Bank CEOs meet with Trump to discuss Fannie Mae and Freddie Mac - Bloomberg

Introduction & Market Context

L3Harris Technologies Inc (NYSE:LHX) reported first quarter 2025 revenue of $5.1 billion during its earnings presentation on April 24, 2025. The aerospace and defense contractor delivered a non-GAAP diluted EPS of $2.41, showing continued execution of its "Trusted Disruptor" strategy despite a challenging environment. The company’s stock closed at $216.31 on April 23, with premarket trading indicating a decline of 1.53% to $213.00 following the earnings release.

The Q1 results come as L3Harris continues to navigate portfolio adjustments, including the divestiture of its Commercial Aviation Solutions (CAS) business and the realignment of its Flight Operations Solutions (FOS) unit, which have prompted a revision to its full-year guidance.

Quarterly Performance Highlights

L3Harris reported mixed performance across its business segments for the first quarter of 2025, which notably included 12 weeks compared to 13 weeks in the first quarter of 2024.

As shown in the following financial results summary:

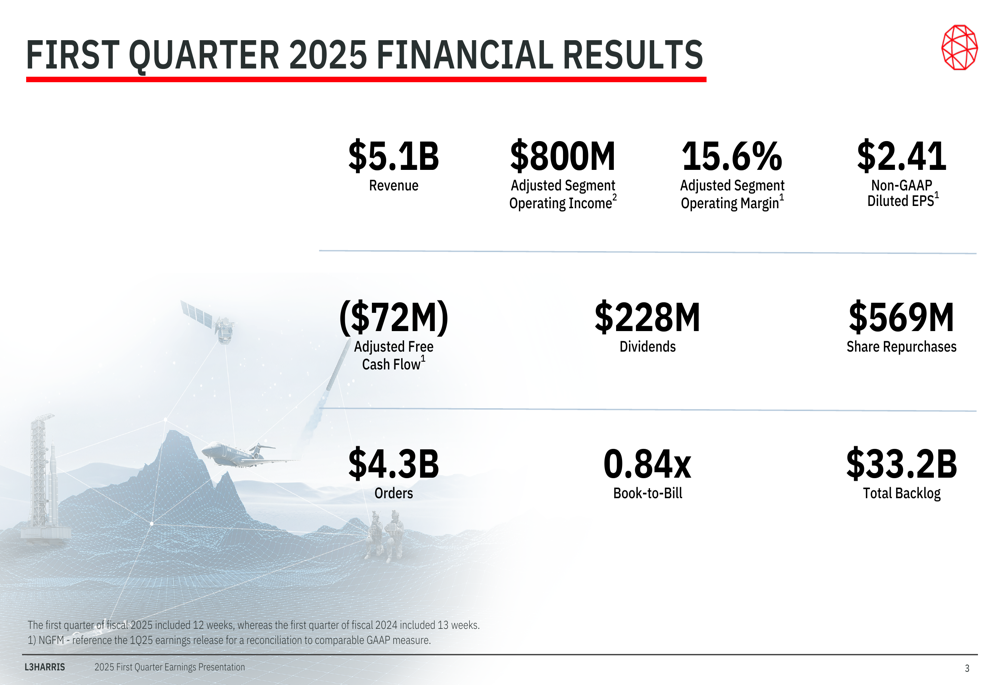

The company generated $5.1 billion in revenue with adjusted segment operating income of $800 million, resulting in an adjusted segment operating margin of 15.6%. While the company returned $797 million to shareholders through dividends ($228 million) and share repurchases ($569 million), it reported negative adjusted free cash flow of $72 million for the quarter. The book-to-bill ratio stood at 0.84x, with total backlog reaching $33.2 billion.

