Infosys, Wipro decline despite upbeat Q2 earnings; margin concerns weigh

Introduction & Market Context

Kite Realty Group Trust (NYSE:KRG), a retail REIT with 180 operating properties spanning 28 million square feet, reported solid first-quarter 2025 results that demonstrated continued operational strength and strategic growth initiatives. The company’s investor presentation, released on April 30, 2025, highlighted improving fundamentals, a major mixed-use acquisition, and a new joint venture that positions KRG for sustained growth.

With a market capitalization of $4.8 billion and enterprise value of $7.9 billion as of April 28, 2025, Kite Realty continues to strengthen its position in the open-air retail sector, particularly in high-growth Sun Belt markets. The stock closed at $21.55 on April 29, 2025, down 1.42% for the day, reflecting broader market volatility despite the company’s positive operational trends.

As shown in the following comprehensive overview of the company’s current position:

Quarterly Performance Highlights

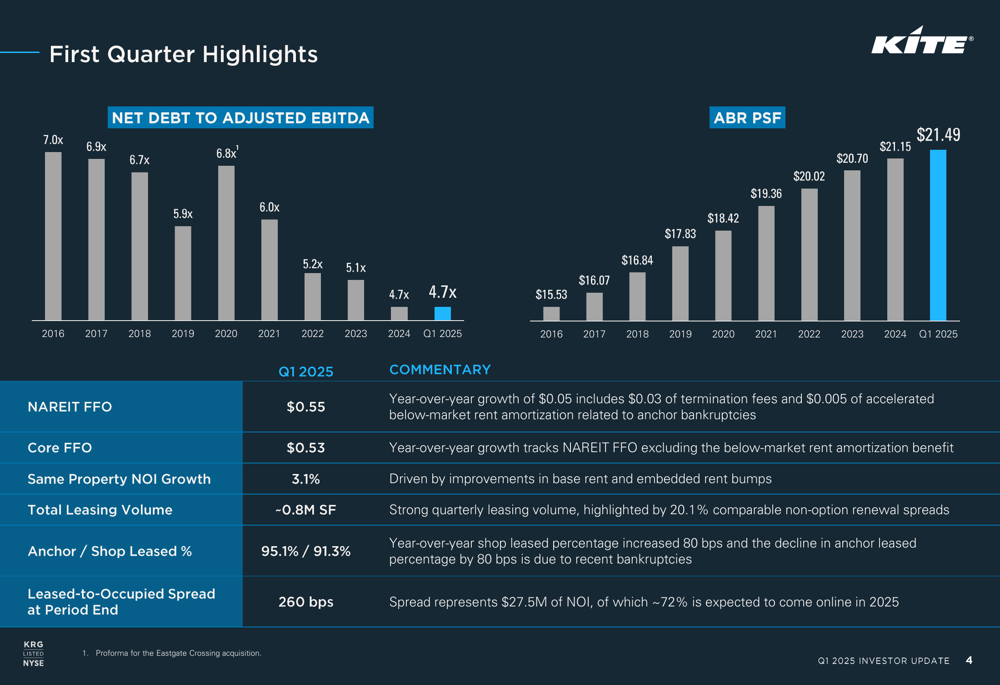

Kite Realty reported NAREIT FFO of $0.55 per share for Q1 2025, representing year-over-year growth of $0.05, which included $0.03 of termination fees and $0.005 of accelerated below-market rent amortization. Core FFO came in at $0.53 per share, showing continued improvement in the company’s underlying business.

Same-property NOI growth reached 3.1% for the quarter, driven by improvements in base rent and embedded rent bumps. The company’s leasing momentum remained strong with approximately 0.8 million square feet of total leasing volume and impressive 20.1% comparable non-option renewal spreads.

The following chart illustrates KRG’s first quarter performance metrics, including the continued improvement in both leverage and average base rent per square foot:

KRG’s portfolio was 93.8% leased at quarter-end, with anchor spaces at 95.1% and shop spaces at 91.3%. The leased-to-occupied spread stood at 260 basis points, representing $27.5 million of NOI, with approximately 72% expected to come online during 2025 – providing significant embedded growth for the remainder of the year.

