US stock futures flounder amid tech weakness, Fed caution

Introduction & Market Context

LATAM Airlines Group SA ADR (NYSE:LTM) presented its second quarter 2025 results on July 29, showcasing record financial performance and strategic initiatives aimed at strengthening its market position. The stock responded positively in premarket trading, rising 2.1% to $42.25, as investors reacted to the company’s strong performance and improved outlook.

The South American carrier has demonstrated resilience and growth in a competitive airline industry, achieving recognition as the "Best Airline in South America" for the sixth consecutive year according to Skytrax 2025 awards.

Quarterly Performance Highlights

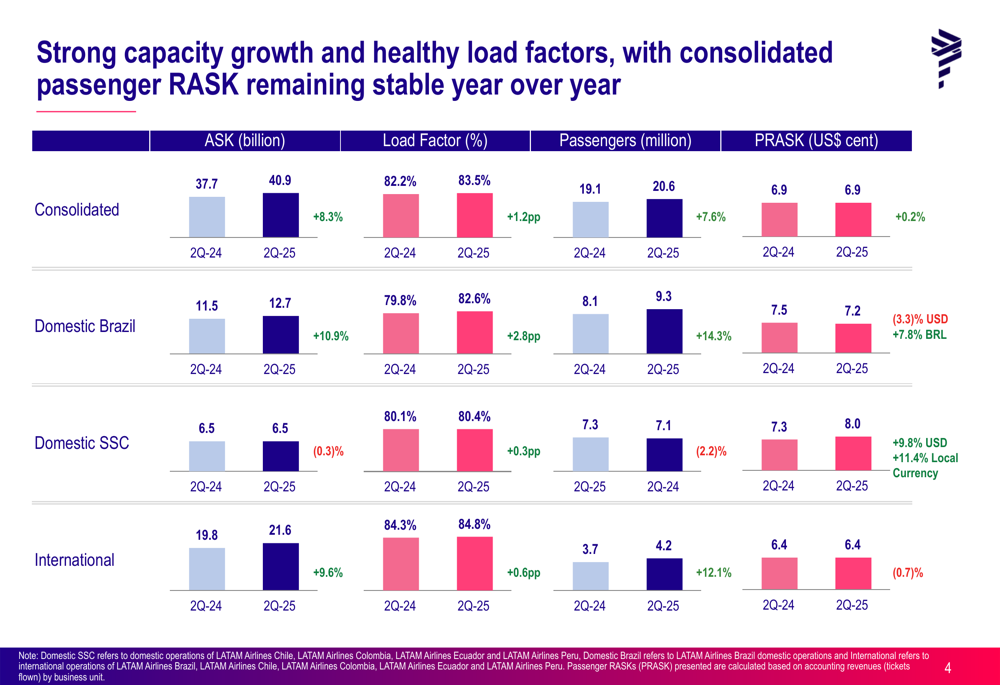

LATAM reported impressive operational metrics for Q2 2025, transporting over 20.5 million passengers with an 8.3% increase in capacity (ASK) year-over-year. The consolidated load factor reached 83.5%, representing a 1.2 percentage point improvement compared to the same period last year.