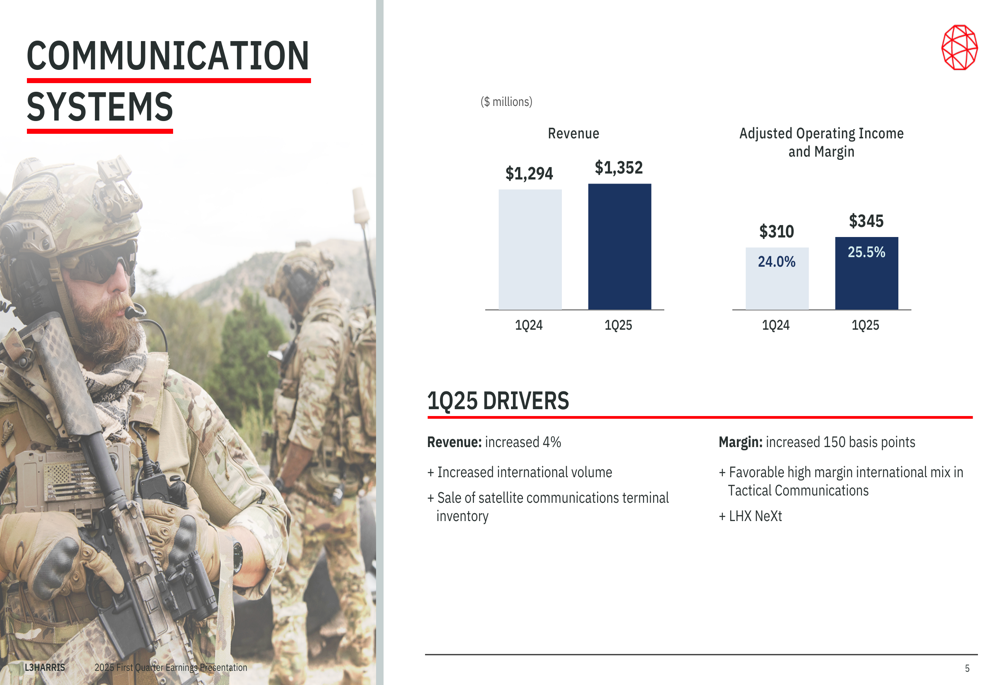

Segment performance varied considerably, with Communication Systems showing the strongest results:

The Communication Systems segment increased revenue to $1,352 million, up from $1,294 million in Q1 2024, while improving its adjusted operating margin to an impressive 25.5%. This growth was driven by increased international volume and sales of satellite communications terminal inventory, with the company’s LHX Next (LON:NXT) initiative contributing to performance improvements.

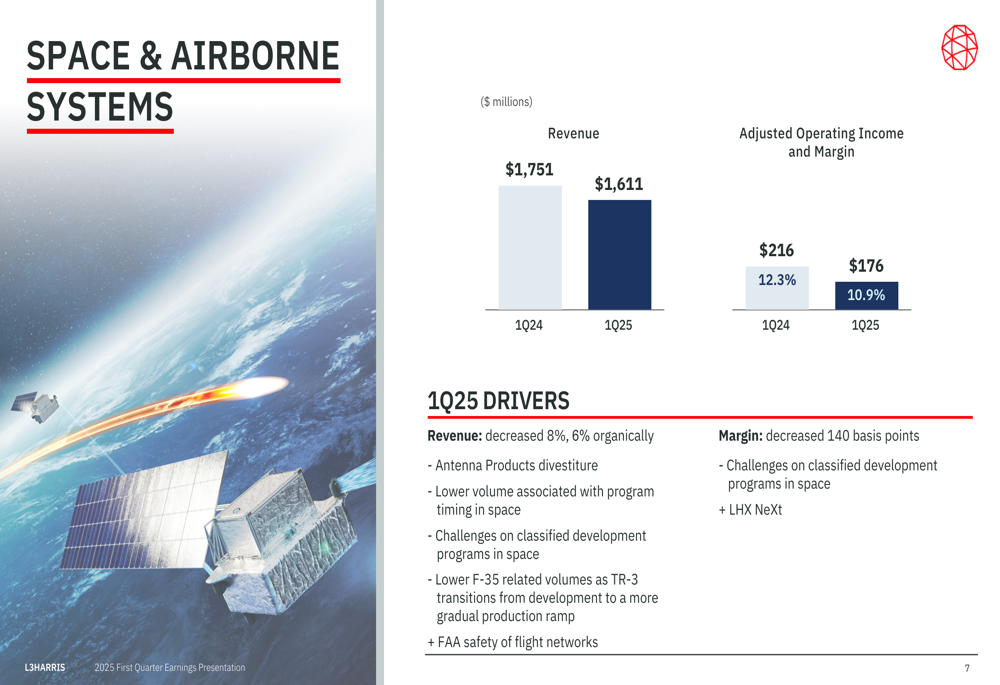

In contrast, the Space & Airborne Systems segment faced challenges:

