Oracle stock falls after report reveals thin margins in AI cloud business

Introduction & Market Context

Lantheus Holdings Inc (NASDAQ:LNTH) presented its first quarter 2025 results on May 7, revealing modest revenue growth amid a strategic transformation focused on acquisitions and pipeline expansion. The radiopharmaceutical company reported that its stock was trading down in premarket activity, with fundamentals data showing a 7.48% decline to $97.00 before market open.

The company’s presentation comes at a pivotal moment as Lantheus works to position itself as a leader in next-generation radiopharmaceuticals through strategic acquisitions while navigating near-term financial challenges.

Quarterly Performance Highlights

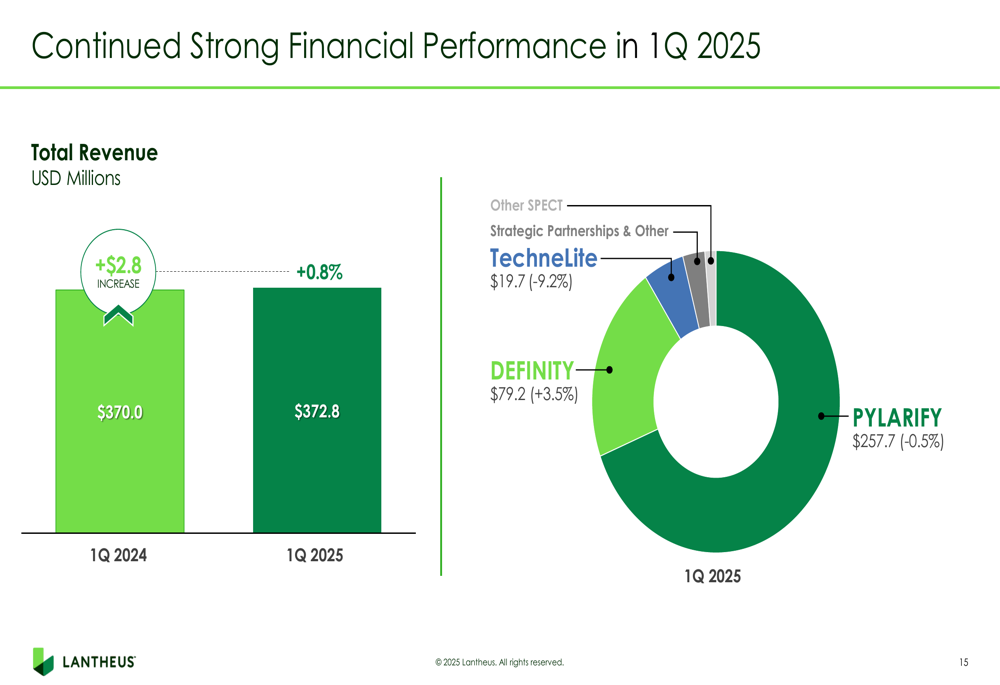

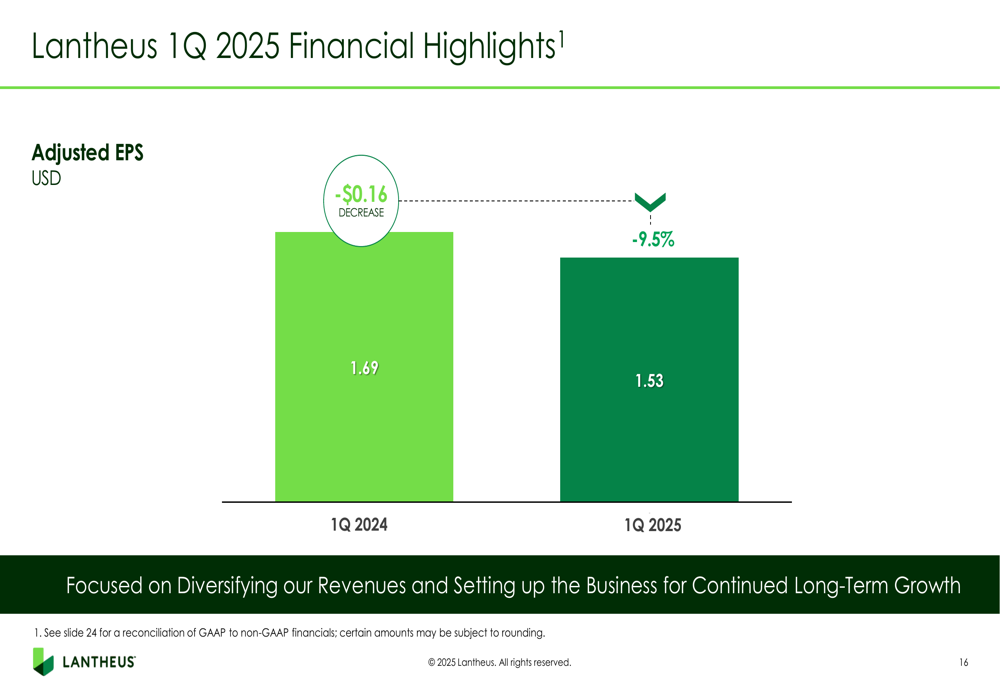

Lantheus reported total revenue of $372.8 million for Q1 2025, representing a modest 0.8% increase compared to $370.0 million in Q1 2024. However, adjusted earnings per share (EPS) declined 9.5% year-over-year to $1.53 from $1.69 in the same period last year.

As shown in the following financial performance overview:

The revenue breakdown reveals that PYLARIFY, the company’s leading PSMA PET imaging agent, generated $257.7 million in net sales, a slight decrease of 0.5% compared to Q1 2024. DEFINITY, the company’s ultrasound enhancing agent, contributed $79.2 million, growing 3.5% year-over-year. TechneLite sales declined 9.2% to $19.7 million.

The company’s adjusted EPS performance illustrates the pressure on profitability:

Lantheus emphasized that it is focused on diversifying revenues and setting up the business for continued long-term growth, despite the near-term earnings pressure.

