S&P 500 slips, but losses kept in check as Nvidia climbs ahead of results

Introduction & Market Context

Kymera Therapeutics (NASDAQ:KYMR) presented its second quarter 2025 financial results on August 11, 2025, highlighting progress across its immunology pipeline despite a significant revenue decline. The company’s stock fell 5.64% in premarket trading to $38.33, reflecting investor concerns about widening losses despite the company’s strong cash position and clinical advancements.

Kymera is positioning itself in the large immunology market, which includes approximately 160 million patients across key diseases. The company noted that only about 5 million patients (3% of those diagnosed) currently receive systemic advanced therapies, representing a significant opportunity for growth.

As shown in the following strategic vision slide, Kymera aims to reinvent disease treatment through its protein degradation platform:

Quarterly Performance Highlights

Kymera reported Q2 2025 revenue of $11.5 million, a significant decrease from $25.7 million in the same period last year. The company’s net loss widened to $76.6 million compared to $42.1 million in Q2 2024, primarily due to increased research and development expenses, which rose to $78.4 million from $59.2 million year-over-year.

Despite the widening losses, Kymera maintained a strong financial position with $963.1 million in cash, cash equivalents, and marketable securities as of June 30, 2025, up from $850.9 million at the end of 2024. This cash runway extends into the second half of 2028, providing substantial resources for the company’s ambitious development plans.

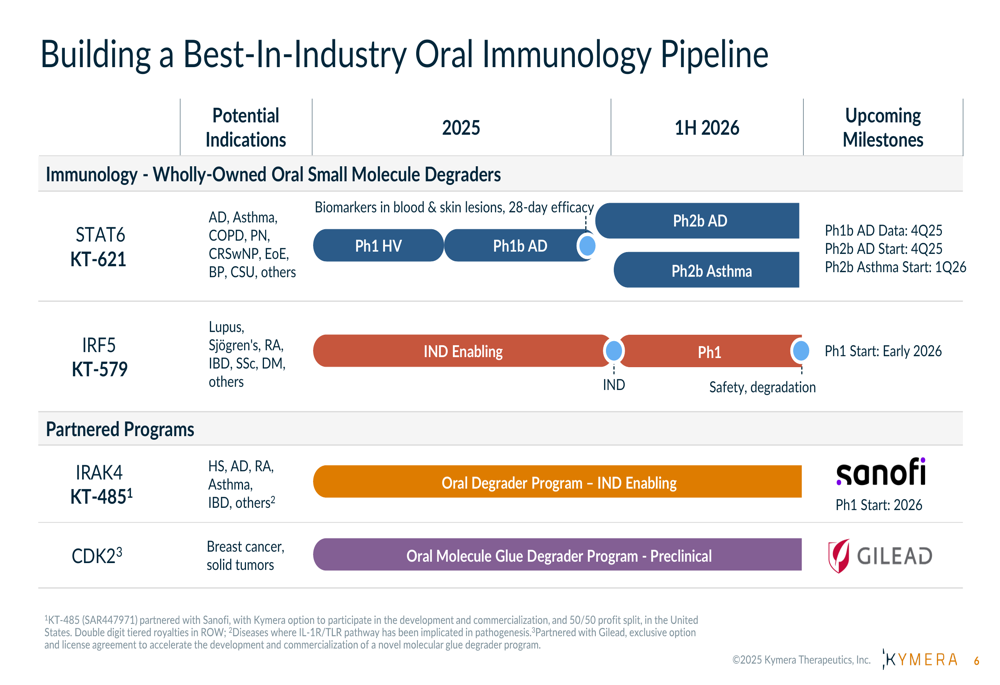

The company’s pipeline has expanded significantly, as illustrated in this comprehensive overview of their immunology programs:

Pipeline Progress

Kymera’s lead asset, KT-621, a STAT6 degrader for atopic dermatitis and other Th2-driven diseases, showed promising results in Phase 1 healthy volunteer studies. The company reported complete STAT6 degradation in both blood and skin, with robust inhibition of biomarkers comparable or superior to published dupilumab data.