SAS revenue declined to $1,611 million from $1,751 million in the prior year period, with adjusted operating margin falling to 10.9%. The company attributed this decline to the Antenna Products divestiture, lower volume associated with program timing in space, and challenges on classified development programs.

Detailed Financial Analysis

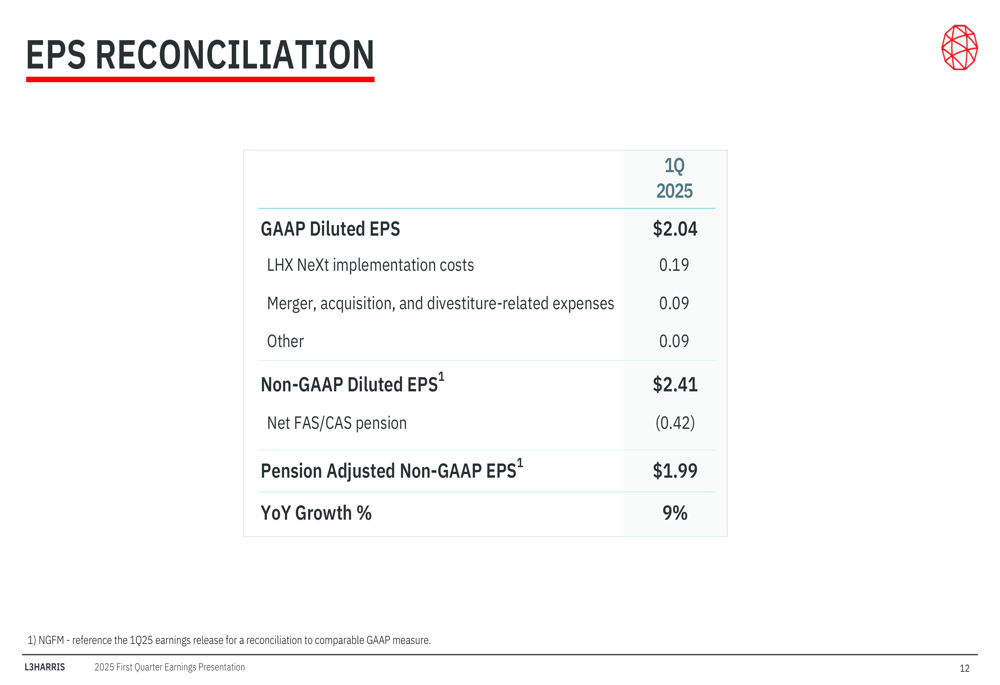

The company’s EPS performance showed improvement year-over-year despite portfolio adjustments. The reconciliation from GAAP to non-GAAP metrics provides insight into the company’s underlying performance:

GAAP diluted EPS of $2.04 was adjusted to $2.41 non-GAAP diluted EPS after accounting for LHX NeXt implementation costs, merger and acquisition-related expenses, and other items. The pension-adjusted non-GAAP EPS of $1.99 represented a 9% year-over-year growth.

