Gold prices inch up with record in sight ahead of key U.S. jobs data

Introduction & Market Context

Finnish elevator and escalator manufacturer KONE Oyj (HE:KNEBV) presented its Q1 2025 interim report on April 30, 2025, highlighting solid performance driven by strong Service and Modernization segments despite continued weakness in the Chinese market. The company reported consistent profitability improvement as its strategic initiatives gained traction across global markets.

KONE operates in a global elevator and escalator market with an installed base of approximately 25 million units growing at low single digits. The company identified significant opportunities in both the Service segment and the Modernization market, where approximately 10 million units are over 15 years old and due for upgrades.

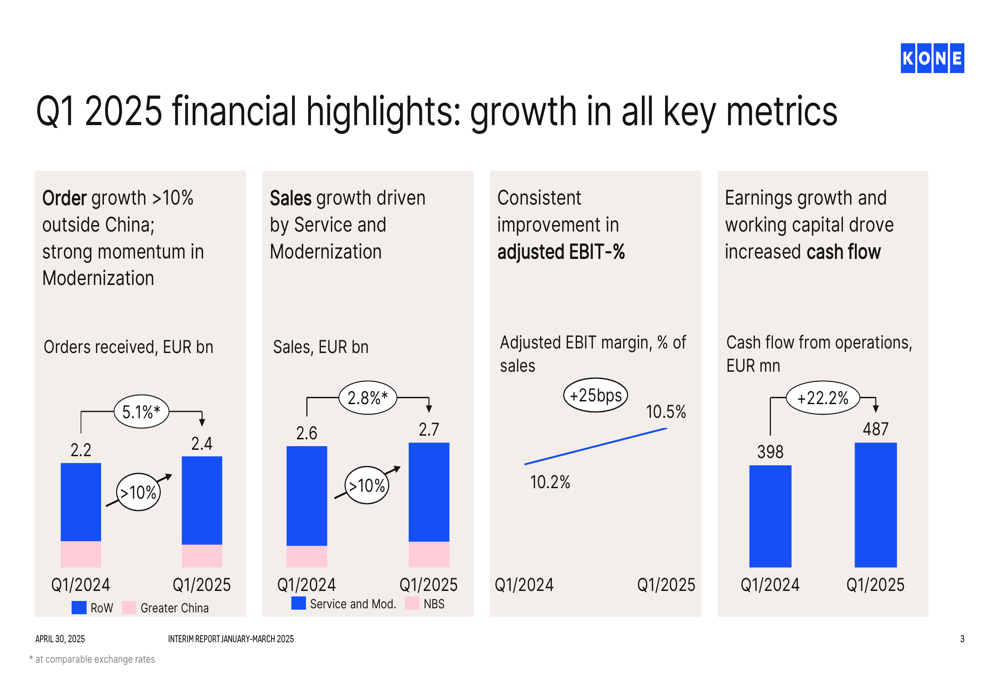

As shown in the following chart of Q1 2025 financial highlights, KONE achieved growth in orders received, sales, adjusted EBIT margin, and cash flow from operations:

Quarterly Performance Highlights

KONE reported Q1 2025 orders received of EUR 2.4 billion, representing a 6.4% increase year-over-year (5.1% at comparable exchange rates). Sales reached EUR 2.7 billion, up 4.1% from the same period last year. The company’s adjusted EBIT margin improved by 25 basis points to 10.5%, while cash flow from operations surged 22.2% to EUR 487 million.

The performance was characterized by strong growth in Service sales (8.5% at comparable exchange rates) and exceptional development in the Modernization segment, which saw approximately 20% growth in both orders and sales. These positive trends helped offset a roughly 15% decline in orders from Greater China, demonstrating the company’s reduced dependency on this previously dominant market.

