Gold rally takes a breather amid Gaza ceasefire, Fed minutes

Introduction & Market Context

Kraft Heinz (NASDAQ:KHC) presented its Q2 2025 business update on July 30, highlighting sequential improvement from Q1 despite year-over-year declines in key metrics. The company’s stock was up 0.7% in premarket trading at $28.76, showing modest investor optimism following the presentation.

The food giant continues to navigate a challenging consumer environment while focusing on strategic investments in its brand portfolio and emerging markets. After experiencing a 4.7% decline in organic net sales during Q1, the company showed improvement with a more modest 2.0% decline in Q2, suggesting that its strategic initiatives may be gaining traction.

Quarterly Performance Highlights

Kraft Heinz reported Q2 2025 results largely in line with expectations, with total revenue of $6.3 billion. Organic net sales declined 2.0%, showing sequential improvement from the 4.7% drop in Q1. Adjusted gross profit margin came in at 34.1%, down 140 basis points compared to the prior year.

As shown in the following financial performance summary:

The company’s adjusted operating income on a constant currency basis was $1.3 billion, representing a 7.7% decline versus the prior year. Adjusted EPS fell 11.5% to $0.69, though this represents an improvement from the $0.62 reported in Q1. A bright spot in the results was year-to-date free cash flow of $1.5 billion, up 29% compared to the prior year.

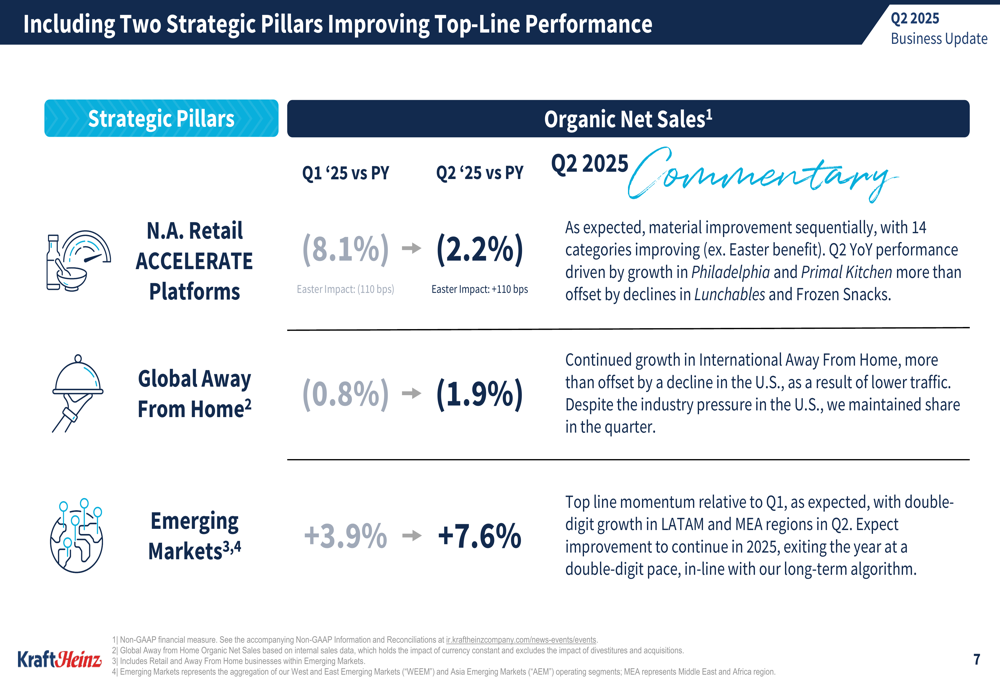

Regional performance varied significantly, with emerging markets showing strong growth while developed markets faced continued headwinds. The company’s strategic pillars demonstrated different trajectories as illustrated in this breakdown:

North America retail platforms showed material sequential improvement from Q1 to Q2, with the year-over-year decline improving from 8.1% to 2.2%. Global Away From Home performance remained challenging, particularly in the U.S. due to lower traffic, though the company maintained market share. Emerging markets continued to accelerate, posting 7.6% growth in Q2 compared to 3.9% in Q1, with double-digit growth in Latin America and Middle East/Africa regions.

Strategic Initiatives

Kraft Heinz is focusing on its Brand Growth System (BGS) as a key driver for future performance. The company plans to significantly expand the coverage of this system from approximately 10% of sales in 2024 to an estimated 40% by the end of 2025.

