightsize capacity, recalibrate its cost structure, and shape a smarter portfolio to enhance long-term competitiveness and profitability.

Forward-Looking Statements

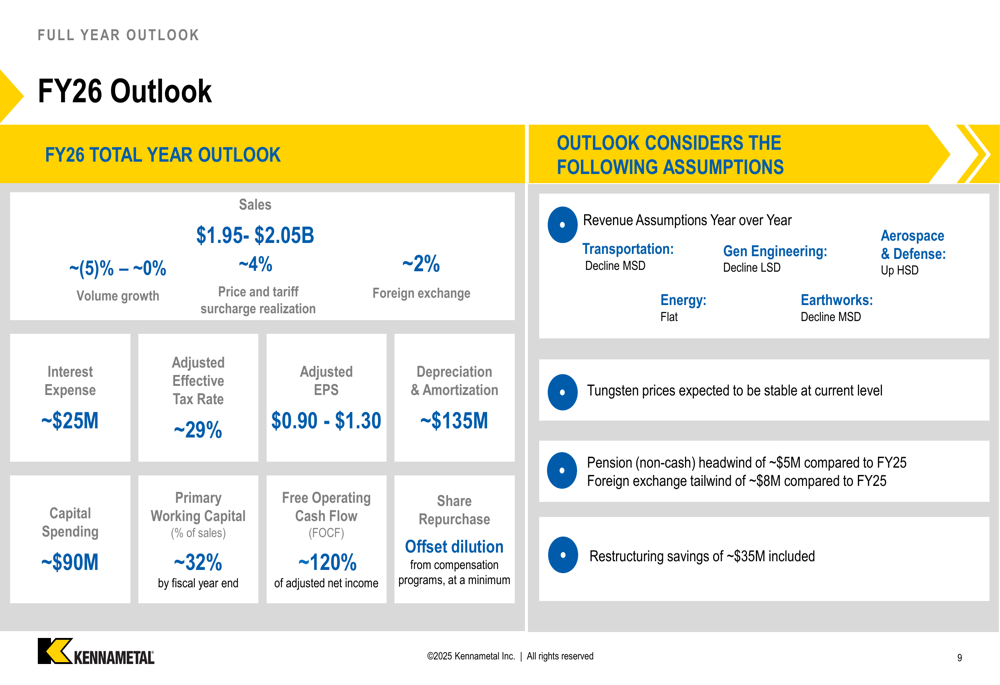

Kennametal’s outlook for fiscal 2026 suggests continued challenges ahead. The company projects sales between $1.95 billion and $2.05 billion, with volume growth ranging from approximately -5% to 0%. This guidance incorporates a ~4% benefit from price and tariff surcharge realization and a ~2% impact from foreign exchange.