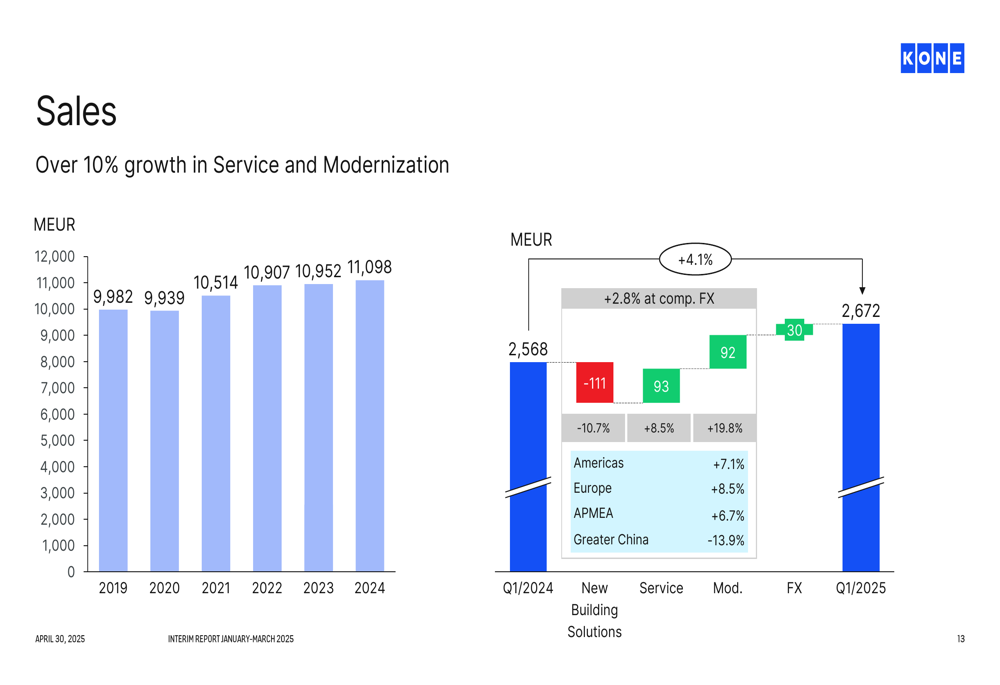

The breakdown of sales by business segment and geographic area provides further insight into KONE’s diversification strategy:

Service now accounts for 44% of total sales (up from 42% in Q1 2024), while New Building Solutions decreased to 35% (from 38%). Geographically, the Americas region increased to 26% of sales (from 24%), while Greater China’s contribution fell to 14% (from 19%), reflecting both market challenges in China and successful growth initiatives elsewhere.

Regional Performance Analysis

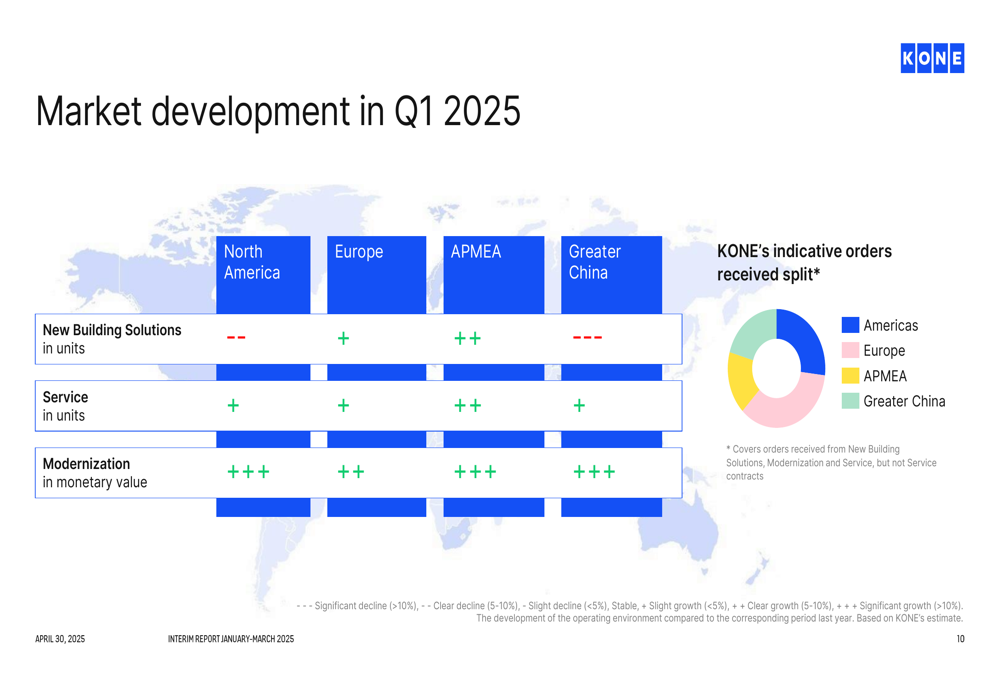

KONE’s performance varied significantly by region in Q1 2025, with markets outside China showing robust growth momentum. Orders received grew by more than 10% in regions outside Greater China, particularly in the Americas and APMEA (Asia-Pacific, Middle East, and Africa).

