Nvidia among investors in xAI’s $20 bln capital raise- Bloomberg

Introduction & Market Context

Knowles Corporation (NYSE:KN) released its first quarter 2025 earnings presentation on April 24, showing signs of stabilization after missing analyst expectations in the previous quarter. The company’s stock closed at $14.82 on the earnings day and saw minimal movement in after-hours trading, with shares up just 0.06% to $15.65.

The presentation comes after a challenging fourth quarter where Knowles missed both EPS and revenue forecasts, which had triggered a 7.21% stock decline. The company appears to be regaining its footing following the completion of its consumer MEMS microphone business divestiture, focusing on its core segments in specialty audio, medical technology, and precision devices.

Quarterly Performance Highlights

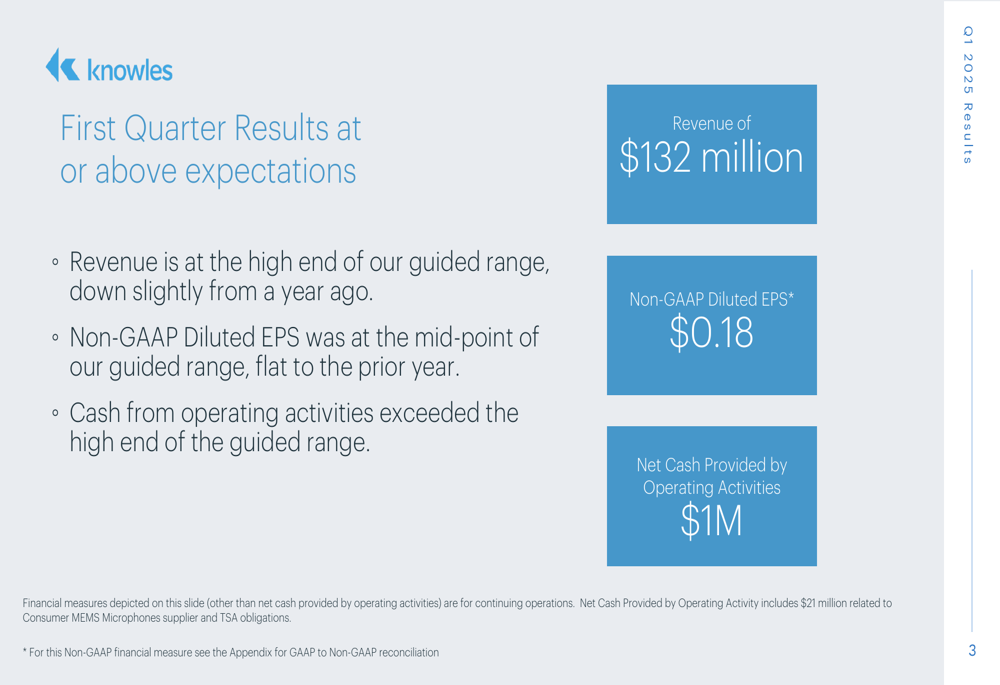

Knowles reported Q1 2025 revenue of $132 million, reaching the high end of its guided range though slightly down from the year-ago period. Non-GAAP diluted earnings per share came in at $0.18, matching the midpoint of guidance and remaining flat compared to Q1 2024.

As shown in the following quarterly results overview:

The company generated $1 million in net cash from operating activities, exceeding the high end of its guided range. However, this figure includes $21 million related to Consumer MEMS Microphones supplier and TSA obligations, suggesting underlying operational cash flow was stronger than the headline figure indicates.

Segment Analysis

Knowles’ performance showed diverging trends across its two main business segments, with MedTech & Specialty Audio showing growth while Precision Devices experienced a slight decline.

The MedTech & Specialty Audio segment posted a 1.2% year-over-year revenue increase to $59.7 million, driven by higher demand in specialty audio products. However, adjusted EBITDA margins contracted significantly, dropping 450 basis points to 39.2% due to unfavorable customer mix and the absence of one-time benefits that had boosted the prior year’s results.

As illustrated in the segment performance chart:

Management expects MedTech & Specialty Audio margins to improve sequentially throughout 2025, with full-year adjusted EBITDA margins projected to reach the low 40% range, driven by mix improvements and higher capacity utilization.

