Fannie Mae, Freddie Mac shares tumble after conservatorship comments

Introduction & Market Context

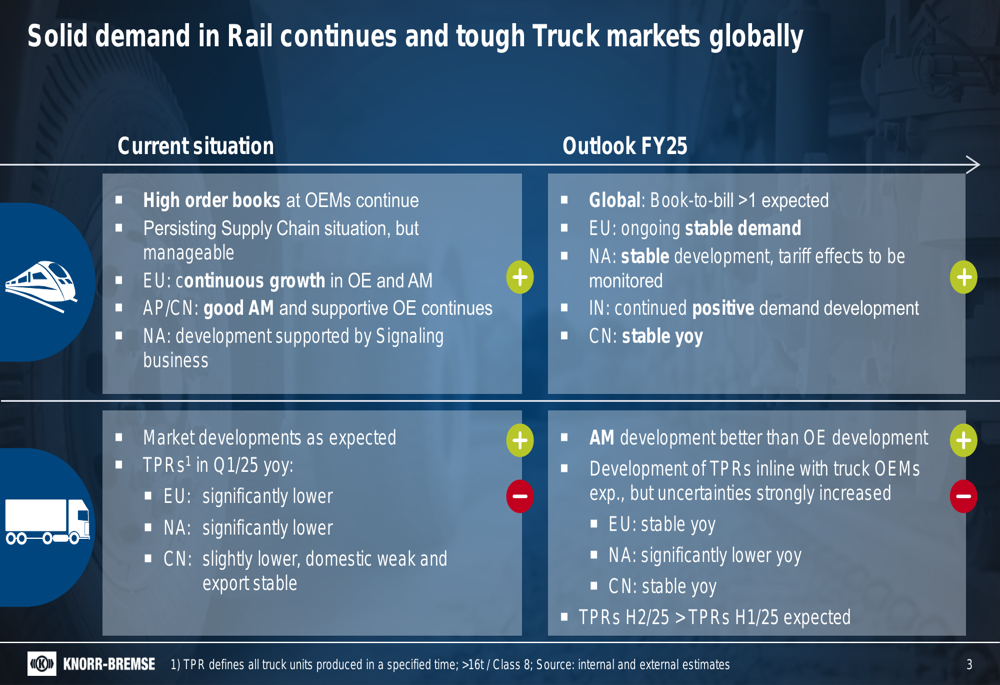

Knorr-Bremse AG (ETR:KBX) presented its Q1 2025 financial results on May 8, highlighting a stable performance amid challenging market conditions, particularly in the commercial vehicle sector. The German braking systems manufacturer reported mixed results with its Rail Vehicle Systems (RVS) division showing strong growth while the Commercial Vehicle Systems (CVS) segment faced significant headwinds.

The company emphasized its balanced business model with a 49% revenue share from Europe, 27% from North America, and 24% from Asia-Pacific, positioning it well to navigate current geopolitical uncertainties. Knorr-Bremse’s stock has shown resilience despite the earnings miss, with shares rebounding 1.44% in recent trading sessions.

As shown in the following overview of key market conditions for both segments:

Quarterly Performance Highlights

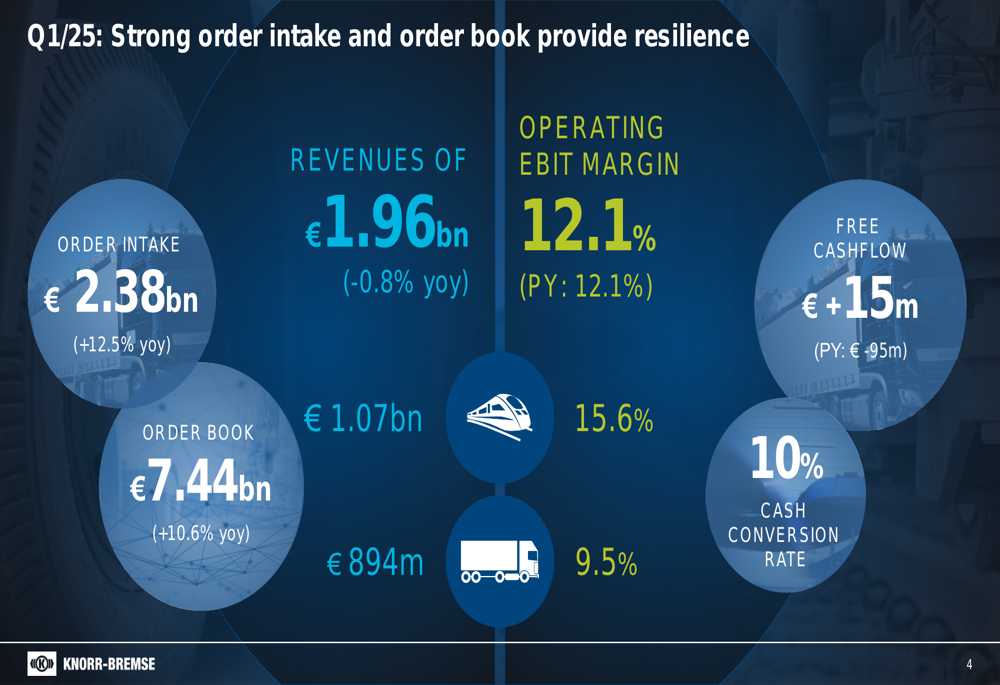

Knorr-Bremse reported Q1 2025 revenue of €1.96 billion, representing a slight decrease of 0.8% year-over-year and falling just short of the €1.98 billion forecast. Despite this, the company maintained its operating EBIT margin at 12.1%, unchanged from the previous year. Earnings per share came in at €0.84, missing analyst expectations of €1.00.

A notable bright spot was the 12.5% year-over-year increase in order intake to €2.38 billion, while the order book grew by 10.6% to €7.44 billion. Free cash flow improved significantly to €15 million, compared to negative €95 million in the same period last year.

The following chart illustrates these key financial metrics:

The company’s revenue split continues to shift toward the rail segment, with RVS contributing €1.07 billion and CVS €894 million. This balanced portfolio approach has helped Knorr-Bremse maintain stability despite the challenging truck market.

Segment Analysis: Rail Vehicle Systems (RVS)

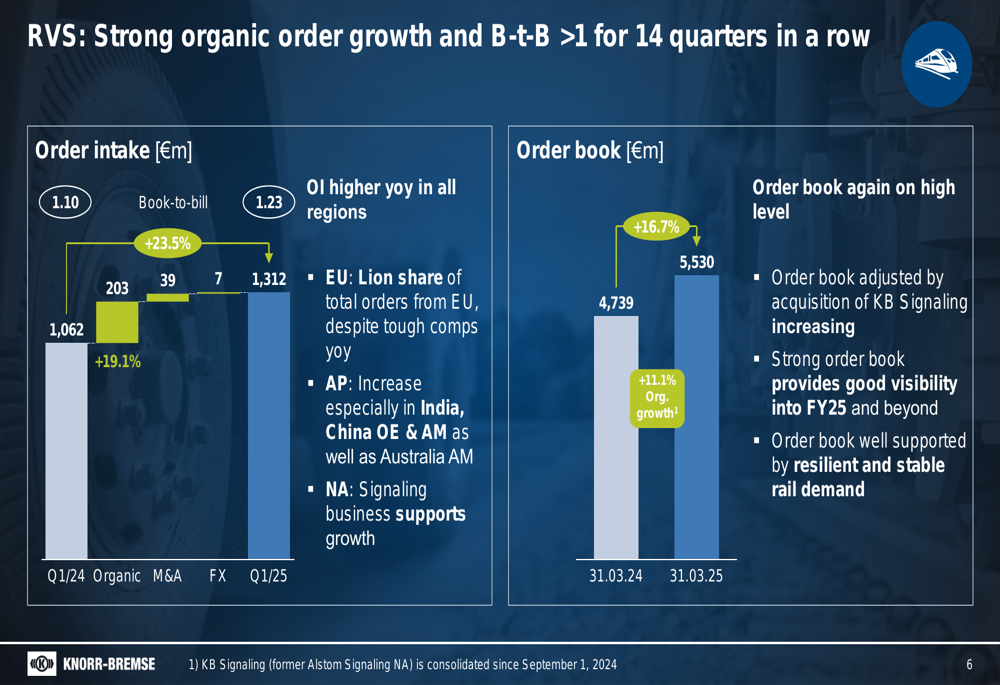

The Rail Vehicle Systems division delivered a strong performance in Q1 2025, with order intake increasing by 23.5% to €1.23 billion. The order book grew by 16.7% to €5.53 billion, demonstrating robust demand across all regions.