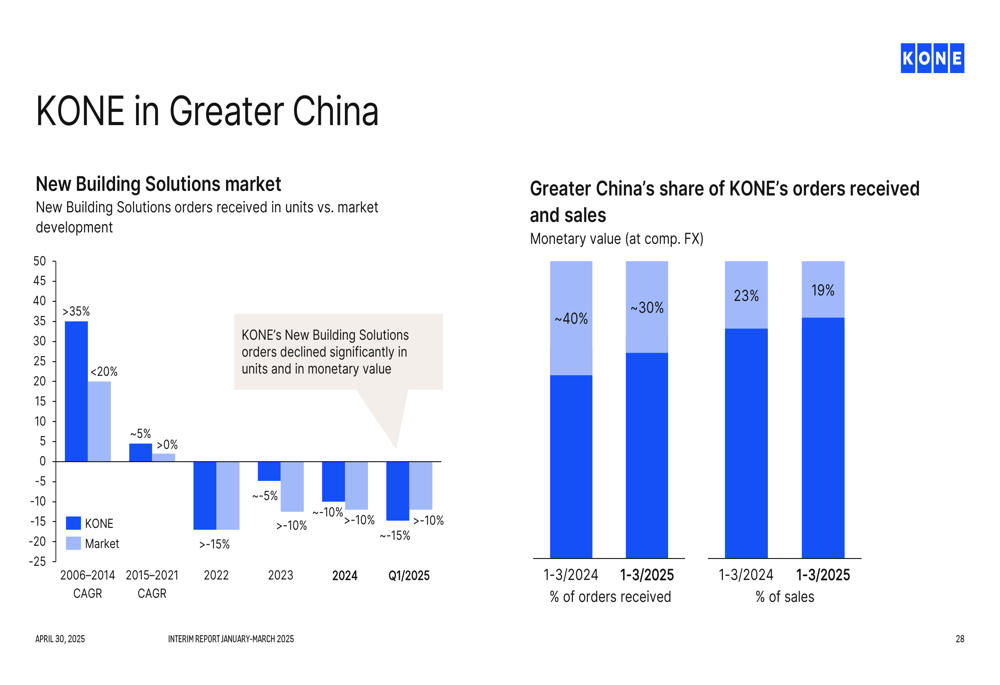

The following visualization illustrates KONE’s changing exposure to the Chinese market:

Greater China’s contribution to KONE’s order book has declined from approximately 40% in Q1 2024 to around 30% in Q1 2025, while its share of sales dropped from about 30% to 19%. This shift reflects both the challenging market conditions in China and KONE’s successful diversification strategy.

The market development across regions shows particularly strong performance in Modernization across all markets, while New Building Solutions faced challenges in most regions:

The company noted that the new construction market in China remained under pressure, with only slight improvements in liquidity. KONE highlighted that policy actions and improved sentiment would be key to recovery in this region, while also noting intense competition in the New Building Solutions pricing environment.

Strategic Initiatives

KONE’s strategic execution appears to be on track, with several initiatives showing positive results. In the Service segment, the company accelerated the deployment of digital solutions, with connectivity reaching approximately 36% and Dynamic Maintenance Planning now live in 22 countries.

The Modernization segment showed good progress in driving partial modernization, with KONE MonoSpace DX Upgrade orders increasing by nearly 30% in Europe. In New Building Solutions, the company strengthened its position in low-rise residential with the KONE MonoSpace 100 DX now available in 19 countries and receiving positive customer response.

