Stock market today: Nasdaq closes above 23,000 for first time as tech rebounds

Kimberly-Clark Corp (NYSE:NASDAQ:KMB) shares jumped 3.51% in premarket trading after the consumer products giant reported its strongest volume growth in five years, according to the company’s Q2 2025 earnings presentation released on August 1, 2025.

Quarterly Performance Highlights

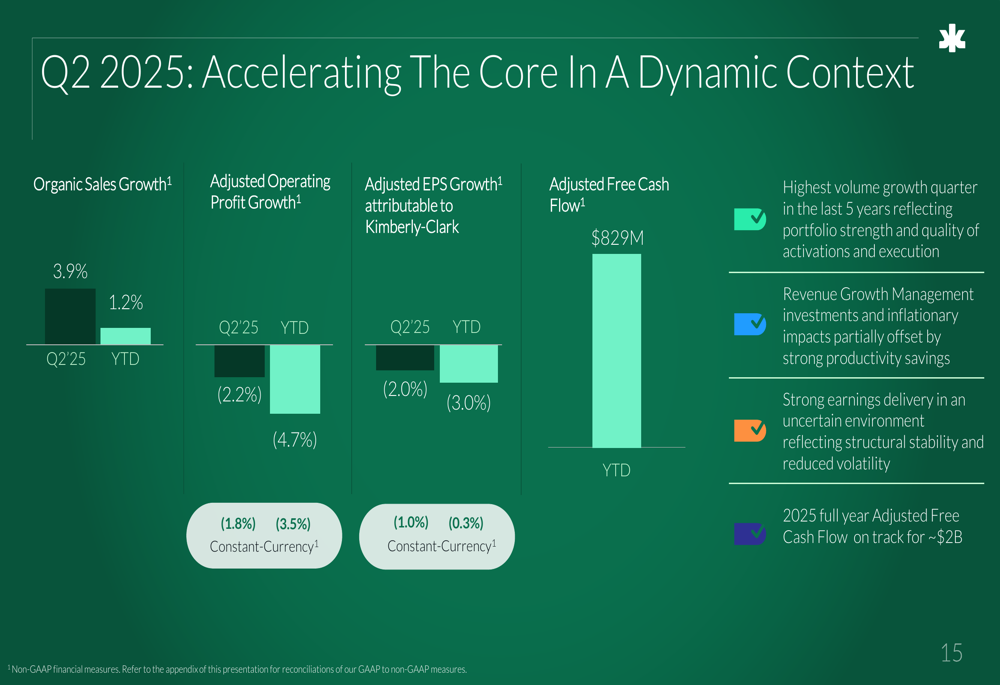

Kimberly-Clark delivered 3.9% organic sales growth in Q2, primarily driven by robust volume increases across key markets. The company achieved 5% volume growth in North America and 6% volume growth in International Personal Care, marking its strongest volume performance in five years.

"We’re building momentum in a dynamic environment," the company noted in its presentation, highlighting that it gained global weighted market share of 10 basis points during the quarter.

Despite the strong volume performance, adjusted operating profit decreased by 2.2% year-over-year, while adjusted earnings per share attributable to Kimberly-Clark declined by 2.0%. The company attributed this primarily to Revenue Growth Management investments.

As shown in the following financial performance summary:

