Gold prices set for weekly drop as dollar surges; Trump tariff action in focus

Introduction & Market Context

Kinaxis Inc (TSX:KXS) presented its Q1 2025 financial results on May 8, 2025, reporting solid growth in key metrics and reaffirming its full-year guidance. The supply chain orchestration software provider’s stock closed at $188.58 on May 7, near its 52-week high of $190.17, suggesting positive market sentiment ahead of the earnings announcement.

Interim CEO and Chair Bob Courteau, alongside CFO Blaine Fitzgerald, highlighted the company’s strong start to fiscal 2025, with double-digit growth in SaaS revenue and a significant improvement in profitability metrics compared to the same period last year.

Quarterly Performance Highlights

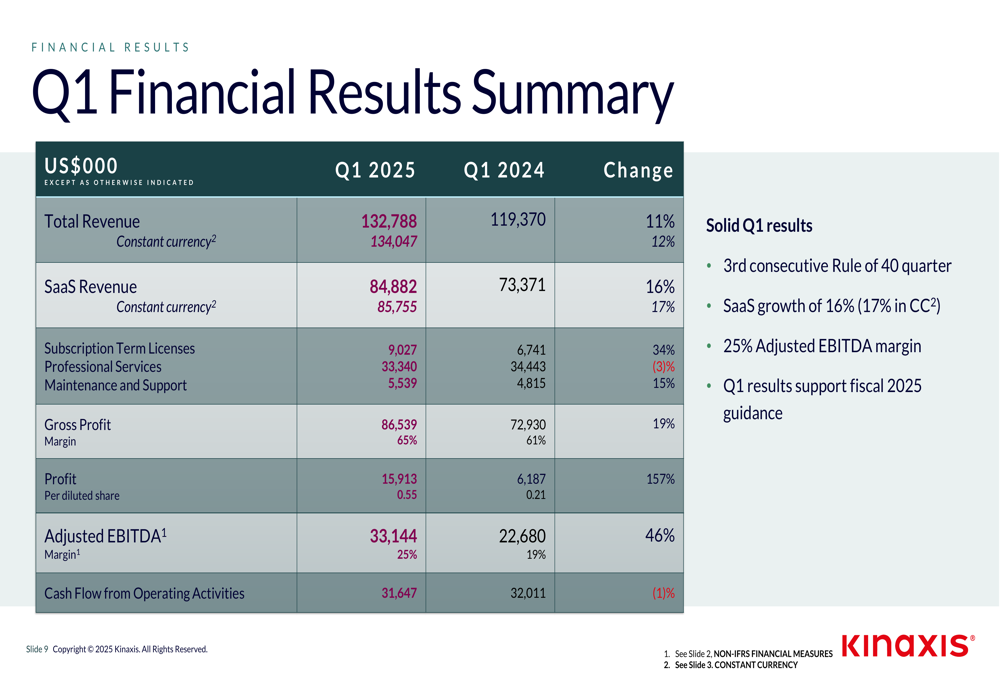

Kinaxis reported Q1 2025 total revenue of $132.8 million, representing an 11% year-over-year increase (12% in constant currency). SaaS revenue, a key growth indicator, reached $84.9 million, up 16% compared to Q1 2024 (17% in constant currency).

As shown in the following financial highlights slide, the company achieved a notable 157% increase in profit to $15.9 million, translating to $0.55 per diluted share:

Adjusted EBITDA grew 46% year-over-year to $33.1 million, with a margin of 25%, marking the company’s third consecutive quarter achieving the "Rule of 40" (where SaaS growth rate plus EBITDA margin exceeds 40%). This represents a significant improvement from the 18% Adjusted EBITDA margin reported in Q4 2024.

The company’s gross profit increased by 19% to $86.5 million, with a gross margin of 65%, while cash flow from operating activities remained stable at $31.6 million, a slight 1% decrease from the previous year.

Detailed Financial Analysis

Kinaxis demonstrated continued momentum in Annual Recurring Revenue (ARR), a critical metric for subscription-based software companies. ARR grew by 14% year-over-year on a constant currency basis to $372 million, with a balanced mix of new and expansion business:

The company highlighted a record quarter for expansion business, with 53% of gross ARR additions coming from existing customers, while new customer acquisitions accounted for 47%. This balanced growth approach indicates both strong customer retention and continued market penetration.

