Bitcoin price today: dips below $112k, near 6-wk low despite Fed cut bets

Introduction & Market Context

L3Harris Technologies (NYSE:LHX) presented its first quarter 2025 earnings on April 24, revealing quarterly revenue of $5.1 billion and non-GAAP diluted earnings per share of $2.41. The defense contractor updated its full-year guidance downward following recent portfolio adjustments, including the divestiture of its Commercial Aviation Solutions business.

The presentation comes as L3Harris shares trade near the lower end of their 52-week range of $193.09 to $265.74. The stock was down 1.53% in premarket trading to $213, continuing a pattern seen after the company’s Q4 2024 results when shares declined despite beating earnings expectations.

Quarterly Performance Highlights

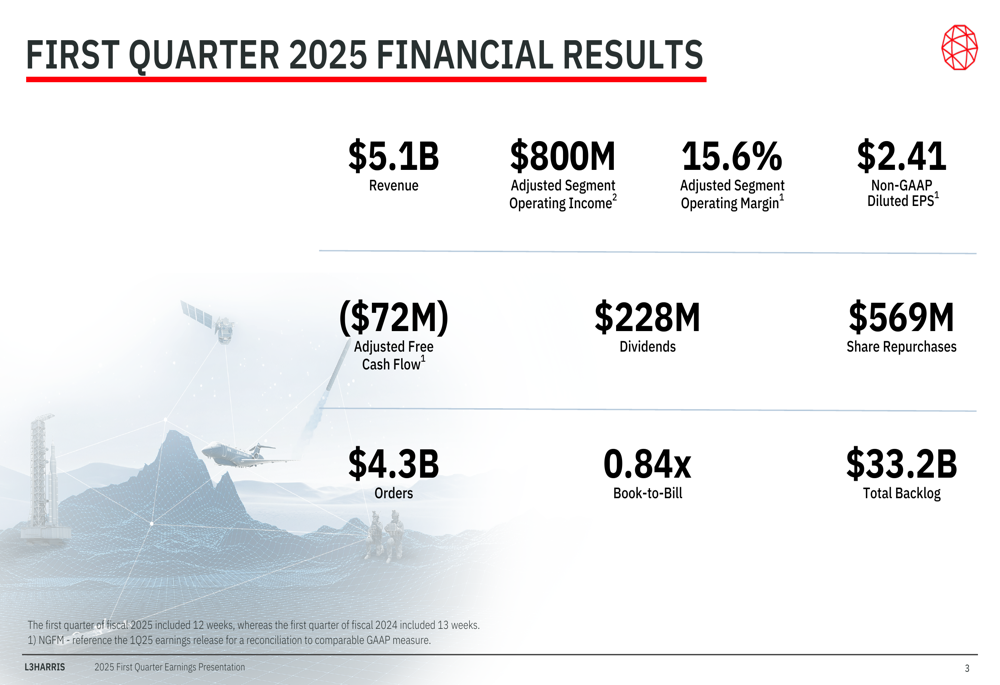

L3Harris reported mixed results for the first quarter of fiscal 2025, which included 12 weeks compared to 13 weeks in the first quarter of 2024. The company achieved $5.1 billion in revenue with adjusted segment operating income of $800 million, translating to an operating margin of 15.6%.

As shown in the following comprehensive financial overview:

The company’s cash position showed negative adjusted free cash flow of $72 million for the quarter. Despite this, L3Harris maintained its shareholder return initiatives with $228 million in dividends and $569 million in share repurchases. The book-to-bill ratio stood at 0.84x, with total backlog reaching $33.2 billion.

Segment Analysis

L3Harris reported varying performance across its four business segments, with Communication Systems emerging as the strongest performer.

The Communication Systems segment posted revenue of $1.35 billion, representing a 4% increase year-over-year, while achieving an impressive operating margin of 25.5% (up 150 basis points). This growth was primarily driven by increased international volume and sales of satellite communications terminal inventory.

Integrated Mission Systems revenue declined 2% to $1.59 billion, though operating margin improved 140 basis points to 12.8%. The company attributed the revenue decrease to lower aircraft missionization volume and a planned ISR mission operations program ramp down.

The Space & Airborne Systems segment faced the most significant challenges, with revenue declining 8% (6% organically) to $1.61 billion and operating margin dropping 140 basis points to 10.9%. The company cited the Antenna Products divestiture and challenges on classified development programs in space as primary factors.

Aerojet Rocketdyne, the company’s newest segment following its acquisition, showed strong revenue growth of 8% (9% organically) to $629 million, though operating margin declined 110 basis points to 12.1% due to lower net favorable EAC (Estimate at Completion) adjustments.