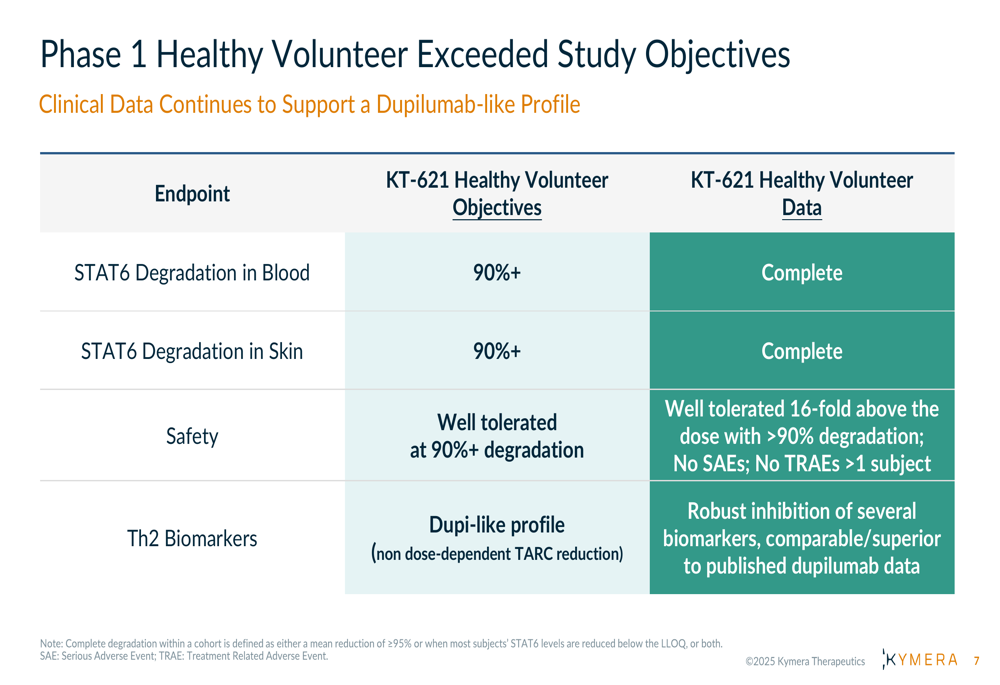

The following slide demonstrates how KT-621 achieved the study objectives with a favorable safety profile:

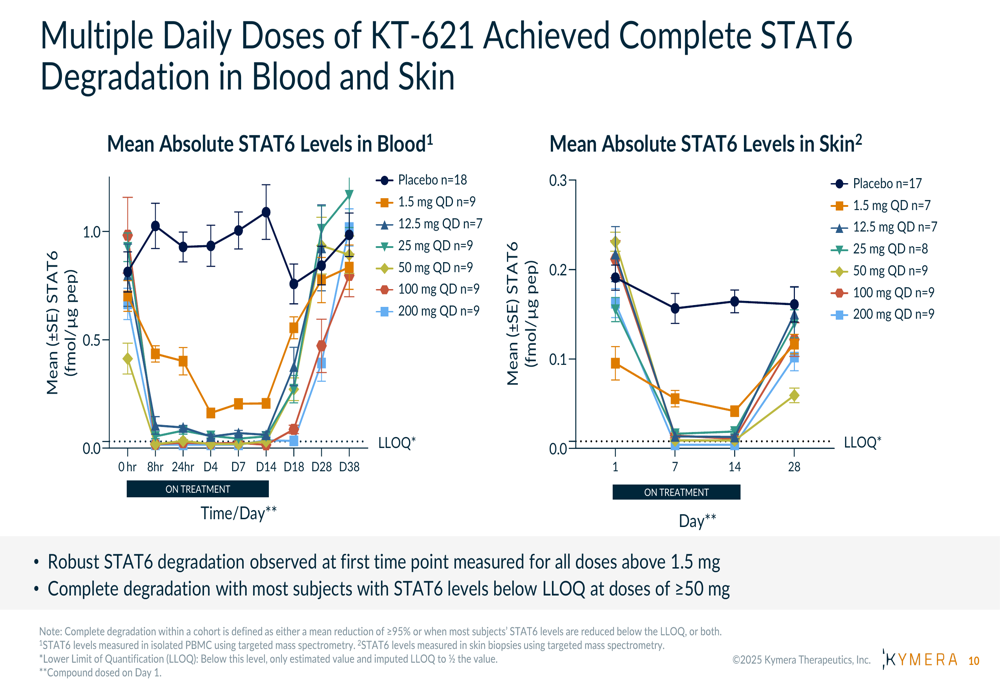

Multiple daily doses of KT-621 achieved complete STAT6 degradation in both blood and skin across various dose levels, as shown in the following data:

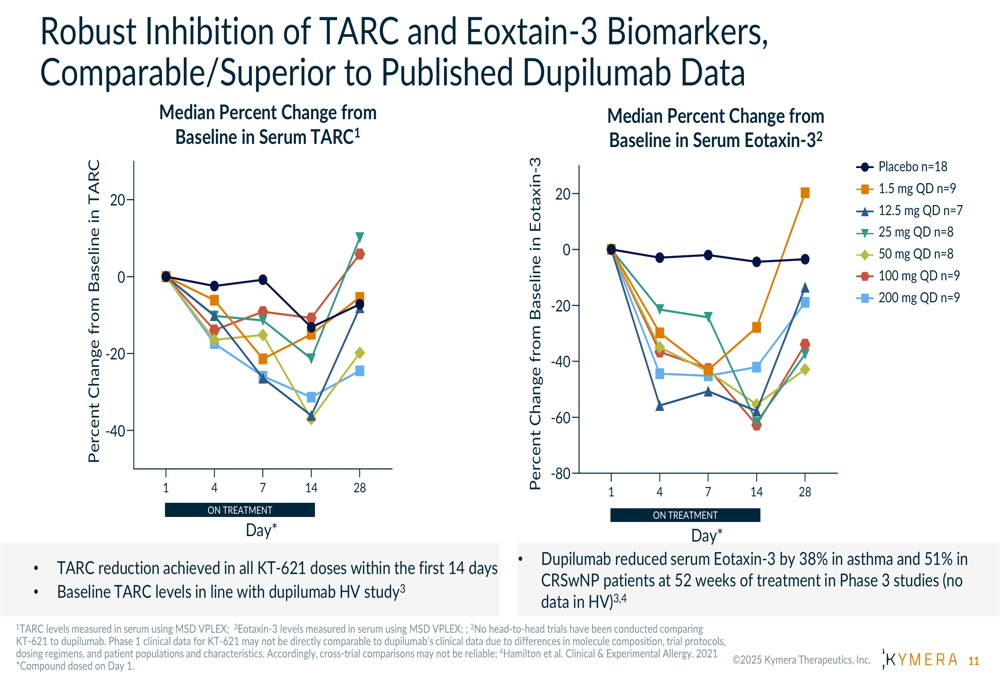

Particularly encouraging was KT-621’s effect on key biomarkers TARC and Eotaxin-3, which showed reductions comparable or superior to published dupilumab data, suggesting potential for similar efficacy with the convenience of oral administration:

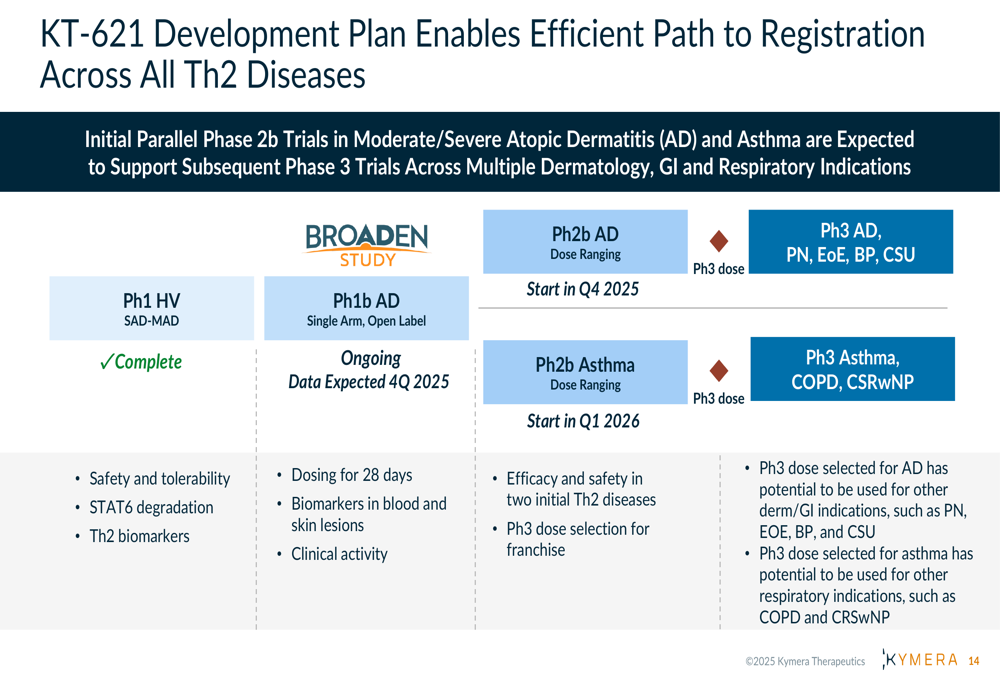

Based on these positive results, Kymera is advancing KT-621 into a Phase 1b trial in atopic dermatitis patients, with data expected in Q4 2025. The company has outlined an efficient development plan aimed at supporting registration across multiple Th2-driven diseases:

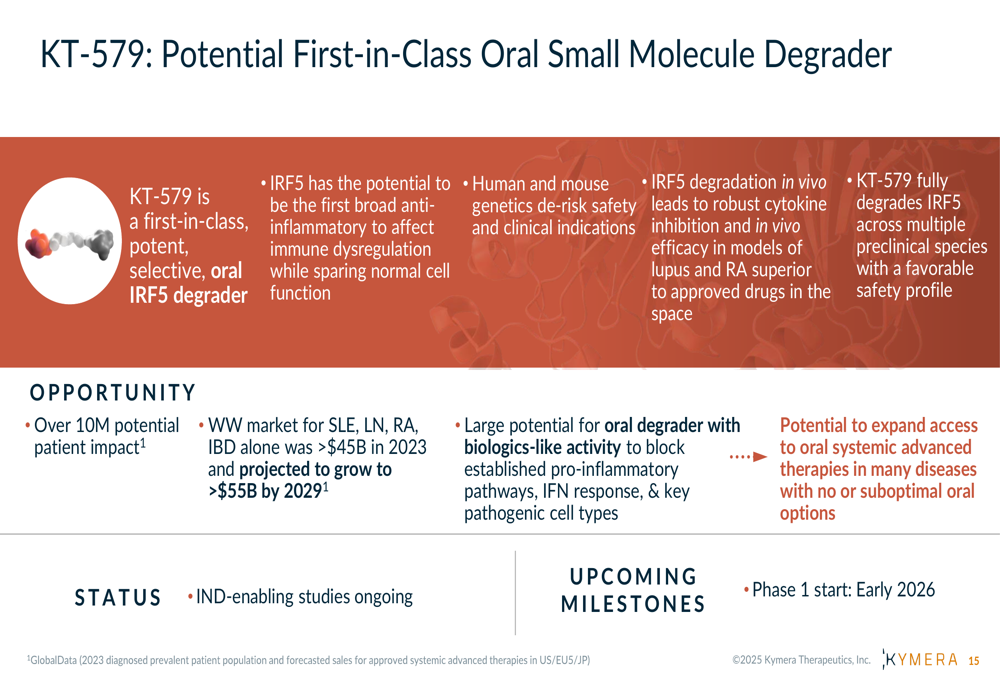

Additionally, Kymera is advancing KT-579, a potential first-in-class oral IRF5 degrader for lupus and other autoimmune conditions. IND-enabling studies are ongoing with Phase 1 start planned for early 2026:

Strategic Positioning

Kymera is strategically targeting the immunology market, where current therapies generate over $100 billion in annual sales. The company noted that approximately two-thirds of these therapies are injectable biologics, presenting an opportunity for oral alternatives like KT-621 and KT-579.

According to industry surveys cited by Kymera, 75% of patients would switch from injectable biologics to oral therapies with similar efficacy profiles. This patient preference, combined with the large untapped market of patients not currently on systemic therapies, represents a significant commercial opportunity.

