Intel stock spikes after report of possible US government stake

Introduction & Market Context

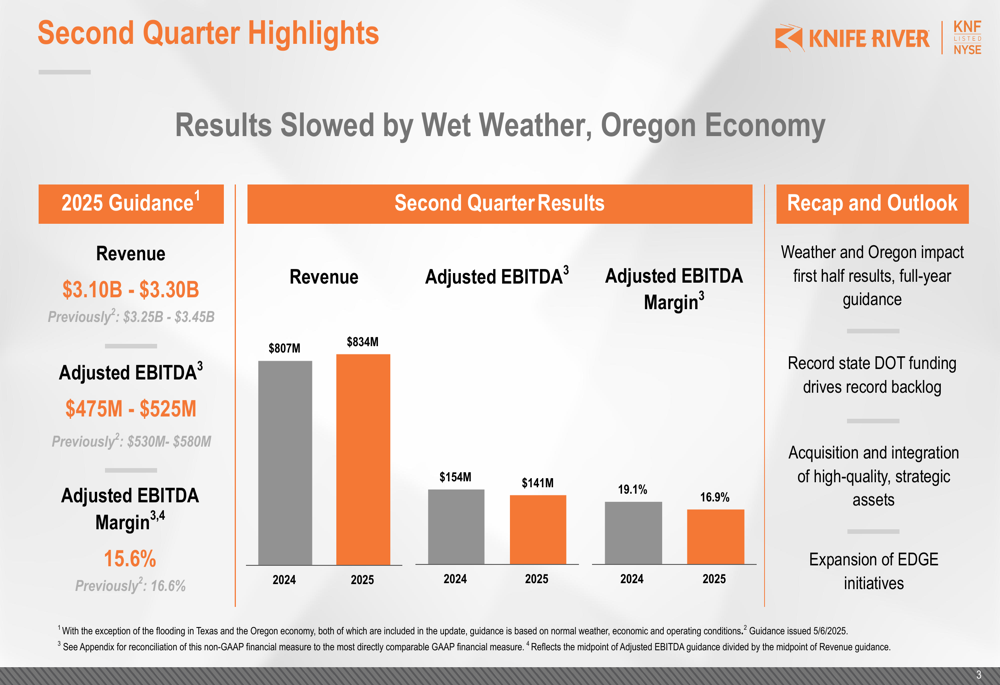

Knife River Corporation (NYSE:KNF) presented its second quarter 2025 results on August 5, revealing how weather challenges and economic headwinds in Oregon impacted performance and forced a downward revision of full-year guidance. The construction materials and contracting services provider saw its stock trade at $84.36, up 1.03% on the day of the presentation, but still well below its 52-week high of $108.83.

The company’s Q2 results reflect a mixed performance with revenue growth offset by margin compression, continuing a challenging trend after Knife River missed both EPS and revenue forecasts in Q1 2025.

Quarterly Performance Highlights

Knife River reported Q2 2025 revenue of $833.8 million, a 3% increase from $807 million in the same period last year. However, adjusted EBITDA declined to $140.8 million from $154 million in Q2 2024, with adjusted EBITDA margin falling to 16.9% from 19.1% a year earlier.

As shown in the following quarterly highlights chart, the company’s performance was significantly impacted by external factors:

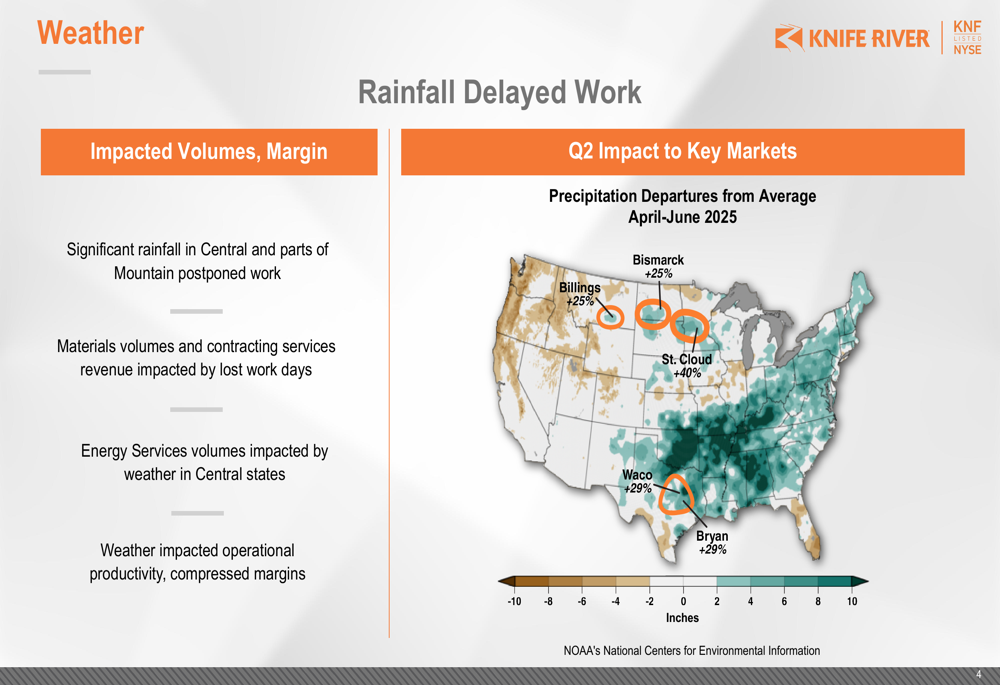

The company attributed the weaker performance primarily to two factors: abnormal rainfall in key operating regions and economic challenges in Oregon. The rainfall impact was particularly significant in the Central and Mountain regions, as illustrated in this precipitation map:

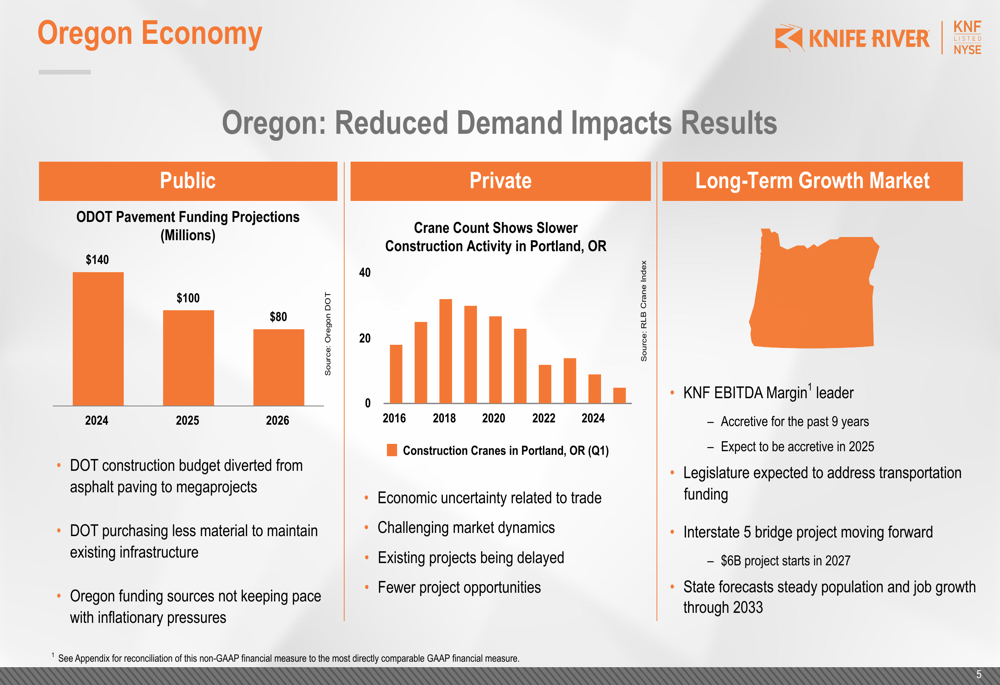

Oregon, which accounts for 23% of Knife River’s revenue, faced specific economic challenges that further pressured results. The state’s Department of Transportation (ODOT) has reduced pavement funding projections from $140 million in 2024 to $80 million in 2026, while construction activity in Portland has declined significantly:

Detailed Financial Analysis

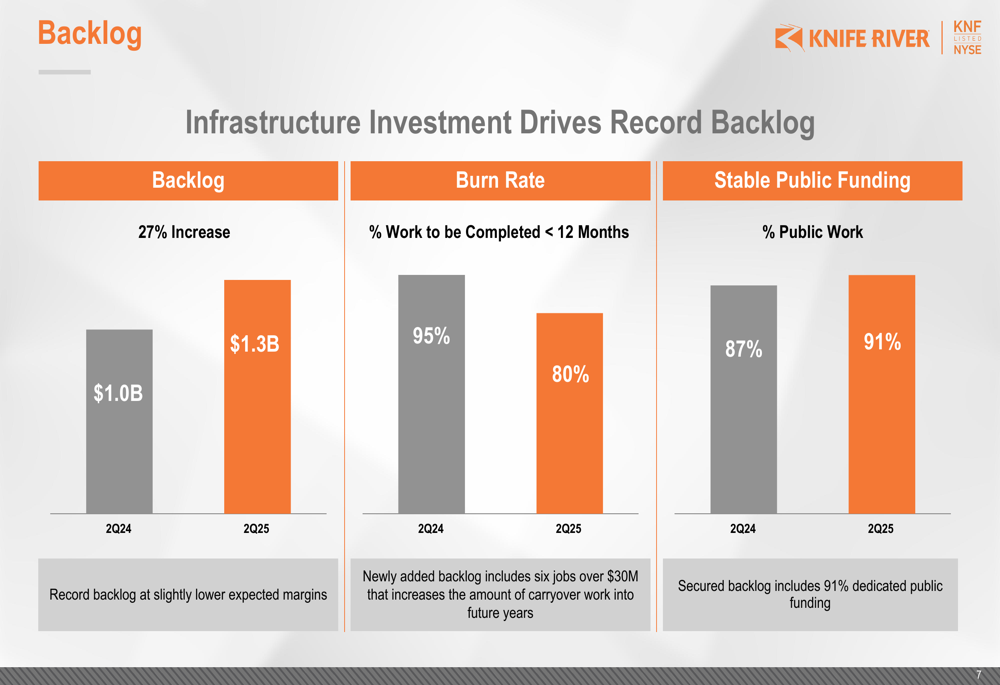

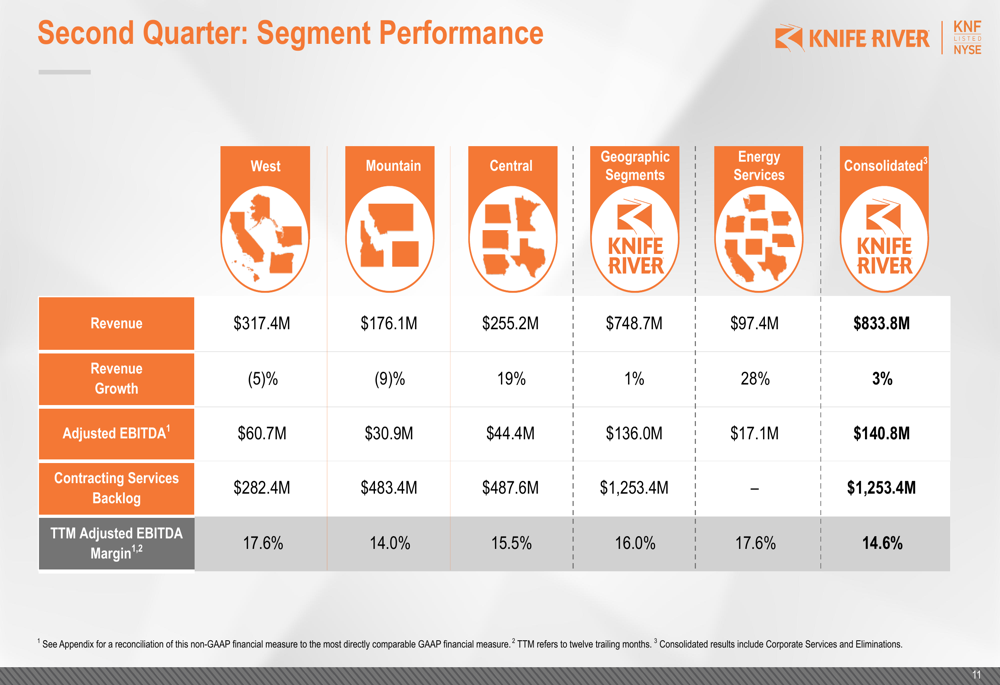

Despite the challenging conditions, Knife River’s contracting services backlog reached a record $1.3 billion, up 27% from $1.0 billion in Q2 2024. Notably, 91% of the backlog consists of public sector projects, up from 87% a year earlier, reflecting the company’s increasing focus on infrastructure work.

The following chart illustrates the significant backlog growth and its composition:

Segment performance varied considerably across regions. The Central segment showed the strongest revenue growth at 19%, while the West and Mountain segments declined by 5% and 9% respectively. Energy Services revenue increased by 28%, though this represents a smaller portion of overall business.

