Street Calls of the Week

Introduction & Market Context

Kirby Corporation (NYSE:KEX) presented its first quarter 2025 earnings results on May 1, showing improved profitability despite slightly lower revenue. The marine transportation and distribution services provider reported earnings per share of $1.33, up from $1.19 in the same period last year, representing a 12% year-over-year increase. This performance comes after Kirby missed analyst expectations in Q4 2024, when it reported adjusted EPS of $1.29 against a forecast of $1.37.

The company’s stock closed at $96.37 on April 30, 2025, and was trading down 1.42% in pre-market activity following the earnings release. Kirby’s shares have been trading well below their 52-week high of $132.21, suggesting investors remain cautious despite the improved earnings performance.

Quarterly Performance Highlights

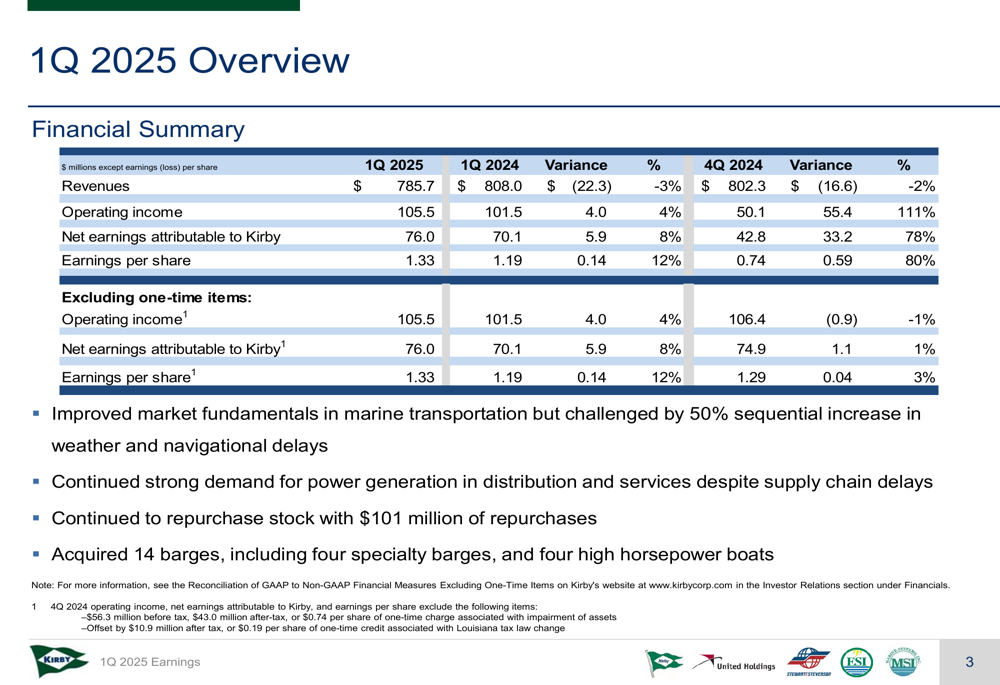

Kirby reported Q1 2025 revenue of $785.7 million, down 2.8% from $808.0 million in Q1 2024 and 2.1% from $802.3 million in Q4 2024. Despite the revenue decline, the company achieved operating income of $105.5 million, up 3.9% year-over-year and a significant 110.6% increase from the previous quarter.

As shown in the following financial summary table:

Net earnings attributable to Kirby reached $76.0 million, an 8.4% improvement from Q1 2024 and a 77.6% jump from Q4 2024. The earnings per share of $1.33 represented a 11.8% year-over-year increase and a 79.7% sequential improvement, reflecting enhanced operational efficiency and favorable pricing in the marine transportation segment.

The company continued its share repurchase program, buying back 1,002,761 shares at an average price of $101.19 during the quarter, indicating management’s confidence in Kirby’s intrinsic value despite recent stock price performance.