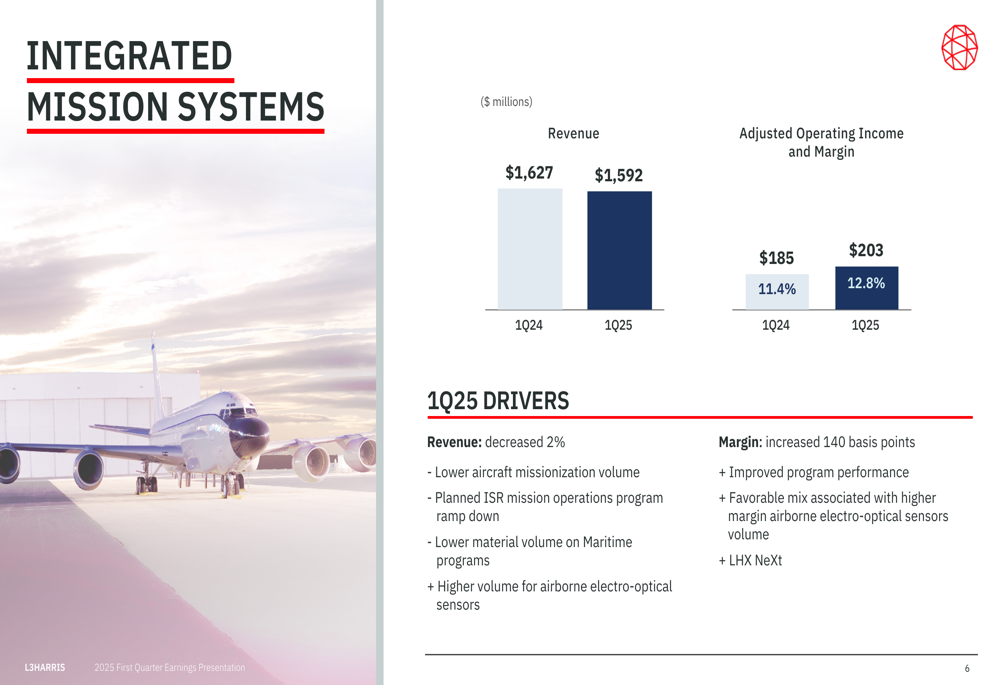

The Integrated Mission Systems segment showed margin improvement despite revenue challenges:

IMS revenue decreased slightly to $1,592 million from $1,627 million in Q1 2024, but adjusted operating margin improved to 12.8% from 11.4%. This segment was impacted by lower aircraft missionization volume and ISR mission operations program ramp down, but benefited from improved program performance and LHX NeXt initiatives.

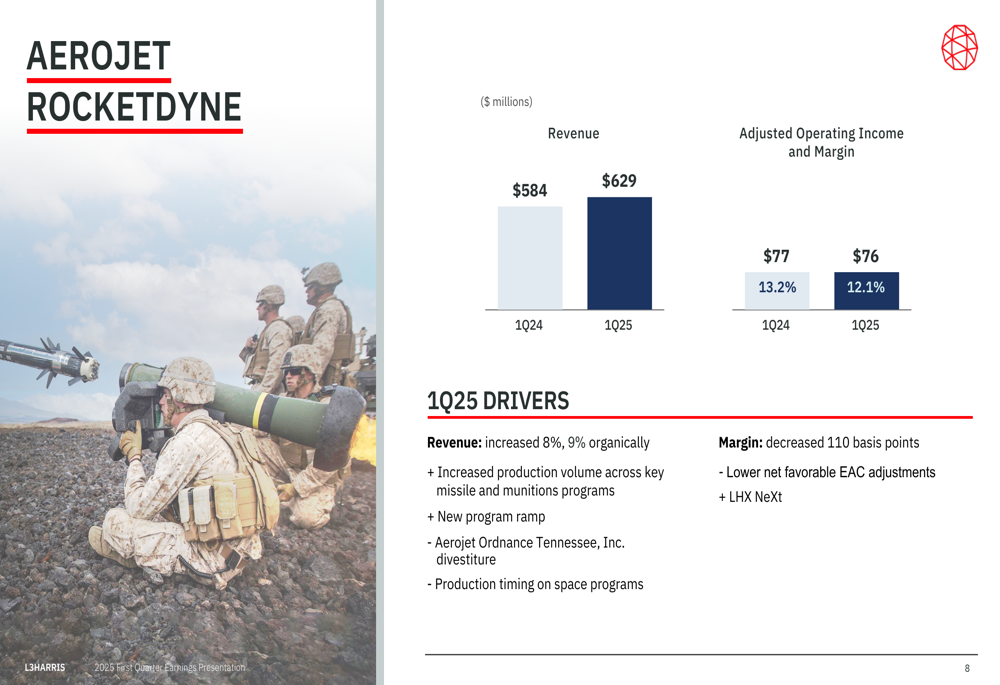

The Aerojet Rocketdyne segment, which L3Harris acquired in 2023, showed revenue growth but margin compression:

AR revenue increased to $629 million from $584 million in Q1 2024, though adjusted operating margin decreased to 12.1% from 13.2%. The growth was driven by increased production volume across key missile and munitions programs and new program ramp-ups.