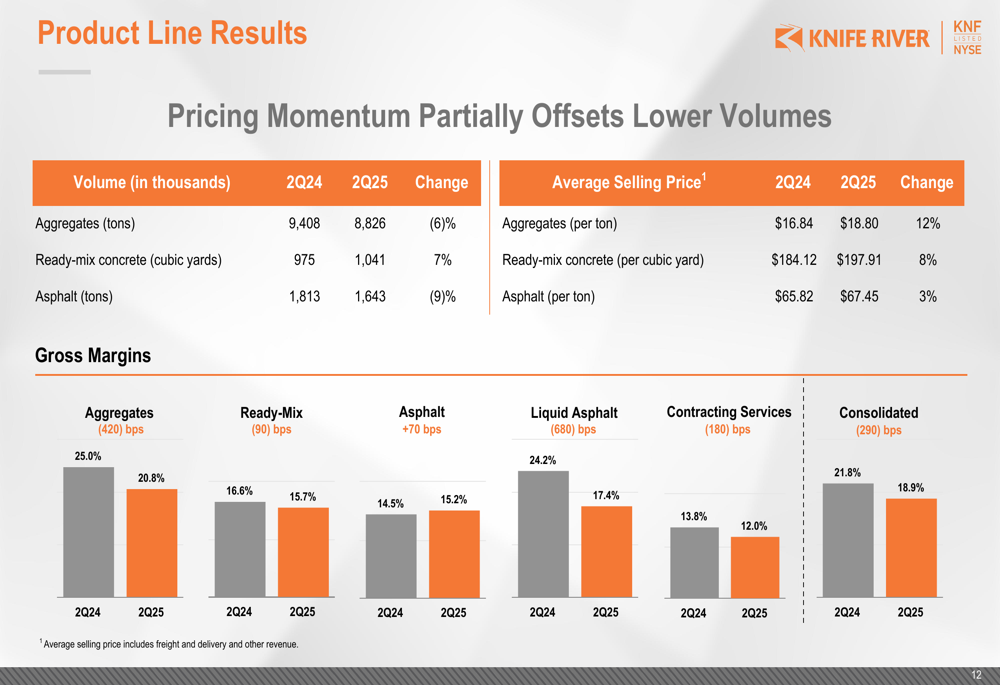

Product line results revealed a pattern of pricing gains partially offsetting volume declines. Aggregates volumes fell 6% year-over-year, but average selling prices increased 12%. Ready-mix concrete volumes grew 7% with an 8% price increase, while asphalt volumes declined 9% with a modest 3% price gain.

The company’s capital position showed increased leverage, with net debt of $1,343.4 million and a net leverage ratio of 3.1x, up significantly from 1.0x at the end of 2024. Available liquidity stood at $321 million, including $294 million in revolver capacity and $27 million in unrestricted cash.

Strategic Initiatives

Knife River continues to execute its EDGE strategy (EBITDA Margin Improvement, Discipline, Growth, Excellence) to navigate current challenges and position for long-term growth. The company has implemented materials pricing and quoting software, added a Senior VP of Aggregates & Rail, and formed 19 PIT Crews focused on operational, commercial, and standardization excellence.

The following slide details the company’s strategic initiatives:

On the acquisition front, Knife River closed two aggregates-led acquisitions since Q1 2025: Kraemer Trucking and Excavating, and High Desert Aggregate & Paving. The company also approved $68 million in capital expenditures for organic growth initiatives in 2025.