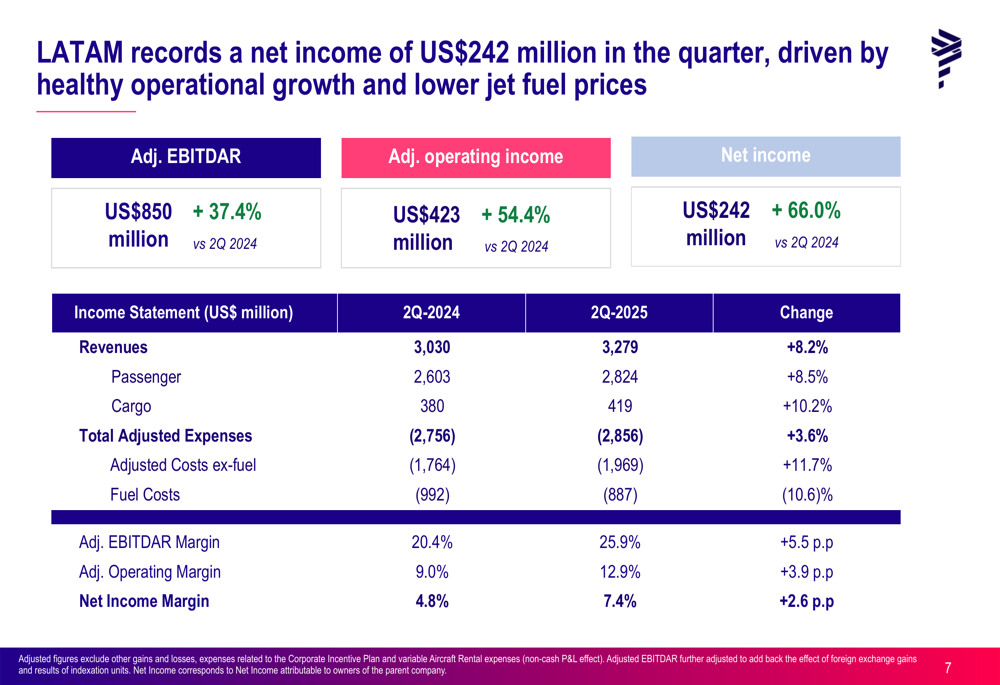

The company’s financial results were equally strong, with total operating revenues increasing 8.2% year-over-year to $3.28 billion. Passenger revenues grew by 8.5% to $2.82 billion, while cargo revenues increased by 10.2% to $419 million.

As shown in the following financial results summary, LATAM achieved significant improvements across all key metrics:

Most notably, adjusted EBITDAR reached $850 million, a 37.4% increase compared to Q2 2024, with a margin of 25.9% (up 5.5 percentage points). The company reported a record second quarter adjusted operating margin of 12.9%, up 3.9 percentage points year-over-year. Net income surged 66.0% to $242 million, representing a 7.4% margin.

Detailed Financial Analysis

LATAM’s operational performance varied across its different markets. The Domestic Brazil segment showed particularly strong results with a 10.9% capacity increase and a significant 2.8 percentage point improvement in load factor to 82.6%. This segment also saw a 14.3% increase in passengers carried.

The company’s international operations expanded capacity by 9.6% and improved load factor by 0.6 percentage points to 84.8%, while passenger numbers increased by 12.1%. The following chart illustrates these operational metrics across LATAM’s different market segments:

The airline has maintained disciplined cost management despite inflationary pressures. Adjusted CASK (Cost per Available Seat Kilometer) excluding fuel remained stable at 4.8 cents in Q2 2025, while Adjusted Passenger CASK excluding fuel was 4.3 cents.

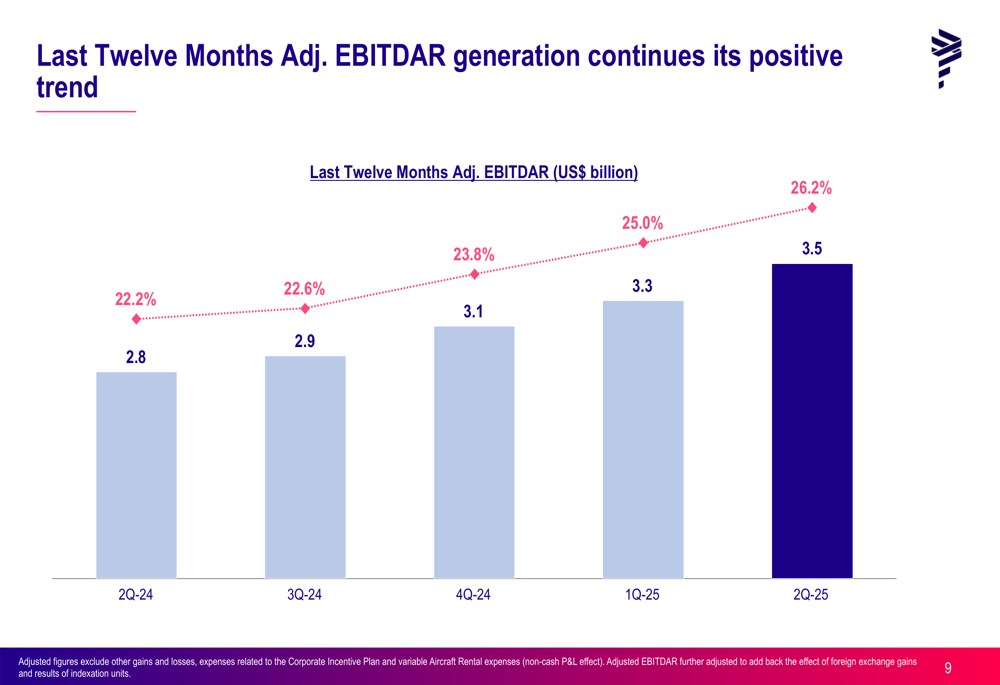

LATAM’s financial strength is evident in its consistently improving EBITDAR trend, which has shown steady growth over the past five quarters:

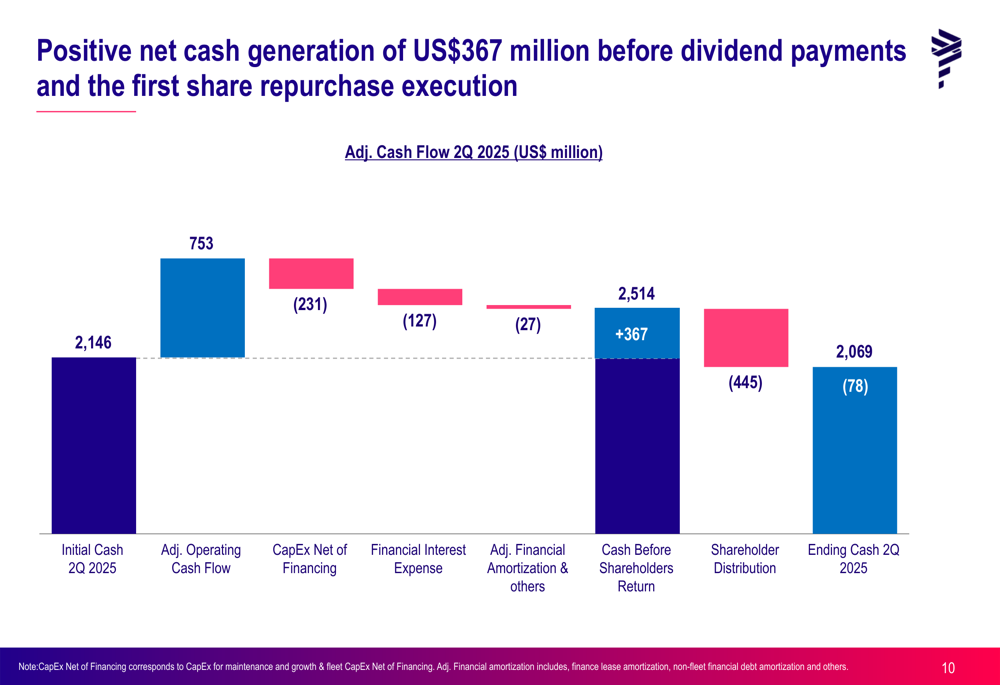

The company generated positive net cash of $367 million before dividend payments and share repurchases in Q2 2025. After distributing $445 million to shareholders, LATAM ended the quarter with a cash position of $2.07 billion.

Strategic Initiatives

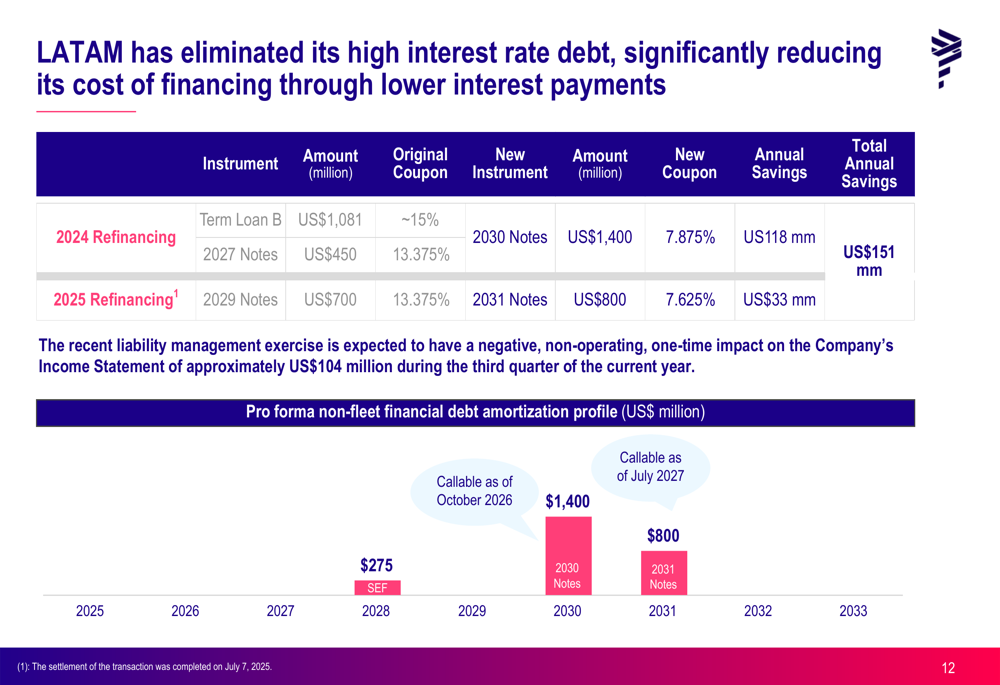

LATAM has implemented several strategic initiatives to enhance its competitive position and financial structure. A key achievement has been the successful refinancing of $800 million in high-interest debt, which has reduced interest costs by over 570 basis points and is expected to generate annual savings of $151 million.

