S&P 500 falls as ongoing government shutdown, trade jitters weigh

Introduction & Market Context

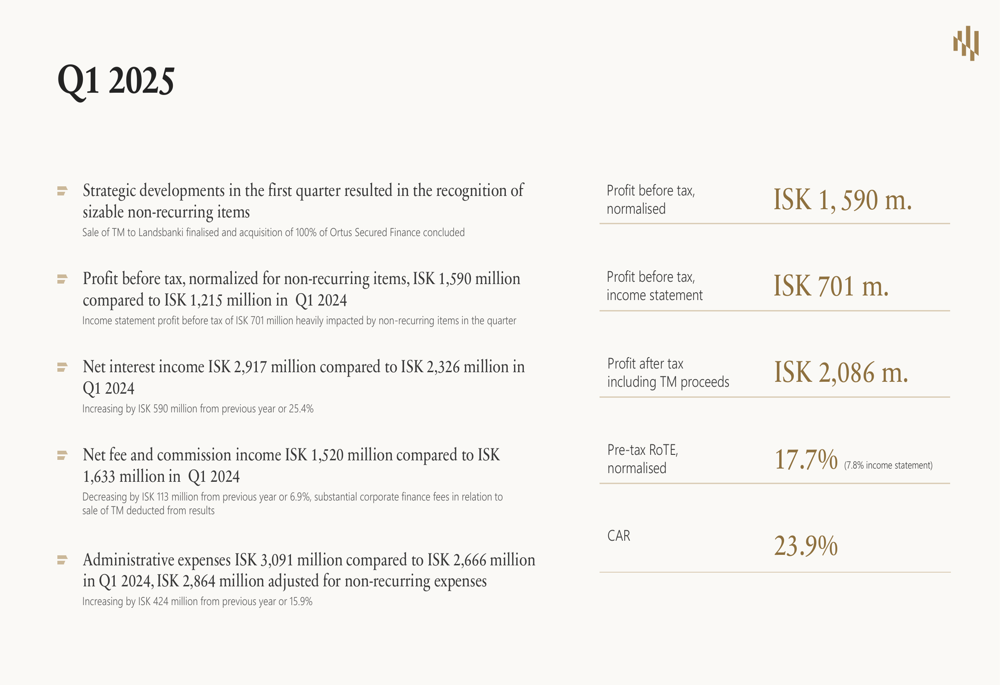

Kvika banki hf (ICE:KVIKA) shares closed at ISK 13.5 on May 7, 2025, up 0.74% following the release of its first quarter 2025 financial results. The Icelandic bank’s presentation revealed a quarter heavily impacted by strategic developments, including the divestment of TM Insurance and the accelerated acquisition of the remaining stake in UK-based Ortus Secured Finance.

These strategic moves created significant non-recurring items that masked what management described as strong underlying performance. The bank’s normalized profit before tax reached ISK 1,590 million, representing a 30.9% increase from ISK 1,215 million in Q1 2024, though reported profit before tax was considerably lower at ISK 701 million.

Executive Summary

Kvika’s Q1 2025 results showed mixed performance across key metrics. Net interest income grew impressively by 25.4% year-over-year to ISK 2,917 million, while net fee and commission income declined by 7% to ISK 1,520 million compared to Q1 2024. Administrative expenses increased to ISK 3,091 million, though ISK 225 million of this was attributed to non-recurring expenses related to strategic initiatives.

The bank reported profit after tax of ISK 2,086 million, which included proceeds from the TM Insurance divestment. Normalized pre-tax return on tangible equity (RoTE) reached 17.7%, while the reported pre-tax RoTE was 7.8%.