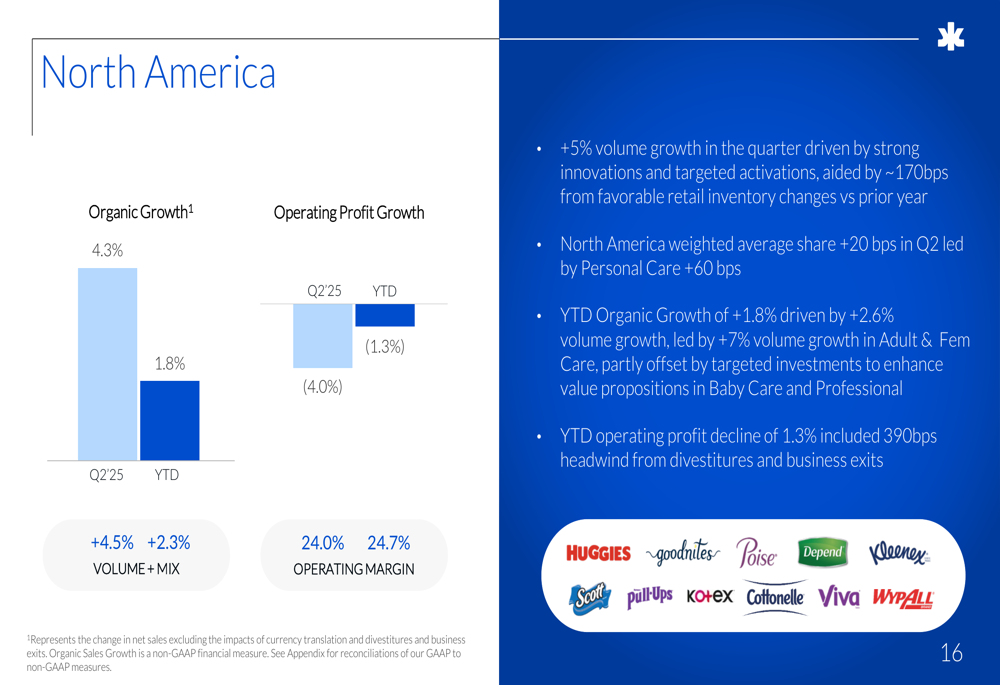

North America, which includes brands like Huggies, Kleenex, and Kotex, posted 4.3% organic growth with volume and mix contributing 4.5%. The segment maintained a strong operating profit margin of 24.0% in Q2, though year-to-date operating profit declined by 1.3%, which included a 390 basis point headwind from divestitures and business exits.

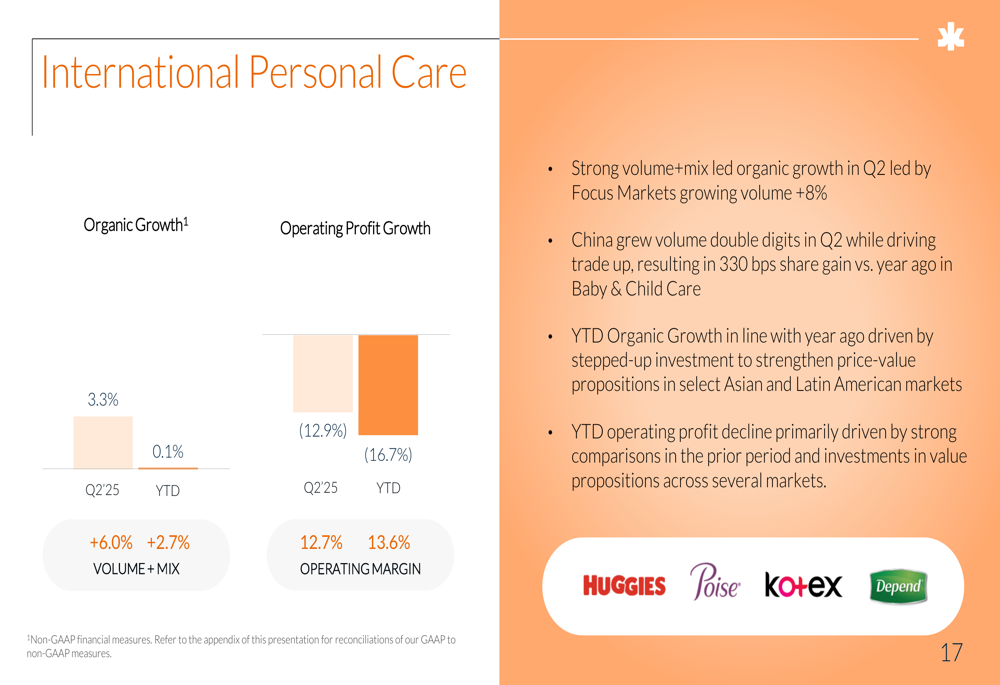

The International Personal Care segment showed similarly strong volume performance with 3.3% organic growth and volume/mix contribution of 6.0%. Operating profit margin for this segment stood at 12.7% for Q2.

Strategic Initiatives

Kimberly-Clark announced two major strategic initiatives that signal a significant transformation for the company. First, it unveiled a $2 billion investment in North America, described as the "largest domestic expansion in 30+ years," aimed at accelerating its innovation pipeline and supporting growth targets.

The company also announced a joint venture with Suzano to create what it calls "a preeminent international tissue and professional products company." The JV values Kimberly-Clark’s International Fiber & Professional business at approximately $3.4 billion, with Suzano taking a 51% stake and Kimberly-Clark retaining 49%. The transaction is expected to close in mid-2026.