As illustrated in the following chart of RVS order development:

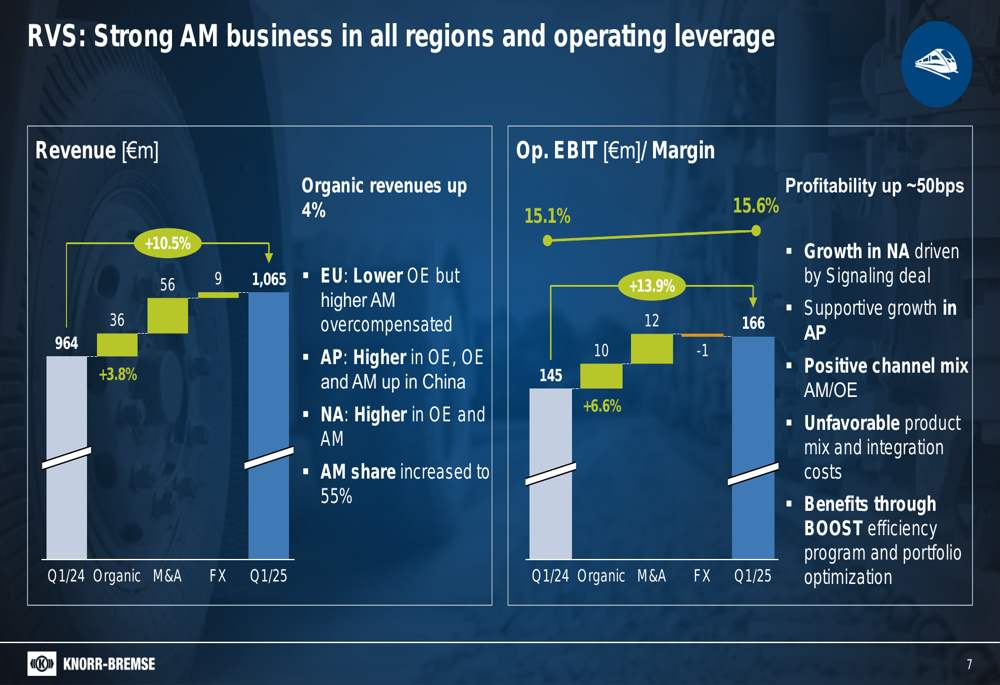

Revenue in the RVS segment increased organically by 4%, with particularly strong performance in the aftermarket business, which now represents 55% of the segment’s revenue. This favorable channel mix helped drive operating EBIT margin improvement from 15.1% to 15.6%.

The following chart details the revenue and margin development in the RVS segment:

Growth in North America was supported by the integration of the recently acquired signaling business, while Asia-Pacific showed positive development, particularly in India and China. The company noted that its BOOST efficiency program and portfolio optimization efforts are delivering benefits despite some integration costs and unfavorable product mix effects.

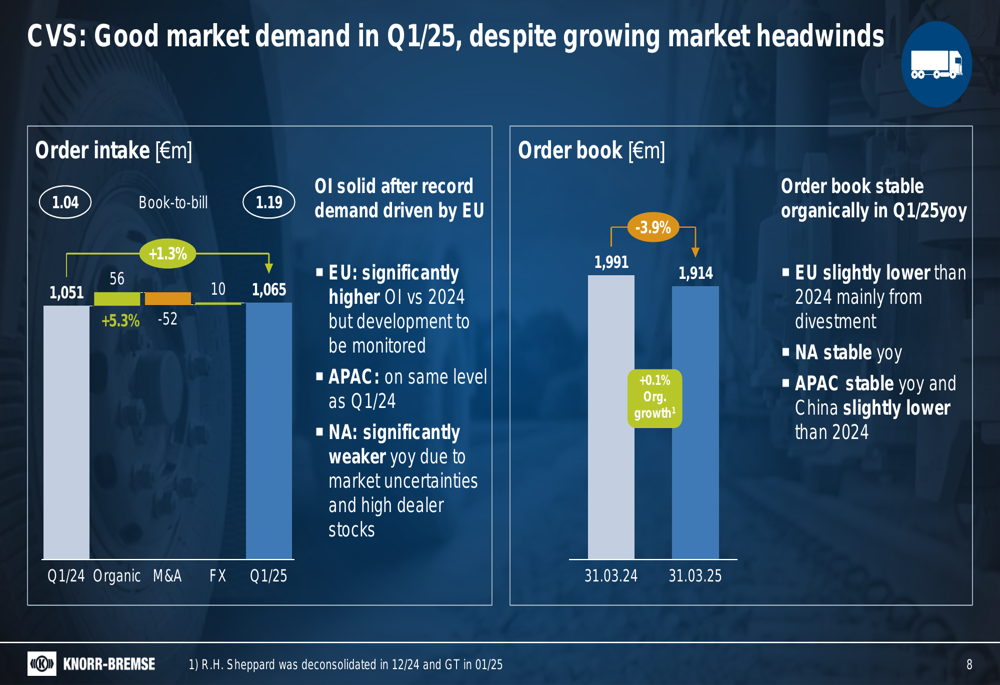

Segment Analysis: Commercial Vehicle Systems (CVS)

In contrast to the rail division, Knorr-Bremse’s Commercial Vehicle Systems segment faced significant challenges in Q1 2025. While order intake increased slightly by 1.3% to €1.05 billion, the order book decreased by 3.9% to €1.91 billion.