As shown in the following financial highlights chart, Kvika maintained a strong capital position with a Capital Adequacy Ratio of 23.9%:

Quarterly Performance Highlights

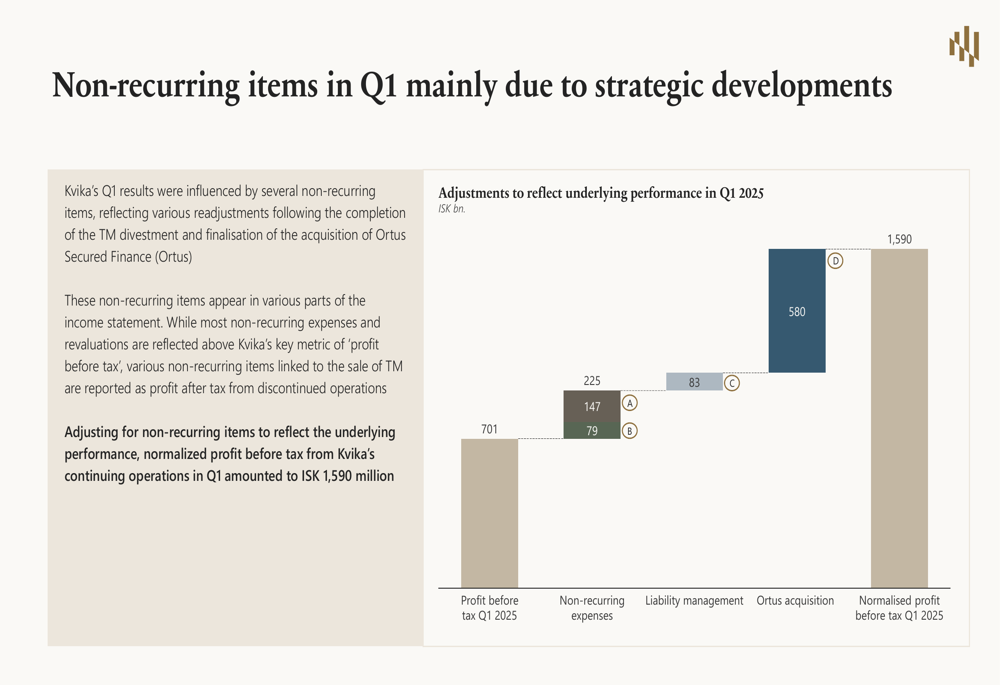

The quarter was significantly impacted by non-recurring items totaling ISK 889 million, which the bank detailed in its presentation. These items included TM divestment-related impacts (ISK 147 million), balance sheet adjustments (ISK 79 million), liability management costs (ISK 83 million), and Ortus acquisition revaluation (ISK 580 million).

The following chart breaks down these adjustments, showing how they affected the reported profit before tax:

By segment, Commercial Banking showed solid performance with a growing loan book and strong deposit base. Vehicle lending grew by 17% year-over-year in Q1, while total deposits increased by over 2% during the quarter. The bank also reported continued momentum in preparing for a new mortgage offering.

Investment Banking delivered good quarterly performance despite market volatility, with strong lending growth and successful completion of the TM sale by Corporate Finance. Asset Management faced challenges from geopolitical tensions and market volatility, with assets under management amounting to ISK 441 billion at the end of March 2025.

The UK segment was a bright spot, with strong Q1 performance driven by continued positive results at Ortus Secured Finance. The bank highlighted that Harpa completed its first private equity transaction during the quarter.