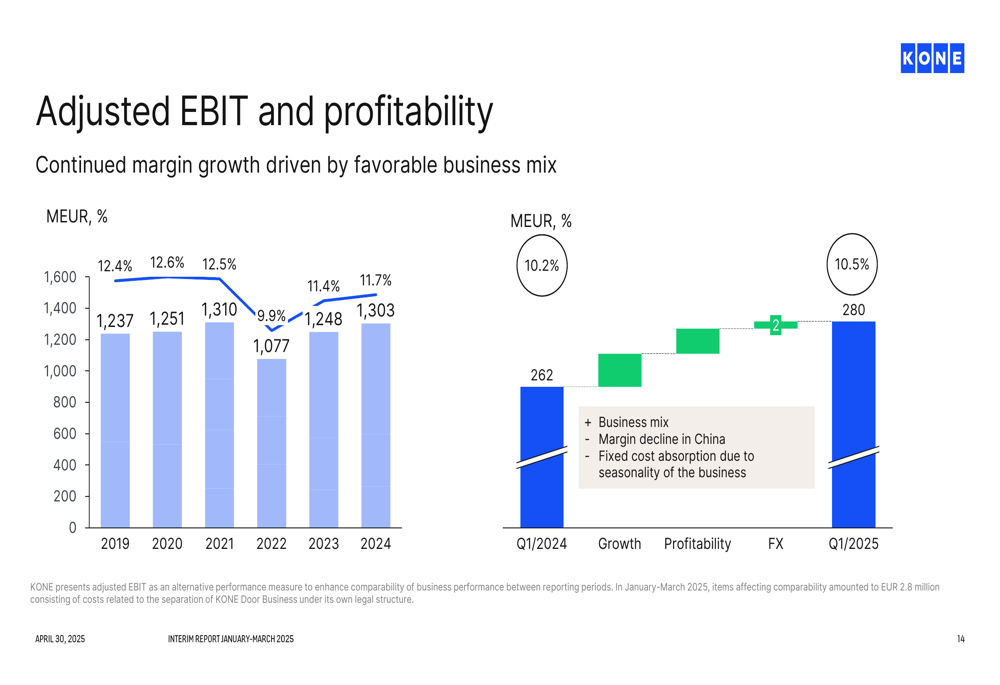

KONE’s profitability improvement demonstrates the effectiveness of these strategic initiatives, as shown in the following chart:

The adjusted EBIT margin increased from 10.2% in Q1 2024 to 10.5% in Q1 2025, driven primarily by favorable business mix, despite some negative impact from China and fixed costs absorption effects.

Business Outlook for 2025

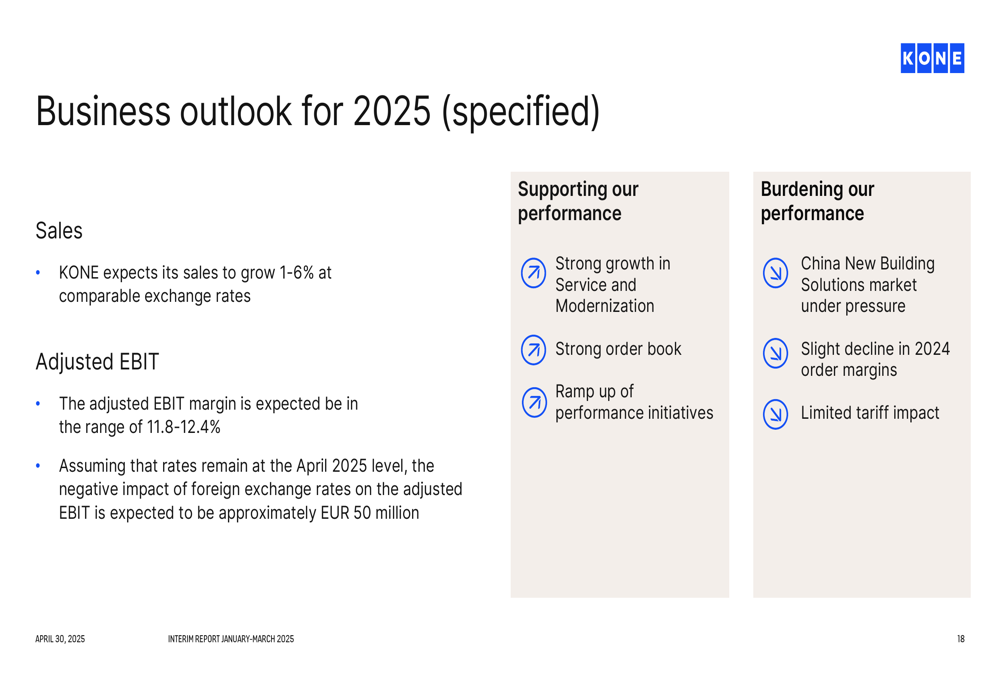

Looking ahead, KONE provided a detailed business outlook for 2025, expecting resilient growth in Service and Modernization segments while acknowledging continued challenges in the New Building Solutions market, particularly in China:

The company expects sales to grow 1-6% at comparable exchange rates in 2025, with the adjusted EBIT margin projected to be in the range of 11.8-12.4%. This outlook is supported by strong growth in Service and Modernization, a robust order book, and various ramp-up initiatives. However, the continued challenges in the Chinese market, slight decline in New Building Solutions, and limited tariff impact are expected to burden performance.

KONE’s market position remains strong, with the company maintaining market leadership in New Building Solutions with close to 20% share globally, while continuing as a challenger in the Service market with approximately 10% share. This positioning, combined with the company’s strategic focus on higher-margin segments and geographic diversification, provides a solid foundation for future growth despite ongoing market challenges in China.

In conclusion, KONE’s Q1 2025 results demonstrate the company’s ability to navigate challenging market conditions through strategic diversification and focus on high-growth, high-margin segments. The consistent improvement in profitability, despite headwinds in China, suggests that the company’s strategy is delivering results and positioning KONE for sustainable growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.