The following chart shows the CVS order development:

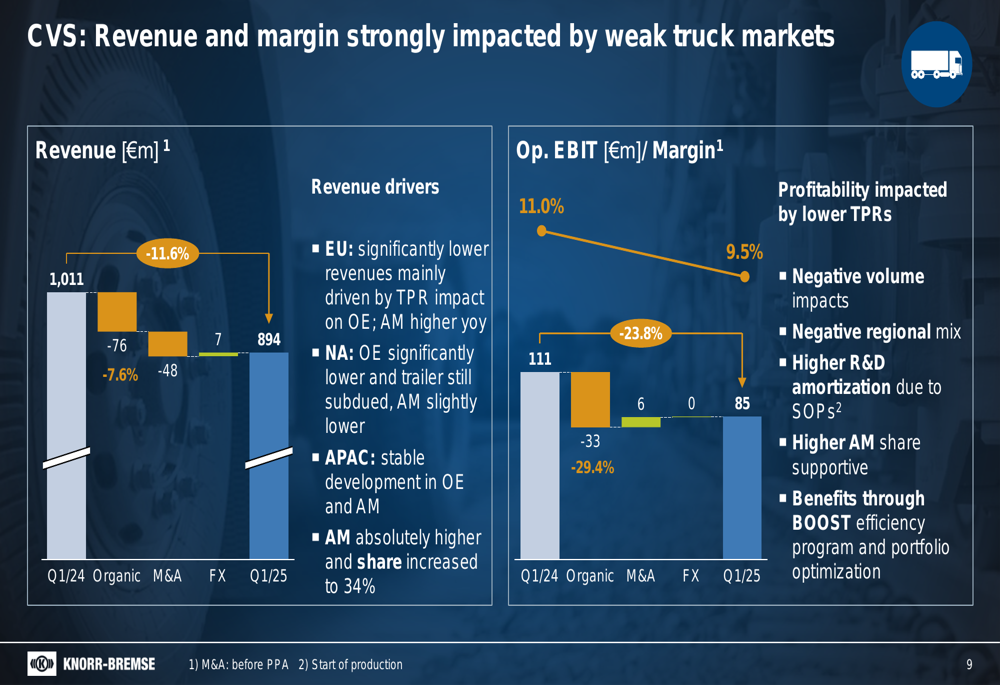

Revenue in the CVS segment declined by 11.6% to €894 million, primarily due to significantly lower truck production rates in Europe and North America. This volume decline, combined with higher R&D amortization, led to a decrease in operating EBIT margin from 11.0% to 9.5%.

The following chart illustrates the revenue and margin development in the CVS segment:

Despite these challenges, the aftermarket business showed resilience, with its share increasing to 34% of segment revenue. Management highlighted that the BOOST efficiency program and portfolio optimization are helping to partially offset the negative volume impacts.