Detailed Financial Analysis

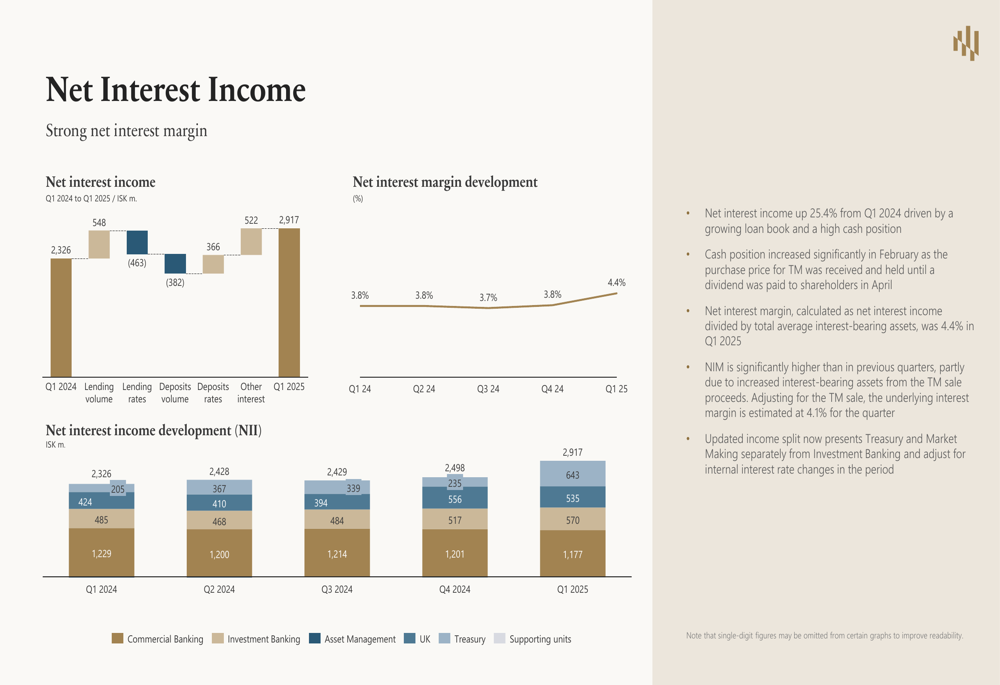

Kvika’s income statement revealed several notable trends. Net interest income increased significantly year-over-year, driven by a growing loan book and high cash position. The following chart illustrates this growth and its drivers:

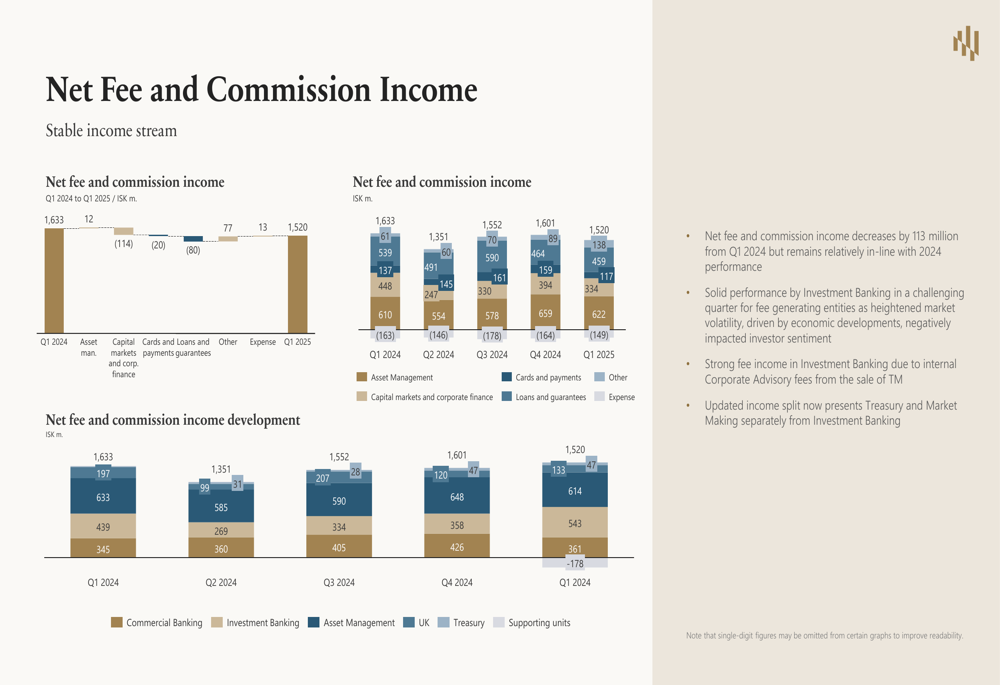

Net fee and commission income decreased slightly compared to Q1 2024 but remained in line with recent quarterly performance. The decline was primarily seen in asset management fees, likely due to market volatility:

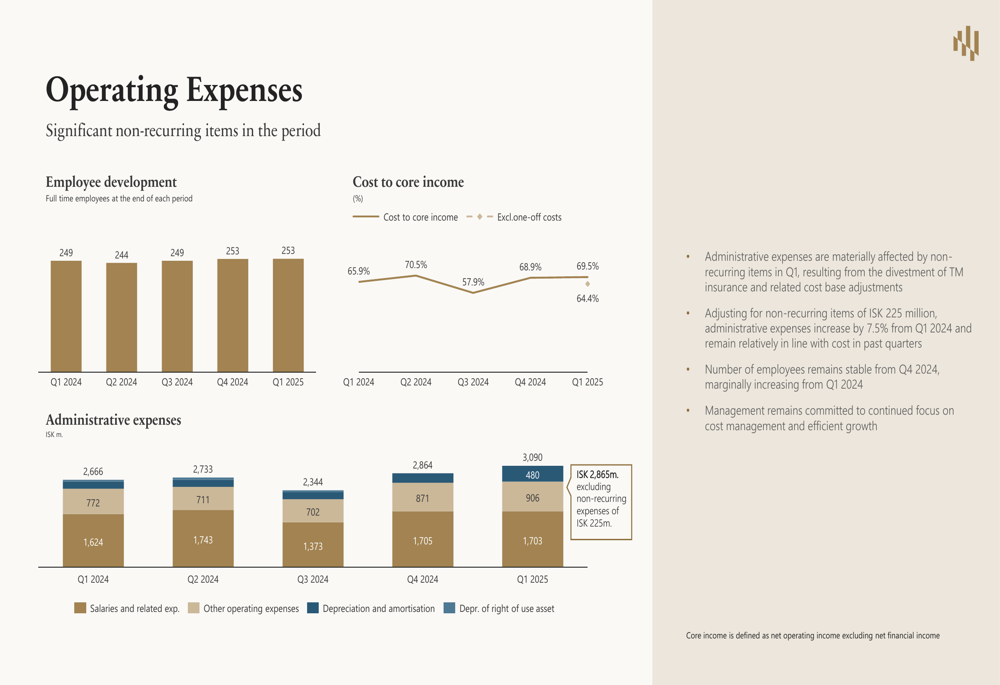

Administrative expenses were materially affected by non-recurring items in Q1, resulting from the divestment of TM Insurance and related cost base adjustments. Adjusting for these non-recurring items of ISK 225 million, administrative expenses increased by 7.5% from Q1 2024:

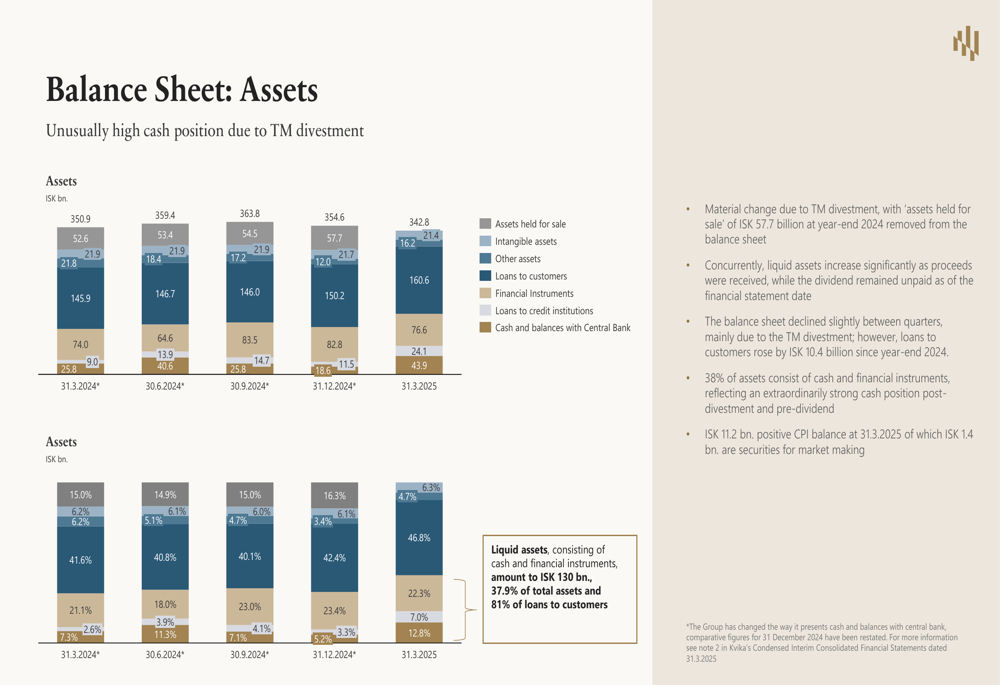

The bank’s balance sheet showed changes reflecting the TM divestment, with assets held for sale decreasing significantly. Loans to customers continued to grow, with particular strength in unsecured loans, real estate, and investment loans:

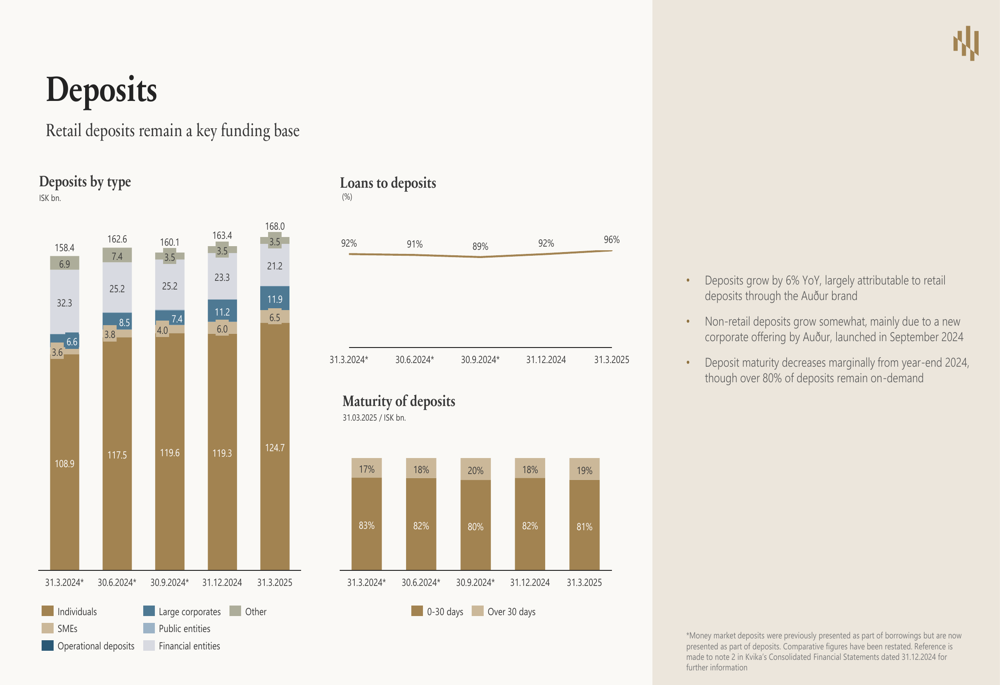

On the liability side, deposits grew by 6% year-over-year, largely attributable to retail deposits through the Auður brand. The loan-to-deposit ratio remained stable at 0.8x:

Strategic Initiatives

A central focus of Kvika’s Q1 presentation was the expedited acquisition of the remaining 19.7% stake in Ortus Secured Finance, completed in March 2025. This acquisition is part of a broader UK consolidation strategy that includes merging Kvika Limited and Ortus, moving the bulk of the UK loan book to Kvika in Iceland, and refinancing it via a European bond offering.