The following illustration shows how the company is implementing its brand growth strategy:

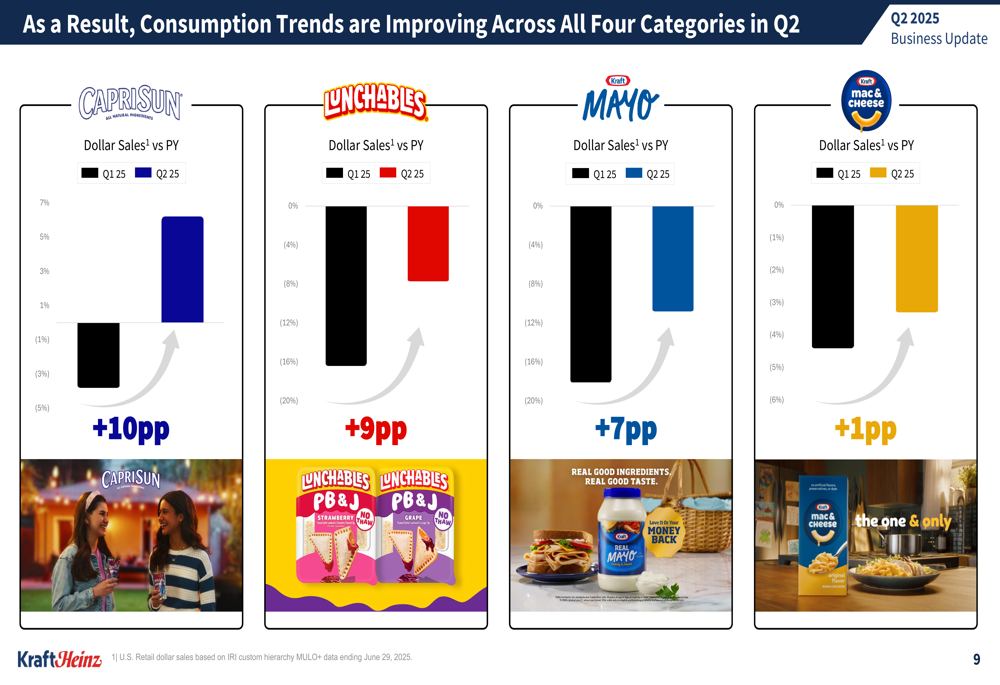

The BGS approach appears to be yielding results for key brands, with consumption trends showing improvement across several product lines. The company highlighted positive momentum in brands like Caprisun, Lunchables, Kraft Mayo, and Kraft Mac & Cheese:

Innovation remains a central focus for Kraft Heinz as it seeks to drive growth through new product offerings and brand extensions. The company is exploring new flavors, expanding accessibility, and delivering unique health-focused benefits to meet evolving consumer preferences:

Financial Analysis

Despite top-line pressure, Kraft Heinz continues to generate strong cash flow and maintain its commitment to shareholder returns. The company has returned $1.4 billion to stockholders year-to-date, including $1 billion in dividends (representing a yield of over 5.5%) and $0.4 billion in share repurchases.