Strategic Initiatives & Acquisitions

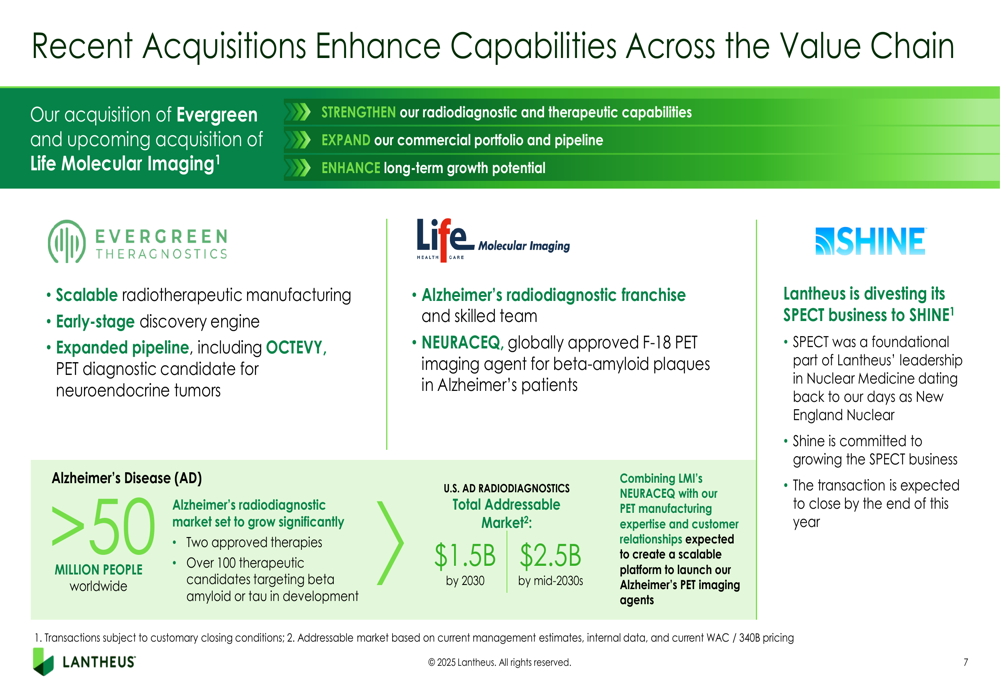

A significant portion of the presentation highlighted Lantheus’ strategic acquisitions aimed at enhancing its capabilities across the radiopharmaceutical value chain. The company closed its acquisition of Evergreen Theragnostics in April 2025 and expects to complete the acquisition of Life Molecular Imaging in Q2 2025, while planning to divest its SPECT business by year-end.

The following slide illustrates how these acquisitions enhance Lantheus’ capabilities:

The acquisition of Life Molecular Imaging brings an Alzheimer’s radiodiagnostic franchise including NEURACEQ, positioning Lantheus in a market expected to reach $1.5 billion by 2030 and $2.5 billion by the mid-2030s. Meanwhile, Evergreen Theragnostics provides scalable radiotherapeutic manufacturing capabilities and an early-stage discovery engine.

Product Performance

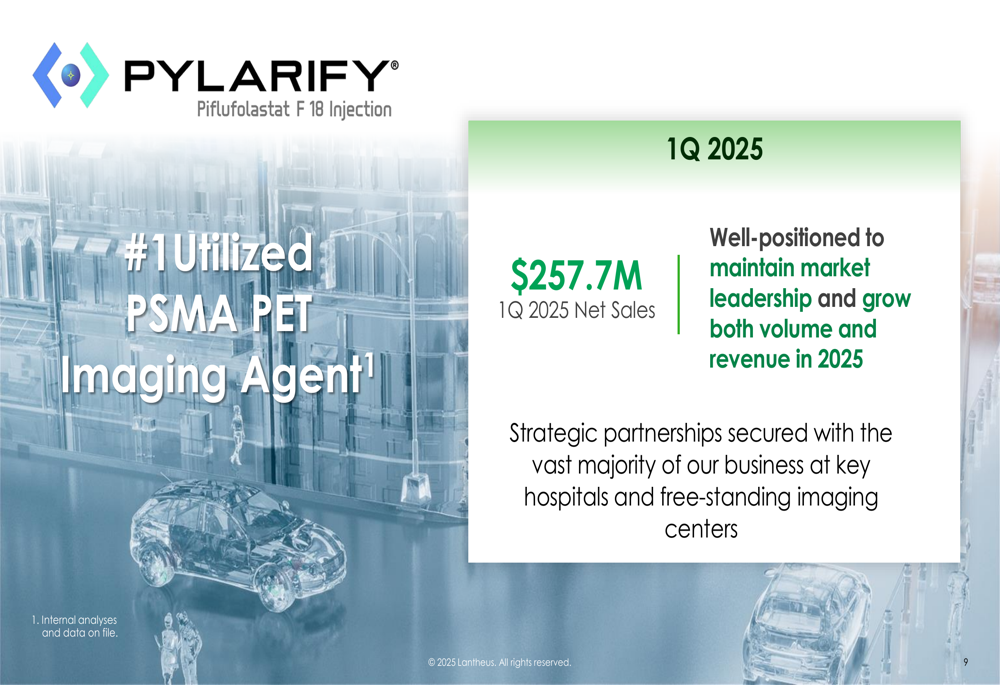

Despite competitive pressures, Lantheus maintained market leadership with its key products. PYLARIFY continues to be the #1 utilized PSMA PET imaging agent in the market:

The company indicated it is well-positioned to maintain market leadership and grow both volume and revenue in 2025 through strategic partnerships at key hospitals and free-standing imaging centers.