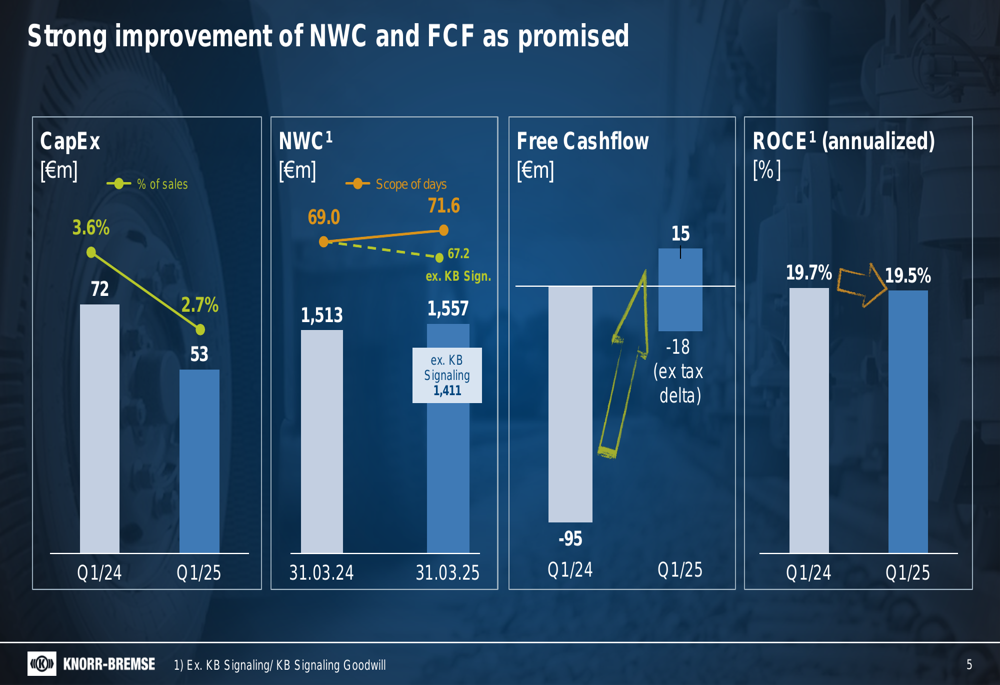

Financial Position and Cash Flow

Knorr-Bremse demonstrated improved financial discipline in Q1 2025, with capital expenditure decreasing from €72 million (3.6% of sales) in Q1 2024 to €53 million (2.7% of sales). This reduction, along with better working capital management, contributed to the positive free cash flow of €15 million, a significant improvement from the negative €95 million in the same period last year.

The following chart details the improvements in working capital and cash flow:

Net working capital increased slightly to €1.56 billion as of March 31, 2025, compared to €1.51 billion a year earlier. However, excluding the impact of the KB Signaling acquisition, net working capital would have decreased to €1.41 billion, reflecting the company’s focus on efficiency.

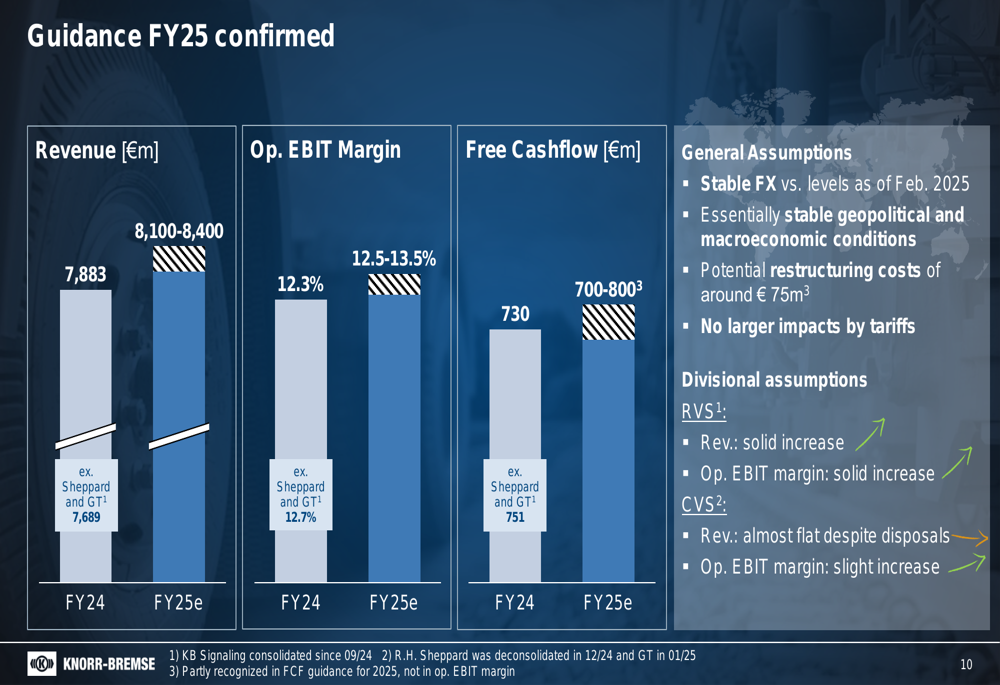

Forward-Looking Statements

Despite the mixed Q1 results, Knorr-Bremse confirmed its full-year 2025 guidance, projecting revenue of €8.1-8.4 billion, an operating EBIT margin of 12.5-13.5%, and free cash flow of €700-800 million.

The guidance is based on several key assumptions, including stable foreign exchange rates, essentially stable geopolitical and macroeconomic conditions, potential restructuring costs of around €75 million, and no significant impacts from tariffs.

As shown in the following guidance overview:

For the Rail Vehicle Systems division, the company expects a solid increase in both revenue and operating EBIT margin. The Commercial Vehicle Systems segment is projected to deliver almost flat revenue despite planned disposals, with a slight increase in operating EBIT margin.

CEO Marc Llistosella emphasized that Knorr-Bremse is well-positioned in challenging geopolitical times, with a balanced revenue mix and strong financial position. The company’s BOOST program, which includes carve-outs and efficiency measures, is progressing as planned and is expected to support margin improvement throughout 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.