Forward-Looking Statements

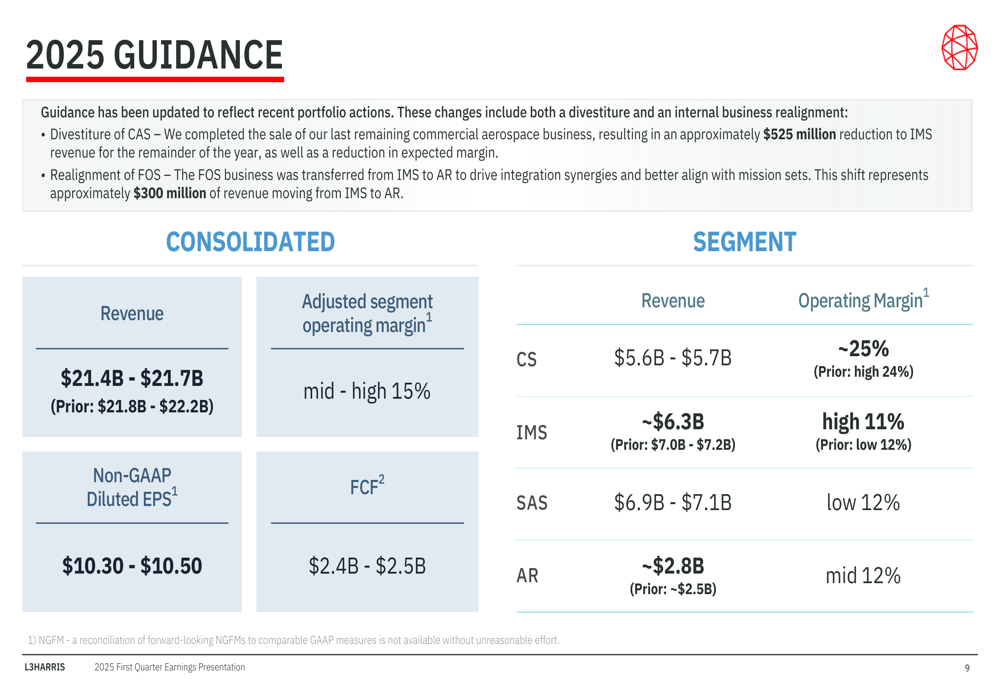

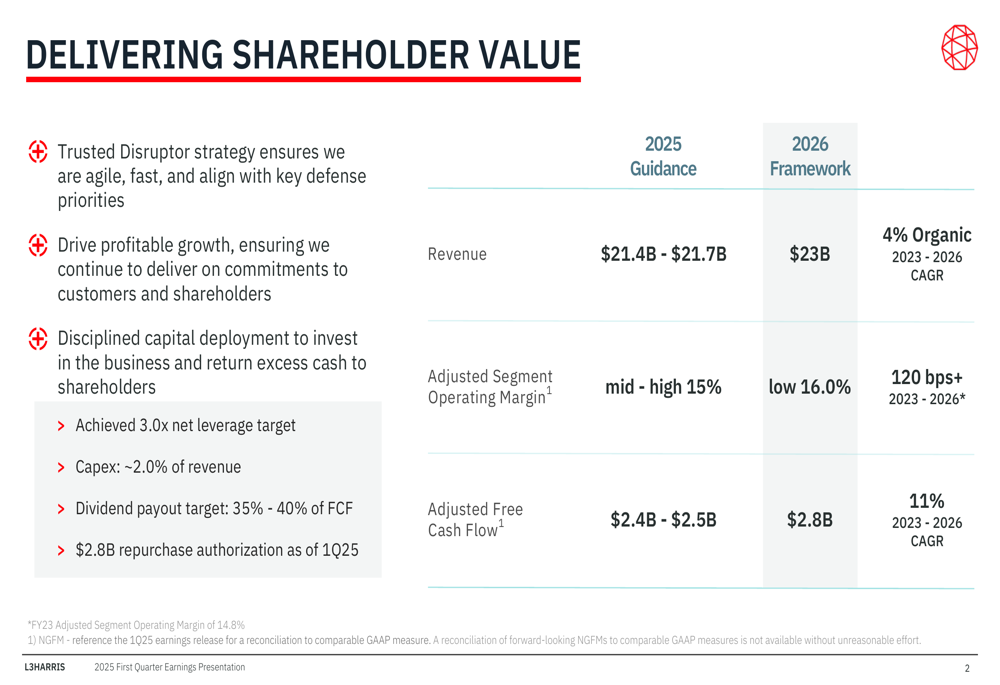

L3Harris revised its 2025 guidance to reflect recent portfolio actions, particularly the divestiture of CAS and realignment of FOS:

The company now projects 2025 revenue of $21.4 billion to $21.7 billion, down from the previous guidance of $21.8 billion to $22.2 billion. The CAS divestiture reduced IMS revenue by approximately $525 million, while the shift of the FOS business from IMS to AR represents approximately $300 million of revenue moving between segments.