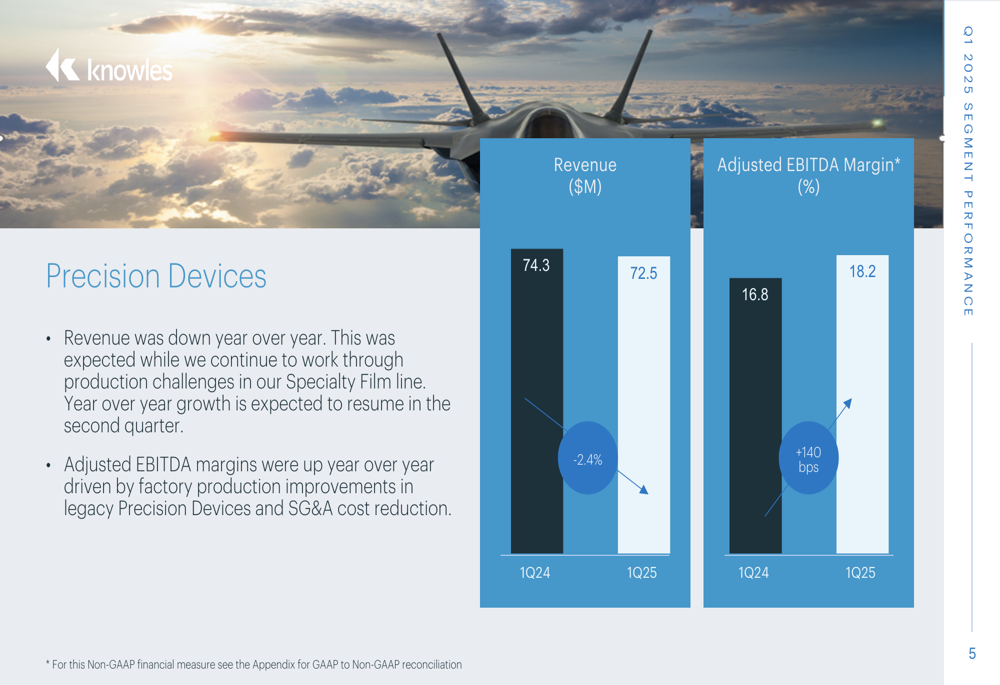

Meanwhile, the Precision Devices segment saw revenue decline by 2.4% year-over-year to $72.5 million, though management anticipates improvement in the second quarter. Despite lower sales, the segment achieved margin expansion, with adjusted EBITDA margins increasing 140 basis points to 18.2%, benefiting from factory production improvements and SG&A cost reductions.

The Precision Devices performance is detailed in the following chart:

This segment improvement is particularly notable given the production challenges in specialty film capacitors mentioned during the company’s Q4 2024 earnings call, suggesting some operational issues may be resolving.

Financial Position & Debt

Knowles maintains a solid financial position with $101.9 million in cash and cash equivalents as of March 31, 2025. The company’s total debt stands at $188.8 million, resulting in a net debt position of $86.9 million.

With trailing 12-month Adjusted EBITDA of $126.7 million, Knowles’ net debt leverage ratio is a conservative 0.7x, providing financial flexibility for potential strategic investments or shareholder returns.

Forward Guidance & Outlook

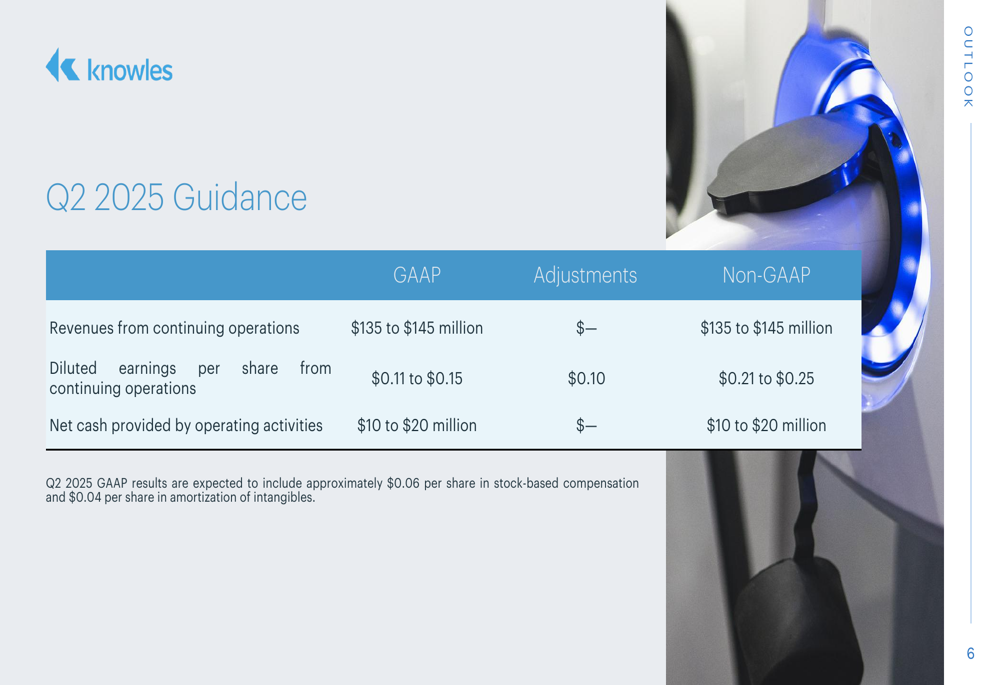

Looking ahead to the second quarter, Knowles provided guidance that suggests sequential improvement in both revenue and earnings. The company expects Q2 2025 revenue to range between $135 million and $145 million, representing potential sequential growth of 2.3% to 9.8%.

Non-GAAP diluted EPS is projected to reach $0.21 to $0.25, a significant improvement from the $0.18 reported in Q1 2025. Net cash provided by operating activities is expected to be $10 to $20 million.

The detailed Q2 2025 guidance is presented in the following slide:

This outlook aligns with management’s previous statements about returning to growth in Q2 2025, as mentioned in the company’s Q4 2024 earnings call. The projected improvement suggests the company is successfully navigating its transition following the divestiture of its consumer MEMS microphone business.

Knowles appears positioned for stronger performance in the coming quarters, with improving operational metrics and a continued focus on its core high-margin segments. Investors will be watching closely to see if the company can deliver on its projected sequential growth and margin improvements throughout the remainder of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.