The following slide details the structure and strategic benefits of this joint venture:

"This joint venture represents a major step forward in our transformation," the company stated, noting that the partnership with Suzano will help reduce Kimberly-Clark’s exposure to volatile input costs while allowing it to focus on "proprietary, right-to-win spaces to improve growth trajectory."

The company also highlighted its progress in transformation initiatives, including marketing excellence recognized with 11 Cannes Lions awards:

Detailed Financial Analysis

Kimberly-Clark’s Q2 results show a company in transition, investing in growth while managing profitability. The company reported adjusted free cash flow of $829 million year-to-date and maintained that it is on track to achieve approximately $2 billion for the full year 2025.

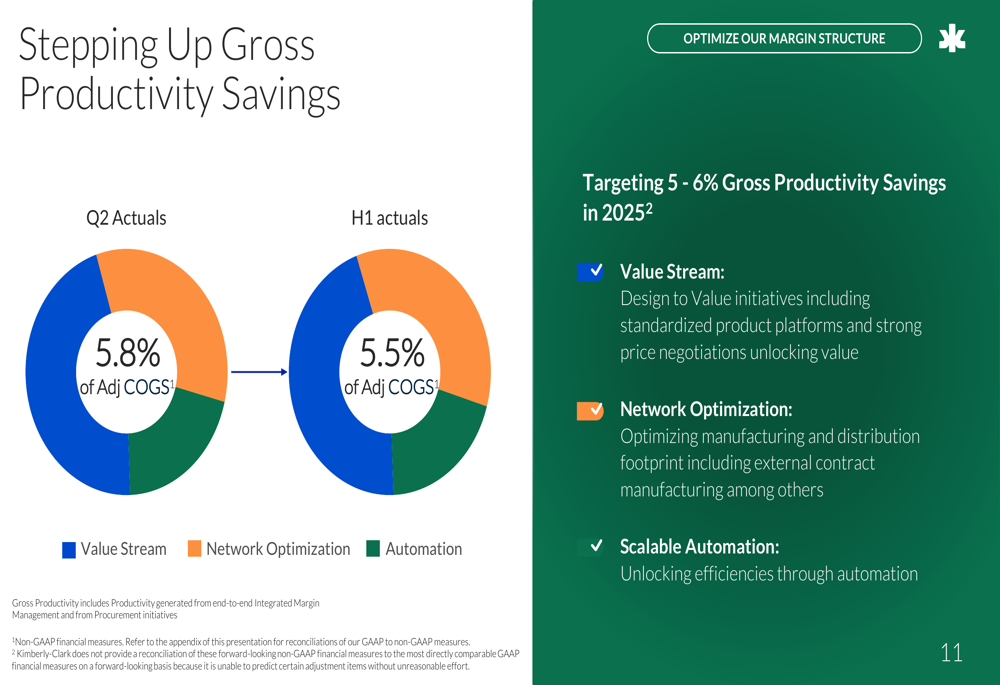

Gross productivity remains a bright spot, with Q2 delivery at 5.8% of adjusted cost of goods sold, exceeding the company’s target range of 5-6% for 2025. This productivity is being driven by value stream optimization, network optimization, and automation initiatives.