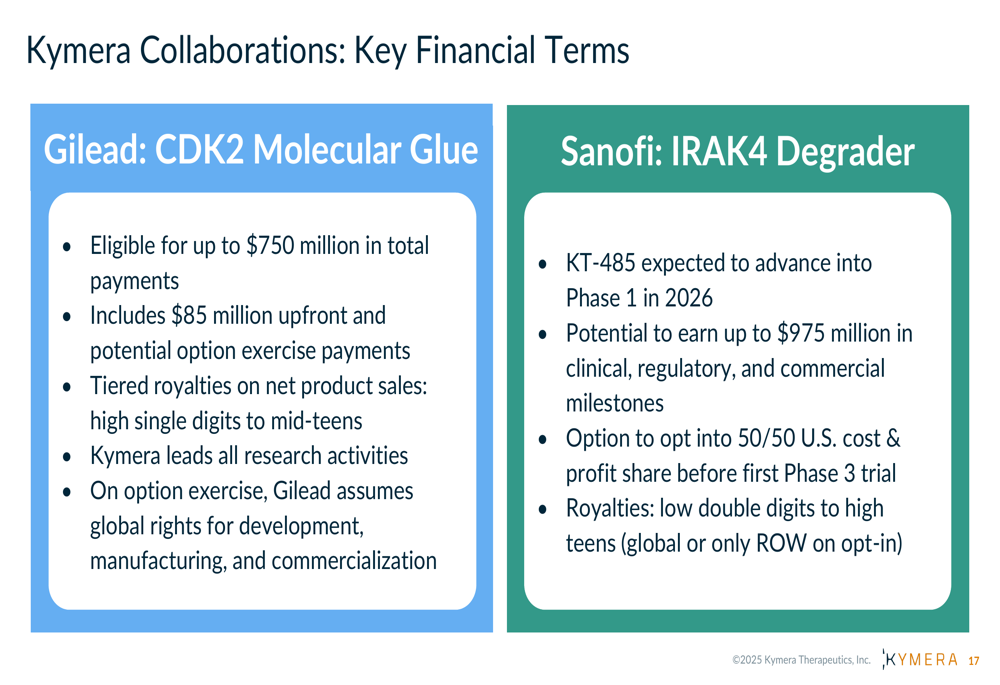

The company has also secured valuable partnerships with major pharmaceutical companies. Kymera’s collaboration with Gilead (NASDAQ:GILD) on CDK2 molecular glue degraders could yield up to $750 million in total payments, while its partnership with Sanofi (NASDAQ:SNY) on IRAK4 degraders has potential for up to $975 million in milestones:

Financial Analysis

Kymera’s Q2 2025 financial results revealed several key trends. Collaboration revenue decreased to $11.5 million for the three months ended June 30, 2025, compared to $25.7 million in the same period of 2024. For the first half of 2025, revenue was $33.6 million, down slightly from $35.9 million in the first half of 2024.

Research and development expenses increased significantly to $78.4 million in Q2 2025 from $59.2 million in Q2 2024, reflecting the company’s expanded clinical activities and pipeline advancement. General and administrative expenses remained relatively stable at $17.6 million compared to $17.4 million in the prior year period.

The company’s net loss widened to $76.6 million in Q2 2025 from $42.1 million in Q2 2024. For the first half of 2025, the net loss was $142.2 million compared to $90.6 million in the first half of 2024.

Despite these increased losses, Kymera’s cash position strengthened to $963.1 million as of June 30, 2025, compared to $850.9 million at the end of 2024. This increase suggests a significant cash infusion during the quarter, potentially from partnership activities or financing.

Forward-Looking Statements

Kymera outlined several key upcoming milestones that could serve as catalysts for the company. For KT-621, data from the Phase 1b trial in atopic dermatitis is expected in Q4 2025, with plans to initiate Phase 2b studies in atopic dermatitis in Q4 2025 and in asthma in Q1 2026.

For KT-579, the company is conducting IND-enabling studies with plans to enter Phase 1 clinical trials in early 2026. Additionally, Kymera’s partnered IRAK4 degrader program with Sanofi (KT-485) is expected to enter Phase 1 trials in 2026.

The company remains on track to deliver a total of 10 investigational degrader drugs into the clinic by 2026, having already delivered 5 since 2020. This ambitious pipeline expansion, coupled with the company’s strong cash position, positions Kymera to potentially capture significant market share in the immunology space if its clinical programs continue to demonstrate positive results.

However, investors will be closely watching the company’s burn rate and clinical progress, as the widening losses and revenue decline in Q2 2025 have raised some concerns despite the promising clinical data and strategic positioning.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.