The company’s debt refinancing strategy has significantly improved its financial profile, as illustrated in the following chart:

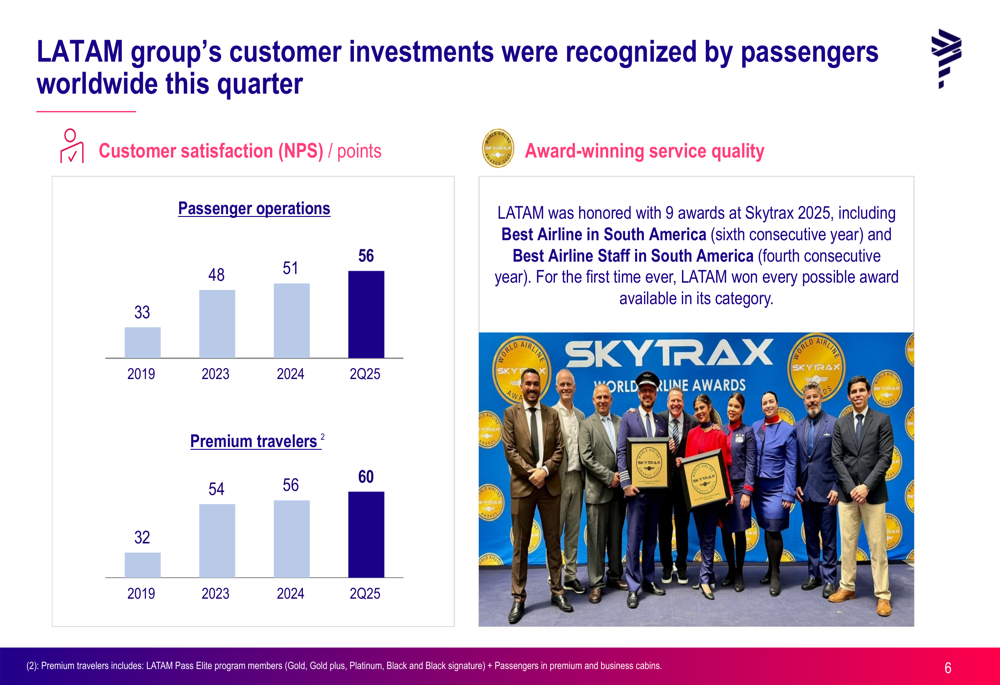

The airline has also focused on enhancing its premium travel experience through fleet modernization. Currently, 64% of LATAM’s wide-body fleet has been retrofitted with new Premium Business cabins, and approximately 90% of its narrow-body fleet offers onboard connectivity. These improvements have contributed to record customer satisfaction scores, with the Net Promoter Score (NPS) reaching 56 points in Q2 2025.