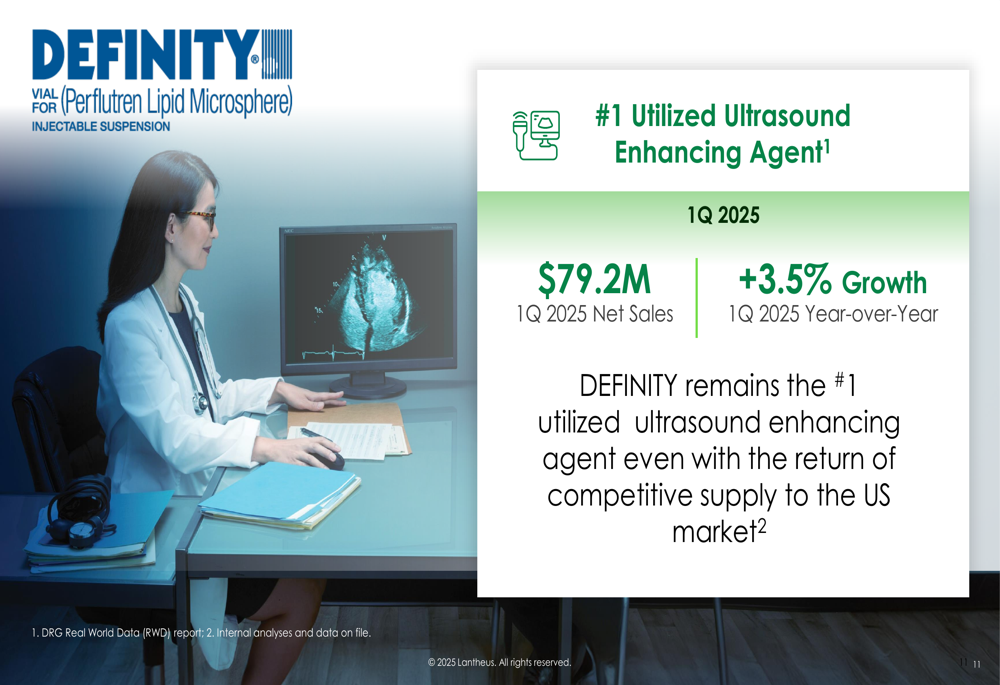

Similarly, DEFINITY maintained its position as the leading ultrasound enhancing agent:

Notably, DEFINITY achieved 3.5% growth year-over-year despite the return of competitive supply to the US market, demonstrating the product’s strong market position.