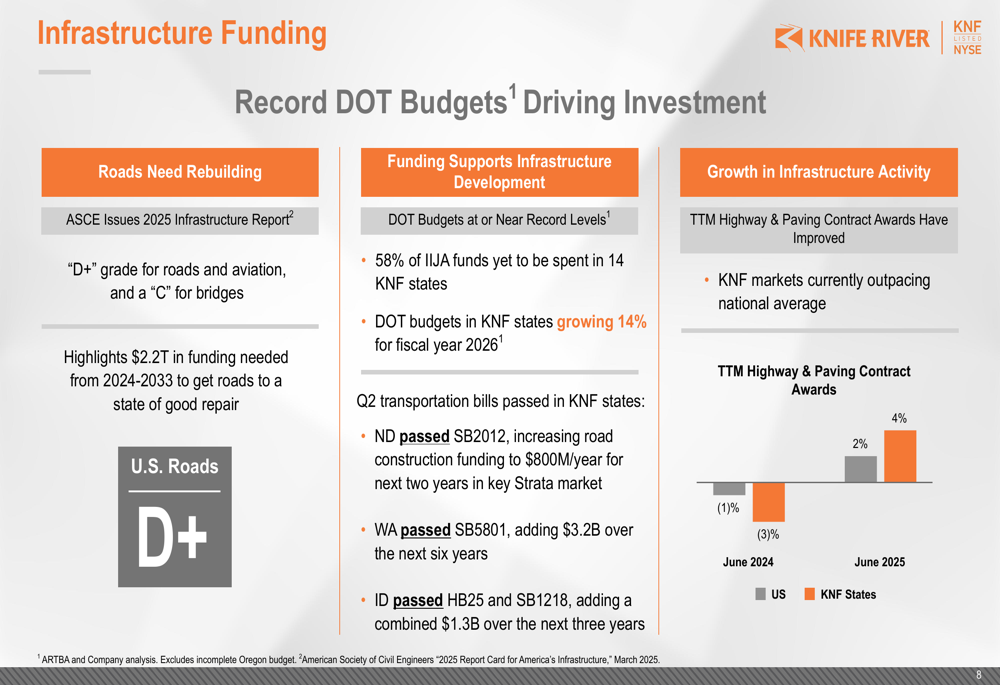

The infrastructure investment environment remains favorable for Knife River’s long-term prospects. The American Society of Civil Engineers (ASCE) gave U.S. infrastructure a "D+" grade for roads and aviation and a "C" for bridges, highlighting the need for significant investment. Additionally, 58% of Infrastructure Investment and Jobs Act (IIJA) funds remain to be spent in Knife River’s 14 operating states.

Forward-Looking Statements

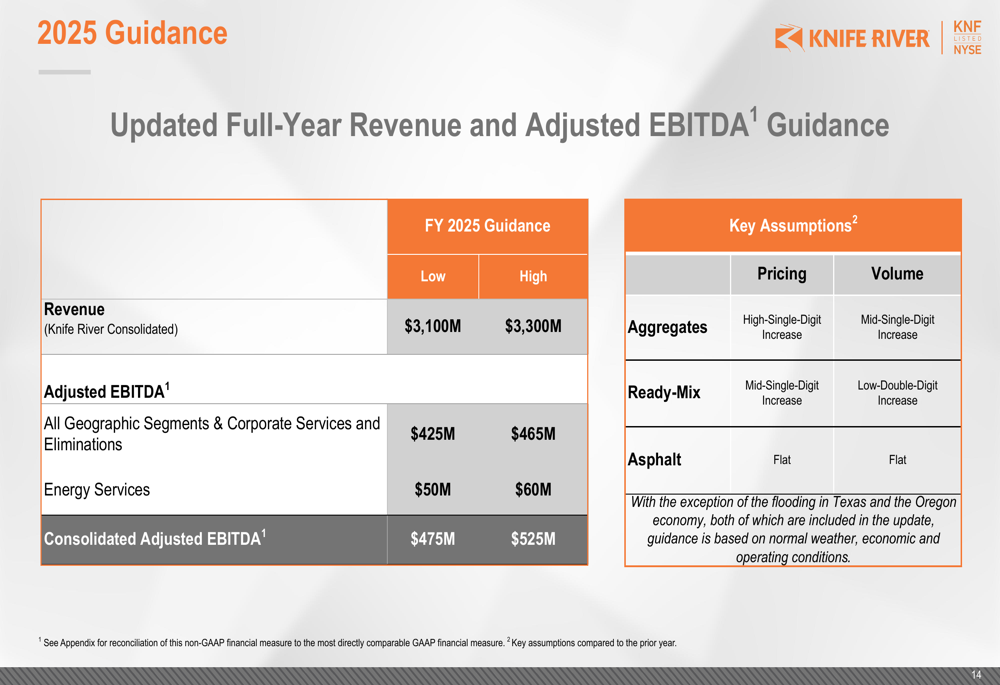

In response to the challenging first half, Knife River revised its full-year 2025 guidance downward. Revenue is now projected at $3.10-$3.30 billion, down from the previous guidance of $3.25-$3.45 billion. Adjusted EBITDA guidance was reduced to $475-$525 million from $530-$580 million previously.

The updated guidance assumes normal weather and economic conditions for the remainder of the year, with the exception of flooding in Texas and continued economic challenges in Oregon:

Management provided a detailed breakdown of the $55 million guidance revision, noting that 75% of the impact was weighted to the first half of the year. Factors affecting the revision include the softer Oregon market, unfavorable weather, energy services performance, and lack of asphalt paving in certain regions. Positive offsets include strong materials pricing, gain on asset sales, and contributions from recent acquisitions.

Despite the near-term challenges, Knife River expects to benefit from record state Department of Transportation budgets, with DOT funding in its operating states projected to grow 14% for fiscal year 2026. The company also anticipates net leverage to improve to below 2.5x by year-end, suggesting confidence in stronger cash flow generation in the second half of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.