The bank highlighted the success of the Ortus acquisition, noting that the total purchase price from 2018-2025 amounted to GBP 34.7 million (including a potential maximum earnout of GBP 1.6 million). For context, Ortus reported profit before tax of GBP 8.0 million in 2024 and had a book value of equity of GBP 27.8 million as of December 31, 2024.

Management emphasized that the accelerated acquisition brought forward the revaluation expense of ISK 580 million in Q1, which significantly impacted reported results but positions the bank for stronger future performance through its consolidated UK operations.

Forward-Looking Statements

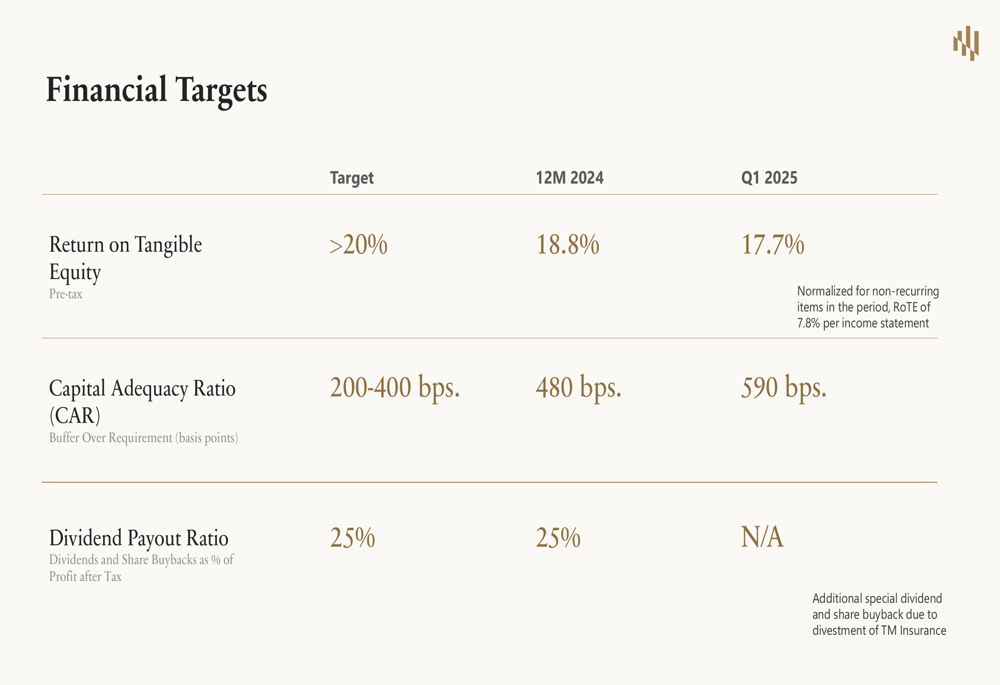

Kvika reaffirmed its financial targets in the presentation, showing progress against its goals for return on tangible equity, capital adequacy ratio, and dividend payout ratio:

The bank described itself as being in an "enviable position after strategic milestones," highlighting its strong capital base, earnings stability, growing net interest income, and improved infrastructure following the strategic developments in Q1.

Management expressed confidence that the non-recurring expenses incurred during the quarter would lead to a reduced cost base going forward, as TM no longer contributes to shared costs, and the UK consolidation is expected to create operational efficiencies.

Looking ahead, Kvika appears well-positioned to benefit from its strategic repositioning, with strong capital and liquidity ratios providing flexibility for future growth. The bank’s normalized performance metrics suggest underlying strength despite the temporary impact of strategic developments on reported figures.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.