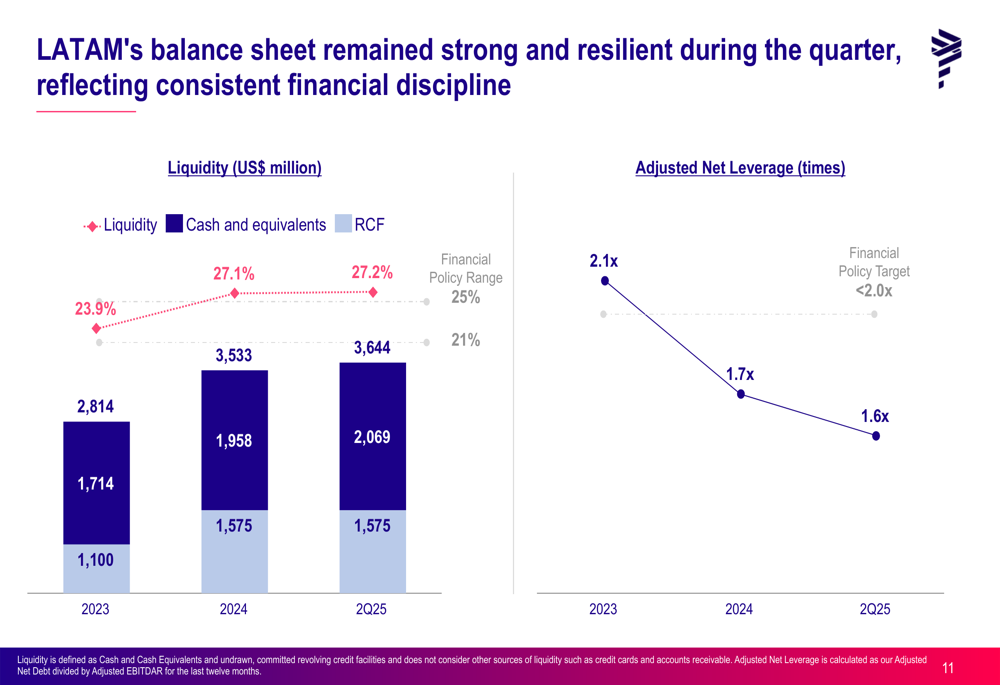

LATAM’s balance sheet has strengthened considerably, with liquidity of $3.64 billion (representing 27.2% of LTM revenue) and adjusted net leverage of 1.6x, down from 2.1x in 2023.

Forward-Looking Statements

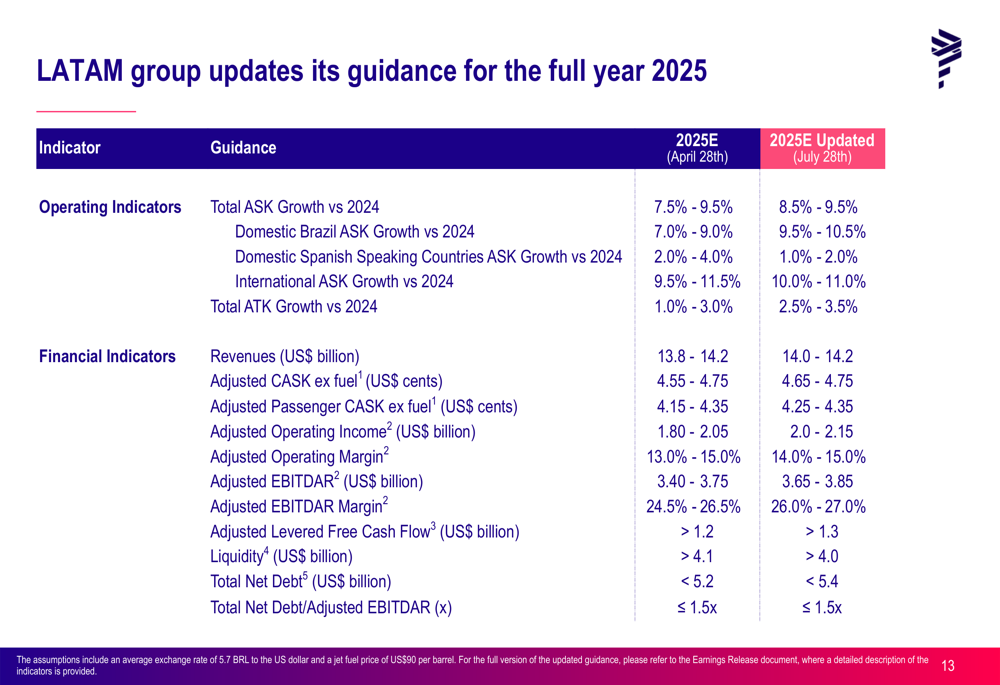

Based on its strong performance in the first half of the year, LATAM has updated its guidance for 2025. The company now expects total ASK growth between 8.5% and 9.5% compared to 2024, with revenues projected to reach between $14.0 and $14.2 billion.

Adjusted operating income is forecast to be between $2.0 and $2.15 billion, while adjusted EBITDAR is expected to range from $3.65 to $3.85 billion. The company anticipates adjusted levered free cash flow to exceed $1.3 billion, with liquidity remaining above $4.0 billion and total net debt below $5.4 billion.

LATAM’s fleet expansion plans remain on track, with 14 new aircraft delivered in the first half of 2025 and an additional 12 expected in the second half of the year. This fleet modernization supports the company’s growth strategy while improving operational efficiency.

The airline’s focus on shareholder returns continues, with a new share repurchase program approved for up to 3.4% of outstanding shares. Within this program, LATAM launched a share repurchase for up to 2.4% via a pro rata mechanism effective between July 1st and July 30th, 2025.

As LATAM continues to execute its strategic initiatives and capitalize on strong demand across its markets, the company appears well-positioned to maintain its leadership in South American aviation while delivering improved financial results and shareholder value.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.