Despite these adjustments, L3Harris maintained its adjusted segment operating margin guidance in the mid to high 15% range and adjusted its non-GAAP diluted EPS guidance to $10.30 to $10.50.

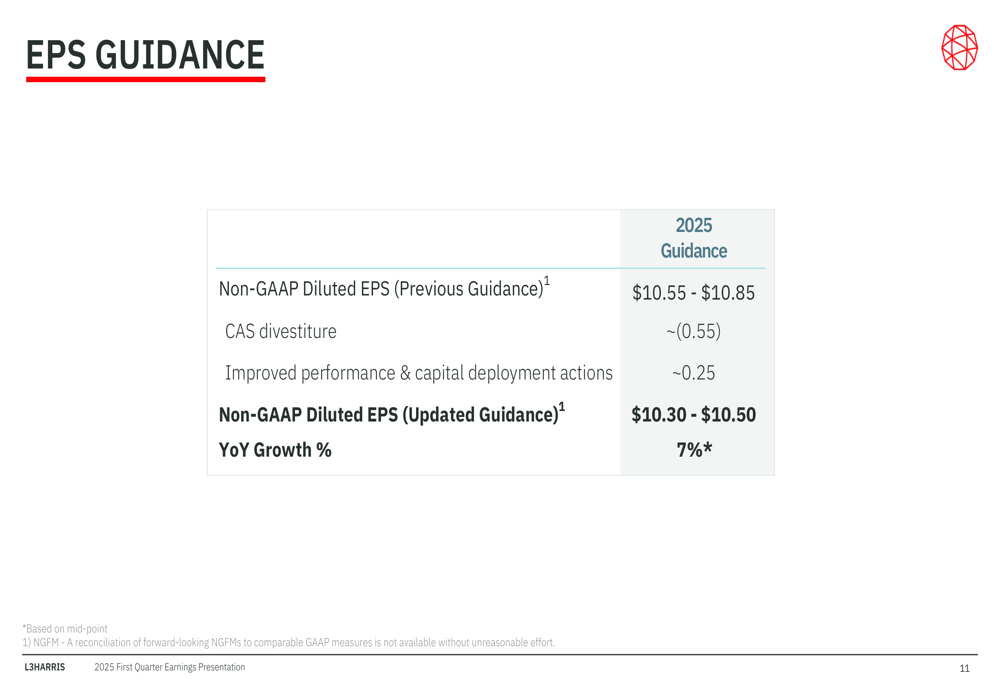

The EPS guidance adjustment reflects the impact of portfolio changes:

The previous EPS guidance of $10.55 to $10.85 was reduced by approximately $0.55 due to the CAS divestiture, partially offset by approximately $0.25 from improved performance and capital deployment actions, resulting in the updated guidance of $10.30 to $10.50, which still represents 7% year-over-year growth.