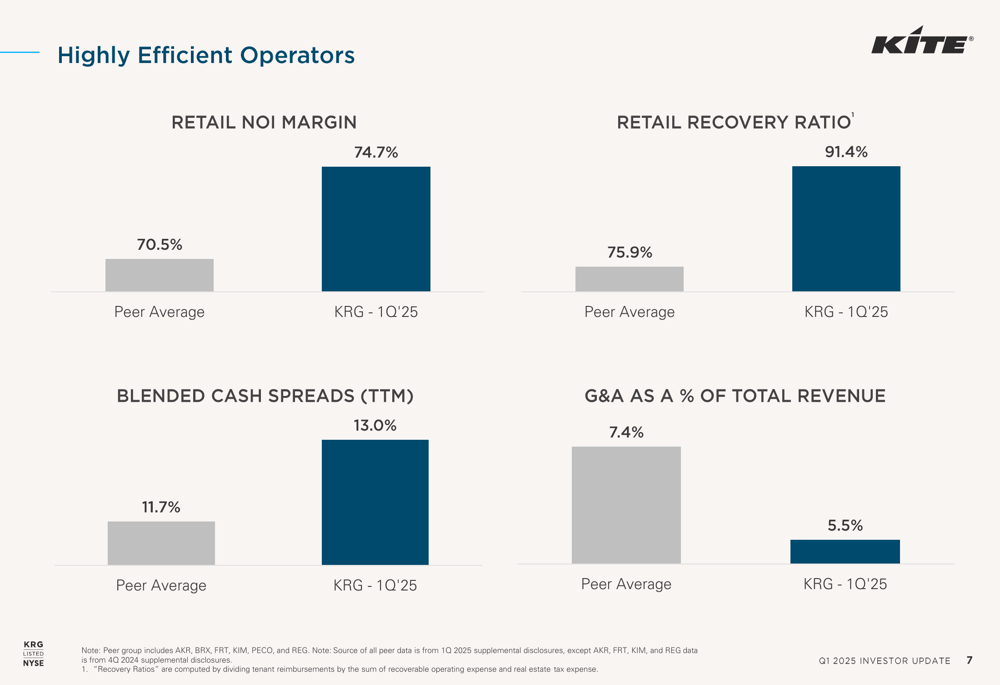

The company’s operational efficiency continues to outpace its peer group across key metrics. KRG achieved a retail NOI margin of 74.7% compared to the peer average of 70.5%, and a retail recovery ratio of 91.4% versus the peer average of 75.9%. These metrics demonstrate the company’s superior property management capabilities and strategic tenant selection.

As shown in the following comparison with industry peers:

Strategic Initiatives

The most significant strategic development in Q1 was Kite Realty’s acquisition of Legacy West, a premier mixed-use asset in Plano, Texas, in partnership with Singapore’s sovereign wealth fund GIC. This "generational" mixed-use property spans 35 acres and includes 344,000 square feet of retail (48% of total NOI), 444,000 square feet of office (27% of NOI), and 782 multifamily units (25% of NOI).

Legacy West features luxury retail tenants including Gucci, Louis Vuitton, Tiffany & Co (NYSE:TIF)., and Chanel, with average retail sales exceeding $1,000 per square foot. The acquisition is immediately accretive to FFO per share and enhances the portfolio’s embedded rent bumps to 260 basis points compared to the portfolio average of 168 basis points.

The joint venture structure with GIC allows KRG to leverage its operating expertise while diversifying risk. KRG maintains a 52% interest in the venture and serves as the operating member, with plans to potentially expand the relationship through additional investments.

"The Legacy West acquisition checks all the boxes for us," noted the company in its presentation. "It’s immediately accretive to FFO, enhances our portfolio’s cruising speed with superior embedded rent bumps, and establishes relationships with luxury tenants that can benefit our broader portfolio."