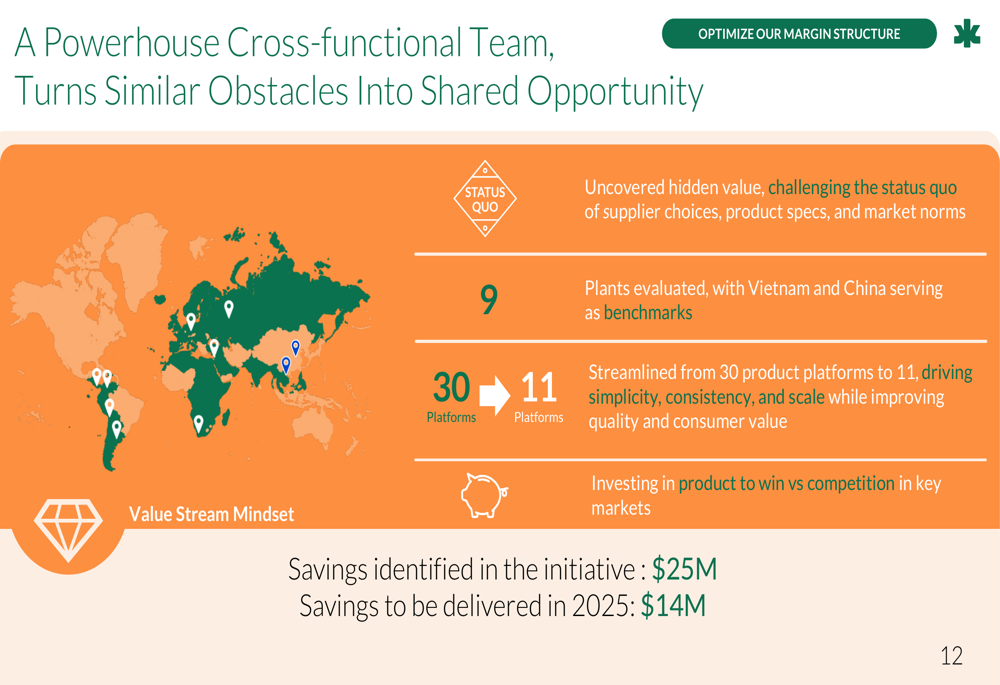

The company provided an example of its cross-functional approach to productivity, highlighting how it streamlined from 30 product platforms to 11, identifying $25 million in savings with $14 million to be delivered in 2025.

Forward-Looking Statements

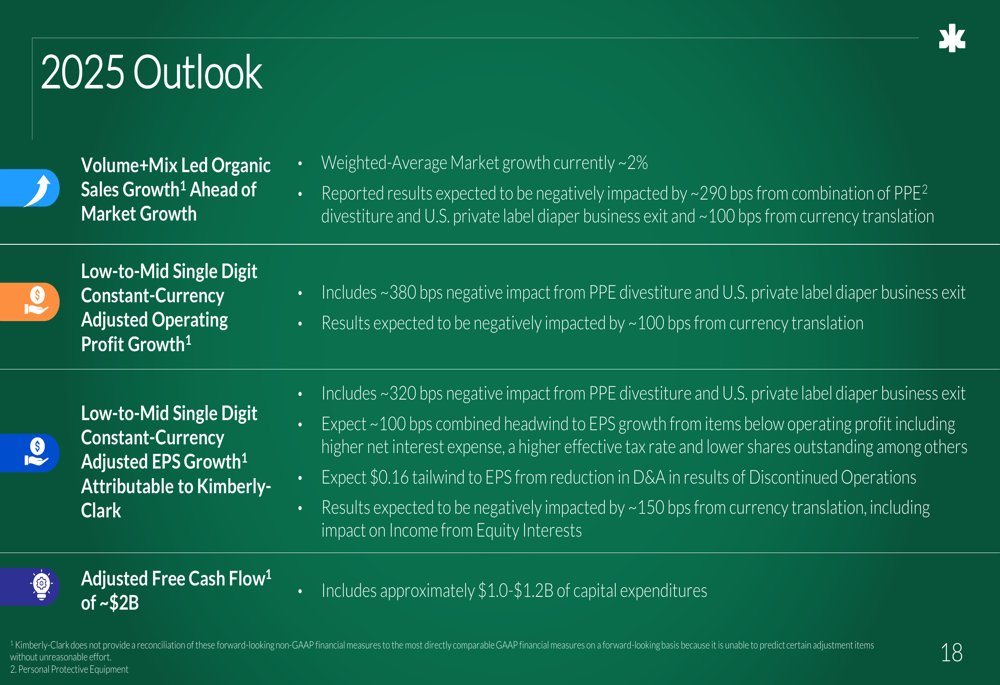

Looking ahead, Kimberly-Clark maintained its 2025 outlook, projecting volume and mix-led organic sales growth ahead of market growth (currently estimated at approximately 2%). The company expects low-to-mid single-digit constant-currency adjusted operating profit growth and similar growth in adjusted earnings per share.

This outlook represents a significant improvement from the Q1 2025 guidance, which according to previous earnings coverage had been revised to flat EPS growth from an earlier projection of 6.5% growth. The more optimistic Q2 outlook suggests the company’s strategic initiatives and volume growth are beginning to yield positive results.

The company’s strategic roadmap emphasizes a phased approach to value creation, with 2024 focused on establishing a foundation, 2025 on scaling initiatives while transforming, and 2026 and beyond aimed at accelerating growth and leveraging scale for industry-leading returns.

The positive premarket trading reaction of +3.51% indicates that investors are responding favorably to Kimberly-Clark’s volume growth and strategic transformation efforts, despite the slight decline in adjusted operating profit and EPS. With shares closing at $124.62 on July 31, 2025, the stock remains below its 52-week high of $150.45, suggesting potential upside if the company continues to execute on its transformation strategy.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.