Detailed Financial Analysis

Marine Transportation Segment

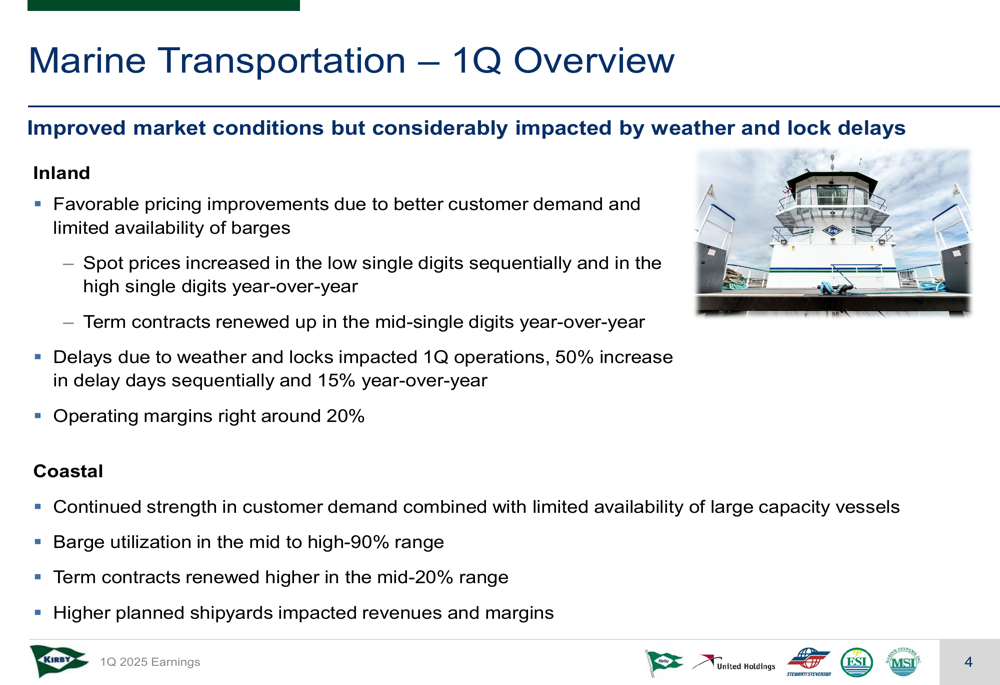

Kirby’s Marine Transportation segment, which includes both inland and coastal operations, demonstrated strong performance in Q1 2025. The segment benefited from favorable pricing improvements, with inland spot rates increasing by 5-7% year-over-year and term contract renewals up 8-10%. Coastal term contract renewals showed even stronger growth at 15-20% year-over-year.

The following slide illustrates the operational highlights for the Marine Transportation segment:

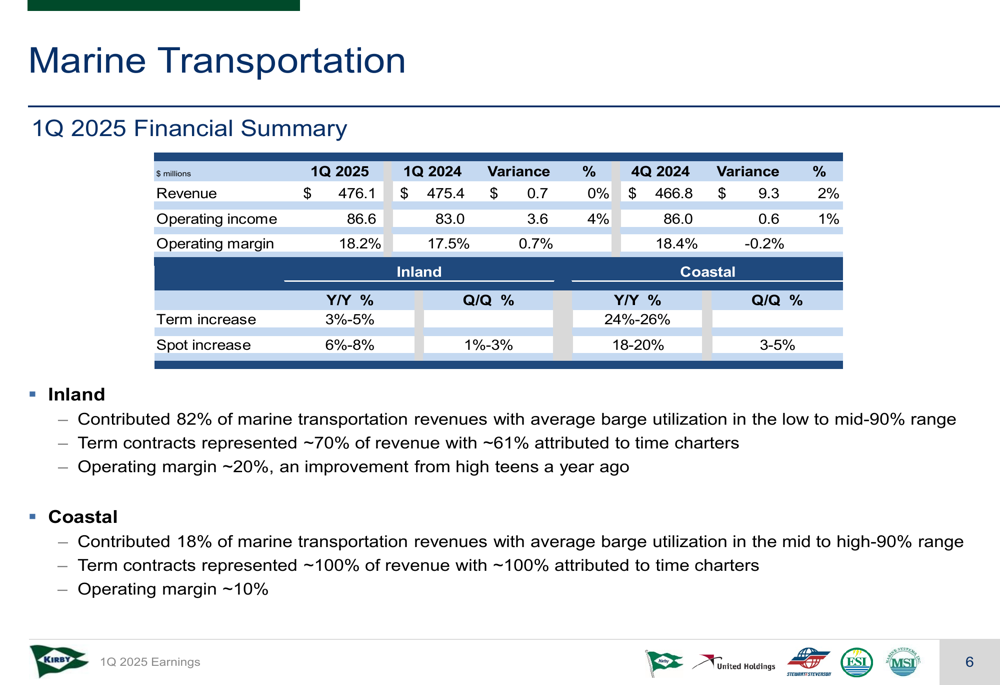

Financial results for the Marine Transportation segment show solid performance despite weather-related delays that impacted operations by 15% year-over-year:

The inland marine business achieved an operating margin of 18.2%, demonstrating the positive impact of improved pricing and operational efficiency. Coastal operations continued to benefit from high barge utilization and stronger contract renewals, though planned shipyard maintenance affected some operations during the quarter.

Distribution & Services Segment

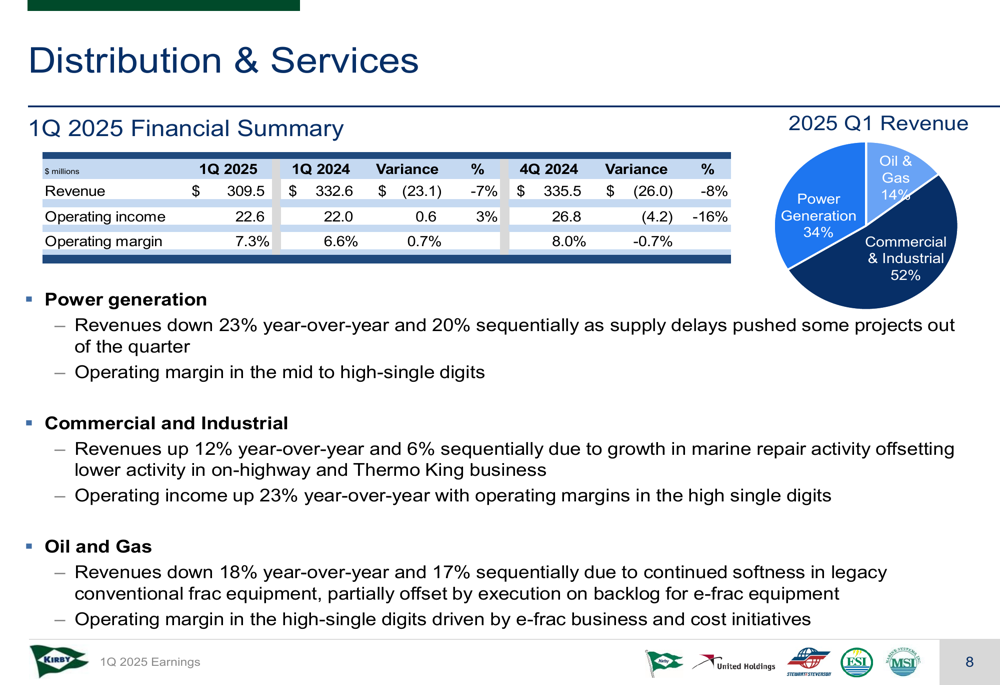

The Distribution & Services segment presented a more mixed picture, with revenue of $309.5 million and an operating margin of 7.3% in Q1 2025:

As illustrated in the revenue breakdown, Commercial/Industrial represented 52% of the segment’s revenue, followed by Power Generation (HM:PGV) at 34% and Oil & Gas at 14%. The Power Generation business saw strong order intake but experienced lower revenues due to supply chain delays. The Commercial and Industrial division reported increased revenue and operating income, while the Oil and Gas division faced softness in conventional business but managed to increase operating income.

Strategic Initiatives

Kirby continues to manage its fleet strategically, with a focus on maintaining appropriate capacity while retiring older assets. For the inland segment, the company started Q1 2025 with 1,094 barges (24.2 million barrels capacity) and ended with 1,111 barges (24.6 million barrels). The coastal fleet remained stable at 28 barges with 2.9 million barrels capacity.