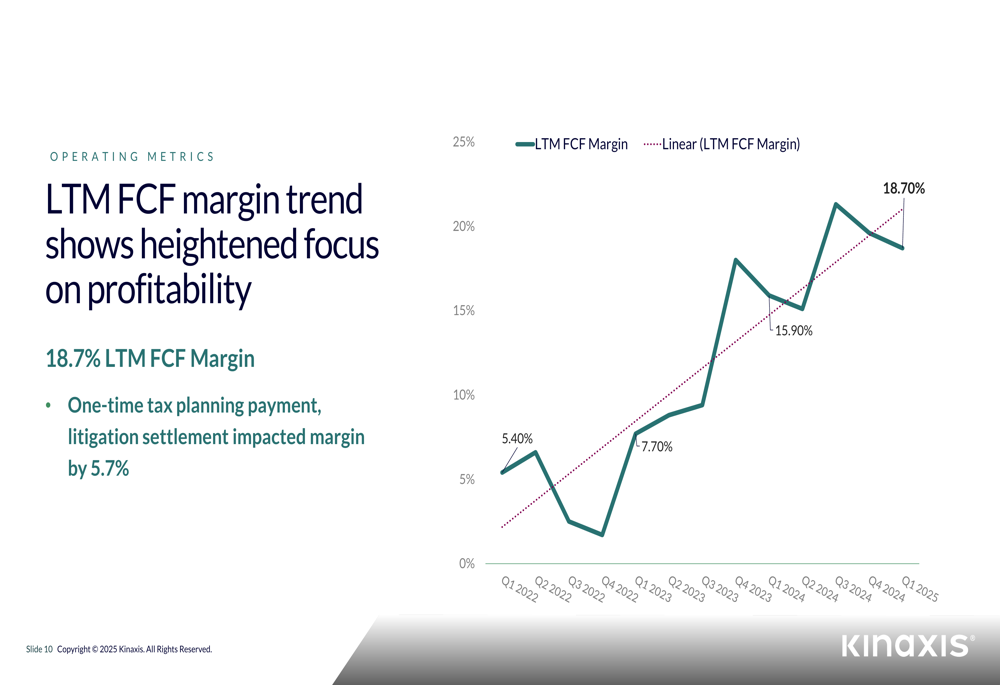

Free cash flow performance has shown consistent improvement, with Last Twelve Months (LTM) Free Cash Flow margin reaching 18.7%, despite being impacted by a one-time tax planning payment and litigation settlement:

The company’s Remaining Performance Obligation (RPO), which represents contracted but not yet recognized revenue, grew to $812 million, providing strong visibility into future revenue streams. Kinaxis has achieved a 3-year compound annual growth rate (CAGR) of 19% for total revenue and 20% for SaaS revenue.

Competitive Industry Position

Kinaxis maintained its leadership position in the 2025 Gartner (NYSE:IT) Magic Quadrant for Supply Chain Planning Solutions for the 11th consecutive year, reinforcing its strong competitive standing in the market:

This recognition highlights the company’s continued innovation and execution in the supply chain planning space, positioning it favorably against competitors in both completeness of vision and ability to execute.