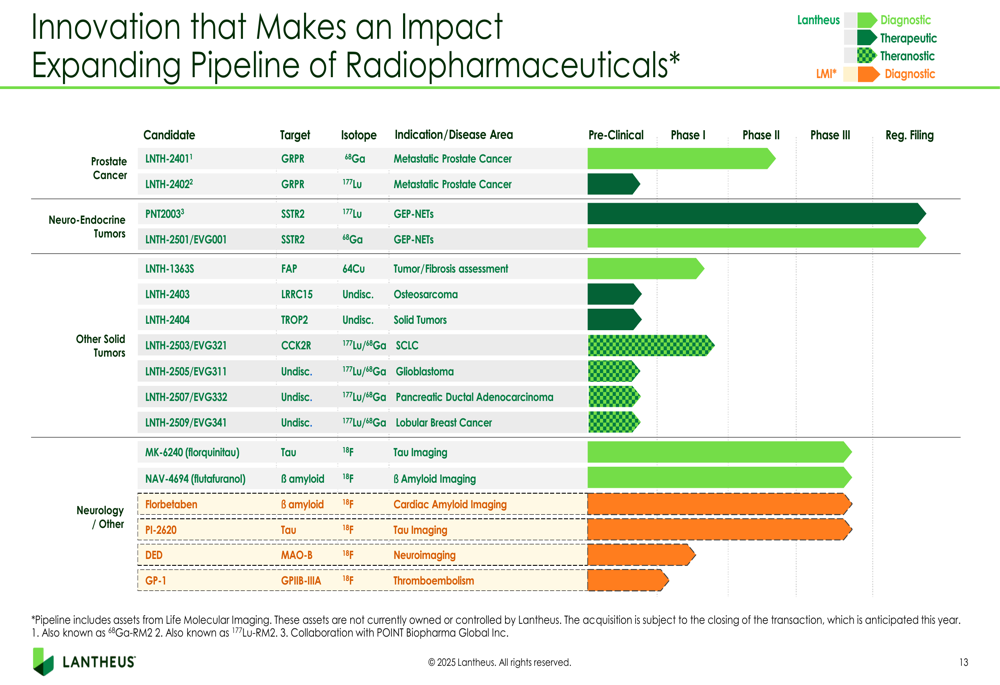

Pipeline & Future Growth

Lantheus presented an expanding pipeline of radiopharmaceuticals spanning multiple therapeutic areas, including prostate cancer, neuro-endocrine tumors, other solid tumors, and neurology:

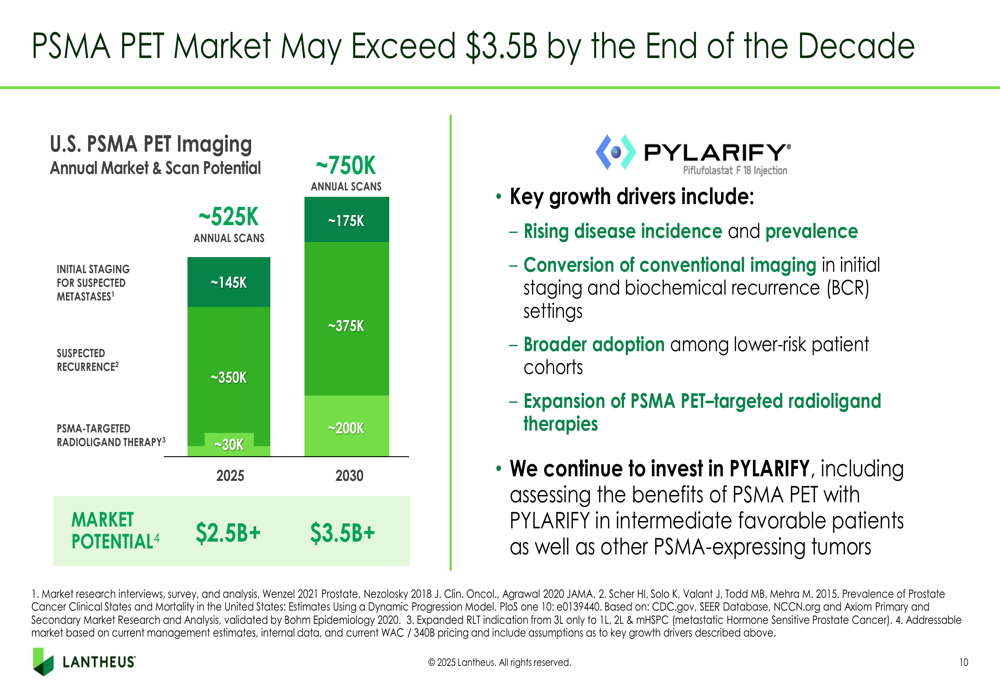

The company highlighted the significant market opportunity in PSMA PET imaging, projecting that the U.S. market potential may exceed $3.5 billion by the end of the decade:

Key growth drivers include rising disease incidence and prevalence, conversion from conventional imaging, broader adoption, and expansion of PSMA PET-targeted radioligand therapies.