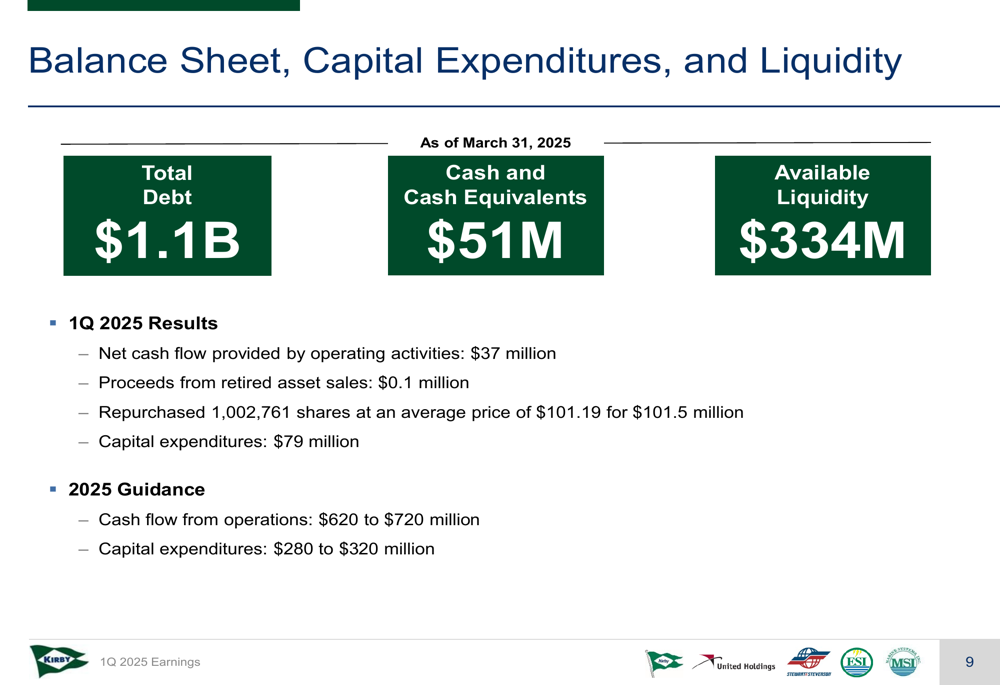

The company’s balance sheet remains solid, with total debt of $1.1 billion, cash and cash equivalents of $51 million, and available liquidity of $334 million as of March 31, 2025. Kirby generated strong cash flow from operations during the quarter, allowing for continued investment in the business while returning capital to shareholders through stock repurchases.

The following slide details Kirby’s financial position and capital allocation:

Forward-Looking Statements

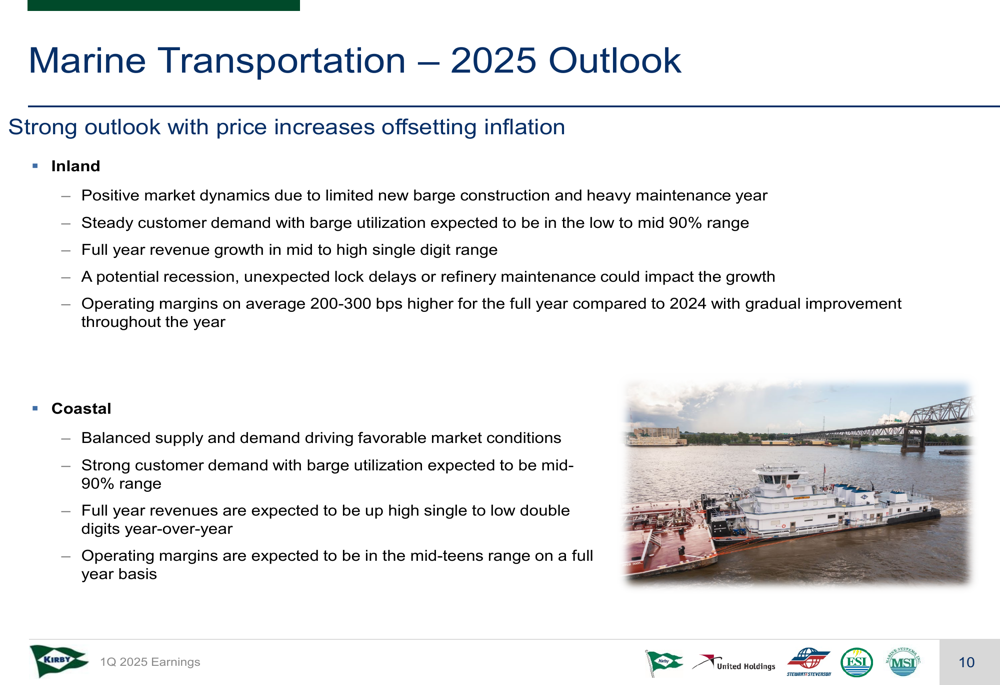

Kirby’s outlook for 2025 remains positive, particularly for the Marine Transportation segment. The company anticipates continued favorable market dynamics for inland operations, with revenue growth projected in the mid to high single digits and operating margins expected to improve by 200-300 basis points.

As shown in the Marine Transportation outlook slide:

For the coastal business, Kirby expects balanced supply and demand conditions to persist, with high single to low double-digit revenue growth and operating margins in the mid-teens.

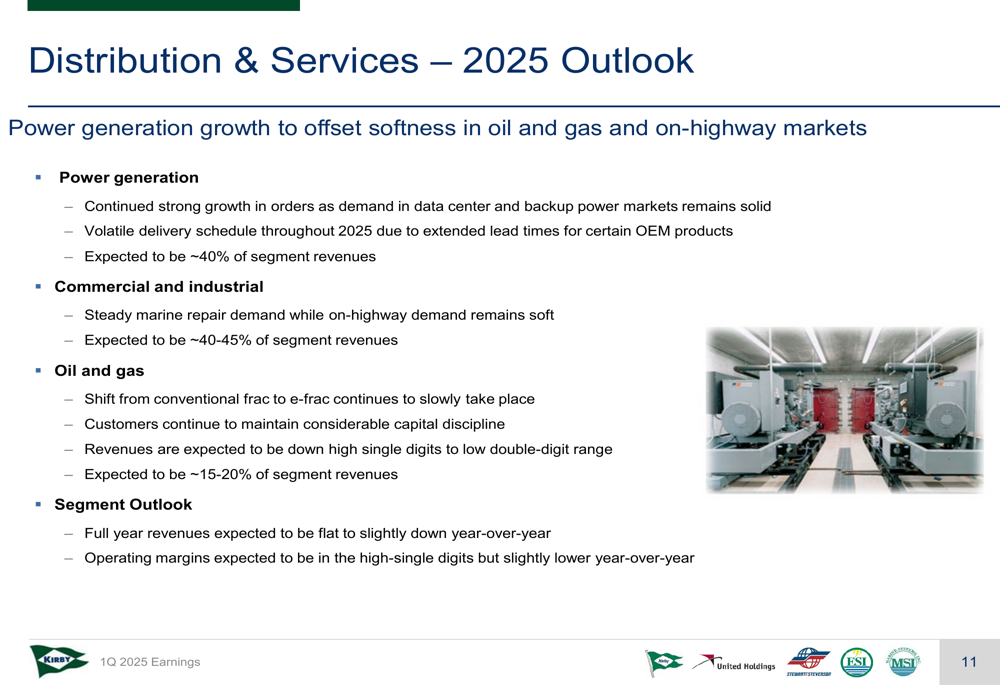

The Distribution & Services segment faces more challenges, as illustrated in the following outlook:

Power generation is expected to continue showing strong growth in orders, offsetting softness in oil and gas and on-highway markets. However, the company projects full-year segment revenues to be flat to slightly down compared to 2024.

Overall, Kirby’s 2025 guidance includes cash flow from operations between $620 to $720 million and capital expenditures between $280 to $320 million, reflecting management’s confidence in continued operational improvements despite revenue headwinds in certain segments.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.