Strategic Initiatives

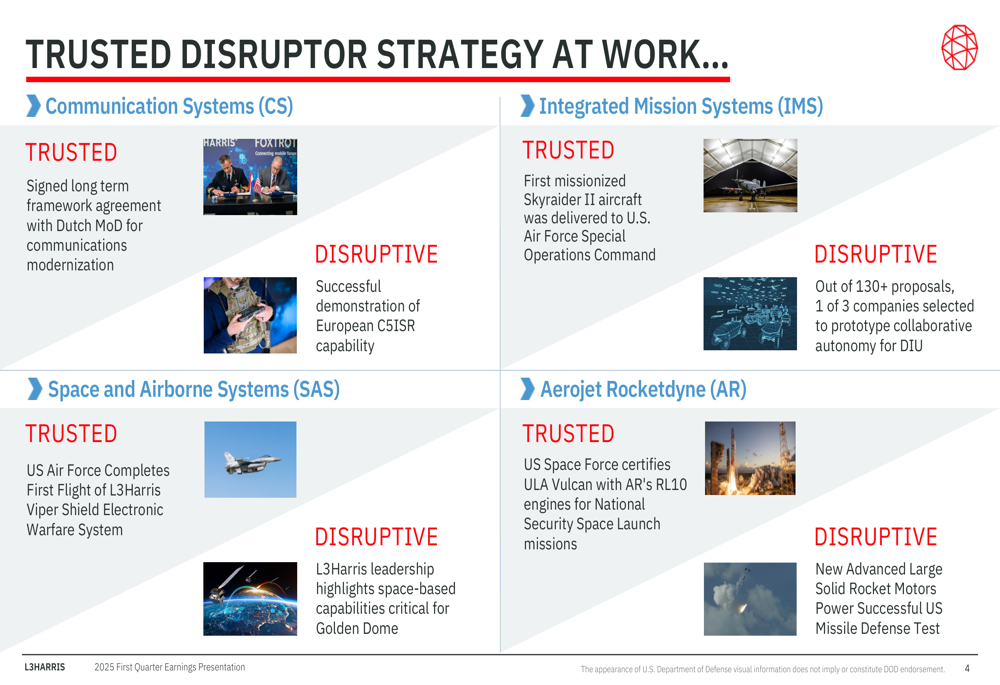

L3Harris continues to execute its "Trusted Disruptor" strategy, focusing on agility, speed, and alignment with key defense priorities:

The company’s strategic framework aims to drive profitable growth while maintaining disciplined capital deployment. L3Harris is targeting a 4% organic revenue CAGR from 2023 to 2026, with adjusted segment operating margin expansion of 120+ basis points over the same period. The 2026 framework projects revenue of $23 billion with adjusted segment operating margin in the low 16% range and adjusted free cash flow of $2.8 billion.

The company highlighted several examples of its strategy in action across business segments:

Key achievements included signing a long-term framework agreement with the Dutch Ministry of Defense for communications modernization, delivering the first missionized Skyraider II aircraft to U.S. Air Force Special Operations Command, completing the first flight of the Viper Shield Electronic Warfare System, and receiving U.S. Space Force certification for ULA Vulcan with AR’s RL10 engines for National Security Space Launch missions.

L3Harris remains committed to shareholder returns through its capital allocation strategy, targeting a 3.0x net leverage ratio, capital expenditures of approximately 2% of revenue, and a dividend payout of 35-40% of free cash flow. The company had a $2.8 billion share repurchase authorization as of Q1 2025, demonstrating its continued focus on returning value to shareholders despite the negative free cash flow in the quarter.

As L3Harris navigates its portfolio transformation and executes its strategic initiatives, investors will be watching closely to see if the company can deliver on its revised 2025 guidance and longer-term financial targets while maintaining its position as a key player in the aerospace and defense industry.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.