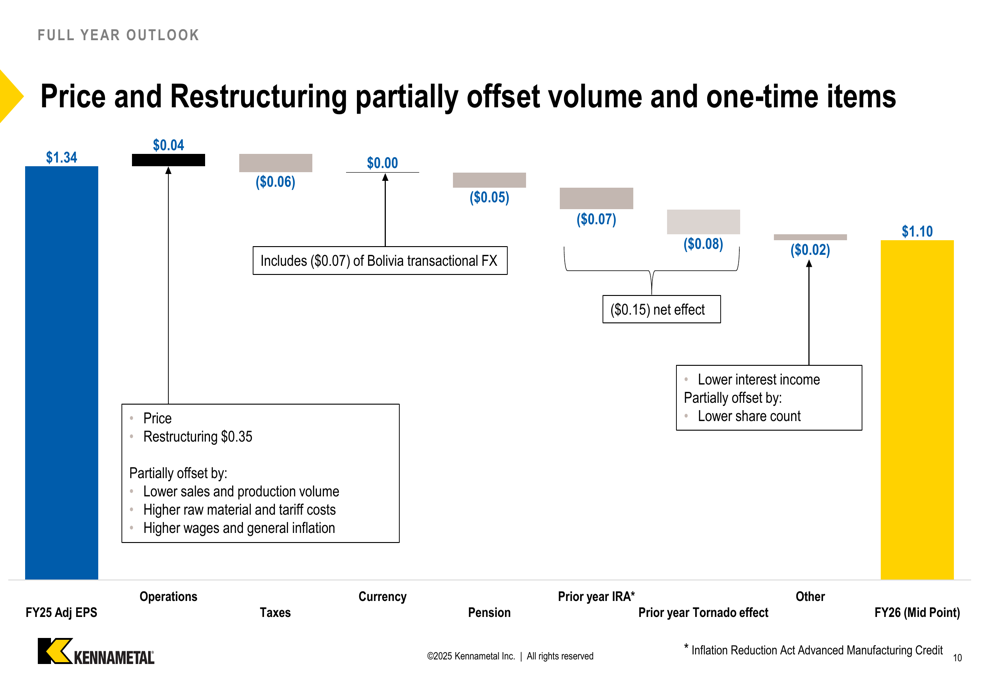

Notably, the company expects adjusted EPS to range from $0.90 to $1.30 for FY26, with the midpoint of $1.10 representing a significant decline from the $1.34 reported in FY25. The following bridge chart illustrates the factors expected to impact EPS in the coming fiscal year:

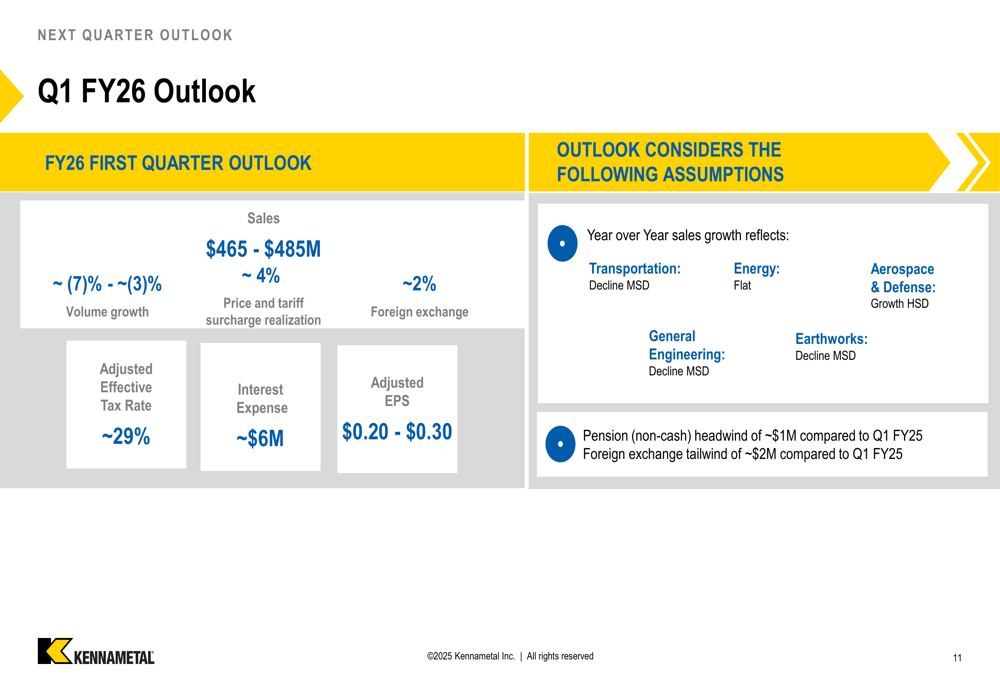

For the first quarter of fiscal 2026, Kennametal anticipates sales between $465 million and $485 million, with adjusted EPS in the range of $0.20 to $0.30.

Market Reaction

The market’s negative reaction to Kennametal’s results and outlook stands in stark contrast to the company’s performance just one quarter ago. In Q3 FY25, Kennametal had significantly outperformed expectations with an adjusted EPS of $0.47 versus a forecast of $0.25, driving cautious optimism among investors.

However, the combination of disappointing Q4 results and a weaker-than-expected FY26 outlook has erased those gains, with the stock now trading well below its 52-week high of $32.18. The 8.52% premarket decline suggests investors are concerned about the company’s ability to navigate the persistent macroeconomic headwinds and generate growth in the coming fiscal year.

The stock had already experienced significant pressure prior to this earnings release, declining 31.4% over the past six months according to previous reports, and today’s reaction indicates continued investor skepticism about Kennametal’s near-term prospects despite its ongoing restructuring efforts.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.