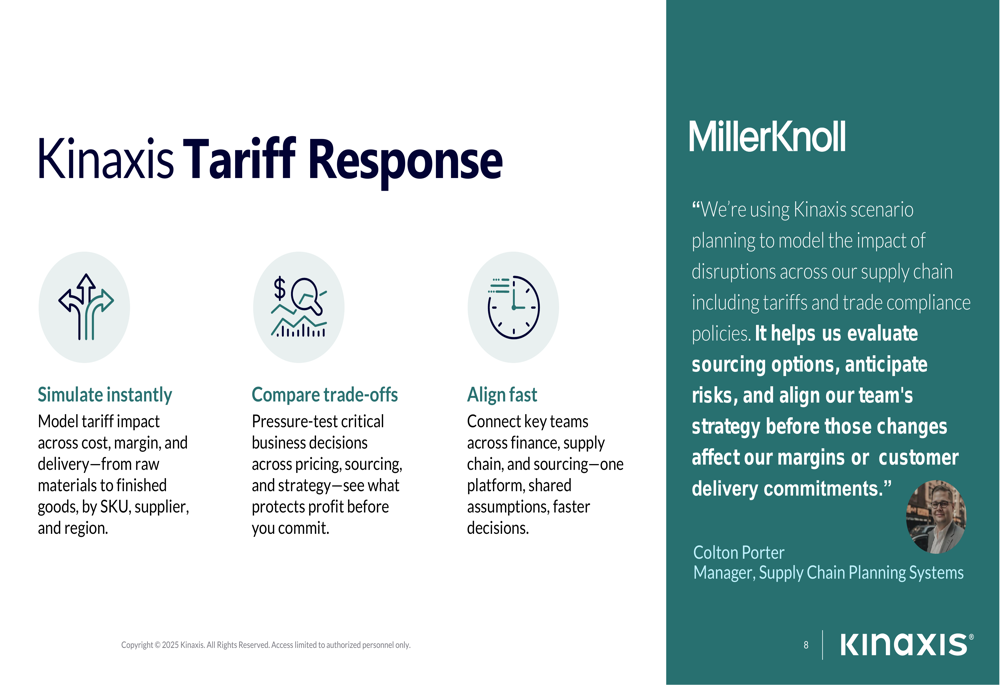

The company showcased a customer success story featuring MillerKnoll (NASDAQ:MLKN), which leverages Kinaxis solutions to simulate tariff impacts, compare trade-offs, and align key teams with shared assumptions:

Strategic Initiatives

Kinaxis emphasized its innovation focus during the presentation, highlighting three key areas showcased at its Kinexions event, which attracted 1,000 attendees:

1. Strategic partnership with Databricks to enhance data integration capabilities

2. Development of Agentic AI to create new digital co-workers

3. Advancement of Predictive AI for machine learning forecasting solutions

The company also continued its share buyback program, repurchasing 157,428 common shares in Q1 at an average price of $110.49. The current plan, which expires on November 5, 2025, allows for the purchase of up to 1.4 million shares (5% of outstanding shares).

Forward-Looking Statements

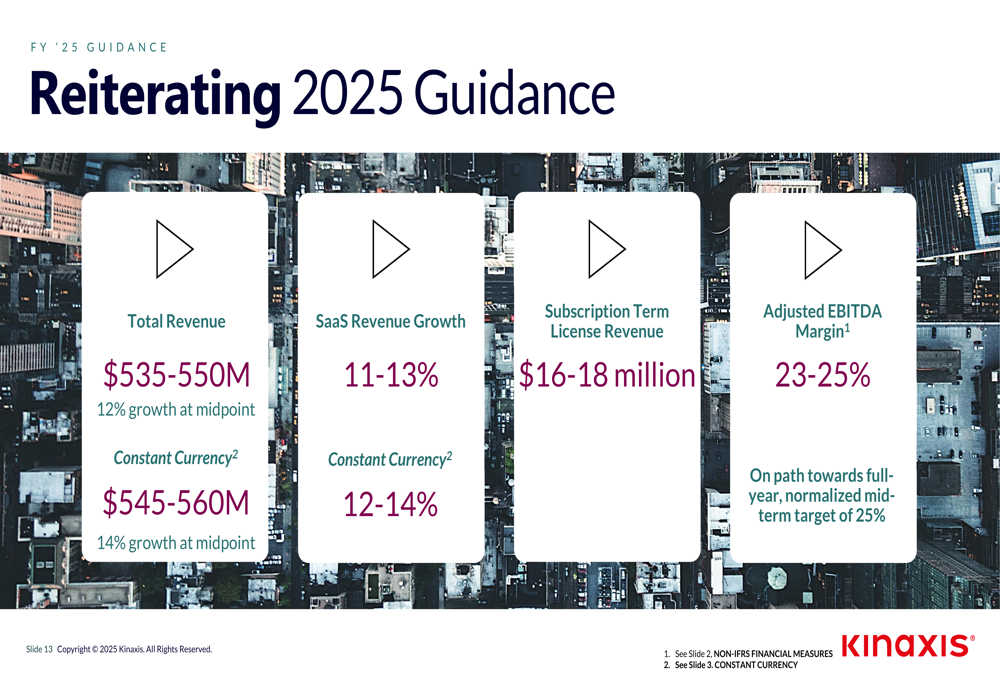

Kinaxis reiterated its full-year 2025 guidance, maintaining the same targets presented in its Q4 2024 earnings call:

The company expects total revenue between $535-550 million, representing 12% growth at the midpoint (or $545-560 million in constant currency). SaaS revenue growth is projected at 11-13% (12-14% in constant currency), with subscription term license revenue of $16-18 million.

Adjusted EBITDA margin is expected to be 23-25%, with management noting they are on track toward a full-year, normalized mid-term target of 25%. This guidance suggests confidence in the company’s ability to maintain its growth trajectory while continuing to improve profitability metrics.

The presentation highlighted ongoing business momentum with new customer wins across multiple industries, including Sun Pharma and Demant A/S in life sciences, a major semiconductor company in high tech, Veolia in industrial, and Delta Faucet Company and Workwear Outfitters in consumer products.

With a strong Q1 performance and reaffirmed guidance, Kinaxis appears well-positioned to continue its growth trajectory in the supply chain orchestration market throughout 2025, balancing revenue growth with improving profitability metrics.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.