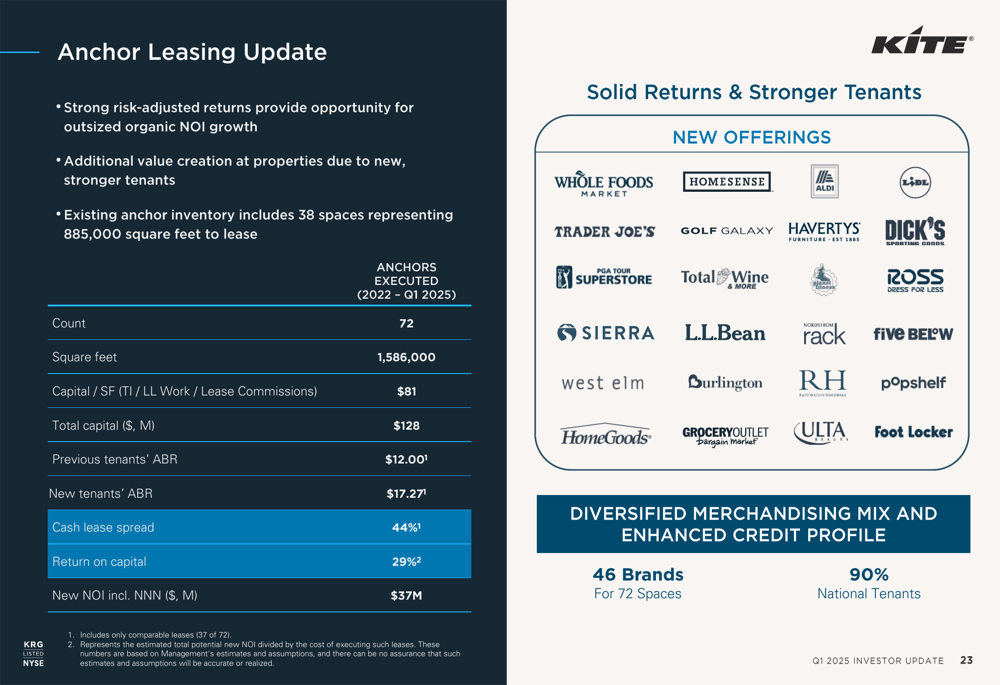

KRG’s anchor leasing strategy continues to show strong results, with 72 leases executed from 2022 through Q1 2025, representing 1.6 million square feet at a capital investment of $81 per square foot. These leases generated a 44% cash lease spread and a 29% return on capital, demonstrating the company’s ability to attract high-quality tenants at favorable terms.

The following slide details the company’s anchor leasing results:

Balance Sheet Strength

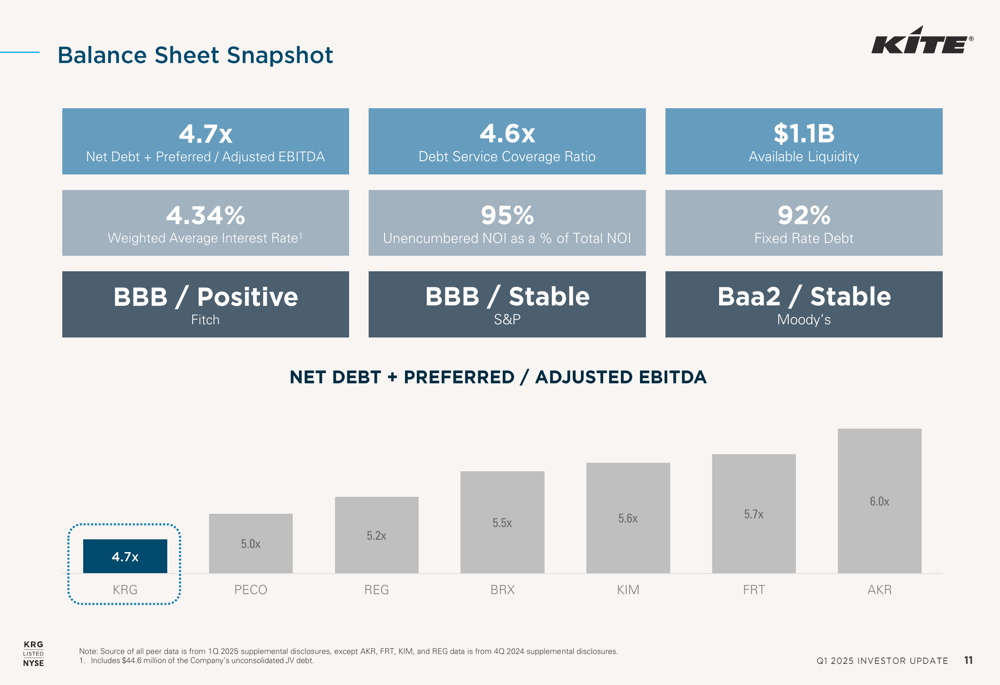

Kite Realty has significantly improved its balance sheet over the past several years, reducing its net debt to adjusted EBITDA ratio from 6.9x in 2016 to 4.7x in Q1 2025. This leverage level compares favorably to the peer average of 5.5x, providing KRG with additional financial flexibility for future growth opportunities.

The company maintains investment grade credit ratings (BBB/Baa2/BBB from S&P, Moody’s, and Fitch, respectively) and has approximately $1.1 billion in available liquidity. Its debt maturity profile is well-staggered, with minimal near-term maturities and 92% fixed-rate debt at a weighted average interest rate of 4.34%.

