Intel stock spikes after report of possible US government stake

Krispy Kreme Inc (NASDAQ:DNUT) shares fell 3.51% in Thursday’s premarket trading after the company’s Q2 2025 earnings presentation revealed a substantial net loss and outlined a comprehensive turnaround strategy. The donut chain’s stock, which has already declined over 65% in the past year, traded at $3.30 following the August 7 presentation.

Quarterly Performance Highlights

Krispy Kreme reported net revenue of $379.8 million for the second quarter of fiscal 2025, with organic revenue declining 0.8% compared to the same period last year. The company posted a GAAP net loss of $441.1 million, primarily due to non-cash goodwill and other asset impairment charges totaling $406.9 million.

Adjusted EBITDA came in at $20.1 million, while cash used for operating activities was $32.5 million. Despite financial challenges, the company continued to expand its reach, with global Points of Access (POA) increasing by 2,260 locations, or 14.3%, to 18,113.

As shown in the following quarterly highlights:

These results follow a disappointing first quarter where Krispy Kreme missed earnings expectations with a negative EPS of $0.05 and revenue of $375.2 million, slightly below analyst forecasts.

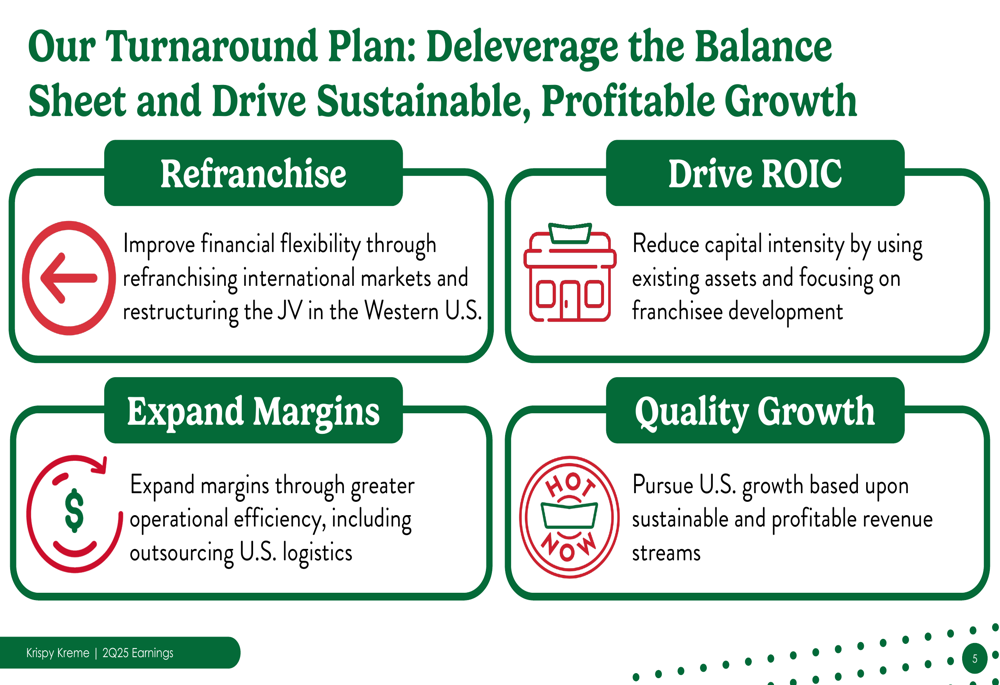

Turnaround Strategy

CEO Josh Charlesworth is spearheading a comprehensive turnaround plan focused on deleveraging the balance sheet and driving sustainable, profitable growth. The strategy is built around four key pillars: refranchising to improve financial flexibility, driving return on invested capital (ROIC), expanding margins through operational efficiency, and pursuing quality growth with sustainable revenue streams.

The company’s strategic framework is illustrated in this turnaround plan overview:

This strategic pivot comes as Krispy Kreme faces significant challenges, including the recent end of its McDonald’s (NYSE:MCD) USA partnership, which was initially paused during Q1 2025. The company’s purpose statement, "To touch & enhance lives through the joy that is," remains central to its business approach, supported by five strategic focus areas.

As shown in the company’s purpose and strategy framework:

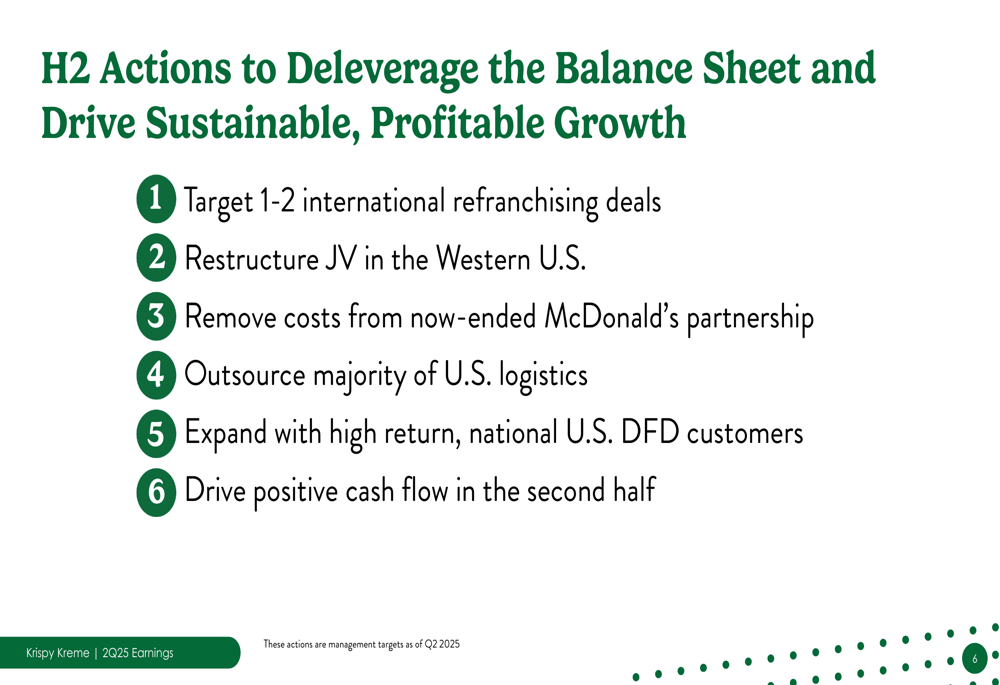

H2 2025 Strategic Initiatives

For the second half of fiscal 2025, Krispy Kreme has outlined six specific actions to deleverage its balance sheet and improve financial performance:

1. Targeting one to two international refranchising deals

2. Restructuring joint ventures in the Western United States

3. Removing costs associated with the now-ended McDonald’s partnership

4. Outsourcing the majority of U.S. logistics operations

5. Expanding with high-return, national U.S. Delivered Fresh Daily (DFD) customers

6. Driving positive cash flow in the second half

These initiatives are detailed in the following slide:

The focus on refranchising represents a significant shift in Krispy Kreme’s business model, potentially reducing capital requirements while improving financial flexibility. This approach aligns with the company’s stated goal of improving capital efficiency, a key component of its turnaround strategy.

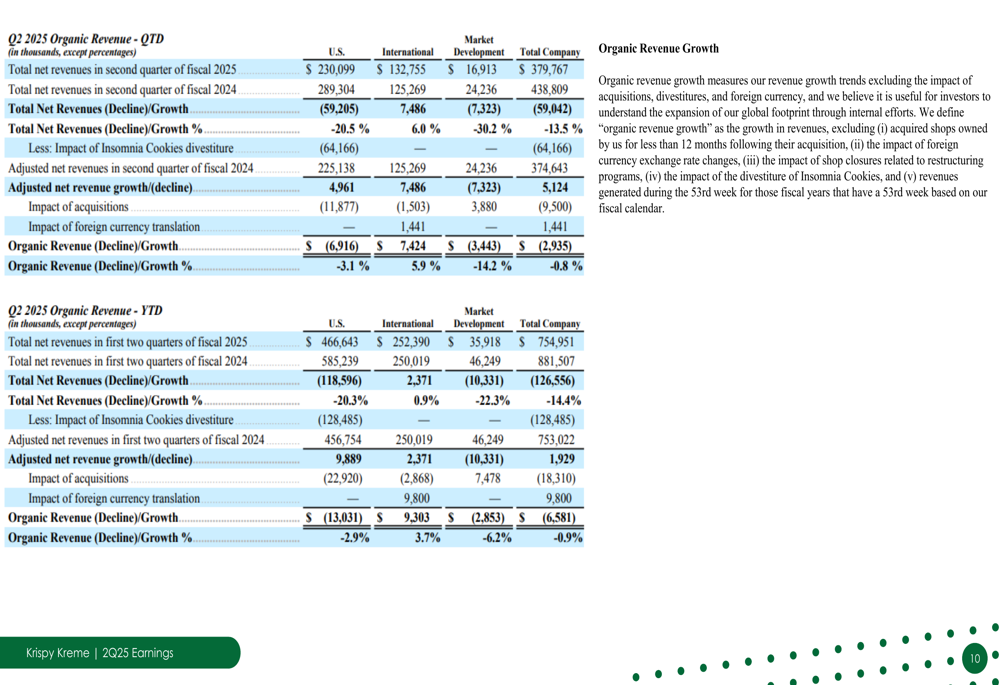

Financial Analysis

A deeper look at Krispy Kreme’s financial performance reveals continued challenges. The $441.1 million net loss, even when excluding impairment charges, indicates ongoing operational difficulties. The company’s cash flow remains negative, with $32.5 million used in operating activities during Q2.

The organic revenue decline of 0.8% suggests Krispy Kreme is struggling to grow its core business despite expanding its global footprint. This contrasts with the 14.3% increase in Points of Access, indicating that new locations may not be generating the expected revenue levels.

As detailed in the organic revenue growth breakdown:

Forward Outlook

Krispy Kreme’s presentation focused heavily on turnaround strategies rather than specific forward guidance, continuing the trend from Q1 when the company withdrew its full-year outlook. The emphasis on deleveraging and driving positive cash flow in the second half of 2025 suggests management is prioritizing financial stability over aggressive growth.

The end of the McDonald’s partnership represents both a challenge and an opportunity. While it removes a potential growth avenue, the company plans to redirect resources to more profitable channels, particularly expanding with high-return DFD customers.

Investors will be watching closely to see if Krispy Kreme’s turnaround initiatives can stem the significant stock price decline experienced over the past year. With shares trading near their 52-week low of $2.50, the company faces pressure to demonstrate that its strategic shift can deliver improved financial results and restore investor confidence.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.