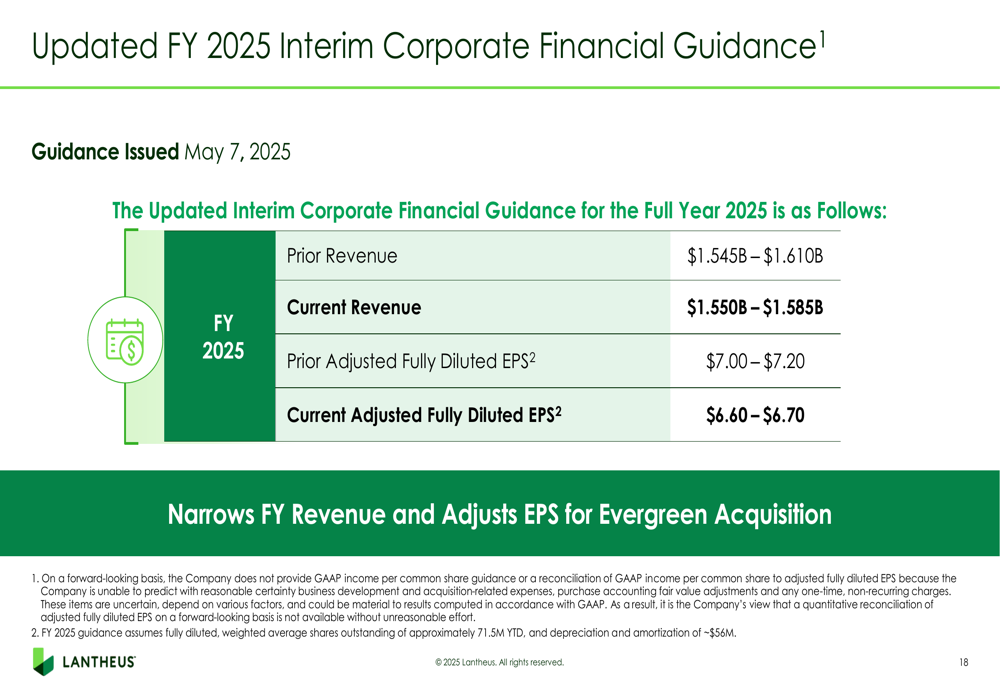

Financial Outlook & Guidance

Lantheus updated its financial guidance for full-year 2025, narrowing its revenue range and lowering its EPS expectations:

The company narrowed its revenue guidance to $1.550-$1.585 billion from the previous $1.545-$1.610 billion, while reducing adjusted EPS guidance to $6.60-$6.70 from $7.00-$7.20. Management attributed these changes to the impact of the Evergreen acquisition.