Updated 2025 Guidance

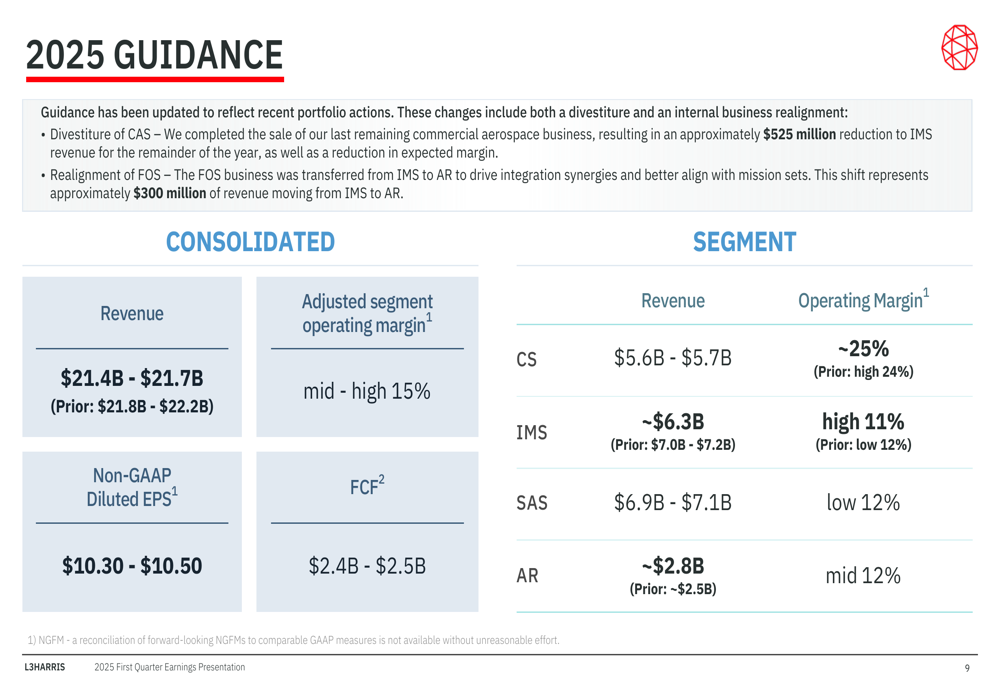

L3Harris revised its full-year 2025 guidance, primarily reflecting recent portfolio actions including the divestiture of Commercial Aviation Solutions (CAS) and the realignment of Flight Operations Services (FOS). The updated outlook is illustrated in the following guidance summary:

Revenue guidance was lowered to $21.4-21.7 billion from the previous $21.8-22.2 billion, with the CAS divestiture reducing IMS revenue by $525 million and the FOS realignment transferring $300 million from IMS to Aerojet Rocketdyne.

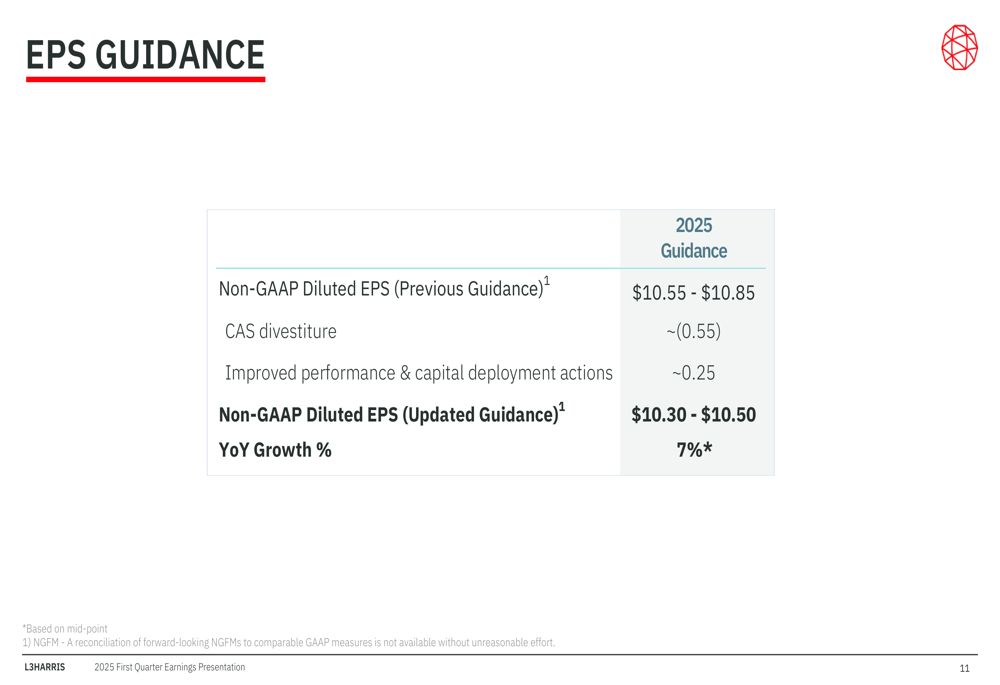

The company also adjusted its EPS guidance as detailed in this breakdown:

Non-GAAP diluted EPS guidance was reduced to $10.30-10.50 from the previous $10.55-10.85, with the CAS divestiture accounting for approximately $0.55 of the reduction, partially offset by improved performance and capital deployment actions contributing about $0.25.

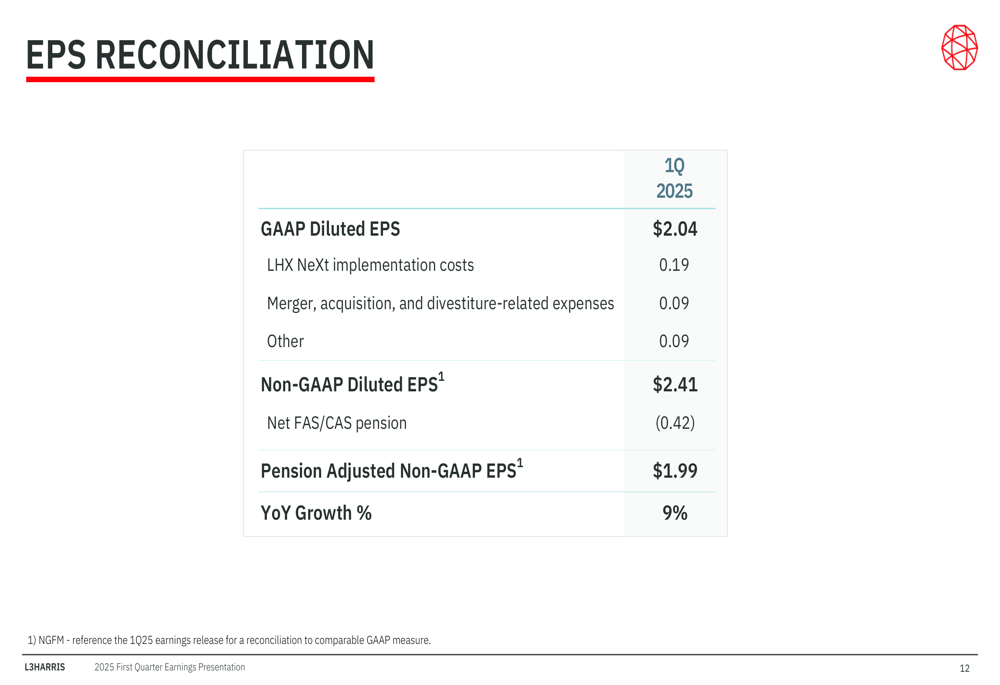

The reconciliation between GAAP and non-GAAP earnings provides further context:

Strategic Initiatives

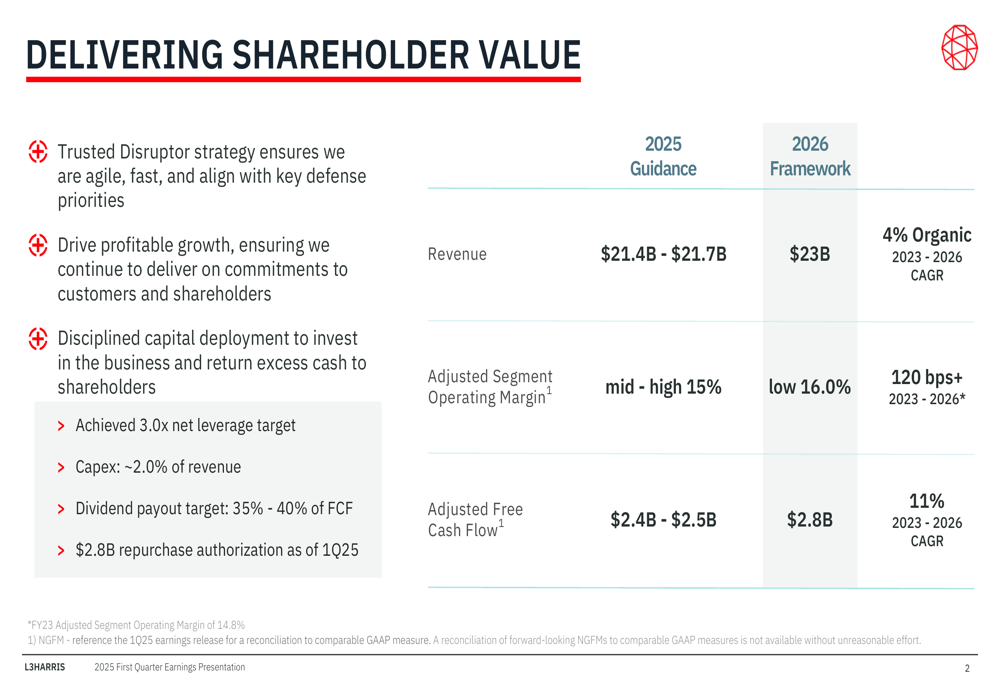

L3Harris continues to execute its "Trusted Disruptor" strategy, focusing on agility, speed, and alignment with key defense priorities. The company’s long-term financial framework targets 4% organic revenue CAGR from 2023-2026 and 11% adjusted free cash flow CAGR over the same period.

The strategic roadmap and financial targets are outlined in this comprehensive framework:

The company highlighted several strategic achievements across its business segments, including a long-term framework agreement with the Dutch Ministry of Defence for communications modernization, delivery of the first missionized Skyraider II aircraft to the U.S. Air Force Special Operations Command, and US Space Force certification of ULA Vulcan with Aerojet Rocketdyne’s RL10 engines.

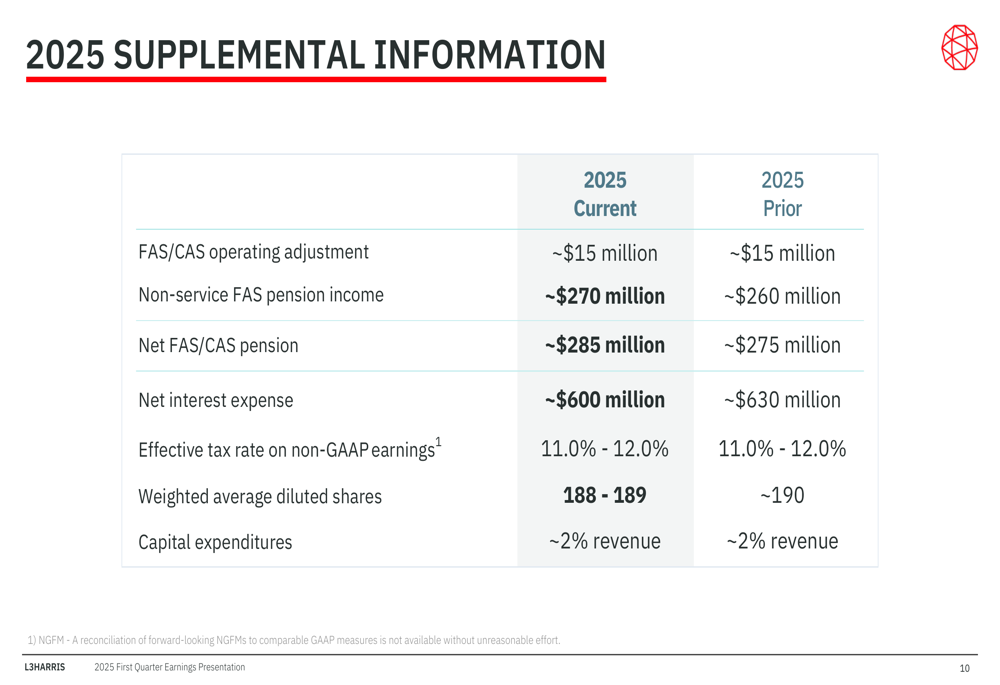

L3Harris also provided additional financial context for 2025, including updates to pension income and interest expense projections:

The company increased its projected non-service FAS pension income to approximately $270 million (from $260 million) and reduced its expected net interest expense to approximately $600 million (from $630 million). Additionally, the weighted average diluted share count was lowered to 188-189 million from approximately 190 million, reflecting ongoing share repurchase activity.

Despite the guidance reduction, L3Harris maintains its capital allocation priorities, including achieving a 3.0x net leverage target, allocating approximately 2.0% of revenue for capital expenditures, and targeting a 35-40% dividend payout as a percentage of free cash flow. The company had $2.8 billion remaining in its share repurchase authorization as of the first quarter.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.