As illustrated in the following balance sheet snapshot:

Forward-Looking Statements

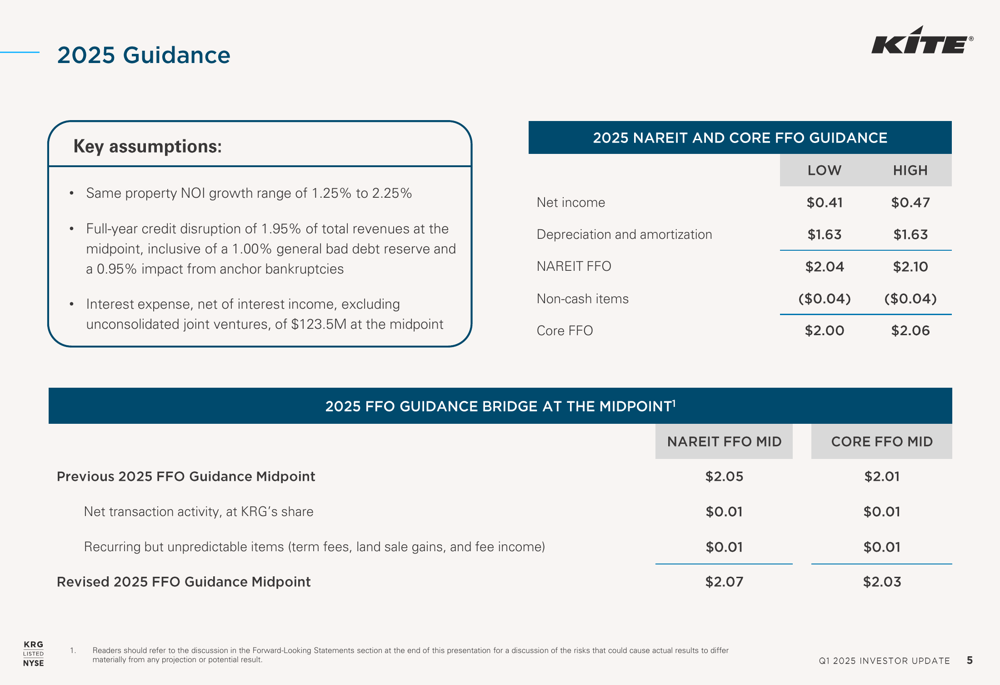

For full-year 2025, Kite Realty provided NAREIT FFO guidance of $2.04 to $2.10 per share and Core FFO guidance of $2.00 to $2.06 per share. This represents a modest increase from previous guidance, reflecting the positive impact of recent strategic initiatives.

The company projects same-property NOI growth of 1.25% to 2.25% for 2025, a relatively conservative outlook that accounts for potential credit disruptions. Management has budgeted for 1.95% of total revenues in credit disruption at the midpoint, including a 1.00% general bad debt reserve and 0.95% impact from anchor bankruptcies.

As shown in the detailed 2025 guidance:

KRG’s signed-not-open pipeline of $27.5 million provides visibility into future NOI growth, with 38% coming from anchor tenants and 62% from shop tenants. Approximately 89% of this pipeline is from the same-property NOI pool, which will directly benefit comparable growth metrics.

The company continues to focus on improving its embedded growth profile by implementing higher fixed rent bumps in new leases. In Q1 2025, 92% of new leases and non-option renewals included fixed rent bumps of 3% or greater, and 96% included fixed CAM provisions, enhancing the predictability and growth of future cash flows.

Competitive Industry Position

Kite Realty’s portfolio is strategically positioned to benefit from favorable demographic trends, with 69% of ABR coming from Sun Belt markets and 65% from the top 10 population growth states. The company’s top five states by ABR concentration are Texas (27%), Florida (12%), Maryland (6%), North Carolina (6%), and Indiana (5%).

The retail real estate market continues to benefit from limited new supply, which has driven leased rates for open-air retail to record highs. KRG’s portfolio composition is well-balanced, with 13% neighborhood centers, 48% community centers, 19% power centers, and 19% lifestyle/mixed-use properties. Importantly, 80% of the company’s ABR comes from properties with a grocery component, providing stability and consistent foot traffic.

The company’s tenant base is diverse, with the top 15 tenants accounting for only 21.1% of ABR. This diversification reduces concentration risk and provides resilience against individual tenant challenges. The tenant mix is balanced between essential retail (31%), restaurants (19%), and other retail/services (50%), creating a complementary ecosystem within its properties.

In conclusion, Kite Realty’s Q1 2025 presentation demonstrates a company executing effectively on its strategic initiatives while maintaining operational excellence and financial discipline. The Legacy West acquisition and GIC joint venture represent significant growth catalysts, while the company’s conservative guidance and strong balance sheet position it well to navigate potential market challenges in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.