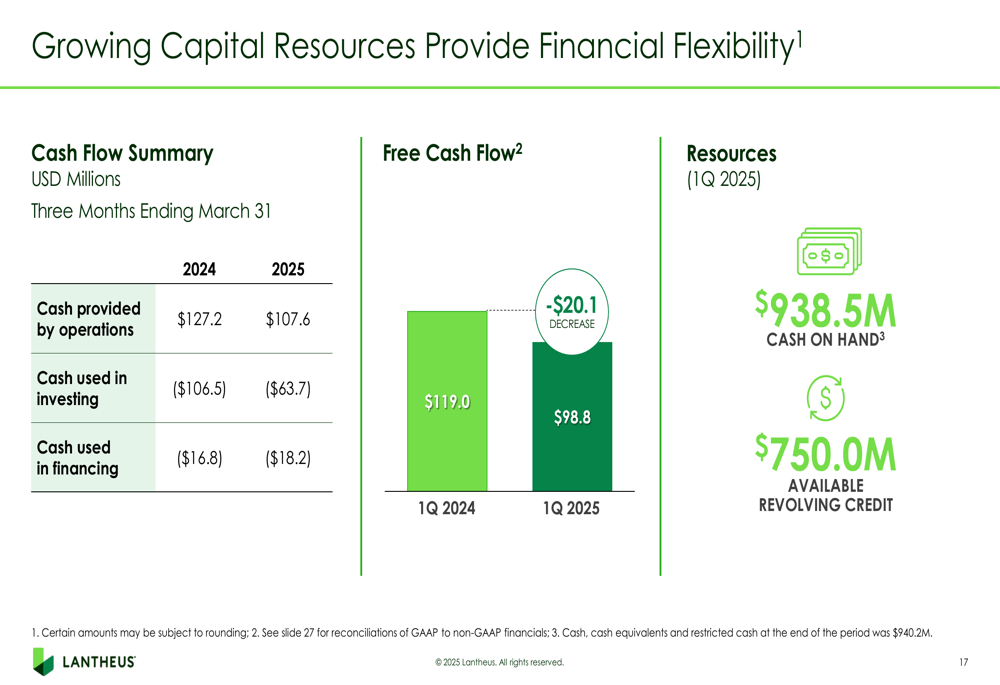

The company’s financial position remains strong, with $938.5 million in cash on hand and $750.0 million available under its revolving credit facility:

Free cash flow was $98.8 million in Q1 2025, down from $119.0 million in Q1 2024, reflecting the company’s increased investments in future growth.

Conclusion

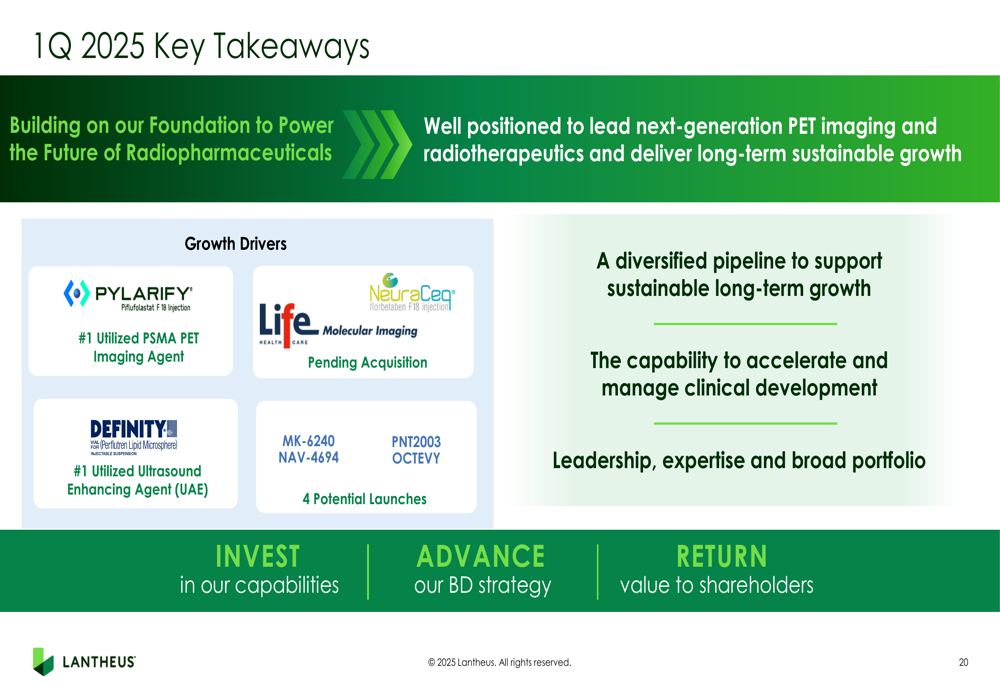

Lantheus’ Q1 2025 presentation reveals a company in transition, balancing near-term financial challenges with strategic investments for long-term growth. While revenue growth has slowed and profitability has declined, the company is actively reshaping its portfolio through acquisitions and pipeline development to position itself as a leader in the expanding radiopharmaceutical market.

The key takeaways from the presentation highlight this strategic focus:

Investors will likely be watching closely to see how quickly Lantheus can integrate its acquisitions and whether its pipeline can deliver the anticipated commercial launches between 2026-2027 to drive future growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.