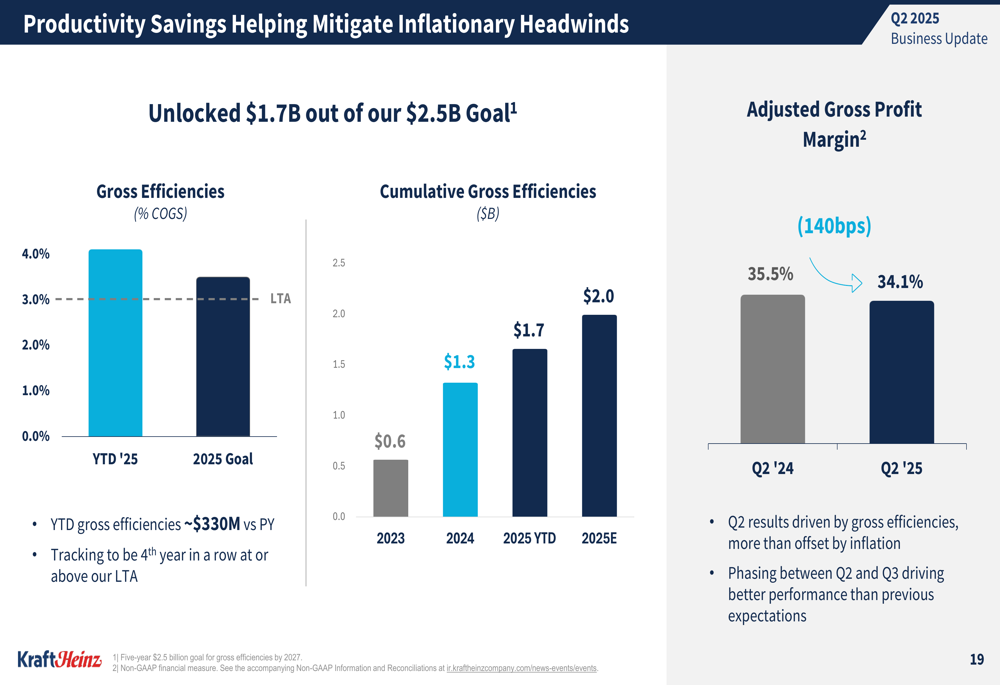

Productivity savings remain on track, with the company having unlocked $1.7 billion of its $2.5 billion goal as shown in the following chart:

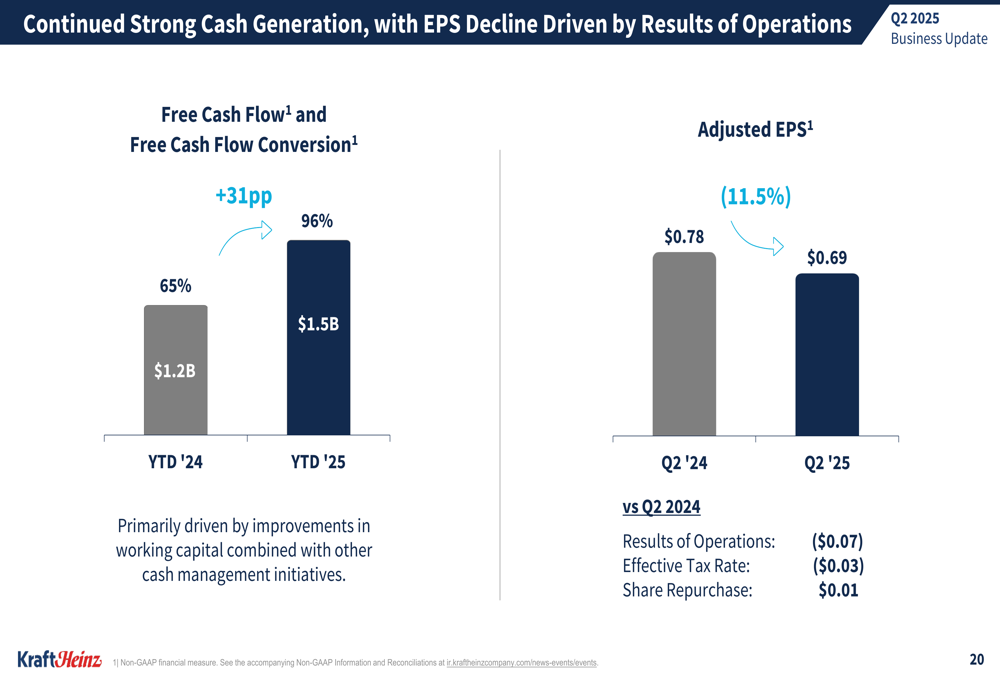

Cash generation has been particularly strong, with free cash flow conversion improving by 31 percentage points despite the decline in adjusted EPS:

The company’s inflation picture varies significantly by region, with North America experiencing deflation of 12.5% while emerging markets face inflation of 52.3%. This divergent inflation environment presents both challenges and opportunities for margin management across the company’s global portfolio.

Forward-Looking Statements

Kraft Heinz reiterated its full-year 2025 outlook, projecting organic net sales to decline between 1.5% and 3.5%, and constant currency adjusted operating income to decline between 5% and 10%. The company expects adjusted EPS to range from $2.51 to $2.67, with free cash flow projected to be flat compared to the prior year.

The outlook reflects continued challenges in developed markets balanced by accelerating growth in emerging markets, which the company expects to exit 2025 at a double-digit growth pace in line with its long-term algorithm.

CEO Carlos Abrams-Rivera emphasized the company’s commitment to disciplined investments to provide value to consumers while driving product and brand superiority. CFO Andre Maciel highlighted the company’s strong cash generation capabilities and commitment to maintaining its net leverage target while returning capital to stockholders.

As Kraft Heinz navigates through 2025, its focus on brand growth, emerging markets expansion, and productivity savings will be critical to offsetting the headwinds in its core developed markets. While near-term challenges persist, the sequential improvement from Q1 to Q2 suggests the company’s strategic initiatives may be starting to gain traction.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.